Press release

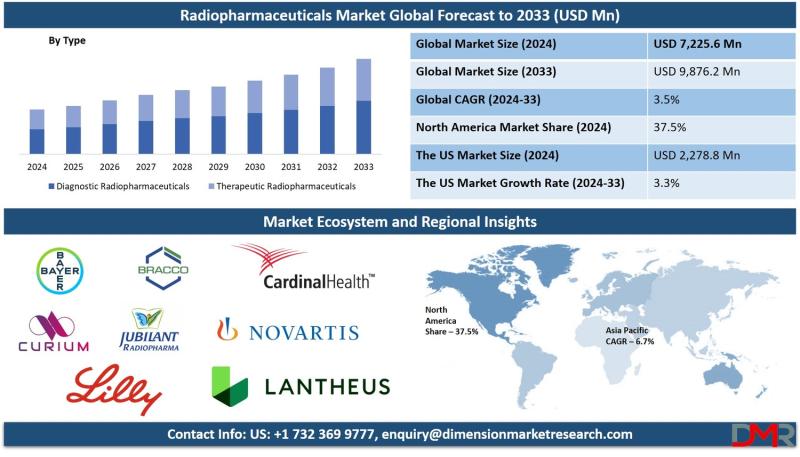

Radiopharmaceuticals Market to Reach $9,876.2 million by 2033 as Theranostics and PET Imaging Drive Precision Cancer Care

Radiopharmaceuticals Market Size, Share, Trends & Outlook Report 2034

Radiopharmaceuticals-radioactive compounds used for both diagnostic imaging and targeted therapy-have become indispensable in modern healthcare, enabling non-invasive visualization of internal organs and precise treatment of malignant tumors. According to Dimension Market Research, the U.S. market alone is projected to reach USD 2,278.8 million in 2024 and grow to USD 3,049.4 million by 2033 at a CAGR of 3.3% , driven by high chronic disease incidence, advanced nuclear medicine infrastructure, and significant R&D investments. With North America commanding 37.5% of global market revenue, the sector is witnessing steady growth as healthcare systems increasingly adopt nuclear medicine for early disease detection and targeted therapy.

📄 Get Your Sample Report Today → https://dimensionmarketresearch.com/request-sample/radiopharmaceuticals-market/

🔷 The News Angle: From Diagnostic Imaging to Theranostic Precision-The Radiopharmaceutical Evolution

The dominant narrative reshaping the global radiopharmaceuticals market is the fundamental transition from standalone diagnostic imaging agents to theranostic platforms that combine diagnosis and therapy into a single, personalized treatment approach-enabling physicians to see, target, and treat diseases with unprecedented precision.

The rise of theranostics is the most powerful catalyst. Theranostics-the convergence of diagnostic and therapeutic devices-enables individual changes in treatment plans even though the same radiopharmaceutical is used for both diagnosis and therapy of diseases such as cancer. Lutetium-177 works for both imaging of prostate cancer tumors and treatment of them. The concept of theranostics is growing rapidly since it opens opportunities for more personalized, less toxic treatment of cancers, generating demand for new theranostic radiopharmaceuticals worldwide. This approach is transforming cancer care, with therapeutic radiopharmaceuticals including Lu-177 and I-131 treating prostate cancer and thyroid cancer, respectively, with significantly fewer side effects compared to conventional therapies.

Oncology as the primary driver is equally transformative. The application segment continues to be dominated by oncology, accounting for 31.5% market share in 2024, driven by high demand for diagnostic imaging and therapeutic intervention in cancer care. The global burden of cancer has increased tremendously over recent decades, with millions of new cases diagnosed every year, creating an emerging need for state-of-the-art imaging technologies including PET and SPECT for early detection and tumor monitoring. Fluorine-18 (FDG), the main radiopharmaceutical used in PET scans, plays a great role in monitoring metabolic activity in cancerous cells, making it of immense importance in diagnosis, staging, and treatment planning.

Diagnostic radiopharmaceuticals maintaining leadership represents the third pillar. Diagnostic radiopharmaceuticals dominate the type segment with 63.1% market share in 2024, due to wide applications in nuclear medicine imaging techniques including PET and SPECT scans. These radiopharmaceuticals have important applications in diagnosing cancers, cardiovascular conditions, and neurological disorders, visualizing internal organ functions and abnormalities. Growing worldwide prevalence of chronic diseases requiring early diagnosis and monitoring by advanced diagnostic techniques has made this a major driver for diagnostic radiopharmaceutical demand. Technetium-99m and Fluorine-18 view internal metabolic and physiological processes in real-time, with non-invasive diagnostic modalities making these radiopharmaceuticals a must for clinical use.

🔷 Key Insights: Data Points Defining the Radiopharmaceuticals Market

North America Leads (37.5% Share in 2024): Superior healthcare facilities, enhanced utilization of nuclear medicine, strong R&D centers, high chronic disease prevalence, and FDA support for new molecular agents drive regional dominance.

Diagnostic Radiopharmaceuticals Dominate Type Segment (63.1% Share): Wide applications in PET and SPECT scans, growing chronic disease prevalence requiring early diagnosis, and shift toward non-invasive diagnostic procedures drive dominance.

Oncology Leads Application Segment (31.5% Share): High demand for diagnostic imaging and therapeutic intervention in cancer care; millions of new cancer cases annually drive need for PET and SPECT technologies.

Fluorine-18 Derivatives Lead Radioisotope Segment: Used in PET for tumor diagnostics and neurological studies; short half-life (110 minutes) suitable for clinical imaging; high-resolution images enable early cancer detection.

Cyclotrons Lead Source Segment: Primary technology for producing short-life radioisotopes for PET imaging; enable on-site manufacturing; reduce transportation issues; produce Gallium-68, Carbon-11, and Nitrogen-13.

Hospitals Lead End-User Segment: Primary end-users for advanced diagnostic and therapeutic procedures; specialized equipment and professionals; complex therapeutic cases requiring special care and monitoring.

Therapeutic Radiopharmaceuticals Fastest-Growing: Lutetium-177 and Yttrium-90 in targeted cancer therapy; theranostics approach gaining momentum.

U.S. Market Strength: Location of origin for developing new nuclear medicine technologies in PET and SPECT modalities; increasing budget for cancer-related research and growing number of clinical trials for new radiopharmaceuticals.

Government Initiatives: Major funding for nuclear medicine in North American and European countries; faster clearance for new radiopharmaceuticals.

📄 Get the Insights You Need to Drive Real Impact → https://dimensionmarketresearch.com/request-sample/radiopharmaceuticals-market/

🔷 Market Dynamics: Drivers, Restraints, and Strategic Opportunities

Drivers: Chronic Disease Prevalence & Government Investments

The primary driver is the increasing prevalence of chronic diseases worldwide. Global incidence of cancer, cardiovascular diseases, and neurological disorders is a major growth factor for the radiopharmaceutical market. These conditions require high-precision diagnosis and reliable treatment, both made available by radiopharmaceuticals. Rising cancer incidences are driving PET and SPECT market demand where Fluorine-18 and Technetium-99m are key radiopharmaceuticals.

Simultaneously, government initiatives and investments are driving market expansion. Major funding is being made by governments across the globe by investing in nuclear medicine and healthcare systems, mainly in North American and European countries. Governments are offering faster clearance for new radiopharmaceuticals, and healthcare systems worldwide increasingly incorporate nuclear medicine services. Favorable measures accompanying enhanced investments in R&D of nuclear medicine applications are primarily boosting market growth.

Restraints: High Costs & Stringent Regulations

Despite momentum, significant barriers remain. High cost of radiopharmaceuticals represents a major restraint. Radioisotope production is an expensive process involving technologies including cyclotrons and nuclear reactors, making radiopharmaceuticals expensive. Specialized healthcare facilities and legal requirements increase costs, reducing feasibility and availability, especially in low- and middle-income countries.

Additionally, stringent regulatory requirements restrain market growth. Radiopharmaceuticals involve strict regulatory rules because of radioactive elements. Observing these regulations can be difficult due to high safety measures and strict quality standards. Getting regulatory clearances from authorities including the FDA and EMA may take time, meaning organizations may take longer to introduce new products to market-a factor limiting growth.

Opportunities: Emerging Markets & Therapeutic Expansion

The Asia-Pacific region presents the most promising opportunity for the radiopharmaceutical market due to constantly developing healthcare sectors and increasing demand for nuclear medicines. Nuclear medicine facilities are being developed in countries including India and China, with more diagnostic and therapeutic services being added. Growing rates of chronic diseases in these areas are fueling market growth, presenting opportunities for international players looking to enter the market.

Chronic disease management through therapeutic radiopharmaceuticals shifting from diagnostic applications offers new growth prospects. Lutetium-177 and Yttrium-90 in cancer management through targeted therapy represent a new frontier in cancer treatment with minimal side effects and invasiveness. As the shift toward therapeutic applications continues, new radiopharmaceuticals are predicted to appear in the market, driving growth of the therapeutic segment.

🔷 Selective Segmentation: Where the Growth is Concentrated

By Radioisotope (Fluorine-18 Derivatives-Dominant Share): Fluorine-18 derivatives dominate due to their use in PET for tumor diagnostics and neurological studies. Fluorine-18 is the officially and commonly used isotope during PET scans, with F-18 fluorodeoxyglucose detecting metabolic activity within malignant cells. Its short half-life of 110 minutes is suitable for clinical imaging studies, enabling completion of imaging studies in relatively short time to minimize radiation exposure. High-resolution images assist in early detection of cancer and several other diseases, improving disease outcomes. These radiopharmaceuticals find application in neurological symptoms including Alzheimer's disease and cardiology. Technetium-99 and Lutetium-177 represent significant secondary radioisotope segments.

By Type (Diagnostic Radiopharmaceuticals-63.1% Share): Diagnostic radiopharmaceuticals dominate due to wide applications in nuclear medicine imaging techniques including PET and SPECT scans. These radiopharmaceuticals have important applications in diagnosing cancers, cardiovascular conditions, and neurological disorders, visualizing internal organs and abnormalities. Growing worldwide prevalence of chronic diseases requiring early diagnosis and monitoring by advanced diagnostic techniques drives demand. Non-invasive diagnostic modalities make these radiopharmaceuticals a must for clinical use, especially in oncology and cardiology. Therapeutic Radiopharmaceuticals (alpha emitters, beta emitters including Lutetium-177) represent the fastest-growing segment due to theranostics adoption.

By Source (Cyclotrons-Dominant Share): Cyclotrons dominate as the primary technology for producing short-life radioisotopes, especially for PET imaging including Fluorine-18. Installation of cyclotrons in hospitals enables on-site manufacturing of life-critical radiopharmaceutical products with extremely short half-lives, reducing transportation issues and ensuring on-time product availability for diagnosis. Cyclotrons produce a wide range of radioisotopes including Gallium-68, Carbon-11, and Nitrogen-13 required in various PET scans for oncology, cardiology, and neurology. Flexibility and efficiency in producing radioisotopes make them irreplaceable in nuclear medicine. Nuclear Reactors and Generators represent significant secondary source segments.

By Application (Oncology-31.5% Share): Oncology dominates the application segment due to high demand for diagnostic imaging and therapeutic intervention in cancer care. The global burden of cancer has increased tremendously, with millions of new cases diagnosed every year, creating an emerging need for state-of-the-art imaging technologies including PET and SPECT for early detection and tumor monitoring. Fluorine-18 (FDG) plays a great role in monitoring metabolic activity in cancerous cells, making it of immense importance in diagnosis, staging, and treatment planning. The trend toward theranostics-integrating diagnostic and therapeutic use in single radiopharmaceuticals-has changed cancer care. Cardiology, Neurology, and Endocrinology represent significant secondary application segments.

By End-User (Hospitals-Dominant Share): Hospitals dominate as primary end-users of radiopharmaceuticals for advanced diagnostic and therapeutic procedures. Radiopharmaceuticals remain important in nuclear medicine departments for PET and SPECT scans crucial for diagnosing cancer, cardiovascular diseases, and neurological conditions. Hospitals have specialized equipment and professionals specialized in handling such equipment. Complex cases involving therapeutic radiopharmaceuticals including Iodine-131 for thyroid cancer and Lutetium-177 for advanced prostate cancer require special care, monitoring, and regulatory protocols for dealing with radioactive drugs-provided only in hospital settings. Medical Imaging Centers and Cancer Research Institutes represent significant secondary end-user segments.

🔷 Regional Analysis: North America Leads, Asia-Pacific Emerges as Fastest-Growing

North America (37.5% Revenue Share in 2024): North America holds the major market share of the global radiopharmaceuticals market due to superior healthcare facilities and enhanced utilization of nuclear medicine products. The region's dominance is driven by the tremendous market for diagnostic and therapeutic applications of radiopharmaceuticals, especially in the United States where there are ample R&D centers for nuclear medicine applications. Chronic diseases including cancers, cardiovascular disorders, and neurological disorders have become more common in North America, implying the need for state-of-the-art diagnostic imaging and treatment solutions. Radiopharmaceuticals used in PET and SPECT scans to diagnose fresh cases of cancer and other chronic diseases are key reasons for the region's market share. Governments and private investors have invested heavily in research and production. The FDA is advancing support of new molecular agents, creating positive conditions for introduction and market expansion. Major market players including GE Healthcare, Cardinal Health, and Lantheus Holdings strengthen the region's global market position.

The U.S. Market (USD 2,278.8 million in 2024, 3.3% CAGR): The U.S. radiopharmaceutical market is one of the largest and most developed markets globally, occupying a leading position. Steady increase in market size is driven by continued incidence of chronic diseases including cancer and cardiovascular diseases requiring better diagnostic and treatment solutions. Key market trends include increased use of therapeutic radiopharmaceuticals in targeted cancer therapies including Lutetium-177 for prostate cancer. New radiopharmaceutical development including integration into precision medicine strategies has fueled demand. The United States is the location of origin for developing new technologies in nuclear medicine in both PET and SPECT modalities. The highly developed healthcare sector with regular R&D activities enables the U.S. to retain the top position. Increasing budget for cancer-related research and growing number of clinical trials for new radiopharmaceuticals fuel market growth.

Europe: Europe's radiopharmaceutical market is characterized by strong nuclear medicine infrastructure, government support for radiopharmaceutical research, and high adoption of PET and SPECT imaging across major economies including Germany, France, the UK, and Italy. The European Medicines Agency provides regulatory pathways for new radiopharmaceuticals, and the region's focus on theranostics and personalized medicine drives innovation.

Asia-Pacific (Fastest-Growing Region): The Asia-Pacific region presents the most promising opportunity for the radiopharmaceutical market due to constantly developing healthcare sectors and increasing demand for nuclear medicines. Nuclear medicine facilities are being developed in countries including India and China, with more diagnostic and therapeutic services being added. Growing rates of chronic diseases in these areas are fueling market growth. IBA opened a new manufacturing facility in India for medical isotope production (January 2024), aimed at meeting growing demand for radiopharmaceuticals in the Asia-Pacific region. Japan's advanced nuclear medicine infrastructure and aging population drive steady demand.

📄 Get the Full Premium Report Now- https://dimensionmarketresearch.com/checkout/radiopharmaceuticals-market/

🔷 Competitive Landscape: Global Leaders, Nuclear Medicine Specialists, and Emerging Innovators

The radiopharmaceuticals market is highly competitive, with key players controlling large market shares through new product development, cooperation strategies, and ongoing R&D.

Global Radiopharmaceutical Leaders: Bayer AG, Bracco Imaging S.p.A., Cardinal Health, Inc., Eli Lilly and Company, Curium Pharma, Lantheus Holdings, Inc., Novartis AG, Nordion (Canada) Inc., and Jubilant Radiopharma dominate with extensive product portfolios, global distribution networks, and strong R&D capabilities. GE Healthcare is a leading player in imaging radiopharmaceuticals. Cardinal Health expanded its nuclear pharmacy network in the U.S. (April 2024), enhancing distribution capabilities for radiopharmaceuticals. Lantheus Holdings received FDA approval for a new radiopharmaceutical targeting prostate cancer (March 2024), increasing its presence in the oncology segment.

Technology and Equipment Providers: Ion Beam Applications (IBA) and Siemens Healthineers are major players in cyclotron technology and nuclear medicine imaging systems. IBA announced the launch of a new compact cyclotron for radioisotope production (September 2024), aimed at improving radiopharmaceutical availability for cancer diagnosis and therapy. Siemens Healthineers partnered with Harvard Medical School (June 2024) to advance nuclear medicine imaging research and novel radiopharmaceutical development.

Recent Developments Highlighting Market Momentum:

September 2024: Ion Beam Applications (IBA) launched a new compact cyclotron for radioisotope production.

August 2024: GE Healthcare introduced a new line of theranostic radiopharmaceuticals for precision cancer therapy.

June 2024: Siemens Healthineers partnered with Harvard Medical School to advance nuclear medicine imaging research.

April 2024: Cardinal Health expanded its nuclear pharmacy network in the U.S., enhancing distribution capabilities.

March 2024: Lantheus Holdings received FDA approval for a new radiopharmaceutical targeting prostate cancer.

January 2024: IBA opened a new manufacturing facility in India for medical isotope production.

November 2023: Cardinal Health entered a collaboration with Pfizer to develop radiopharmaceuticals for neurological disorder diagnosis.

🔷 The Road Ahead: What Decision-Makers Need to Know

For B2B decision-makers-nuclear medicine department directors, radiopharmaceutical manufacturers, healthcare investors, and oncology treatment planners-the strategic imperative is clear: radiopharmaceuticals have moved from diagnostic imaging agents to therapeutic platforms enabling precision cancer care. The 3.5% CAGR reflects steady demand driven by chronic disease prevalence, theranostics adoption, and technological advancement in nuclear medicine.

Key strategic imperatives include:

Invest in theranostic radiopharmaceutical development. Lutetium-177 and Yttrium-90 in targeted cancer therapy represent the fastest-growing segment. The convergence of diagnostic and therapeutic applications creates significant opportunities.

Prioritize diagnostic radiopharmaceuticals for oncology applications. With 63.1% market share, diagnostic agents remain the foundation. Fluorine-18 and Technetium-99m are essential for PET and SPECT imaging in cancer, cardiac, and neurological applications.

Expand cyclotron infrastructure for on-site isotope production. Short half-lives of key isotopes including Fluorine-18 (110 minutes) make on-site production essential. Investment in cyclotrons reduces transportation issues and ensures timely availability.

Expand into Asia-Pacific emerging markets. India and China are developing nuclear medicine facilities with increasing diagnostic and therapeutic services. Local manufacturing partnerships and distribution networks will capture growth.

Navigate regulatory pathways strategically. FDA and EMA approvals for new radiopharmaceuticals require significant investment in safety and quality documentation. Early engagement with regulatory bodies accelerates market entry.

The full report from Dimension Market Research provides granular segmentation by radioisotope (Fluorine-18 derivatives-FDG, sodium fluoride, sodium flucicovine, sodium florbetapir, sodium flurbetaben-Technetium-99, Lutetium-177, Gallium-68, Zirconium-89, 11C-choline, 14C-urea), type (diagnostic radiopharmaceuticals-SPECT, PET-therapeutic radiopharmaceuticals-alpha emitters, beta emitters), source (cyclotrons, nuclear reactors, generators), application (oncology, cardiology, neurology, endocrinology), end-user (hospitals, medical imaging centers, cancer research institutes), and 20+ regional markets, offering actionable intelligence for strategic planning.

📄 Explore the Report with TOC → https://dimensionmarketresearch.com/report/radiopharmaceuticals-market/

For Sales or Inquiries, Contact

Robert John

957 Route 33, Suite 12 #308 Hamilton Square, NJ-08690 USA

Email: enquiry@dimensionmarketresearch.com

United States: (+1 732 369 9777)

Tel No: +91 88267 74855

Dimension Market Research (DMR) is a market research and consulting firm based in India & US, with its headquarters located in the USA. The company believes in providing the best and most valuable data to its customers using the best resources and analysts to work on, to create unmatchable insights into the industries and markets while offering in-depth results of over 30 industries, and all major regions across the world. We also believe that our clients don't always want what they see, so we provide customized reports as well, as per their specific requirements, to create the best possible outcomes for them and enhance their business through our data and insights in every possible way.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Radiopharmaceuticals Market to Reach $9,876.2 million by 2033 as Theranostics and PET Imaging Drive Precision Cancer Care here

News-ID: 4513081 • Views: …

More Releases from Dimension Market Research

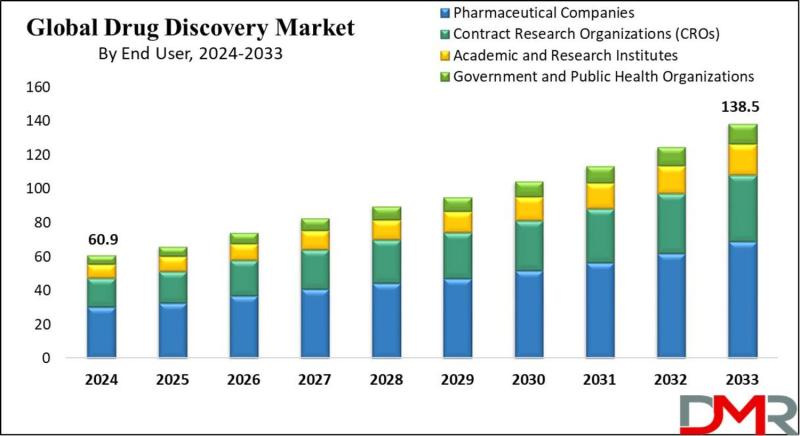

Drug Discovery Market to Reach $138.5 Billion by 2033 as AI-Powered Screening an …

The global Drug Discovery Market is poised for substantial growth, with market valuation projected to rise from an estimated USD 60.9 billion in 2024 to USD 138.5 billion by 2033, registering a strong compound annual growth rate (CAGR) of 9.6%. According to Dimension Market Research, this expansion is being driven by four converging forces: the rising demand for novel therapeutics addressing chronic diseases, the integration of artificial intelligence and machine…

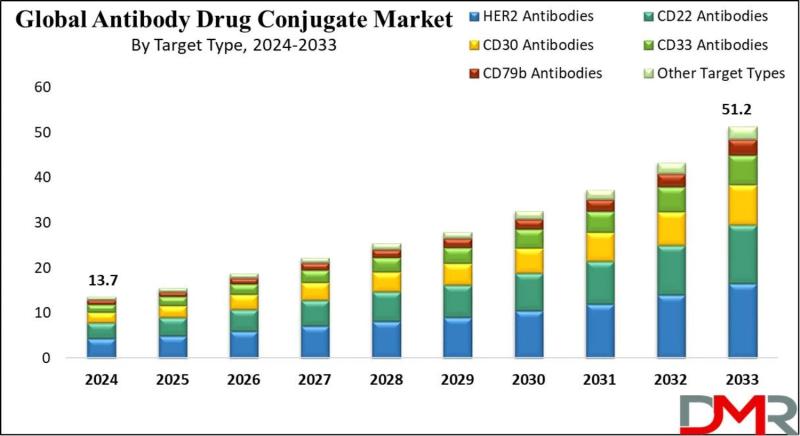

Antibody Drug Conjugates Market to Nearly Quadruple to $51.2 Billion by 2033 as …

According to Dimension Market Research, the Global Antibody Drug Conjugates (ADC) Market is poised for explosive exponential growth, projected to surge from USD 13.7 billion in 2024 to a staggering USD 51.2 billion by 2033, registering a remarkable compound annual growth rate (CAGR) of 15.8%. This growth reflects the accelerating clinical and commercial validation of ADCs as one of the most promising therapeutic modalities in modern oncology.

Antibody drug conjugates-often described…

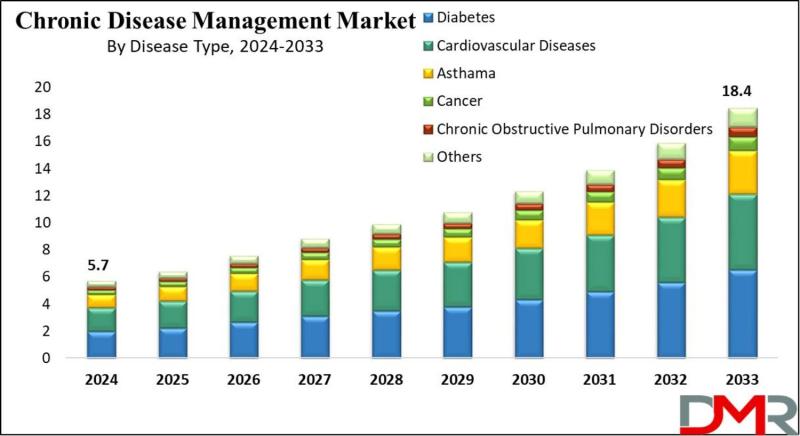

Chronic Disease Management Market to Surpass $18.4 Billion by 2033 as Telehealth …

According to Dimension Market Research, the Global Chronic Disease Management Market is poised for substantial expansion, projected to surge from USD 5.7 billion in 2024 to USD 18.4 billion by 2033, registering a robust compound annual growth rate (CAGR) of 13.9%. This growth reflects the accelerating global burden of non-communicable diseases (NCDs) and the fundamental shift from episodic, reactive care toward continuous, technology-enabled chronic condition management.

Chronic diseases-including diabetes, cardiovascular disease,…

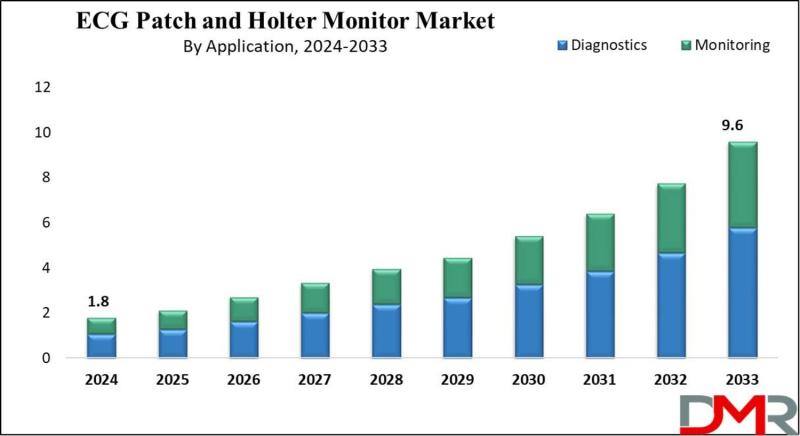

ECG Patch and Holter Monitor Market to Skyrocket 20.3% Annually, Reaching $9.6 B …

According to Dimension Market Research, the Global ECG Patch and Holter Monitor Market is poised for explosive exponential growth, projected to surge from USD 1.8 billion in 2024 to a staggering USD 9.6 billion by 2033, registering a remarkable compound annual growth rate (CAGR) of 20.3%. This transformation reflects the accelerating global shift toward wearable, patient-centric cardiac monitoring solutions that offer comfort, convenience, and continuous data capture far beyond traditional…

More Releases for PET

Pet Travel Services Market Is Booming So Rapidly | RoyalPaws, Pet Port, Pet Oasi …

The Global Pet Travel Services Market Size is estimated at $2.8 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 8.6% to reach $5.9 Billion by 2034.

The latest study released on the Global Pet Travel Services Market by USD Analytics Market evaluates market size, trend, and forecast to 2034. The Pet Travel Services market study covers significant research data and proofs to be a handy…

Pet Carriers Market is Booming Worldwide | K&H Manufacturing, Sherpa Pet, Quaker …

Worldwide Pet Carriers Market In-depth Research Report 2024, Forecast to 2030 is the latest research study released by HTF MI evaluating the market risk side analysis, highlighting opportunities, and leveraging strategic and tactical decision-making support. The report provides information on market trends and development, growth drivers, technologies, and the changing investment structure of the Worldwide Pet Carriers Market. Some of the key players profiled in the study are K&H Manufacturing…

Pet Air Shipping Service Market Growth Expected to See Next Level: Pet Travel, P …

Latest Study on Industrial Growth of Global Pet Air Shipping Service Market 2024-2030. A detailed study accumulated to offer the Latest insights about acute features of the Pet Air Shipping Service market. The report contains different market predictions related to revenue size, production, CAGR, Consumption, gross margin, price, and other substantial factors. While emphasizing the key driving and restraining forces for this market, the report also offers a complete study…

Pet Shops Market 2023- Industry Comprehensive Understanding | PETSMART, PETCO, P …

The Pet Shops market research report is proficient and top to bottom research by specialists on the current state of the industry. This statistical surveying report gives the most up to date industry information and industry future patterns, enabling you to distinguish the items and end clients driving income development and benefit. It centres around the real drivers and restrictions for the key players and present challenge status with development…

Pet Bag Market Set for More Growth : Gen7Pets, Sherpa Pet, Quaker Pet

Advance Market Analytics published a new research publication on "Pet Bag Market Insights, to 2028" with 232 pages and enriched with self-explained Tables and charts in presentable format. In the Study you will find new evolving Trends, Drivers, Restraints, Opportunities generated by targeting market associated stakeholders. The growth of the Pet Bag market was mainly driven by the increasing R&D spending across the world. Some of the key players profiled…

Pet Veterinary Diets Market 2019 Industry Dynamics - Mars, Farmina Pet Foods, Ni …

Recent market research study Global Pet Veterinary Diets Market 2019-2024 now available with Fior Markets provides a comprehensive market analysis based on past and current situation of the market. The report covers future trends, current growth drivers, thoughtful insights, facts, market valuation, competitive spectrum, regional share, and revenue predictions. The report shows the market size, share, business growth enhancers, and obstructers, prior and current trends being followed by the market.…