Press release

ASEAN EV Mobility Infrastructure Market: Charging Stations, Software and Energy Systems

QY Research can provide sample pages, table of contents, supplier coverage, pricing logic, market size, CAGR, gross margin etc.

Southeast Asia's EV market is entering a new phase. The early story was about electric cars, scooters, buses and battery factories. The next story is about the infrastructure that makes electrification usable at scale: charging availability, charger uptime, digital payment, energy management, battery monitoring, fleet scheduling and mobility data integration.

This matters because EV adoption does not scale on vehicle supply alone. A taxi operator cannot electrify a fleet if charging queues are unpredictable. A logistics company cannot commit to electric vans if depot charging is unreliable. A city cannot electrify buses if power connection, charging management and route scheduling are not coordinated. Smart mobility infrastructure is therefore becoming the operating system of the EV transition.

For manufacturers, exporters and investors, Southeast Asia is attractive because it combines high urban density, two-wheeler mobility, ride-hailing, bus modernization, e-commerce logistics, government incentives and a fast-growing Chinese EV supply chain presence. The opportunity is not only hardware sales. It extends across chargers, charging modules, payment platforms, fleet software, energy storage, grid services, battery swapping, telematics and maintenance networks.

Market Definition: More Than Charging Stations

EV Smart Mobility Infrastructure refers to the integrated physical and digital infrastructure that supports electric mobility use cases across private vehicles, two-wheelers, ride-hailing, buses, logistics fleets, taxis, commercial depots and urban transport systems.

• Charging hardware: AC chargers, DC fast chargers, high-power chargers, pantograph bus chargers and portable chargers.

• Power electronics and modules: charging modules, rectifiers, power cabinets, connectors, cables, cooling components and metering devices.

• Digital charging platforms: charger management systems, payment apps, roaming, load balancing, uptime monitoring and customer analytics.

• Fleet and mobility software: route planning, telematics, battery state-of-health monitoring, depot scheduling and driver behavior analytics.

• Energy infrastructure: transformers, switchgear, energy storage, solar-plus-charging integration, V2G readiness and utility connection services.

• Battery swapping and service networks: two-wheeler swapping, taxi fleet battery services and commercial vehicle energy-as-a-service models.

The key point for investors is that EV Smart Mobility Infrastructure is a system market. A charger without software has weak operating leverage. Software without enough chargers has limited network value. Grid equipment without fleet demand is underutilized. The strongest platforms combine hardware deployment, utilization data, energy optimization and customer access.

Value Chain: Where the Profit Pools Are Moving

The market opportunity stretches from upstream power electronics to downstream mobility operations. Suppliers should avoid treating Southeast Asia as a simple charger export market; the region increasingly requires localized deployment, interoperability, financing and maintenance.

• Upstream components: SiC/GaN power modules, charging modules, connectors, cables, displays, payment terminals, relays, metering chips, embedded controllers and battery management components.

• Midstream equipment: AC wallboxes, DC fast chargers, charging cabinets, battery swapping cabinets, bus chargers, depot charging systems and energy storage integration.

• Software layer: charging management systems, mobile payment, roaming, fleet scheduling, battery analytics, load management, cybersecurity and data dashboards.

• Deployment layer: charging point operators, utilities, EPC contractors, landlords, parking operators, petrol station operators, fleet owners and public transport agencies.

• Downstream users: private EV owners, ride-hailing drivers, taxi fleets, bus operators, e-commerce logistics, delivery platforms, factories, commercial buildings and municipal transport systems.

The margin opportunity shifts upward when suppliers move from selling equipment to managing uptime, utilization, software, service contracts and energy optimization.

Market Size and Growth Outlook

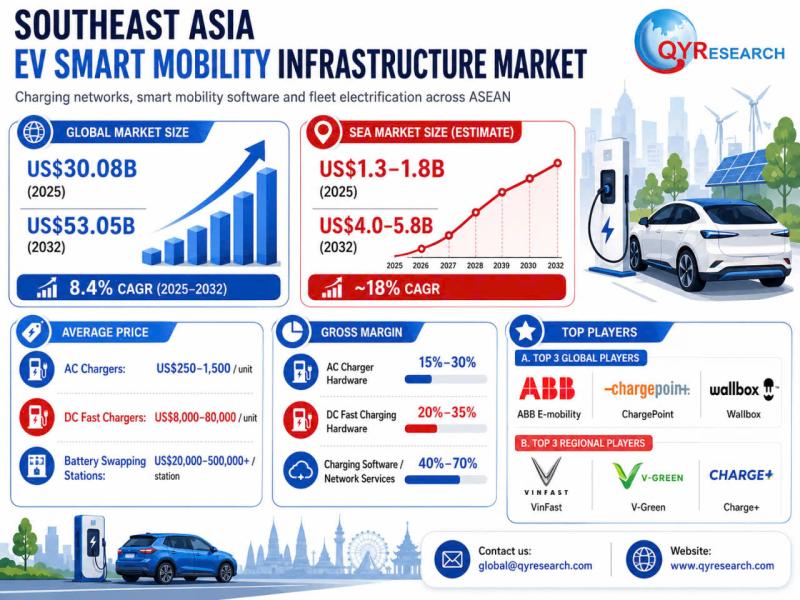

QY Research public-indexed benchmark data indicates that the global Electric Vehicle Charging and Swapping Station market was valued at approximately US$30.08 billion in 2025 and is expected to reach around US$53.05 billion by 2032. QY Research also indicates that the global EV DC Fast Charger market is projected to grow from US$5.18 billion in 2025 to US$20.30 billion by 2032, while the global Electric Vehicle Home Charger market is estimated at US$4.08 billion in 2025 and US$20.27 billion by 2032.

For Southeast Asia, QY Research estimate for the addressable EV Smart Mobility Infrastructure market is approximately US$1.3-1.8 billion in 2025, with potential to reach US$4.0-5.8 billion by 2032. This estimate includes charging hardware, charging management software, fleet charging systems, depot infrastructure, battery swapping systems, payment/roaming platforms and energy management integration. It excludes the value of EV vehicles themselves.

The implied regional growth is faster than many mature markets because Southeast Asia is scaling from a lower infrastructure base while EV adoption is accelerating. The region's bottleneck is not only vehicle affordability; it is charging density, grid connection, charger reliability and operating economics.

• AC home and destination chargers: estimated hardware price range of US$250-1,500 per unit depending on power, connectivity and certification.

• Public AC chargers: estimated US$800-3,500 per charger, before installation and civil works.

• DC fast chargers: estimated US$8,000-80,000 for 30-180 kW units; high-power systems can exceed US$100,000-200,000 per charging point.

• Battery swapping cabinets/stations: estimated US$20,000-500,000+, depending on two-wheeler, passenger car or fleet format.

• Gross margin estimate: basic AC charger hardware 15-30%, DC fast charging hardware 20-35%, charging software/network services 40-70%, with project margins dependent on utilization, land cost and electricity tariff.

Demand Evidence: EV Adoption Is Outrunning Infrastructure Comfort

The demand signal is becoming clearer. According to the International Energy Agency, Southeast Asia electric car sales more than doubled in 2025 to more than half a million units, representing close to one in five new cars sold across the region. The growth was led by Viet Nam, Indonesia and Thailand, supported by policy incentives, domestic manufacturing and lower-cost imports, particularly from China.

The interpretation is not simply that more EVs are being sold. It is that mobility infrastructure must become smarter as utilization rises. Early adopters can tolerate limited charging options. Fleet operators cannot. When EVs move into taxis, delivery vans, buses and company fleets, the infrastructure requirement becomes operational: chargers must be available, monitored, billed, maintained and connected to energy systems.

This is why Southeast Asia's EV infrastructure demand is likely to be fleet-led and city-led before becoming fully mass-market. Ride-hailing vehicles, urban delivery fleets, airport taxis, bus depots, shopping malls, commercial buildings, logistics parks and residential compounds will become the most important demand pools.

Charging Targets Create a Visible Infrastructure Pipeline

Policy targets are not sales orders, but they matter because they define the scale of infrastructure that governments, utilities and private operators are trying to unlock. The IEA notes that Indonesia aims to reach 30,000 charging stations by 2030, while Thailand targets 12,000. These targets create demand visibility for chargers, grid connection, site acquisition, payment platforms, maintenance services and utility coordination.

The commercial implication is clear: charging infrastructure is moving from pilot installation to network planning. The next phase will reward companies that can provide site selection, grid assessment, charger utilization analytics, maintenance response, software uptime and integrated payment systems, not only imported charging hardware.

Country Dynamics: Uneven Adoption, Different Entry Strategies

• Viet Nam: The market is led by domestic EV adoption and a concentrated charging ecosystem. VinFast's scale, V-Green's infrastructure role and electric taxi deployment make Viet Nam a high-growth but relatively closed ecosystem. Opportunities exist in fleet software, maintenance, energy storage, charging components and B2B depot infrastructure.

• Thailand: Thailand is the region's automotive manufacturing hub. EV incentives, Chinese OEM investment and domestic production requirements create demand for public chargers, dealership charging, factory charging, logistics fleets and industrial park infrastructure. The market is competitive and increasingly professional.

• Indonesia: Indonesia's advantage is scale: population, nickel/battery ecosystem, logistics demand and government ambition. The opportunity is long-term and large, but execution depends on grid readiness, site economics, charging utilization and regional coverage outside Jakarta and Java.

• Malaysia: Adoption is lower than Thailand and Viet Nam but supported by import incentives, national EV policy and a strong electronics/industrial base. The opportunity is attractive for premium residential chargers, commercial buildings, fleet depots, smart parking and energy management.

• Singapore: Singapore is small but high-value. It is a reference market for charging software, fleet electrification, payment interoperability, smart parking, urban logistics, regulatory-grade mobility data.

• Philippines: EV adoption accelerated from a low base. The near-term market is likely to be project-based: malls, commercial buildings, fleet depots, public transport, two-wheelers, logistics corridors.

Competitive Landscape: Hardware Is Global, Deployment Is Local

The market includes global charger OEMs, Chinese power-electronics suppliers, utilities, petrol station operators, fleet platforms, local EPCs, software firms and EV manufacturers. No single supplier type owns the whole value chain. Hardware suppliers need local partners. Charging point operators need reliable equipment and financing. Fleet operators need software. Utilities need load visibility.

Global / Multinational Supplier Groups

• ABB - DC fast chargers and fleet charging systems

• Siemens - EV chargers, grid connection and eMobility software

• Schneider Electric - energy management and charging infrastructure solutions

• Delta Electronics - AC/DC chargers and power electronics modules

• Kempower - modular DC fast charging systems for fleets

• Tritium - liquid-cooled DC fast charging hardware

• ChargePoint - networked charging software and station management

• Wallbox - connected residential and commercial EV chargers

• StarCharge - EV chargers and energy management platforms

• TELD - charging network technology and platform solutions

• Huawei Digital Power - high-power charging and energy management solutions

• Autel Energy - smart AC/DC charging equipment and software

• BYD - EV ecosystem, charging and battery technology

• Tesla - destination charging and high-power charging ecosystem

• Shell Recharge - charging network operation and energy retail

Regional and Local Southeast Asian Players

• V-Green (Vietnam) - Charging network operator and VinFast infrastructure partner

• VinFast (Vietnam) - EV manufacturer with integrated charging ecosystem

• GSM / Green SM (Vietnam) - Electric taxi and fleet mobility operator

• SP Group (Singapore) - EV charging network and energy utility operator

• Charge+ (Singapore) - Public and residential EV charging operator

• ComfortDelGro (Singapore) - Fleet operator and mobility electrification player

• Gentari (Malaysia) - Clean energy and EV charging infrastructure operator

• TNB Electron (Malaysia) - Utility-backed EV charging infrastructure network

• JomCharge / EV Connection (Malaysia) - Charging network and installation service provider

• EVLOMO (Thailand) - EV charging and battery infrastructure developer

• PTT OR EV Station PluZ (Thailand) - Petrol-station-linked EV charging network

• EA Anywhere (Thailand) - EV charging network and energy ecosystem player

• EGAT / EleX by EGAT (Thailand) - Utility-linked charging infrastructure provider

• PLN (Indonesia) - National utility and SPKLU charging infrastructure operator

• Voltron (Indonesia) - EV charging network and platform operator

• Starvo (Indonesia) - EV charging station provider and CPO partner

• Mober (Philippines) - Electric logistics fleet and charging user

• Meralco / MServ (Philippines) - Utility and EV charging solutions provider

• Grab (Regional) - Ride-hailing and fleet electrification demand aggregator

• SWAT Mobility (Singapore) - Fleet routing and mobility optimization software

Local players may not dominate the manufacturing of high-power charger modules, but they are increasingly important in site access, permitting, utility coordination, fleet relationships, software localization and maintenance execution. For foreign charger exporters, local partners often determine whether a product becomes a deployed network or remains a catalog item.

Opportunities for Manufacturers, Exporters and Investors

• Target fleet depots before mass public charging: taxis, buses, logistics vans and corporate fleets deliver more predictable utilization than low-density public sites.

• Bundle hardware with software: operators increasingly need charging management, billing, load balancing, uptime monitoring and driver apps.

• Develop mid-cost DC fast charging portfolios: Southeast Asia needs robust and affordable 60-180 kW chargers more than premium ultra-high-power systems in many early corridors.

• Support two-wheeler and delivery electrification: battery swapping, small-format chargers and fleet dashboards can scale faster than passenger-car-only infrastructure.

• Partner with utilities and property owners: grid connection, transformers, substations, parking access and electricity tariffs are decisive project variables.

• Create after-sales capability: charger downtime damages user trust; maintenance response and spare parts availability can become a competitive differentiator.

• Monitor software profit pools: recurring revenue may come from charging management, fleet analytics, roaming, payment integration and energy optimization.

The near-term opportunity is not to build the largest number of chargers; it is to build the most utilized, reliable and digitally managed charging assets.

Risks and Barriers to Monitor

• Utilization risk: low early traffic can make public chargers financially unattractive without fleet anchors or subsidies.

• Grid connection bottlenecks: transformer capacity, permitting, peak demand charges and land availability can delay deployment.

• Standards and compatibility: CCS, GB/T, CHAdeMO, NACS-related developments and OEM-specific requirements can complicate procurement.

• Price competition: Chinese chargers and EVs may reduce hardware margins while accelerating adoption.

• Policy volatility: incentives, import duties, battery localization rules and tax exemptions can change demand quickly.

• Operational reliability: charger downtime, payment failure and poor service can slow consumer trust.

• Capital intensity: charging point operators must finance equipment, construction, electricity connection and maintenance before utilization matures.

• Cybersecurity and data concerns: connected charging platforms process payment, vehicle, location and energy data, creating security and privacy risks.

Geopolitical and Supply Chain Factors

The most relevant geopolitical factor is China's growing role in EV exports, battery supply and charger hardware. Lower-cost Chinese EVs are accelerating adoption across Southeast Asia, but they also increase exposure to standards, tariffs, battery chemistry shifts and political scrutiny. For local governments, the strategic question is how to attract EV investment while building domestic capabilities in batteries, power electronics and charging infrastructure.

Battery supply is another major factor. Indonesia is positioning itself around nickel and battery materials, but the global shift toward LFP batteries reduces the certainty that nickel alone will define regional EV competitiveness. Thailand is using automotive policy to attract EV production. Viet Nam is building a domestic EV ecosystem around VinFast. Singapore and Malaysia are focusing more on software, grid, urban infrastructure and higher-value services.

For suppliers, geopolitics changes sourcing strategy. Buyers may ask for alternative manufacturing locations, local service, cybersecurity documentation, software data hosting options and compliance with local grid and payment standards. ASEAN can benefit as a neutral deployment region, but infrastructure investors must monitor policy changes closely.

Future Outlook: From Charging Deployment to Mobility Infrastructure Platforms

Southeast Asia's EV Smart Mobility Infrastructure market is unlikely to grow evenly. It will develop in waves: first in high-density urban areas, then fleet depots and logistics corridors, then residential compounds and intercity travel routes. The winners will not necessarily be the lowest-cost charger suppliers. They will be companies that can solve the full operating problem: where to charge, when to charge, how to pay, how to balance load, how to maintain uptime and how to optimize fleets.

Demand will increasingly shift from standalone equipment toward managed infrastructure. Charging hardware will remain necessary, but differentiation will come from software, energy integration, utilization analytics, interoperability and service contracts. As EV penetration rises, the cost of unreliable charging will increase for consumers, fleets and cities. That makes smart infrastructure more valuable.

For investors, the market deserves monitoring because it sits at the intersection of transport electrification, urban infrastructure, grid modernization, battery supply chains and digital mobility platforms. Southeast Asia may not be the largest EV market globally, but it may become one of the most dynamic markets for practical, cost-sensitive and fleet-oriented EV infrastructure deployment.

Final Conclusion

EV Smart Mobility Infrastructure may not be as visible as electric vehicles themselves, but it will increasingly determine whether EV adoption scales profitably in Southeast Asia. The region's next phase is not only about selling more EVs; it is about building the charging, energy, payment, data and fleet-management systems that allow EVs to become reliable daily infrastructure.

For manufacturers and exporters, the opportunity is to provide reliable chargers, power modules, energy systems and software-ready devices. For charging operators and utilities, the opportunity is to build high-utilization networks and fleet charging hubs. For investors, the opportunity is to identify the platforms that can convert early EV adoption into recurring infrastructure revenue. This market deserves close monitoring because it is becoming foundational to Southeast Asia's mobility transition.

Report Coverage and Related QY Research Reports:

The full QY Research report can cover market definition, market size, CAGR, product segmentation, pricing logic, gross margin indicators, key companies, country outlook, charging use cases, fleet electrification, energy management, competitive landscape and customized regional analysis.

Contact Information:

Tel: +1 626 2952 442 (US); +86-1082945717 (China); +84 865 216594 (Vietnam)

Email: global@qyresearch.com; tranlethanhhang@qyresearch.com

Website: www.qyresearch.com

Address: Room 2905, Vili International, 167 Linhe West Road, Tianhe District, Guangzhou, Guangdong Province, China

About QY Research

QY Research has established close partnerships with over 71,000 global leading players. With more than 20,000 industry experts worldwide, we maintain a strong global network to efficiently gather insights and raw data. Our 36-step verification system ensures the reliability and quality of our data. With over 2 million reports, we have become the world's largest market report vendor. Our global database spans more than 2,000 sources and covers data from most countries, including import and export details. We have partners in over 160 countries, providing comprehensive coverage of both sales and research networks. A 90% client return rate and long-term cooperation with key partners demonstrate the high level of service and quality QY Research delivery. More than 30 IPOs and over 5,000 global media outlets and major corporations have used our data, solidifying QY Research as a global leader in data supply. We are committed to delivering services that exceed both client and societal expectations.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release ASEAN EV Mobility Infrastructure Market: Charging Stations, Software and Energy Systems here

News-ID: 4544081 • Views: …

More Releases from QY Research

Top 30 Indonesian Cotton Spun Yarn Public Companies Q3 2025 Revenue & Performanc …

1) Overall companies performance (Q3 2025 snapshot)

PT Indo-Rama Synthetics Tbk

PT Sri Rejeki Isman Tbk

PT Pan Brothers Tbk

PT Trisula Textile Industries Tbk

PT Asia Pacific Fibers Tbk

PT Asia Pacific Investama Tbk

PT Argo Pantes Tbk

PT Century Textile Industry Tbk

PT Century Textile Industry Tbk

PT Eratex Djaja Tbk

PT Ever Shine Tex Tbk

PT Sunson Textile Manufacturer Tbk

PT Tifico Fiber Indonesia Tbk

PT Ricky Putra…

How Nanotechnology is Transforming UV Protection Across Coatings, Plastics, Elec …

The global UV Blocking Nanoparticle Additives market is entering a period of non-linear value creation as end-users increasingly prioritize performance, durability, transparency, and multifunctionality over conventional UV stabilizers. Historically, demand growth was driven primarily by volume expansion in plastics, coatings, and personal care products. However, the industry is now shifting toward engineered nanomaterials with controlled particle morphology, narrow size distributions, advanced surface treatments, and application-specific formulations.

This transition is transforming the…

From Structural Adhesives to Battery Systems: Toughening Nanoparticles Become a …

The global Toughening Nanoparticle Additives market is entering a period of non-linear value inflection as demand shifts away from conventional commodity fillers toward engineered nano-scale performance enhancers capable of improving fracture toughness, fatigue resistance, thermal stability, and structural durability. Historically, the market expanded primarily through incremental volume growth within coatings and adhesives. The current investment cycle is increasingly driven by aerospace composites, electric vehicles, wind turbine blades, advanced electronics, and…

From Consumer Device to Connected Health Platform: The Investment Case for Elect …

The global electronic blood pressure meter market is entering a phase of non-linear value creation driven by the convergence of chronic disease management, remote patient monitoring, and connected healthcare infrastructure. While the industry historically competed on unit volume and low-cost manufacturing, capital allocation is increasingly shifting toward software-enabled diagnostics, cloud-based patient management systems, and AI-assisted cardiovascular monitoring. This transition is altering margin structures across the value chain and creating differentiated…

More Releases for Southeast

Commercial Plumbing Services Across the Southeast

Performance Plumbing Inc. announced continued commercial plumbing service operations across multiple Southeastern states. The company provides installation, repair, maintenance, hydro jetting, slab plumbing, and water heater services for commercial properties.

Birmingham, Alabama, United States, 20th May 2026 - Columbiana, Alabama, Performance Plumbing Inc. announced continued expansion and availability of its commercial plumbing services for businesses throughout Alabama, Tennessee, Mississippi, and Georgia. The company provides commercial plumbing solutions for a range of…

Residential Construction Trends Shaping Southeast Missouri Communities

Residential development across Southeast Missouri is experiencing steady and meaningful growth, driven by changing homeowner expectations, regional economic stability, and an increased focus on long-term living solutions. New Home Construction In Southeast Missouri has become a central topic among families, investors, and local planners who are looking for housing that balances modern design with practical functionality. This growth reflects not only population movement into the region but also a shift…

Home Maintenance Services in Southeast Louisiana: Elevates Home Care, HomeSmiles …

HomeSmiles Southeast Louisiana now offers bundled maintenance packages to enhance the health, safety, and energy efficiency of homes for local homeowners.

Industry analysts note a growing trend toward bundled home services as consumers seek convenience and reliability from trusted providers. Homeowners now have convenient access to professional home maintenance services in Southeast Louisiana [https://homesmiles.com/location/homesmiles-southeast-louisiana/], ensuring their home systems are in optimal operating condition.

HomeSmiles Southeast Louisiana is positioned at the forefront of…

AMCI Support Expands to Southeast Asia (SEA)

AMCI is proud to announce the addition of AVS Control as an official manufacturer's representative for the Southeast Asia (SEA) region.

AVS Control brings a hands-on approach to industrial automation sales and support, offering localized technical guidance to customers throughout the SEA market. With a strong foundation in automation technology and a deep understanding of regional application needs, AVS Control is well positioned to help engineers, OEMs, and system integrators identify…

Southeast Asia Air Conditioners Market

Redding California, February 5, 2024- Meticulous Research®, a leading global market research company, has unveiled its latest research report titled "Southeast Asia Air Conditioners Market by Type (Split, Window, Centralized/Ducted, Others), Tonnage (Up to 2 Tons, 2 Tons to 5 Tons, Others), Technology (Inverter, Non-inverter), End User (Residential, Commercial, Industrial), and Geography-Forecast to 2030." Published in [Month] 2023, the report forecasts the Southeast Asia air conditioners market to achieve a…

Opportunities For Cheese Innovation In Southeast Asia

Summary

There is great growth potential for cheese in Southeast Asia. Rapid urbanization, greater travel, and an influx of Western expatriates are creating greater exposure to other cultures and international cuisines, which is an important driver for cheese innovation in the region. There is greater awareness and penetration of milder cheeses like cheddar and mozzarella, due to their versatility for home cooking and immediate consumption, and availability through Western foodservice offerings…