Press release

True Fleet in 2016 ends with bang for the EU-5

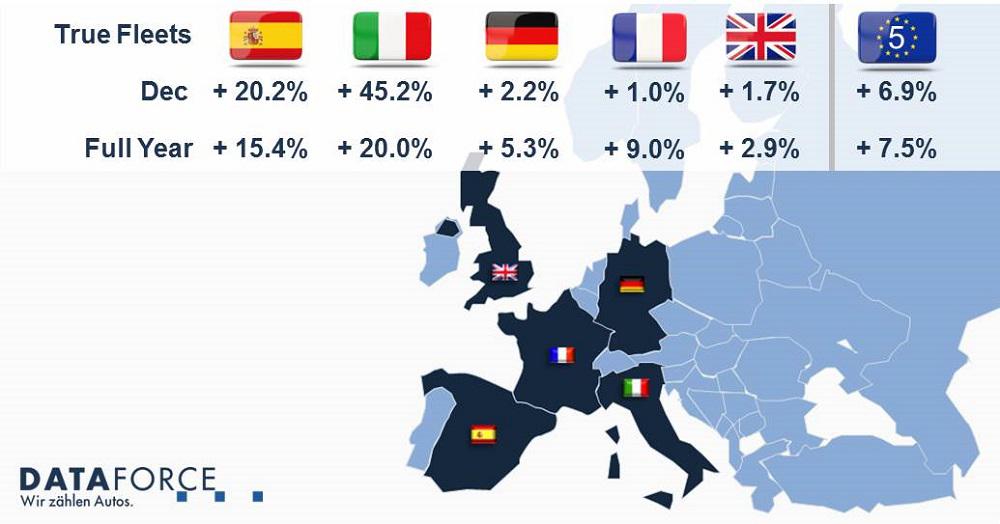

Spain

What a successful year for the Spanish True Fleet Market. A very strong result in December (+ 20.2%) pushed the growth rate for the full year 2016 to an impressive + 15.4%. Putting this into context, the passenger car total market achieved 1,192,418 registered vehicles for 2016 (an increase of 12.0% over 2015 total) so the 235,895 produced by True Fleet not only represents almost 20% of the Spanish Total Market but for the 4th year in a row has grown its market share.

2016 has ended with a record year for the True Fleet EU-5, recording its highest volume as a collective since 2005, registering a little over 2.8 million cars. All countries finished with positive figures, though some more than others.

Looking on the year-to-date figures, the Top 17 brands in True Fleets were all able to raise their volumes compared to 2015. In December, the French car manufacturers were shining especially bright. Renault was in the lead in December with a surplus of + 91.5% and achieving its best market share since October 2005. The biggest part of this increase came from the Megane, Clio and Captur models, where all three earned the December number one spot from their respective vehicle segments. Thanks to a very good performance in the last quarter, the Megane was very close to taking the crown as the number one fleet car for 2016. In the end it was narrowly beaten by the Seat Leon, with the gap was no more than 136 registrations.

Meanwhile Dacia actually doubled its fleet registrations when compared to December 2015, earning rank number nine and an all-time high market share of 4.7% for the Romanian manufacturer!

For the YTD vehicle segment SUV continues to dominate with a share of 29.7% followed by Compact Cars (24.8%) and Small Cars (15.2%). The Middle Class car group is still losing ground with a share of just 13.2% for full year 2016 and only 10.8% in December. This equates to the lowest percentage in the Spanish True Fleet Market ever for the likes of Volkswagen Passat, Audi A4, BMW 3 Series, Opel Insignia or Mercedes C Class.

Italy

The Italian True Fleet Market has had a tremendous 2016. Not only did it achieve its best year and its best December numbers since Italian Dataforce statistics began in 2004 but with true style and flair registered the highest monthly growth rate of 2016 with a + 45.2% against its 2015 comparative month. Passenger Car Total Market also had a standout 2016 registering 1,864,018 vehicles and delivering on its 5th consecutive year of growth.

While there were no major surprises in the 2016 Top 20 brands there were some excellent growth rates in the year-on-year comparison. Mini managed a + 41.1 which secured them 18th place, Toyota produced + 42.5% jumping to 11th place but the largest growth came from Hyundai which delivered a + 56.4%, moving them into 20th position. This was achieved in no small part by the domination of the Tucson which accounted for a staggering 65.8% of all True Fleet Hyundai’s for 2016. Just outside the Top 20 though there were two SUVs that delivered stand out numbers for their manufacturer.

Maserati’s Levante delivered another record month of registrations, beating itself again to take the position of best True Fleet monthly volume for a Maserati ever. While the F-Pace became the Jaguar camp’s most registered model for True Fleet since 2005 delivering 45.7% of all Jaguar registrations for 2016.

As we continued our look through Italy’s Top 20, December data showed noticeable growth from Lancia, Nissan and Volvo with these manufacturers achieving three digit growth numbers of + 270.4, + 153.2, and + 113.6% respectively. Again we cannot finish the press release without mentioning Italy’s #1 manufacturer. Not only were December’s Top 5 model positions all claimed by Fiat’s 500, Panda, 500X, Tipo and the 500L but combined these managed to account for a remarkable 19.9% of all the Italian monthly True Fleet volume.

Germany

Boom! We have a new all-time record: with almost 829,000 new passenger car registrations the German True Fleet Market achieved its new record outpacing 2015 (which was already a record year) by + 5.3%. Although the fourth quarter was not as impressive as the first three, by years end 10 out of the 12 months produced a growth against its 2015 comparative month.

Compared to last year the Top 9 brands all kept their positions and achieved an increasing in volume with the exception of the market leader. Just behind the Top 4 of Volkswagen (#1 position) and the three premium brands Audi, BMW and Mercedes, Ford and Skoda both raised their fleet registrations with double-digit growth rates (+ 11.5% and + 10.2% respectively). Opel, Renault and Seat followed with Nissan able to enter the Top-10 with a very impressive performance of + 48.4%.

Within Ford the biggest part of the up growth was caused by the new generations of the vans Galaxy and S-Max (who is leading the Large Van segment) additionally supported in volume growth by the all new SUV Ford Edge and the Sports Car Ford Mustang. And we are not talking about an exotic player given the fact that the Mustang is positioned just below the Audi TT and six places above the Mazda MX5 in the True Fleet Model ranking 2016. At Skoda the Superb pushed the brand’s success with an increase of almost 130% and being the strongest importer model in the Middle Class behind Volkswagen Passat, Audi A4, BMW 3 Series and Mercedes C-Class.

France

Similar to Germany the True Fleet Market of its western neighbour state France achieved a new all-time record as well. With a count of more than 467,000 new passenger car registrations for the full year 2016 the growth rate amounted to an impressive + 9.0%. As the Private Market growth was flat (+ 0.3%), the Total Market share of both True Fleets and Special Channels (Short Term Rentals, Dealerships/Manufacturers) peaked with 23.2% and 27.3% respectively.

Market leader Renault was able to increase the fleet volume with a double-digit growth of +11.4% followed by Peugeot, Citroen and Volkswagen. On ranks number 5-7 we can find the premium package of BMW, Audi and Mercedes all significantly growing with rates of 15.9%, 10.9% and 15.5%. The Top 10 list is completed by Nissan, Ford and Opel.

The analysis on model level underlines the dominance of the home brands. Volkswagen Golf as the first non-French competitor is ranked 12th in 2016. Beside the Golf only Nissan Qashqai, Volkswagen Passat and Audi A4 were able to find a place within the 20 most preferred models for French company car drivers.

Eight years of consecutive growth finally brought the SUV to the vehicle segment pinnacle. Pushing its volume above 2015’s by a remarkable 29.5%, SUV finally took the crown from Small Cars. The most popular market players are Renault Kadjar and Renault Captur followed by Nissan Qashqai, Peugeot 2008, Volkswagen Tiguan and BMW’s X1 which gained no less than 17 positions in the ranking.

UK

Overall the UK Total Market finished with 2,692,786 registrations generating a +2.3% for its year on year comparison but as we know from previous releases it was clear to see the market endured a turbulent 2016. True Fleet for the most part remained positive and while the market stumbled slightly in the months preceding the Brexit vote, it finished well and delivered a + 2.9% for the full year.

Within the Top 10 brands of 2016 BMW, Mercedes, Kia and Audi were the only manufacturers to improve in the year-on-year comparison. Kia had the largest growth with + 39.0%, followed by BMW with a + 22.3%, Mercedes with + 17.9% and Audi on + 12.8%. It was interesting to see that while the German manufacturer’s predominately achieved this through registration of Compact or Middle Class cars, Kia delivered with an SUV. The Sportage once again dominated the Korean manufacturer’s volume for the year providing 66.4% of all registrations for the brand with an amazing increase of 15.0% over the 2015 percentage total.

In the vehicle segment, SUV’s dominance continues un-abated increasing its market share by 2.9% for 2016. In the SUV model Top 5 the Nissan Qashqai retained its #1 position followed by the Kia Sportage (moving up from 5th), the Opel Mokka (dropping from 2nd), and the Ford Kuga (remaining in 4th), with the Hyundai Tucson rounding out the 5 with the largest lift in rank (moving up from 19th). Notable mentions within the Top 20 must also go to the Renault Kadjar which had a stellar year registering a + 655.3% growth (moving from 33rd to 7th) and also the Jeep Renegade delivering a + 170.0% (moving from 30th to 18th).

Rounding out our UK press release we looked at Top 10 manufacturers for December. While the VW group is still mired in controversy surrounding the emissions scandal there was at least some good news from the UK. Three out of the 4 double-digit growth brands were part of the group, VW produced + 17.0, Audi delivered a + 27.9% with Skoda registering + 39.0%. After looking deeper into the Skoda numbers it was refreshing to see that the growth was spread across 5 of the 7 current market models and with the recent addition of the Kodiaq SUV to the line-up Skoda’s 2017 should be even better.

DATAFORCE – Focus on Fleets

Dataforce is the leading provider of fleet market data and automotive intelligence solutions in Europe. In addition, the company also provides detailed information on sales opportunities for the automotive industry, together with a wide portfolio of information based on primary market research and consulting services. The company is based in Frankfurt, Germany.

Benjamin Kibies

Automotive Analyst

Dataforce Verlagsgesellschaft für

Business Informationen mbH

Hamburger Allee 14

60486 Frankfurt am Main

Telefon +49 69 95930-232

Fax +49 69 95930-549

E-Mail benjamin.kibies@dataforce.de

Web www.dataforce.de

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release True Fleet in 2016 ends with bang for the EU-5 here

News-ID: 425924 • Views: …

More Releases from Dataforce Verlagsgesellschaft für Business Informationen mbH

What is the Dataforce Sales channel outlook for 2021?

Following a contraction of around 26% in 2020 things can only get better. But how fast will the recovery be and what is the outlook for the channels?

Slow start, rev up

We expect the first half year of 2021 to remain rather challenging. Strict Containment measures will probably need to be maintained into spring, which will weigh down economic sentiment. At the same time, early 2021 may not be the best…

Generation change at Dataforce: Marc A. Odinius now sole owner and Managing Dire …

The long-standing Managing Director Marc Odinius has acquired all shares of the Dataforce Verlagsgesellschaft für Business Informationen mbH and is now Managing Director and sole owner of the Company.

Mission of Dataforce

As to the mission of the automotive data- and market-research company, with 87 Employees, counting 27 different nationalities who reside in Frankfurt, Rome and Beijing, Odinius stated: Dataforce is always in search of unique information which will make the automotive…

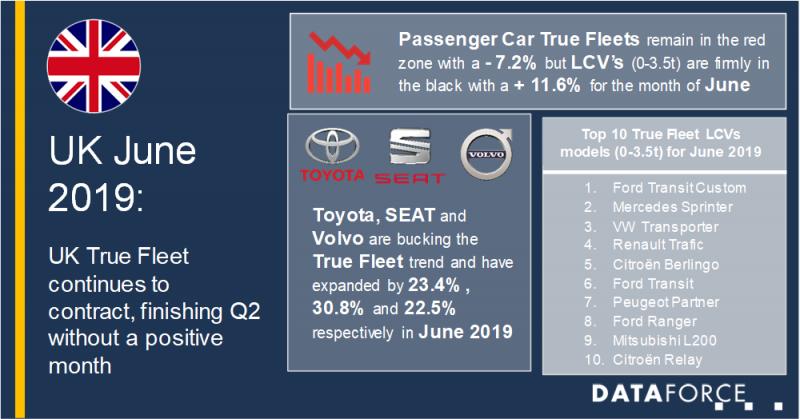

UK True Fleet continues to contract, finishing Q2 without a positive month

Now with the first half of the year having gone by in a blur of negative growth we can only hope that the second half will bring some more positive momentum especially around the plate change month in September. UK True Fleet produced a - 7.2% in June which leaves the channel down 6.2% year-to-date (YTD). The Private Market was also in the red with a 4.8% which…

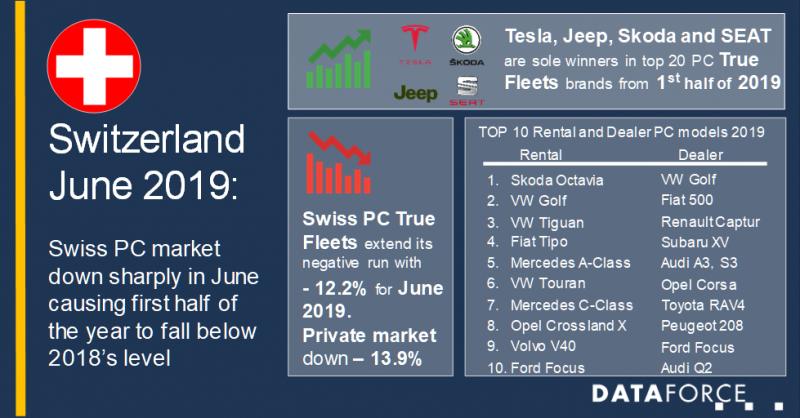

Swiss car market turns into the red on sharp contraction in June

In June 2019 new passenger car registrations in Switzerland were down sharply on the same month last year. Nearly 28,000 registered passenger cars represent an overall market decline of 11.2%. Registrations of light commercial vehicles fell even more sharply (11.9%).

Weak June causes passenger car market to fall below previous year's level

Both the Private Market ( 13.9%) and the commercial market ( 8.4%) can look back on a weak…

More Releases for Fleet

Fleet Tracking and Logistics Market is thriving worldwide by 2027 | Top Key Play …

Fleet Tracking and Logistics Market research is an intelligence report with meticulous efforts undertaken to study the right and valuable information. The data which has been looked upon is done considering both, the existing top players and the upcoming competitors. Business strategies of the key players and the new entering market industries are studied in detail. Well explained SWOT analysis, revenue share and contact information are shared in this report…

Fleet Management Consulting Service Market will reach USD 39.94 Billion by 2032 …

The global fleet management size is expected to grow USD 39.94 Billion by 2032 from USD 21.6 Billion in 2021, at a Compound Annual Growth Rate (CAGR) of 10.5% during the forecast period.

The presence of various key players in the ecosystem has led to a competitive and diverse market. The market include a high growth rate for the adoption of cloud computing and analytics, declining hardware and IoT connectivity costs,…

Fleet Management Solution Market: Start managing fleet data, access and update i …

The report "Global Fleet Management Solution Market By Deployment Model (On-premise, and On-Demand Hybrid), By Solution (Asset Management, Information Management, Driver Management, Safety and Compliance Management, Risk Management, Operations Management, and other Solutions), By End User (Transportation, Energy, Construction, Manufacturing, and Other End Users), and Region - Global Forecast to 2029". Gradually adopting transportation by businesses to enhance their offerings this results in considerable rise over the past few years…

Fleet Management Market Insights | Key players: ARI Fleet Management, Azuga, Che …

According to recent research "Fleet Management Market by Solution (Operations Management, Vehicle Maintenance and Diagnostics, Performance Management, Fleet Analytics and Reporting), Service (Professional and Managed), Deployment Type, Fleet Type, and Region - Global Forecast to 2023", the global fleet management market size is expected to grow from USD 15.9 billion in 2018 to USD 31.5 billion by 2023, at a Compound Annual Growth Rate (CAGR) of 14.7% during the forecast…

Fleet software comm.fleet: Effective cost control for fleet managers

Relief for fleet managers: identify the cost drivers of the company and take appropriate actions with the fleet management software comm.fleet

The adoption of a multifunctional controlling system is an indispensable prerequisite for an effective and systematic management of all company fleet costs. Be it a question of planning enhancement and control, budgeting coordination or the execution and analysis of a target-performance comparison with the purpose of a perfect fleet administration,…

Fleet Specialisation-Cover 4 Fleet Insurance Investigate Future Fleet Trends

Victoria, London ( openpr ) June 10, 2011 - Economically driven by the need to immerse their resources in core activities, companies will turn to fleet outsourcing options. Even in the case of fleet contract hire, there are case studies which are dramatic in the current economic environment.

Take the case study of Fraikin , which was originally established in France in 1944 and is today the biggest commercial…