Press release

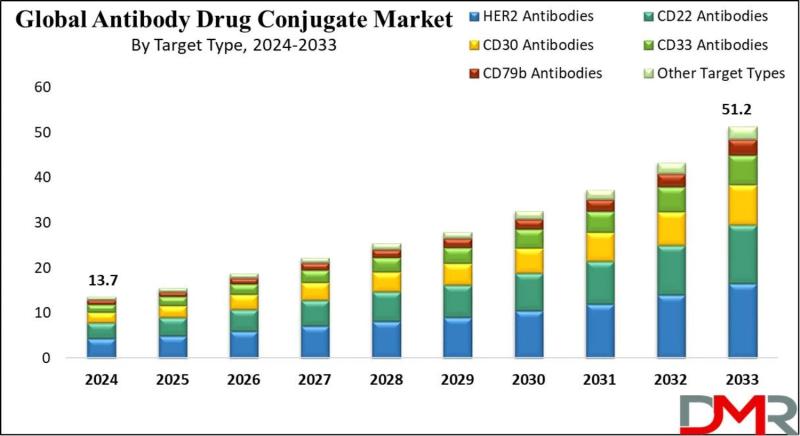

Antibody Drug Conjugates Market to Nearly Quadruple to $51.2 Billion by 2033 as Precision Oncology Enters a New Era

Antibody Drug Conjugates Market Size, Share, Trends & Outlook Report 2033

Antibody drug conjugates-often described as "biological smart bombs"-combine the targeting precision of monoclonal antibodies with the cell-killing potency of cytotoxic chemicals, delivering medicine directly to cancer cells while sparing healthy tissue. With cancer cases continuing to rise globally (approximately 19.3 million new cases annually) and conventional chemotherapy limited by systemic toxicity, ADCs represent a paradigm shift toward targeted, patient-centric cancer care. For pharmaceutical executives, oncology researchers, and healthcare investors, the message is clear: ADCs are no longer a niche modality-they are becoming backbone therapies across multiple tumor types.

📄 Get Your Sample Report Today → https://dimensionmarketresearch.com/request-sample/antibody-drug-conjugates-market/

🔷 Unique News Angle: HER2 Remains the Dominant Target at 32.2%, But Novel Antigens and Payload Innovation Are Reshaping the Landscape

While HER2-targeting ADCs (KADCYLA, ENHERTU) maintain their leadership, capturing 32.2% of the target type segment in 2024, the most significant transformation is the rapid expansion beyond HER2 into novel tumor-associated antigens and the evolution of payload technologies. HER2 is amplified in approximately 20-25% of breast cancer patients, establishing it as a critical therapeutic target. However, the ADC pipeline now includes antibodies targeting TROP-2, Nectin-4, CD30, CD79b, and emerging targets in lung, ovarian, gastric, and bladder cancers.

Equally transformative is the innovation in payload technology. MMAE (Monomethyl Auristatin E)-currently dominating the payload type segment-binds to microtubules causing cell cycle arrest and apoptosis. Next-generation payloads including PBD dimers, camptothecin derivatives, and novel topoisomerase inhibitors are expanding therapeutic windows and overcoming resistance mechanisms. The convergence of novel targets, optimized linkers, and increasingly potent payloads is transforming ADCs from specialized therapies into platform technologies applicable across oncology.

🔷 Key Insights: The Data Driving the ADC Revolution

North America Leads with 42.7% Market Share: North America dominates the global ADC market, driven by high cancer incidence, advanced healthcare infrastructure, strong pharmaceutical R&D investment, and an ideal regulatory environment (FDA) enabling rapid approval and implementation. The US market alone reaches USD 4.9 billion in 2024, growing to USD 17.1 billion by 2033 at 14.8% CAGR.

KADCYLA Leads Products at 24.1% Market Share: KADCYLA (trastuzumab emtansine)-an ADC for HER2-positive breast cancer-holds the largest product share based on extensive efficacy and safety data. FDA approval in multiple indications, including adjuvant settings for early-stage breast cancer, and Roche's unparalleled marketing and distribution reinforce its dominance.

HER2 Antibodies Dominate Target Type at 32.2%: HER2-targeting ADCs lead due to their efficacy in treating HER2-positive cancers (breast, gastric). KADCYLA and ENHERTU have demonstrated remarkable success in clinical trials, with high incidence of HER2-positive breast cancer driving sustained demand.

MMAE/Auristatin Leads Payload Type: MMAE (Monomethyl Auristatin E) dominates the payload segment due to potent cytocidal effects on cancer cells, binding to microtubules to cause cell cycle arrest and apoptosis at low drug concentrations with minimal systemic toxicity. MMAE-based ADCs (ADCETRIS, PADCEV) show high clinical benefits for lymphomas and urothelial carcinoma.

Blood Cancer Leads Applications: Blood cancers (leukemia, lymphoma, multiple myeloma) dominate the application segment because ADCs are highly effective in treating these malignancies. ADCs like ADCETRIS (CD30) and POLIVY (CD79b) bind to specific antigens on hematologic cancer cells, delivering toxic payloads directly to tumor sites with minimal side effects compared to conventional therapies.

📄 Get the Insights You Need to Drive Real Impact → https://dimensionmarketresearch.com/request-sample/antibody-drug-conjugates-market/

🔷 Market Dynamics: Drivers, Restraints, and the Combination Therapy Opportunity

Drivers:

The primary catalyst is technological advancements in ADC development, including new linkers (cleavable VC and hydrazone linkers enabling tumor microenvironment-specific drug release), potent therapeutic payloads (MMAE, DM4, PBD dimers), and effective conjugation strategies making ADCs safer and more effective. Additionally, the increasing prevalence of cancer globally drives demand for more effective treatments with fewer detrimental effects on healthy tissues, with ADCs delivering cytotoxic agents directly to tumor cells.

Restraints:

High development costs remain a significant barrier. ADCs are constructed via multiple steps-generation of monoclonal antibodies, synthesis of cytotoxic drugs, and linking both components-contributing to higher development and manufacturing costs. The financial risk inherent in ADC business, particularly at developmental stages, is a major challenge for pharma firms. Additionally, regulatory challenges-ADCs must undergo rigorous procedures to determine efficacy, safety, and quality-with long, intricate clinical trial processes potentially delaying market access.

Opportunities:

Emerging markets across Asia-Pacific, Latin America, and the Middle East present significant growth potential. Improving healthcare facilities, rising cancer awareness, increasing healthcare expenditure, and regulatory environments trending toward approval of new therapies create favorable conditions for ADC expansion. Additionally, combination therapies-ADCs combined with immunotherapies or checkpoint inhibitors-exhibit synergistic effects, increasing response rates and overcoming resistance mechanisms, expanding ADC applications and fueling market growth.

🔷 Trends Reshaping the ADC Landscape

Rising Adoption of ADCs in Oncology:

The use of ADCs is growing steadily, most frequently applied in oncology due to targeted action combining monoclonal antibody function with cytotoxic drug effects. Marketed ADCs including KADCYLA, ENHERTU, and ADCETRIS have shown positive clinical improvement across different cancer types, with more approvals entering the market driving growth.

Expansion of ADCs Beyond Oncology:

While oncology remains the leading indication for ADC development, research is shifting toward converting ADCs for non-oncological indications including autoimmune diseases and infections. Research is in progress to find suitable targets and create ADCs for these indications, suggesting new therapeutic options and increasing the overall market size.

Linker Technology Innovation:

Cleavable linkers (VC, hydrazone) facilitate drug release at the tumor microenvironment, increasing therapeutic efficiency while resolving stability issues and controlled release problems with minimal off-target effects. New generations of peptide linkers and disulfide linkers represent continuing innovation, with linker technology remaining a critical ADC development factor.

Next-Generation Payload Development:

Beyond MMAE/auristatin dominance, next-generation payloads including PBD dimers, camptothecin derivatives, and novel topoisomerase inhibitors are expanding therapeutic windows, overcoming resistance mechanisms, and enabling activity in previously refractory tumor types.

🔷 Segmentation Spotlight: KADCYLA, HER2, MMAE, and Hospital Dominance

By Product (KADCYLA at 24.1%): KADCYLA dominates due to extensive efficacy and safety data for HER2-positive breast cancer, with trastuzumab (humanized anti-HER2 monoclonal antibody) conjugated with cytotoxic agent DM1. FDA approval in multiple indications including adjuvant early-stage breast cancer, numerous clinical trials supporting efficacy, and Roche's unparalleled marketing and distribution ensure high patient availability.

By Target Type (HER2 Antibodies at 32.2%): HER2-targeting ADCs dominate due to efficacy in treating HER2-positive cancers. HER2 is amplified in approximately 20-25% of breast cancer patients, making it a critical treatment development target. KADCYLA and ENHERTU deliver cytotoxic payloads directly to tumor cells, increasing therapeutic effect while decreasing systemic side effects, with continuous improvements enriching application scope.

By Payload Type (MMAE/Auristatin Leads): MMAE (Monomethyl Auristatin E) dominates due to potent cytocidal effects, binding to microtubules causing cell cycle arrest and inducing apoptosis at low drug concentrations with minimal systemic toxicity. MMAE-based ADCs including ADCETRIS (lymphomas) and PADCEV (urothelial carcinoma) demonstrate high clinical benefits, with ongoing research fine-tuning implementation.

By Application (Blood Cancer Leads): Blood cancers (leukemia, lymphoma, multiple myeloma) dominate because ADCs are highly effective in treating hematologic malignancies. ADCETRIS (CD30) and POLIVY (CD79b) bind specific antigens on cancer cells, directing toxic payloads to tumor sites with selective treatment enhancing efficacy while minimizing side effects compared to conventional therapies.

By End User (Hospitals & Specialty Cancer Centers Lead): Hospitals and specialty cancer centers dominate due to efficient and effective healthcare service delivery, major sources of cancer treatment, and comprehensive resources to manage complex therapies like ADCs. These institutions are frequently engaged in clinical studies based on ADC therapies, enabling patients to benefit from emerging platforms.

🔷 Technology Deep-Dive: Linkers and Payloads

By Technology Type (Cleavable Linkers Lead): Cleavable linker antibodies (VC, hydrazone) dominate due to effectiveness in facilitating drug release at the tumor microenvironment, increasing therapeutic efficiency while resolving stability issues with minimal off-target effects. Peptide linkers and disulfide linkers represent continuing innovation generations.

By Payload Technology (MMAE Leads): MMAE and other auristatins dominate payload technology due to strong cytocidal effects. Binding to microtubules causes cell cycle arrest and apoptosis at low drug concentrations with minimal systemic toxicity. MMAE-based ADCs show high clinical benefits for lymphomas and urothelial carcinoma.

📄 Get the Full Premium Report Now - https://dimensionmarketresearch.com/checkout/antibody-drug-conjugates-market/

🔷 Regional Analysis: North America Leads, Asia-Pacific Accelerates

North America (42.7% share - USD 13.7 billion total market): North America holds the largest share in the global ADC market due to high cancer incidence driving demand for prominent treatment forms, advanced healthcare systems enabling access to sophisticated therapies, and the presence of major large-scale pharma players with robust research facilities. An ideal regulatory environment (FDA) increases approval and implementation of new treatments. Advanced clinical trial structures enable rapid evaluation and approval of new ADCs. University-industry relationships for research and development offer additional support, creating opportunities for further inventions.

Europe: The European market represents a significant share, with Germany, France, and the UK leading adoption. Strong healthcare infrastructure, regulatory harmonization (EMA), and increasing investment in precision oncology support growth. Recent EMA approvals (Seattle Genetics for multiple myeloma, December 2023) signal continued market expansion.

Asia-Pacific (Fastest-Growing Region): The Asia-Pacific region is expected to witness the most significant growth, driven by improving healthcare infrastructure, increasing healthcare expenditure, large cancer patient populations, and growing awareness of advanced oncology treatments. Japan's advanced regulatory framework, China's rapid biotech expansion, and India's growing clinical trial capabilities create favorable conditions. Daiichi Sankyo's strategic partnership with Scripps Research Institute (October 2023) and Eli Lilly's licensing agreement with Zymeworks for Asia-Pacific commercialization (January 2023) signal increasing regional focus.

Latin America and Middle East & Africa: These regions represent emerging opportunities, with countries like Brazil, Mexico, Saudi Arabia, and UAE investing in healthcare digitization and oncology infrastructure, though market penetration remains limited by reimbursement challenges and regulatory pathways.

🔷 Competitive Landscape: Global Giants, Emerging Biotechs, and Strategic Collaborations

The ADC market is widely competitive, with global players and emerging biotechs seeking market share through continuous innovation and strategic collaborations.

Key Players:

Hoffmann-La Roche Ltd. (Switzerland): Global ADC leader with KADCYLA and POLIVY; reported promising phase III trial results for HER2-targeting gastric cancer ADC (June 2024).

Pfizer, Inc. (US): Received FDA approval for new ADC targeting triple-negative breast cancer biomarker (July 2024), offering novel treatment for hard-to-treat subtype.

AstraZeneca (UK/Sweden): Expanded ADC manufacturing capabilities with new state-of-the-art facility (November 2023) to meet growing global demand.

Daiichi Sankyo Company, Limited (Japan): Entered strategic partnership with Scripps Research Institute (October 2023) to develop next-generation ADCs with novel payloads and linker technologies; partnered with AstraZeneca on ENHERTU.

Seagen, Inc. (US): Received EMA approval for ADC treating relapsed/refractory multiple myeloma (December 2023), marking first European market entry.

Gilead Sciences, Inc. (US): Markets TRODELVY for metastatic triple-negative breast cancer and urothelial cancer.

Astellas Pharma, Inc. (Japan): Markets PADCEV (with Seagen) for urothelial cancer.

ADC Therapeutics SA (Switzerland): Focuses on novel ADCs for hematologic and solid tumors.

ImmunoGen Inc. (US): Develops next-generation ADCs with novel payload technologies.

GlaxoSmithKline plc (UK): Launched phase I clinical trial for new ADC targeting unique antigen in small-cell lung cancer (September 2023).

Recent Developments Signal Unprecedented Momentum (2023-2024):

2024:

July: Pfizer received FDA approval for new ADC targeting triple-negative breast cancer biomarker.

June: Roche reported promising phase III trial results for HER2-targeting gastric cancer ADC.

2023:

December: Seattle Genetics received EMA approval for ADC treating relapsed/refractory multiple myeloma.

November: AstraZeneca expanded ADC manufacturing capabilities with new facility.

October: Daiichi Sankyo entered strategic partnership with Scripps Research Institute.

September: GlaxoSmithKline launched phase I trial for small-cell lung cancer ADC.

August: Merck & Co. presented ASCO data on ADC plus immune checkpoint inhibitor combination.

July: Bristol-Myers Squibb initiated phase II trial for metastatic colorectal cancer ADC.

June: Novartis received orphan drug designation for rare sarcoma ADC.

May: AbbVie received FDA breakthrough therapy designation for CD123-targeting ADC in acute myeloid leukemia.

April: Sanofi announced positive phase II results for HER2-low breast cancer ADC.

March: Johnson & Johnson formed collaboration with Genmab for novel ADC antibody engineering.

February: Takeda received FDA fast-track designation for advanced bladder cancer ADC.

January: Eli Lilly entered licensing agreement with Zymeworks for Asia-Pacific ADC commercialization.

🔷 The Future of ADCs (2024-2033): Novel Targets, Combination Regimens, and Platform Expansion

Looking ahead, three forces will define the ADC market trajectory. First, expansion beyond HER2 into novel targets-including TROP-2, Nectin-4, CD30, CD79b, and emerging antigens in lung, ovarian, gastric, and pancreatic cancers-will dramatically expand the addressable patient population. Second, combination regimens with immunotherapies (checkpoint inhibitors, bispecific antibodies) will become standard, exhibiting synergistic effects that increase response rates and overcome resistance mechanisms. Third, platform expansion beyond oncology-into autoimmune diseases, infectious diseases, and inflammatory conditions-represents a frontier opportunity. Research is in progress to identify suitable targets for non-oncological indications. By 2033, ADCs will be not just an oncology modality but a versatile therapeutic platform applicable across multiple disease areas.

The full report provides granular segmentation by product (KADCYLA, ENHERTU, ADCETRIS, PADCEV, TRODELVY, POLIVY), target type (HER2, CD22, CD30, CD33, CD79b antibodies), technology (cleavable/non-cleavable/linkerless antibodies; linker technology including VC, Sulfo-SPDB, VA, hydrazone, disulfide, peptide; payload technology including MMAE, MMAF, DM4, camptothecin derivatives, PBD dimers, SN-38), payload type (MMAE/auristatin, calicheamicin, maytansinoids, PBD dimers, camptothecin derivatives, SN-38), application (blood cancer including leukemia, lymphoma, multiple myeloma; breast cancer; urothelial & bladder cancer; lung cancer; ovarian cancer; gastric cancer), and end user (hospitals & specialty cancer centers, biotech & pharma companies, academic & research institutes, CROs). Regional deep-dives cover North America (US, Canada), Europe (Germany, UK, France, Italy, Russia, Spain, Benelux, Nordic), Asia-Pacific (China, Japan, South Korea, India, ANZ, ASEAN), Latin America, and Middle East & Africa with 10-year forecasts, competitive vendor market share analysis, and clinical trial pipeline assessment.

📄 Explore the Report with TOC → https://dimensionmarketresearch.com/report/antibody-drug-conjugates-market/

For Sales or Inquiries, Contact

Robert John

957 Route 33, Suite 12 #308 Hamilton Square, NJ-08690 USA

Email: enquiry@dimensionmarketresearch.com

United States: (+1 732 369 9777)

Tel No: +91 88267 74855

Dimension Market Research (DMR) is a market research and consulting firm based in India & US, with its headquarters located in the USA. The company believes in providing the best and most valuable data to its customers using the best resources and analysts to work on, to create unmatchable insights into the industries and markets while offering in-depth results of over 30 industries, and all major regions across the world. We also believe that our clients don't always want what they see, so we provide customized reports as well, as per their specific requirements, to create the best possible outcomes for them and enhance their business through our data and insights in every possible way.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Antibody Drug Conjugates Market to Nearly Quadruple to $51.2 Billion by 2033 as Precision Oncology Enters a New Era here

News-ID: 4512424 • Views: …

More Releases from Dimension Market Research

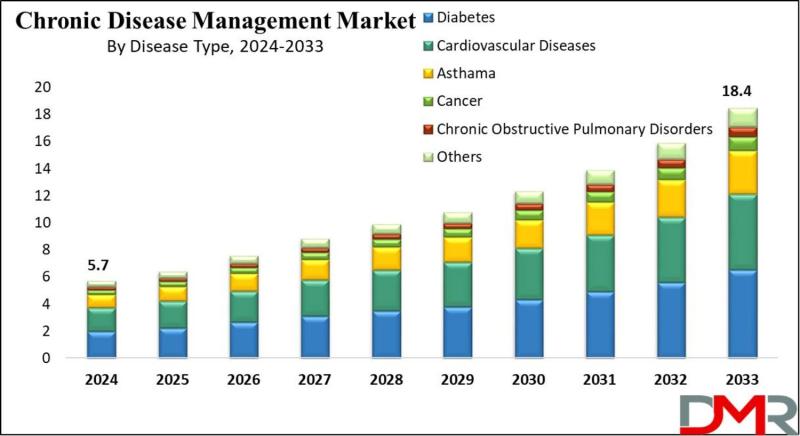

Chronic Disease Management Market to Surpass $18.4 Billion by 2033 as Telehealth …

According to Dimension Market Research, the Global Chronic Disease Management Market is poised for substantial expansion, projected to surge from USD 5.7 billion in 2024 to USD 18.4 billion by 2033, registering a robust compound annual growth rate (CAGR) of 13.9%. This growth reflects the accelerating global burden of non-communicable diseases (NCDs) and the fundamental shift from episodic, reactive care toward continuous, technology-enabled chronic condition management.

Chronic diseases-including diabetes, cardiovascular disease,…

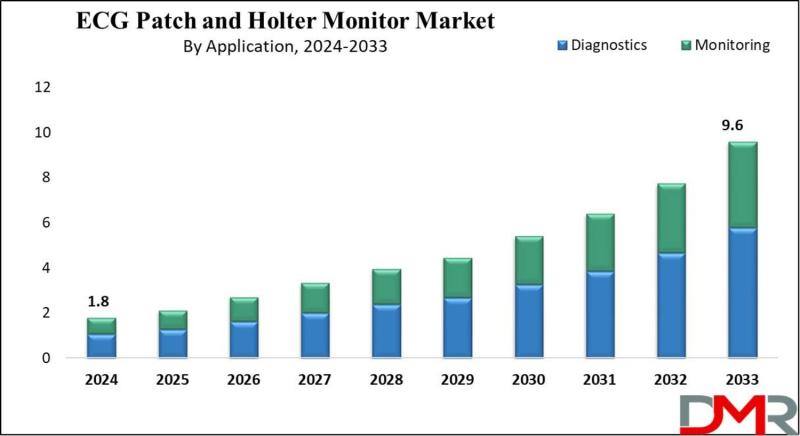

ECG Patch and Holter Monitor Market to Skyrocket 20.3% Annually, Reaching $9.6 B …

According to Dimension Market Research, the Global ECG Patch and Holter Monitor Market is poised for explosive exponential growth, projected to surge from USD 1.8 billion in 2024 to a staggering USD 9.6 billion by 2033, registering a remarkable compound annual growth rate (CAGR) of 20.3%. This transformation reflects the accelerating global shift toward wearable, patient-centric cardiac monitoring solutions that offer comfort, convenience, and continuous data capture far beyond traditional…

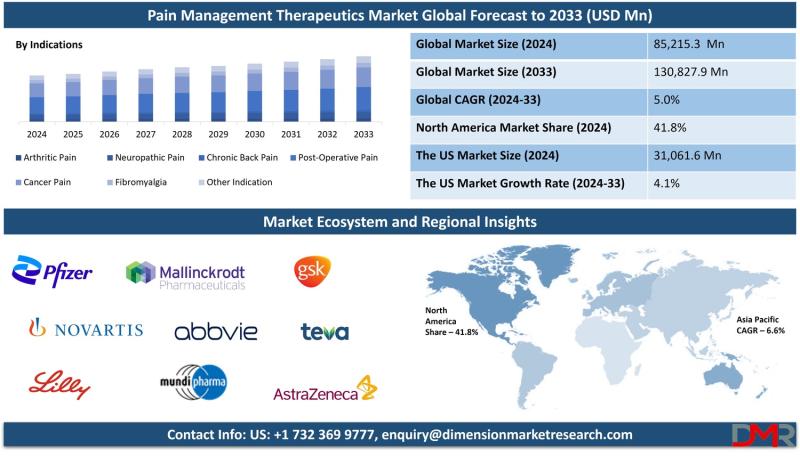

Pain Management Therapeutics Market to Reach $130,827.9 million by 2033 as Non-O …

According to Dimension Market Research, the Global Pain Management Therapeutics Market is projected to expand from USD 85,215.3 million in 2024 to USD 130,827.9 million by 2033, registering a steady compound annual growth rate (CAGR) of 5.0%. This growth reflects the escalating global burden of chronic pain conditions-arthritis, neuropathic pain, cancer pain, and fibromyalgia-coupled with a transformative shift toward safer, non-opioid therapeutic alternatives.

Chronic pain affects an estimated 1.5 billion people…

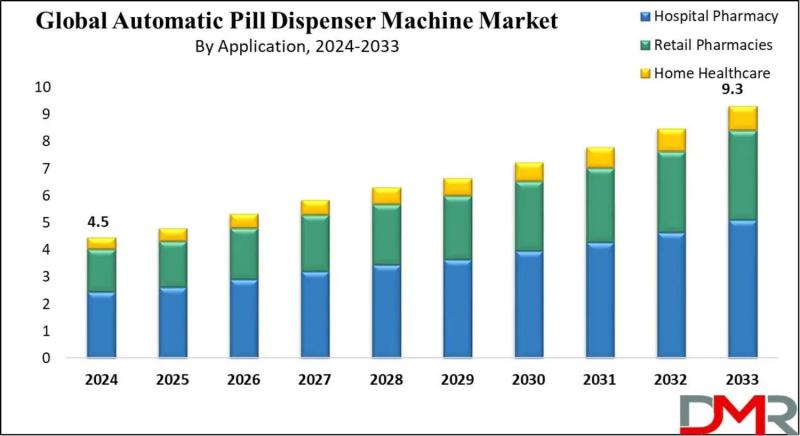

Automatic Pill Dispenser Market to Double to $9.3 Billion by 2033 as Aging Popul …

According to Dimension Market Research, the Global Automatic Pill Dispenser Machine Market is poised for substantial growth, projected to expand from USD 4.5 billion in 2024 to USD 9.3 billion by 2033, registering a robust compound annual growth rate (CAGR) of 8.5%. This growth reflects the accelerating global imperative to reduce medication errors, improve patient adherence, and manage complex pharmaceutical regimens for an aging population.

Medication errors remain one of the…

More Releases for ADC

ADC Market: Transforming Cancer Treatment

The global market for antibody-drug conjugates (ADCs) was valued at US$ 11.32 billion in 2023 and is expected to reach US$ 27.37 billion by 2033, growing at a compound annual growth rate (CAGR) of 9.23% from 2024 to 2033. This growth is primarily driven by the increasing prevalence of cancer and the growing demand for safe and effective treatments.

Antibody Drug Conjugates: A Growing Force in Cancer Treatment and Market Expansion

Key…

With Knockout ADC Innovations, Creative Biolabs Took Center Stage at the 2024 Wo …

Creative Biolabs wrapped up a successful show at the 15th Annual World ADC San Diego in the beginning of November, where its third year of participation, highlighting its dedication to the advancement of antibody-drug conjugate (ADC) technology.

New York, USA - November 13, 2024 - Creative Biolabs seized the spotlight at Booth 313 by offering groundbreaking solutions across the entire ADC development spectrum, which demonstrate their unrivaled expertise and dedication to…

Showing Off Their ADC Game: Creative Biolabs Hits the 15th Annual World ADC Summ …

From November 4, Creative Biolabs will be back at the 15th Annual World ADC Summit in San Diego, marking its fourth year at the leading global gathering featuring innovative conjugates.

New York, USA - November 6, 2024 - Creative Biolabs invites all ADC enthusiasts, from new entrants to seasoned experts, to explore its comprehensive suite of ADC solutions and experience the latest in antibody-drug conjugate (ADC) innovation at Booth #313.

Image: https://www.getnews.info/uploads/0c59d26f78bf6dd58aafee5bc68d7d8c.jpg

"2023…

ADC Drugs For Breast Cancer Treatment

Breast cancer is the malignant tumor with the highest morbidity and mortality among women worldwide. At present, the main therapeutic methods include surgery, chemotherapy, radiotherapy, endocrine therapy and targeted therapy, etc. The development and marketing of new drugs have far-reaching significance in improving the survival of breast cancer patients and changing the pattern of breast cancer treatment.

On February 24, 2023, The NMPA approved Enhertu, an injectable drug developed jointly by…

Analog-to-Digital Converters Market by Product (Ramp ADC, Integrating ADC, Succe …

Analog-to-Digital Converters Market by Product (Ramp ADC, Integrating ADC, Successive Approximation ADC, Delta-sigma ADC, and Others (Pipelined/Flash ADC)), and Application (Consumer Electronics and Industrial) - Global Opportunity Analysis and Industry Forecast, 2017-2023

Full Report : https://www.alliedmarketresearch.com/analog-to-digital-converters-market

Increasing disposable income and technological advancements supplement the analog-to-digital converters market. However, complex design of the ADC hampers this market growth. On the other hand, encouragement in digitization of work processes by government in emerging economies,…

Global Data Converters Market Report 2017 (Analog to Digital Converter, Current …

The research report titled Global Data Converters Sales Market Report 2017 market size and forecast and overview on current market trends.

This report studies sales (consumption) of Global Data Converters Market 2017, especially in United States, China, Europe and Japan, focuses on top players in these regions/countries, with sales, price, revenue and market share for each player in these regions, covering

National Semiconductor

Nippon Precision Circuits Inc

Micro Analog systems

Microchip Technology.

TelCom Semiconductor, Inc

Vishay Siliconix

Texas…