Press release

Automotive Bioplastics Face a Profitability Paradox as Regulatory Pressure Mounts

Automotive Bioplastics Market

The Compliance Trap That's Reshaping Material Economics

Automakers are discovering that meeting 2025-2030 emissions and recyclability mandates isn't just about electrification. Material composition now directly impacts regulatory compliance scores, fleet-level carbon accounting, and increasingly, consumer purchasing decisions in key markets. The challenge: bioplastics currently cost 20-40% more than conventional petroleum-based alternatives, yet regulatory frameworks in the EU, California, and emerging Asian markets are making their adoption less optional by the quarter.

This isn't a gradual transition. Manufacturers who treat bioplastics as a future consideration rather than a current procurement priority are building compliance risk into every vehicle platform they design today. The material decisions made in 2025 will determine which OEMs face costly redesigns, supply chain disruptions, or market access restrictions by 2027.

Request Report Sample: https://marketmindsadvisory.com/request-sample/?report_id=16780

Why Waiting for Cost Parity Is the Wrong Strategy

The conventional wisdom suggests waiting until bioplastic costs converge with traditional plastics before committing to large-scale adoption. This logic ignores three accelerating realities that are fundamentally altering the business case.

First, regulatory timelines are compressing. What were once 2030 targets are becoming 2026-2027 compliance requirements in major markets. The EU's End-of-Life Vehicles Regulation and California's Advanced Clean Cars II standards are creating hard deadlines that don't accommodate gradual material transitions.

Second, the total cost equation is shifting. When factoring in carbon border adjustment mechanisms, extended producer responsibility fees, and the growing price premium consumers will pay for demonstrably sustainable vehicles, the cost gap narrows considerably. Early movers are discovering that bioplastic adoption, when integrated at the platform design stage rather than retrofitted, adds 0.8-1.2% to vehicle costs while potentially commanding 2-3% price premiums in sustainability-conscious segments.

Third, supply chain positioning is becoming winner-take-all. The limited number of suppliers capable of delivering automotive-grade bioplastics at scale means early contract commitments secure preferential pricing, technical collaboration, and supply certainty. Manufacturers entering negotiations in 2026-2027 will face constrained capacity and premium pricing as leading OEMs lock in multi-year agreements.

Three Structural Forces Redefining Material Strategy

The Performance Credibility Threshold

Bioplastics have moved beyond niche interior trim applications. Recent material science advances have produced bio-based polymers matching or exceeding petroleum-based plastics in heat resistance, impact strength, and durability for under-hood and structural applications. This performance parity is eliminating the technical objections that previously justified delayed adoption. The strategic question is no longer "can bioplastics perform?" but "which applications should we prioritize for conversion?"

The Circular Economy Mandate

Automotive manufacturers are being forced to think in closed loops, not linear supply chains. Bioplastics derived from renewable feedstocks and designed for recyclability or composting align with emerging circular economy regulations that will require manufacturers to take back and process end-of-life vehicles. Companies without material strategies that accommodate these requirements are building future liabilities into current production.

The Feedstock Diversification Imperative

Petroleum price volatility and geopolitical supply risks are driving automotive procurement teams to diversify material sources. Bioplastics derived from agricultural waste, algae, or captured CO2 offer supply chain resilience that petroleum-dependent materials cannot. This isn't just environmental positioning; it's risk management. Manufacturers with diversified material portfolios will weather commodity price shocks and supply disruptions more effectively than those locked into conventional plastic dependencies.

Browse the Complete Report: https://marketmindsadvisory.com/automotive-bioplastics-market/

Where Strategic Value Concentrates

The highest-return opportunities in automotive bioplastics aren't evenly distributed across vehicle components. Three application categories are emerging as strategic priorities where early adoption delivers disproportionate value.

Interior components represent the immediate conversion opportunity. Door panels, dashboards, seat structures, and trim elements offer large volume potential with lower performance barriers and faster regulatory payback. These visible applications also provide consumer-facing sustainability messaging that supports brand positioning.

Exterior semi-structural components are the next frontier. Bumper beams, wheel arch liners, and underbody shields are seeing successful bioplastic integration in premium and electric vehicle segments. These applications demonstrate technical credibility while contributing meaningfully to whole-vehicle carbon footprint reduction.

Under-hood applications remain the proving ground for next-generation bioplastics. Engine covers, air intake manifolds, and cooling system components require heat and chemical resistance that only recently became achievable with bio-based materials. Success here signals full material maturity and opens the largest volume conversion opportunities.

The Competitive Repositioning Underway

Traditional material suppliers are facing disruption from unexpected directions. Chemical companies with agricultural or biotechnology capabilities are entering automotive supply chains, bringing different cost structures and innovation approaches than incumbent petroleum-based plastic suppliers. This is fragmenting established supplier relationships and creating opportunities for OEMs willing to work with non-traditional partners.

Premium and electric vehicle manufacturers are using bioplastic adoption as a differentiation strategy, creating a sustainability performance gap that mass-market manufacturers will struggle to close without significant investment. This gap is becoming a competitive moat in markets where environmental credentials influence purchase decisions and regulatory treatment.

The risk of commoditization looms for manufacturers who adopt bioplastics reactively rather than strategically. Simply substituting bio-based materials without redesigning components for performance optimization or cost efficiency will result in higher costs without competitive advantage. The winners will be those who use bioplastic adoption as a catalyst for broader material and design innovation.

The Consequences of Delayed Commitment

Companies postponing bioplastic integration are accumulating risks that compound with each product cycle:

* Stranded platform investments: Vehicle architectures designed around conventional plastics will require costly mid-cycle redesigns to accommodate regulatory changes

* Supply chain disadvantage: Late movers will face constrained supplier capacity, premium pricing, and limited technical support as leading manufacturers lock in preferred partnerships

* Regulatory exposure: Non-compliance penalties and market access restrictions will disproportionately impact manufacturers without credible material transition roadmaps

* Brand positioning erosion: Sustainability laggards will face increasing consumer and investor pressure as competitors establish clear environmental leadership

* Talent attraction challenges: Engineering and design talent increasingly prioritizes employers with genuine sustainability commitments, not aspirational targets

Request Report Customization: https://marketmindsadvisory.com/request-customization/?report_id=16780

What This Means for Decision-Makers

For Automotive OEMs and Tier-1 Suppliers

Material strategy can no longer be delegated to procurement as a cost optimization exercise. This requires executive-level decisions about which vehicle platforms will pioneer bioplastic integration, how to structure supplier partnerships that share development risk, and where to invest in internal material science capabilities versus external partnerships. The manufacturers treating this as a 2027-2028 priority are already behind competitors who began platform integration in 2023-2024.

For Material Suppliers and Chemical Companies

The automotive qualification process is lengthy and unforgiving. Suppliers without existing automotive relationships need to begin certification and testing programs immediately to be viable partners for 2027-2028 vehicle launches. The window for establishing credibility is narrowing as OEMs finalize their preferred supplier networks. Companies with agricultural feedstock access or biotechnology capabilities should be actively pursuing automotive partnerships rather than waiting for inbound inquiries.

For Investors and Capital Allocators

Automotive bioplastics represent a rare combination of regulatory tailwinds, technical maturity, and supply-demand imbalance. Investment opportunities span the value chain from feedstock production to material processing to component manufacturing. The highest returns will likely accrue to companies solving specific technical barriers (heat resistance, cost reduction, recycling infrastructure) rather than generalist bioplastic producers. Due diligence should focus on automotive qualification status, offtake agreements with OEMs, and feedstock security.

For Policymakers and Regulators

The pace of regulatory change is outpacing industry's ability to build supply chain capacity and technical capabilities. Policies that provide clear long-term signals, support recycling infrastructure development, and incentivize early adoption will accelerate the transition more effectively than punitive mandates alone. Coordination between vehicle regulations and material/waste management policies is essential to avoid creating compliance requirements without viable execution pathways.

The material decisions automakers make in the next 18 months will determine their competitive position for the next decade.

The automotive bioplastics transition isn't a distant sustainability initiative; it's an immediate strategic imperative with clear winners and losers emerging by 2027. Manufacturers who integrate bioplastics as part of a broader material innovation strategy will build competitive advantages in cost, compliance, and brand positioning. Those who treat it as a reactive compliance exercise will find themselves perpetually behind, paying premium prices for constrained supply while facing regulatory and market pressures their platforms weren't designed to accommodate. The window for proactive positioning is measured in quarters, not years.

Contact Us

Market Minds Advisory

86 Great Portland Street, Mayfair, London,

W1W 7FG, England, United Kingdom

T: +44 020 3807 7725

Email:sales@marketmindsadvisory.com

Website:https://marketmindsadvisory.com/

LinkedIn: https://www.linkedin.com/company/market-minds-advisory/

Facebook: https://www.facebook.com/resvaultmmadvisory/

Twitter: https://x.com/MarketMindsA

Instagram: https://www.instagram.com/marketmindsadvisory

Why choose Market Minds Advisory

Market Minds Advisory delivers decision-grade intelligence trusted by executives across machinery & equipment, packaging, chemical, automotive, information & communication technology, food & beverage, consumer goods, healthcare and other industries. We provide market expansion strategies, go-to-market strategies, market share acceleration, brand positioning analysis, and account enablement and growth. Our forecasting methodology integrates primary interviews, proprietary demand models and continuous market validation to ensure accuracy in volatile and emerging industries. With over 10 years of industry experience and insights derived from primary interviews with several industry stakeholders, our research provides actionable insights and white space analysis for the emerging segments providing the opportunity gaps in the market accounting recent market developments and geopolitical risks. We believe in unlocking growth by helping businesses to see the future of their markets.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Automotive Bioplastics Face a Profitability Paradox as Regulatory Pressure Mounts here

News-ID: 4494209 • Views: …

More Releases from Market Minds Advisory

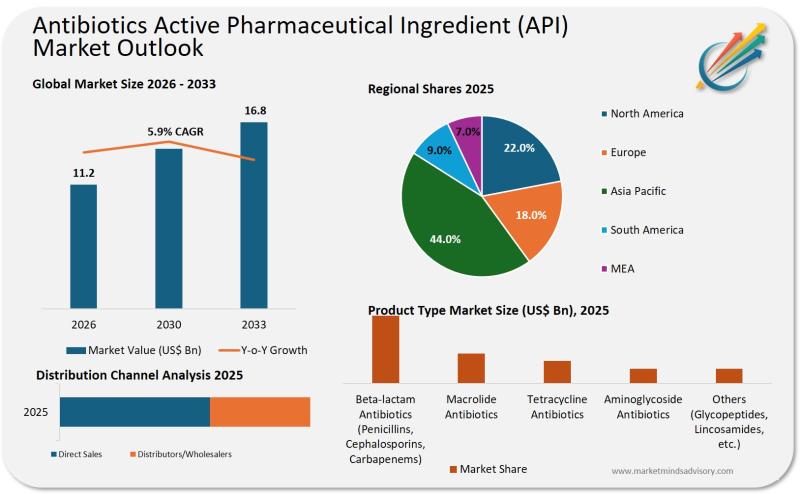

Antibiotics API Supply Chains Are Fracturing And Most Pharma Companies Aren't Re …

The global antibiotics API market is entering a period of structural instability, driven by geopolitical fragmentation, regulatory divergence, and the collapse of economic incentives for new antibiotic development. Companies that fail to reconfigure their sourcing strategies now risk supply disruptions, margin erosion, and regulatory non-compliance within the next 18 to 24 months.

Why This Market Shift Matters Now

For decades, the antibiotics API market operated on a simple logic: consolidate production in…

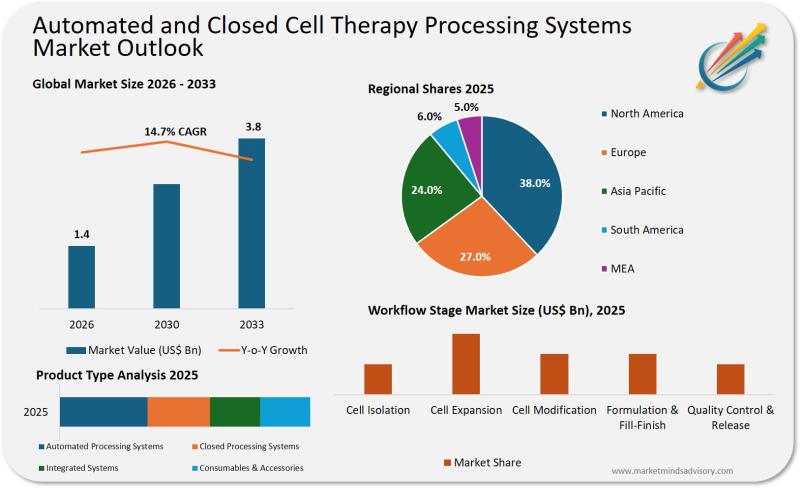

Cell Therapy Manufacturing Is Hitting a Scalability Wall And Most Companies Are …

The promise of personalized medicine is colliding with industrial reality. As CAR-T therapies and regenerative treatments move from clinical trials to commercial scale, manufacturers are discovering that manual processing methods cannot support the volume, consistency, or economics required for mass adoption.

Why Manual Processing Is No Longer Viable

Cell therapy manufacturing today resembles artisan production in an industry demanding automotive-scale precision. Each batch requires specialized cleanroom environments, highly trained personnel, and weeks…

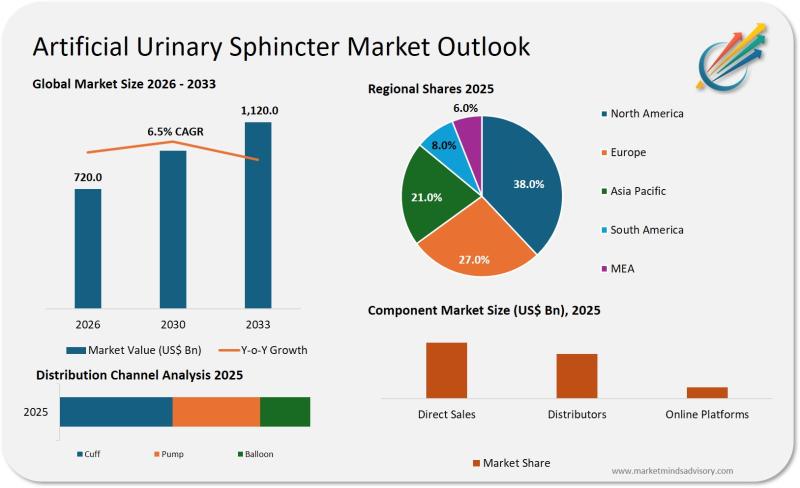

Artificial Urinary Sphincter Market Faces Critical Inflection as Patient Demand …

The gap between clinical need and device evolution is widening, creating strategic risk for medtech players and healthcare systems unprepared for demographic and regulatory shifts.

The Quiet Crisis in Urological Care

Healthcare systems across developed markets are confronting an uncomfortable reality: the population most in need of urinary incontinence solutions is growing faster than the innovation pipeline can support. Artificial urinary sphincters, once considered a mature category, are now at the center…

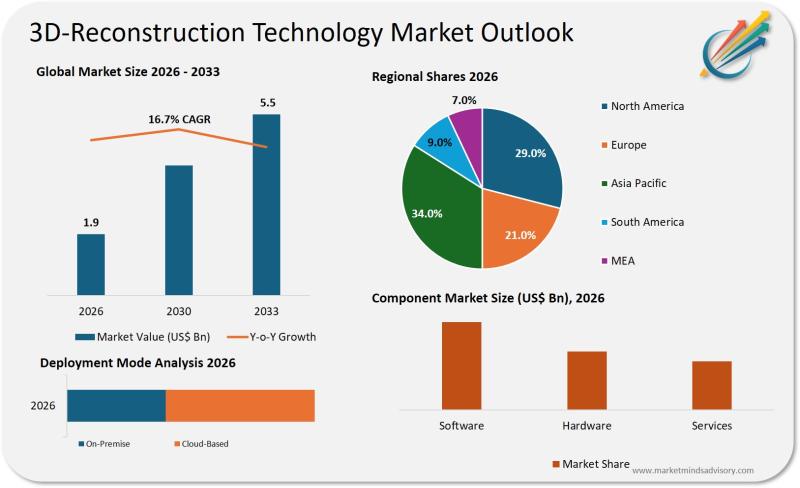

3D Reconstruction Technology Is No Longer Optional It's Infrastructure

Companies treating 3D reconstruction as a visualization tool rather than a strategic capability are already behind. The technology has crossed the threshold from experimental to mission-critical across industries where spatial intelligence determines competitive advantage.

The shift is structural. Organizations that once relied on manual measurement, 2D imaging, or legacy CAD workflows now face competitors deploying real-time 3D reconstruction to compress decision cycles, eliminate rework, and unlock entirely new revenue models. This…

More Releases for Automotive

Automotive Grommet Market set for explosive growth: Cooper Standard Automotive, …

According to HTF MI, "Global Automotive Grommet Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2024-2030". The Global Automotive Grommet Market is anticipated to grow at a compound annual growth rate (CAGR) of 5.96% from 2024 to 2030, reaching USD 100 Billion in 2024 and USD 150 Billion by 2030.

Automotive grommets are protective rings or eyelets made from rubber or plastic, used to protect or cover holes in metal…

KSA Automotive Market | KSA Automotive Industry | KSA Automotive Industry Resear …

Saudi Arabia’s automotive market faced a decline in new car sales due to tripling of value-added tax (VAT) rates. Effective in July 1, 2020, Saudi Arabia hiked its VAT from 5% to 15%.

Vision 2030 trying to attract foreign investment to kick start Dammam manufacturing city to aid re-exports & fulfill domestic demand

Surge in Domestic Manufacturing to gain independence of Imports: With Vision 2030, KSA is trying to gain impendence of…

Automotive Fuel Injectors Market: Growing Automotive Sales Fueling Automotive Fu …

Automotive fuel injectors market is likely to grow at a steady pace in the long run, according to a new report by Fact.MR. The demand for automotive fuel injectors continues to remain influenced with a multitude of industry-specific and macroeconomic factors. Significant growth in the automotive sector, coupled with increasing vehicle fleet remain instrumental in driving the demand for automotive fuel injectors worldwide. Fact.MR estimates that the sales of automotive fuel injectors are expected…

Global Automotive Safety Market 2019 Worldwide Outlook By Autoliv, Delphi Automo …

Automotive safety systems are designed to comply with the standards and regulations prescribed by government agencies and transport authorities worldwide. Passive safety systems are designed to protect passengers, drivers, and pedestrians during an accident.

In terms of region, the global Automotive Passive Safety Systems market can be segmented into North America, Europe, Asia Pacific, and Middle East & Africa. Asia Pacific is likely to hold a prominent share of the global…

Global Oil Pump for Automotive Market 2018 Analysis -Bosch,Denso,Aisin Seiki,Del …

According to this study, over the next five years the Oil Pump for Automotive market will register a xx% CAGR in terms of revenue, the global market size will reach US$ xx million by 2023, from US$ xx million in 2017. In particular, this report presents the global market share (sales and revenue) of key companies in Oil Pump for Automotive business.

Get Sample Copy of this Report for more Information…

Automotive Electronics Market 2026-Bosch Group, Atmel Corporation, Delphi Automo …

Market Overview:-

The global Automotive electronics market generated USD 226.5 billion in 2017 and is anticipated to grow at a CAGR of 9.1% during the forecast period according to a new study published by Polaris Market Research.

Request for sample copy of this report @ https://www.polarismarketresearch.com/industry-analysis/automotive-electronics-market/request-for-free-sample

Automotive electronics are specially-designed electronics intended for use in automobiles. Automotive electronics includes devices that have been designed and adapted for use in automobile applications…