Press release

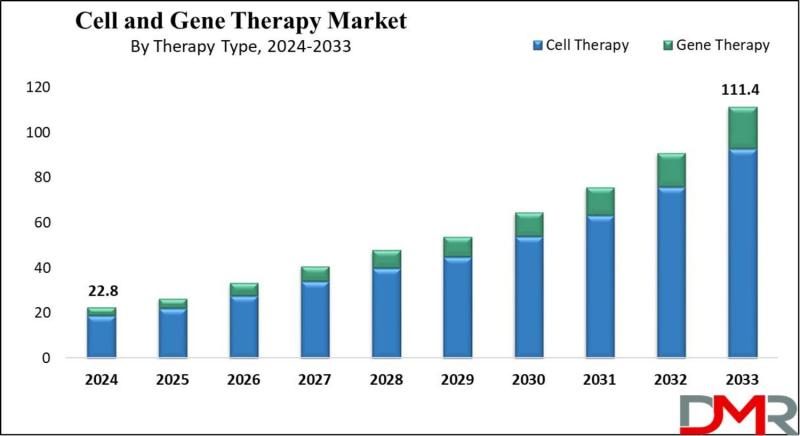

Cell and Gene Therapy Market to Surge from 22.8 billion in 2024 to 111.4 billion by 2033 as FDA Approvals and CRISPR Advancements Reshape Curative Medicine

Cell and Gene Therapy Market Size, Share, Trends & Outlook Report 2033

Cell and gene therapy-revolutionary approaches that modify or replace damaged genes and cells to treat, prevent, or potentially cure diseases-represent a paradigm shift from symptom management to curative treatment. According to Dimension Market Research, the U.S. market alone is projected to reach USD 10.2 billion in 2024 and grow to USD 46.8 billion by 2033 at a CAGR of 18.1% , driven by a strong research infrastructure, a high number of clinical trials, and favorable regulatory assistance from the FDA. With North America commanding 51.1% of global market revenue, the sector is witnessing a transformative era as gene-editing technologies and CAR-T therapies move from experimental to mainstream clinical application.

📄 Get Your Sample Report Today → https://dimensionmarketresearch.com/request-sample/cell-and-gene-therapy-market/

🔷 The News Angle: From Symptom Management to Curative Potential-The Gene Therapy Revolution

The dominant narrative reshaping the global cell and gene therapy market is the fundamental transition from managing chronic disease symptoms to potentially curing genetic disorders and cancers at their molecular roots-enabled by breakthrough technologies including CRISPR gene editing, CAR-T cell therapy, and advanced viral and non-viral delivery systems.

FDA approvals as accelerators are the most powerful catalyst. In December 2023, the U.S. FDA approved two landmark treatments, Casgevy and Lyfgenia, representing the first cell-based gene therapies for the treatment of sickle cell disease (SCD) in patients 12 years and older. Notably, Casgevy is the first FDA-approved treatment to use a type of novel genome editing technology (CRISPR), signaling an innovative advancement in the field of gene therapy. These approvals have validated the therapeutic potential of gene editing and opened the regulatory pathway for subsequent therapies targeting other genetic disorders.

CAR-T therapy as a cancer breakthrough is equally transformative. CAR-T therapy develops patient T-cells to find and remove cancer cells, demonstrating remarkable efficacy in treating leukemia and lymphoma. India launched its first home-grown gene therapy for cancer in April 2024-CAR-T cell therapy-at IIT Bombay, representing a major breakthrough in the battle against cancer. This line of treatment is accessible and less expensive, providing new hope for humankind. CAR-T cell therapy is considered one of the most exceptional developments in medical science and has been available in developed nations. The oncological disorders segment is set to capture the largest share of market revenue in 2024, driven by major R&D in cell and gene therapy targeting cancer at a genetic level.

Allogeneic "off-the-shelf" therapies represent the third pillar. Allogeneic cell therapies, derived from donor cells, are gaining traction as they provide the potential for "off-the-shelf" solutions, minimizing wait times and costs in comparison to autologous therapies (which require extracting, modifying, and re-infusing a patient's own cells). This approach is driving innovation in scalable, ready-to-use treatment options. In February 2024, BioNTech SE and Autolus Therapeutics plc announced a strategic collaboration focused on developing both companies' autologous CAR-T programs toward commercialization. In January 2024, AbbVie and Umoja Biopharma introduced exclusive options and license agreements to develop multiple in-situ generated CAR-T cell therapy candidates in oncology.

🔷 Key Insights: Data Points Defining the Cell and Gene Therapy Revolution

North America Leads (51.1% Share in 2024): Highest number of gene therapy clinical trials, over 400 active companies, favorable FDA regulatory approach, and advanced healthcare infrastructure drive regional dominance.

Cell Therapy Dominates Therapy Type Segment: Extensive potential in treating autoimmune diseases, various cancers, and urinary disorders; substantial funding for new cell line development; companies expanding manufacturing capabilities.

Oncological Disorders Lead Indication Segment: Major R&D in cell and gene therapy targeting cancer at genetic level; CAR-T therapy effectiveness in leukemia and lymphoma; personalized and potentially curative approach.

Hospitals Lead End-User Segment: Ability to provide access to advanced therapies; innovative treatments not available elsewhere; ability to manage complex administration and monitoring requirements.

FDA Breakthrough Approvals: Casgevy and Lyfgenia approved December 2023-first cell-based gene therapies for sickle cell disease; Casgevy is first FDA-approved treatment using CRISPR genome editing technology.

India's Entry: India launched first home-grown CAR-T cell therapy for cancer in April 2024 at IIT Bombay, providing accessible and less expensive treatment option.

Strategic Collaborations: BioNTech and Autolus collaboration for CAR-T commercialization (February 2024); AbbVie and Umoja collaboration for in-situ generated CAR-T therapies (January 2024).

Europe Initiatives: Horizon 2021 program focusing on gene therapy using viral vectors; new collaborative research initiatives boosting manufacturing services across Europe.

Genetic Disorders Fastest-Growing Indication: Growth in genetic and chronic diseases combined with government initiatives promoting public awareness about genetic testing and diagnosis.

In Vivo Therapy Significant Growth: Genetic material delivered directly to targeted cells while remaining in patient's body; correcting genetic defects or enhancing cellular functions.

📄 Get the Insights You Need to Drive Real Impact → https://dimensionmarketresearch.com/request-sample/cell-and-gene-therapy-market/

🔷 Market Dynamics: Drivers, Restraints, and Strategic Opportunities

Drivers: Technological Breakthroughs & Chronic Disease Prevalence

The primary driver is technological advancements and innovations in gene-editing technologies. Breakthroughs in CRISPR and other gene-editing platforms, combined with advances in viral and non-viral delivery systems, are accelerating the development of safer, more effective therapies. These innovations are reducing manufacturing complexity, improving targeting accuracy, and expanding the range of treatable conditions.

Simultaneously, the rising prevalence of chronic and genetic diseases drives adoption. The expanding incidence of cancer, rare genetic disorders, and age-related conditions creates an urgent need for innovative treatment options. Traditional therapies often manage symptoms without addressing root causes. Cell and gene therapies offer the potential for durable, potentially curative outcomes, making them increasingly attractive to patients, providers, and payers.

Restraints: High Costs & Logistical Challenges

Despite momentum, significant barriers remain. High development and treatment costs represent a major restraint. Complex manufacturing processes and regulatory requirements lead to substantial R&D expenditures. Treatments including CAR-T therapies are expensive-often hundreds of thousands of dollars per patient-limiting accessibility and reimbursement options. The need for specialized manufacturing facilities and skilled personnel further escalates costs.

Additionally, regulatory and logistical challenges restrain market expansion. Navigating strict regulatory approvals for novel therapies is time-consuming and uncertain. Ensuring robust supply chains for living cell products with strict temperature and handling requirements creates major hurdles. The complexity of manufacturing autologous therapies (patient-specific) limits scalability. Delays in commercialization and market entry are common.

Opportunities: Emerging Markets & Personalized Medicine Expansion

The Asia-Pacific region provides new opportunities for market players to expand clinical trials and commercialization efforts. Increased healthcare infrastructure investment and government initiatives supporting advanced therapies are accelerating market entry. India's successful launch of affordable CAR-T therapy demonstrates the potential for cost-effective manufacturing and distribution models in emerging economies.

The growing focus on customized therapies opens doors for targeted treatments, including patient-specific CAR-T therapies. Advances in genomics, biomarker identification, and AI-driven patient selection enable more effective patient stratification. Personalized approaches improve clinical outcomes, reduce adverse events, and enhance the value proposition for payers. The shift toward precision medicine fosters market growth as therapies become more targeted and effective.

🔷 Selective Segmentation: Where the Growth is Concentrated

By Therapy Type (Cell Therapy-Dominant Share): Cell therapy accounts for the largest share of market revenue, driven by extensive potential in treating autoimmune diseases, various cancers, and urinary disorders. Substantial funding directed toward development of new cell lines and companies adopting organic and inorganic strategies to expand manufacturing capabilities support growth. Cell therapy involves introducing healthy, modified cells into the body to replace diseased or damaged ones, focusing on improving patient health by restoring normal cellular function or eliminating disease. Gene Therapy maintains the second-largest share, aiming to alter genetic makeup of cells to treat or reverse diseases by repairing damaged genetic material, addressing root causes of genetic disorders and providing potential cures rather than symptom management.

By Indication (Oncological Disorders-Leading Share): Oncological disorders capture the largest share of market revenue, driven by major R&D in cell and gene therapy targeting cancer at a genetic level. CAR-T therapy has demonstrated remarkable efficacy in treating leukemia and lymphoma. These therapies focus on targeting cancer at a genetic level, providing hope for more effective and customized treatment options. Major pharmaceutical companies including Novartis, Bristol-Myers Squibb, and Pfizer have active oncology cell and gene therapy pipelines. Genetic Disorders are the fastest-growing indication, due to growth in genetic and chronic diseases combined with government initiatives promoting public awareness about genetic testing and diagnosis.

By Delivery Method (In Vivo-Significant Growth): In vivo therapy is expected to experience significant growth, with genetic material delivered directly to targeted cells while they remain in the patient's body. This approach eliminates the need for cell extraction, modification, and re-infusion, potentially reducing costs and treatment timelines. In vivo approaches are particularly promising for genetic disorders affecting solid organs including liver, muscle, and central nervous system. Ex Vivo therapy involves extracting cells from the patient, treating them with genetic transformation outside the body, and reintroducing them-allowing careful alteration of genes before cells are returned, ensuring a more controlled approach.

By End-User (Hospitals-Dominant Share): Hospitals exhibit the highest growth along with the majority share throughout the forecast period, owing to hospitals' ability to provide access to advanced therapies, allowing patients to receive innovative treatments not available elsewhere. Hospitals have specialized infrastructure for cell collection, processing, and administration. The complexity of CAR-T therapy administration-requiring apheresis, cell processing, lymphodepletion, and infusion-is well-suited to hospital settings with multidisciplinary care teams. Cancer Care Centers are also set to experience significant growth, leading in research and treatment for cancer, often implementing advanced therapies customized to battle various types of cancer.

🔷 Regional Analysis: North America Leads, Asia-Pacific Emerges as Fastest-Growing

North America (51.1% Revenue Share in 2024): North America holds a major share of the cell and gene therapy market, leading the way with the highest number of gene therapy clinical trials and supporting over 400 companies actively engaged in developing cell and gene therapy products for many medical conditions. Growth is largely driven by developments in healthcare infrastructure, a major number of ongoing clinical trials, and better involvement from firms in gene and cell therapy development. The favorable regulatory landscape, mainly in the U.S., has played a vital role, with the FDA implementing a collaborative regulatory approach that provides direct and consistent support for these innovative therapies. The December 2023 approvals of Casgevy and Lyfgenia for sickle cell disease-including the first FDA-approved CRISPR-based therapy-exemplify this supportive environment.

The U.S. Market (USD 10.2 billion in 2024, 18.1% CAGR): The U.S. provides numerous growth opportunities through its strong research infrastructure, high number of clinical trials, and favorable regulatory assistance from the FDA. Large investments, partnerships, and development in manufacturing technologies further drive market expansion. Growth in demand for customized medicine and therapies targeting cancer and genetic disorders fuels growth opportunities. A strong research ecosystem with significant clinical trials and the FDA helps accelerate innovation. However, high development and treatment costs remain major restraints, limiting patient access and insurance coverage. Overcoming manufacturing challenges and ensuring affordable therapies, especially in complex stem cell therapy procedures, are vital to unlocking the market's full potential.

Europe: Europe is seeing various new collaborative research and innovation initiatives emerging under the Horizon 2021 program, focusing on gene therapy using viral vectors. These initiatives are anticipated to boost the growth of cell and gene therapy manufacturing services throughout Europe, further assisted by the region's developed infrastructure and skilled workforce, which are important for developing research and clinical applications. The UK, Germany, France, and Switzerland are leading European hubs for cell and gene therapy development.

Asia-Pacific (Fastest-Growing Region): Asia-Pacific is emerging as the fastest-growing region, driven by increased healthcare infrastructure investment and government initiatives supporting advanced therapies. India launched its first home-grown CAR-T cell therapy in April 2024, demonstrating the potential for cost-effective manufacturing and distribution models in emerging economies. China, Japan, and South Korea are also expanding cell and gene therapy research and manufacturing capabilities. The region's large patient populations and growing middle-class healthcare spending create significant commercial opportunities.

📄 Get the Full Premium Report Now- https://dimensionmarketresearch.com/checkout/cell-and-gene-therapy-market/

🔷 Competitive Landscape: Global Pharma Leaders, Biotech Innovators, and CRO Partners

The competitive landscape of the cell and gene therapy market is rapidly transforming, with established pharmaceutical players and emerging biotech companies driving innovation.

Global Pharmaceutical Leaders: Novartis, Pfizer, Bristol-Myers Squibb Company, Amgen, Biogen, Sanofi, and AstraZeneca dominate with significant R&D investments, rich clinical pipelines, and global commercial infrastructure. BioNTech SE and Autolus Therapeutics plc announced a strategic collaboration (February 2024) focused on developing both companies' autologous CAR-T programs toward commercialization. AstraZeneca unveiled a collaboration and investment agreement with Cellectis (November 2023) to expand development of next-generation therapeutics in immunology, oncology, and rare diseases.

Cell and Gene Therapy Specialists: Kolon TissueGene Inc, JCR Pharmaceuticals, and Alnylam Pharmaceuticals focus exclusively on cell and gene therapies for specific indications. AbbVie and Umoja Biopharma introduced exclusive options and license agreements (January 2024) to develop multiple in-situ generated CAR-T cell therapy candidates in oncology utilizing Umoja's proprietary VivoVec platform.

Manufacturing and Technology Partners: Thermo Fisher Scientific provides critical manufacturing and research support services essential for cell and gene therapy production.

Recent Developments Highlighting Market Momentum:

April 2024: India launched its first home-grown CAR-T cell therapy for cancer at IIT Bombay-accessible and less expensive treatment.

February 2024: BioNTech SE and Autolus Therapeutics plc announced strategic collaboration to develop autologous CAR-T programs toward commercialization.

January 2024: AbbVie and Umoja Biopharma introduced exclusive options and license agreements for in-situ generated CAR-T cell therapy candidates.

December 2023: U.S. FDA approved Casgevy and Lyfgenia-first cell-based gene therapies for sickle cell disease; Casgevy is first FDA-approved CRISPR-based therapy.

November 2023: AstraZeneca unveiled collaboration and investment agreement with Cellectis to develop next-generation therapeutics.

🔷 The Road Ahead: What Decision-Makers Need to Know

For B2B decision-makers-pharmaceutical R&D executives, biotech investors, hospital administrators, and healthcare policymakers-the strategic imperative is clear: cell and gene therapy has moved from experimental concept to clinical reality. The 19.3% CAGR reflects sustained demand driven by FDA approvals, CRISPR advancements, and the fundamental shift toward curative treatments for previously intractable diseases.

Key strategic imperatives include:

Prioritize CAR-T and allogeneic "off-the-shelf" therapy development. Autologous CAR-T therapies have demonstrated remarkable efficacy, but manufacturing complexity limits scalability. Allogeneic approaches offer "off-the-shelf" solutions with reduced wait times and costs.

Invest in CRISPR and advanced gene-editing platforms. The first FDA-approved CRISPR therapy (Casgevy, December 2023) validates the platform. Companies with proprietary gene-editing technologies and delivery systems will capture significant value.

Expand manufacturing capabilities for viral vectors and cell processing. Manufacturing remains the critical bottleneck. Investment in scalable, cost-effective production platforms-including automated cell processing and closed systems-is essential.

Target oncological disorders while building rare disease pipelines. Oncology is the largest indication segment, but genetic disorders are the fastest-growing. Diversified pipelines balance near-term revenue and long-term growth.

Expand into emerging markets with cost-effective manufacturing models. India's affordable CAR-T therapy demonstrates the potential for lower-cost production serving large patient populations. Strategic partnerships with local manufacturers and research institutions will accelerate market entry.

The full report from Dimension Market Research provides granular segmentation by therapy type (cell therapy-stem cells, T cells, dendritic cells, NK cells, tumor cells-gene therapy), indication (genetic disorders, cardiovascular disorders, neurological disorders, oncological disorders), delivery method (in vivo, ex vivo), end-user (hospitals, academic & research centers, cancer care centers), and 20+ regional markets, offering actionable intelligence for strategic planning.

📄 Explore the Report with TOC → https://dimensionmarketresearch.com/report/cell-and-gene-therapy-market/

For Sales or Inquiries, Contact

Robert John

957 Route 33, Suite 12 #308 Hamilton Square, NJ-08690 USA

Email: enquiry@dimensionmarketresearch.com

United States: (+1 732 369 9777)

Tel No: +91 88267 74855

Dimension Market Research (DMR) is a market research and consulting firm based in India & US, with its headquarters located in the USA. The company believes in providing the best and most valuable data to its customers using the best resources and analysts to work on, to create unmatchable insights into the industries and markets while offering in-depth results of over 30 industries, and all major regions across the world. We also believe that our clients don't always want what they see, so we provide customized reports as well, as per their specific requirements, to create the best possible outcomes for them and enhance their business through our data and insights in every possible way.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Cell and Gene Therapy Market to Surge from 22.8 billion in 2024 to 111.4 billion by 2033 as FDA Approvals and CRISPR Advancements Reshape Curative Medicine here

News-ID: 4513085 • Views: …

More Releases from Dimension Market Research

Kingdom of Saudi Arabia Elderly Healthcare Market to Reach $44,542.4 million by …

The Kingdom of Saudi Arabia (KSA) Elderly Healthcare Market is poised for explosive growth, with market valuation projected to surge from an estimated USD 1,012.6 million in 2024 to USD 4,542.4 million by 2033, registering a remarkable compound annual growth rate (CAGR) of 18.1%. According to Dimension Market Research, this extraordinary expansion is being driven by three converging forces: the rapidly aging Saudi population (over 11% expected to be above…

Radiopharmaceuticals Market to Reach $9,876.2 million by 2033 as Theranostics an …

The global Radiopharmaceuticals Market is on a steady growth trajectory, with market valuation projected to rise from an estimated USD 7,225.6 million in 2024 to USD 9,876.2 million by 2033, registering a compound annual growth rate (CAGR) of 3.5%. According to Dimension Market Research, this expansion is being driven by three converging forces: increasing global prevalence of chronic diseases including cancer and cardiovascular disorders, the rise of theranostics-combining diagnostic and…

Drug Discovery Market to Reach $138.5 Billion by 2033 as AI-Powered Screening an …

The global Drug Discovery Market is poised for substantial growth, with market valuation projected to rise from an estimated USD 60.9 billion in 2024 to USD 138.5 billion by 2033, registering a strong compound annual growth rate (CAGR) of 9.6%. According to Dimension Market Research, this expansion is being driven by four converging forces: the rising demand for novel therapeutics addressing chronic diseases, the integration of artificial intelligence and machine…

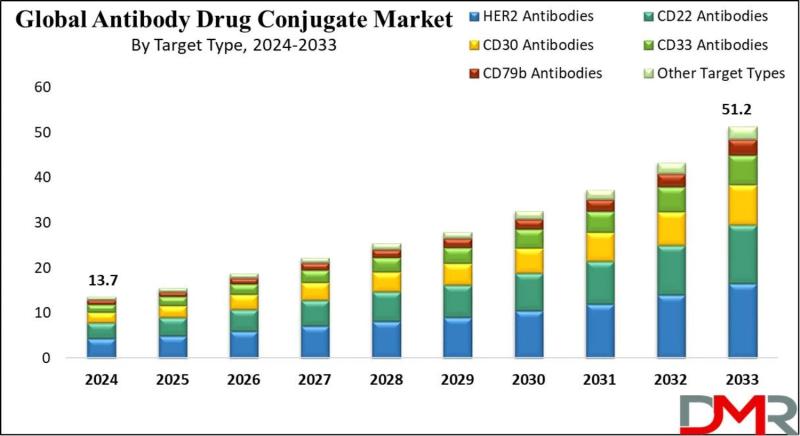

Antibody Drug Conjugates Market to Nearly Quadruple to $51.2 Billion by 2033 as …

According to Dimension Market Research, the Global Antibody Drug Conjugates (ADC) Market is poised for explosive exponential growth, projected to surge from USD 13.7 billion in 2024 to a staggering USD 51.2 billion by 2033, registering a remarkable compound annual growth rate (CAGR) of 15.8%. This growth reflects the accelerating clinical and commercial validation of ADCs as one of the most promising therapeutic modalities in modern oncology.

Antibody drug conjugates-often described…

More Releases for FDA

FDA vs Non-FDA Freeze-Dried Fruit Suppliers: Risk and Market Access Differences

FDA Freeze-Dried Fruit Suppliers vs Non-FDA Approved Producers: Risk and Market Access Differences

Fujian Lixing Food Co., Ltd. - an internationally acclaimed provider of FDA freeze dried fruits and a pioneer in vacuum sublimation technology - today provided an insightful analysis that illuminated critical differences between FDA-registered suppliers and non-approved producers; with rising consumer demand for "clean label" healthy snacks a must, this study illustrates why regulatory compliance must be adhered…

DreaMed receives 5th FDA Clearance

TEL AVIV, Israel: DreaMed Diabetes LTD. ("DreaMed" or the "Company"), developer of the endo.digital Clinical Decision Support System announced today that it has received its 5th U.S Food and Drug Administration (FDA) clearance that expands the scope of AI enhanced treatment recommendations to patients on fixed meal insulin regimens. endo.digital is the first decision support system that has been cleared to assist healthcare providers in the management of diabetes…

FDA Compliant Blood Storage and Preservation

Accsense Monitoring System Automates Data Archive and Alarming

CAS DataLoggers provided the temperature alarming and monitoring system to a hospital blood bank looking to replace their old paper chart recorders as they became unreliable and spare parts were harder to find. For proper blood storage and preservation, the lab’s medical units needed to maintain storage temperatures between 2°C to 6°C (36°F to 43°F), given the perishability of blood components. The facility…

New FDA Design Control Training Courses

Salt Lake City, Utah - February 23 2017 - Procenius Consulting is a medical device consulting firm specializing solely in medical device design controls regulation (21 CFR 820.30).

Announcing New Design Control Training Courses

Procenius Consulting has just launched two new training courses covering basic and advanced topics of medical device design control regulation. These courses focus on compliance, practical implementation and industry best practices techniques for developing or improving a…

fda online training

GRC Training Solutions provides end-to-end FDA compliance solutions for those companies who want to maximize security, minimize operational costs, improve staff productivity and stay on top of all their compliance documentation.

GRC Training Solutions boasts a team of experts and specialists who have a proven track record in working with the biotechnology, medical device, diagnostic and pharmaceutical fields. Our team will work with you closely and develop solutions that meet…

FDA online training

Description:

Device firms, establishments or facilities that are involved in the production and distribution of medical devices intended for use in the U.S are required to register annually. Most establishments that are required to register with the FDA are also required to list the devices that are made there and the activities that are performed on those devices. Initially, FDA issued a 28-page Proposed Rule that would amend its regulations regarding…