Press release

Asia-Pacific at the Core: Manufacturing Scale and Design Innovation Reshape Low-Power Processor Economics

The investment thesis rests on three structural shifts. First, silicon content per device is rising across automotive, industrial IoT, and edge AI endpoints, increasing revenue density per unit. Second, capital expenditure requirements particularly for advanced fabrication and packaging are concentrating supply among a smaller set of vertically integrated or strategically partnered firms. Third, sovereign-backed semiconductor strategies in Asia-Pacific are redirecting supply chains, accelerating localization, and supporting margin expansion. With gross margins averaging 32%, leading players are increasingly capturing value through system-level integration rather than commoditized chip volumes.

Global Overview

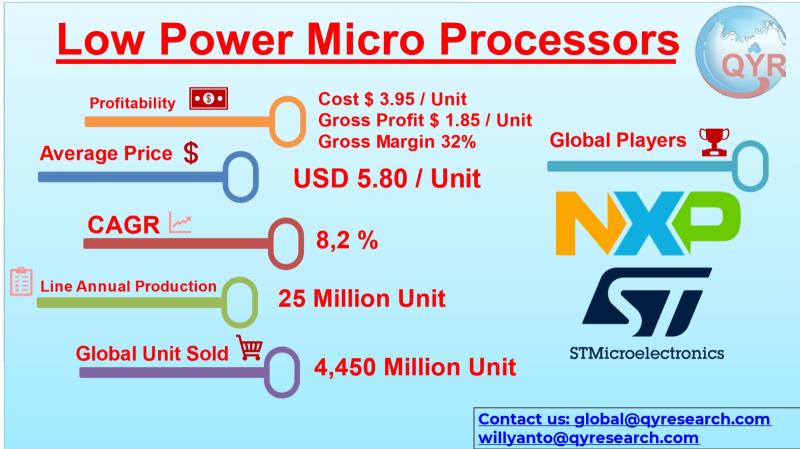

The global low-power MPU market was valued at USD 25,810 million in 2025 and is projected to reach USD 43,439 million by 2032, expanding at a CAGR of 8.2%.

Core demand drivers include the proliferation of edge computing workloads requiring localized processing with minimal energy draw, rapid adoption of AI-enabled IoT devices across industrial and consumer sectors, electrification and digitalization of automotive platforms (including ADAS and infotainment systems), and increased deployment of smart medical and wearable devices with strict power constraints.

Regional Consumption Dynamics (APAC & SEA Focus)

Asia-Pacific represents the largest and fastest-scaling consumption hub, driven by manufacturing concentration and domestic demand expansion. China, South Korea, and Taiwan anchor high-volume electronics production, while Southeast Asia is emerging as both a manufacturing extension and a consumption frontier.

Indonesia is experiencing rising demand tied to smart infrastructure, telecom expansion, and local assembly initiatives. Malaysia continues to strengthen its backend semiconductor ecosystem, particularly in testing and packaging, positioning itself as a critical node in MPU supply chains. Vietnam is rapidly scaling electronics manufacturing, attracting multinational OEMs shifting away from China, while Thailands automotive sector is integrating low-power MPUs into EV platforms and smart mobility systems. Singapore remains a strategic hub for advanced semiconductor R&D, IP design, and high-value wafer fabrication investments.

Sovereign initiatives across the region including incentives, tax structures, and state-backed funds are accelerating fab construction, OSAT (outsourced semiconductor assembly and test) capabilities, and chip design ecosystems, reinforcing APACs dominance in both demand and supply.

Production and Supply Chain

Value capture in the low-power MPU market is increasingly concentrated at the design and advanced manufacturing stages. Fabless semiconductor firms capture significant margins through proprietary architectures (e.g., ARM-based cores), while foundries secure long-term value via advanced node production and capacity control. Backend processes especially advanced packaging such as 2.5D/3D integration are also becoming margin-accretive.

Industry gross margins average around 32%, with leading-edge products achieving higher margins due to integration of AI accelerators, security modules, and heterogeneous computing architectures. However, capital intensity is rising sharply, with leading fabs requiring investments exceeding USD 10 billion per facility.

Asian economies play distinct strategic roles. Taiwan dominates advanced node fabrication, South Korea combines memory and logic integration, China is investing aggressively in domestic semiconductor independence, and Southeast Asia particularly Malaysia and Vietnam is strengthening assembly, testing, and mid-tier manufacturing capabilities. Indonesia is gradually entering the ecosystem through electronics manufacturing services (EMS) and downstream device assembly.

Latest Technological Developments

Integration of edge AI accelerators within low-power MPUs is enabling real-time inference for vision, speech, and predictive analytics without cloud dependency.

Adoption of advanced FinFET and Gate-All-Around (GAA) transistor architectures is reducing leakage currents and improving performance-per-watt metrics.

Development of heterogeneous computing platforms combining CPU, GPU, and NPU cores on a single die is enhancing workload specialization.

Emergence of chiplet-based designs is allowing modular scalability and improved yield economics in advanced nodes.

AI-driven power management systems are dynamically optimizing voltage and frequency scaling based on workload conditions.

Advanced packaging technologies such as fan-out wafer-level packaging (FOWLP) and 3D stacking are improving thermal efficiency and reducing form factor.

Market Breakdown Categories

Technology type segmentation includes ARM-based MPUs, which dominate due to power efficiency and licensing flexibility, and x86-based MPUs, which remain relevant in higher-performance embedded and industrial applications where legacy compatibility is critical.

Product categories span consumer electronics, where volume demand is highest; industrial devices, where reliability and lifecycle longevity drive procurement; automotive systems, which require functional safety and real-time processing; and medical devices, where ultra-low power consumption and precision are essential.

Power profile segmentation includes ultra-low power MPUs (below 1mW standby) used in wearables and IoT sensors, low-power processors for general embedded systems, and energy-efficient high-performance chips designed for edge AI and automotive workloads.

Memory architecture segmentation includes on-chip SRAM solutions optimized for latency-sensitive tasks, MPUs with external DRAM support for higher computational loads, and flash-integrated designs for compact, cost-sensitive devices.

Additional segmentation includes process node classification (≥28nm, 14-28nm, 7-14nm, ≤7nm), packaging type (standard, advanced fan-out, 3D stacked), end-user industry (consumer, automotive, healthcare, industrial automation, telecom), instruction set architecture (RISC, CISC, hybrid), and connectivity integration (Wi-Fi, Bluetooth, 5G-enabled MPUs).

Product Pricing Variations

Pricing varies significantly based on performance class, integration level, and manufacturing node. Entry-level ultra-low power MPUs such as ARM Cortex-M series chips from companies like STMicroelectronics and NXP typically range from USD 1.20 to USD 3.50, targeting IoT sensors and basic embedded systems where cost sensitivity is paramount.

Mid-range low-power processors, including ARM Cortex-A-based chips from Qualcomm and MediaTek, are priced between USD 3.50 and USD 8.00, offering balanced performance and efficiency for smartphones, smart home devices, and industrial controllers.

Higher-end energy-efficient MPUs incorporating AI acceleration such as those produced by Apple, Samsung, and advanced Qualcomm Snapdragon platforms range from USD 8.00 to USD 18.00, reflecting integration of neural engines, advanced GPUs, and high-speed connectivity modules.

Specialized automotive and industrial-grade MPUs, including products from Infineon, Renesas, and Texas Instruments, can command USD 15.00 to USD 40.00+, due to stringent reliability standards, extended temperature ranges, and safety certifications such as ISO 26262 compliance.

Global Top 30 Key Companies in the Low Power Micro Processor Market

Arm Ltd. (Cambridge, United Kingdom)

Qualcomm Incorporated (California, USA)

Apple Inc. (California, USA)

Intel Corporation (California, USA)

Advanced Micro Devices AMD (California, USA)

NXP Semiconductors (Eindhoven, Netherlands)

STMicroelectronics (Geneva, Switzerland)

Renesas Electronics (Tokyo, Japan)

Microchip Technology (Arizona, USA)

Texas Instruments (Texas, USA)

Espressif Systems (Shanghai, China)

GigaDevice Semiconductor (Beijing, China)

Allwinner Technology (Zhuhai, China)

Rockchip Electronics (Fuzhou, China)

Huawei HiSilicon (Shenzhen, China)

Infineon Technologies (Neubiberg, Germany)

Nordic Semiconductor (Trondheim, Norway)

Silicon Laboratories (Texas, USA)

Samsung Electronics (Suwon, South Korea)

MediaTek Inc. (Hsinchu, Taiwan)

NVIDIA Corporation (California, USA)

Broadcom Inc. (California, USA)

Marvell Technology (Delaware, USA)

UNISOC (Shanghai, China)

Realtek Semiconductor (Hsinchu, Taiwan)

VIA Technologies (Taipei, Taiwan)

Ambiq Micro (Texas, USA)

RDA Microelectronics (Shanghai, China)

Rohm Semiconductor (Kyoto, Japan)

Toshiba Electronic Devices (Kawasaki, Japan)

Chapter Outline

Chapter 1: Introduces the report scope of the report, executive summary of different market segments (by region, product type, application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the market and its likely evolution in the short to mid-term, and long term.

Chapter 2: key insights, key emerging trends, etc.

Chapter 3: Manufacturers competitive analysis, detailed analysis of the product manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc.

Chapter 4: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc.

Chapter 5 & 6: Sales, revenue of the product in regional level and country level. It provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and market size of each country in the world.

Chapter 7: Provides the analysis of various market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 8: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 9: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 10: The main points and conclusions of the report.

Related Report Recommendation

Global Low-Power Micro Processor Market Research Report 2026

https://www.qyresearch.com/reports/6453629/low-power-micro-processor

Low-Power Micro Processor- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

https://www.qyresearch.com/reports/6453628/low-power-micro-processor

Global Low-Power Micro Processor Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/6453630/low-power-micro-processor

Global Low-Power Micro Processor Market Outlook, InDepth Analysis & Forecast to 2032

https://www.qyresearch.com/reports/6453631/low-power-micro-processor

Global Micro Processor Melting Point Apparatus Market Research Report 2026

https://www.qyresearch.com/reports/5620744/micro-processor-melting-point-apparatus

Global Micro Processor Unit (MPU) Market Research Report 2025

https://www.qyresearch.com/reports/3533748/micro-processor-unit--mpu

Global Processor Power Module (PPM) Market Research Report 2026

https://www.qyresearch.com/reports/6006224/processor-power-module--ppm

Global Ultralow Power AI Processors Market Research Report 2026

https://www.qyresearch.com/reports/5893039/ultralow-power-ai-processors

Global Low-power Multi-core Digital Signal Processor Market Research Report 2026

https://www.qyresearch.com/reports/5711710/low-power-multi-core-digital-signal-processor

Global Low-power Single-core Digital Signal Processor Market Research Report 2026

https://www.qyresearch.com/reports/5711709/low-power-single-core-digital-signal-processor

About QY Research

QY Research has established close partnerships with over 71,000 global leading players. With more than 20,000 industry experts worldwide, we maintain a strong global network to efficiently gather insights and raw data.

Our 36-step verification system ensures the reliability and quality of our data. With over 2 million reports, we have become the world's largest market report vendor. Our global database spans more than 2,000 sources and covers data from most countries, including import and export details.

We have partners in over 160 countries, providing comprehensive coverage of both sales and research networks. A 90% client return rate and long-term cooperation with key partners demonstrate the high level of service and quality QY Research delivers.

More than 30 IPOs and over 5,000 global media outlets and major corporations have used our data, solidifying QY Research as a global leader in data supply. We are committed to delivering services that exceed both client and societal expectations.

Contact Information:

Tel: +1 626 2952 442 (US) ; +86-1082945717 (China)

+62 896 3769 3166 (Whatsapp)

Email: willyanto@qyresearch.com; global@qyresearch.com

Website: www.qyresearch.com

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Asia-Pacific at the Core: Manufacturing Scale and Design Innovation Reshape Low-Power Processor Economics here

News-ID: 4460385 • Views: …

More Releases from QY Research

Top 30 Indonesian Cocoa Public Companies Q3 2025 Revenue & Performance

1) Overall companies performance (Q3 2025 snapshot)

PT Mayora Indah Tbk

PT Indofood CBP Sukses Makmur Tbk

PT Indofood Sukses Makmur Tbk

PT Garudafood Putra Putri Jaya Tbk

PT Siantar Top Tbk

PT Ultra Jaya Milk Industry Tbk

PT Campina Ice Cream Industry Tbk

PT Buyung Poetra Sembada Tbk

PT Sekar Laut Tbk

PT Nippon Indosari Corpindo Tbk

PT Sariguna Primatirta Tbk

PT Delta Djakarta Tbk

PT Multi Bintang Indonesia Tbk…

APAC Leads the Reconfiguration of Texture-Modified Food Supply Chains Amid Risin …

The Standardized Texture Modified Foods market is entering a non-linear value inflection, shifting from a fragmented, volume-driven food service niche into a capital-intensive, clinically regulated nutrition segment. Historically dominated by small-scale kitchens and localized suppliers, the sector is now undergoing institutionalization driven by hospital procurement standards, aging populations, and reimbursement-linked nutrition protocols. This transition is forcing consolidation, automation, and standardization key levers for margin expansion and valuation uplift.

The inflection is…

From Volume to Precision: Why High Power Fiber Laser Chips Are Entering a New In …

The High Power Fiber Laser Chip market is entering a phase of non-linear value inflection, driven by a structural migration away from commoditized volume production toward precision-engineered, capital-intensive manufacturing. In 2025, global revenue stands at USD 1,465 million, projected to reach USD 2,272 million by 2032, reflecting a 6.5% CAGR. However, this topline growth understates the underlying transformation: value is increasingly captured at the epitaxial wafer, packaging, and thermal management…

The Hidden Layer Powering Every Robot: Motion Control Systems Take Center Stage

Robot Motion Control Systems are core subsystems that manage and coordinate robotic joint and actuator movements for precise operation. They integrate motion controllers, servo drives, feedback sensors (encoders), and algorithms to regulate position, velocity, acceleration, and torque via real-time closed-loop feedback. Production spans upstream components like microprocessors, FPGAs, servo motors, and RTOS software; midstream manufacturing of controllers and drives; and downstream integration into robots by OEMs. These systems ensure synchronized…

More Releases for MPU

MPU with AI: Why digital preparation alone is often not enough

New technologies promise quick solutions--but when it comes to the MPU, placing too much trust in them can be costly.

MPU: More Than Just a Test

The idea of using artificial intelligence to prepare for the Medical-Psychological Examination is gaining increasing attention. Many individuals affected hope that AI-based MPU counseling services or a digital AI MPU advisor will provide a quick, cost-effective, and straightforward solution to regaining their driver's license. But the…

E scooter reform 2026 and 2027: MPU Doktor warns of new fines and technical requ …

The German government is tightening regulations for e-scooters. From 2027, turn signals will become mandatory, while fines for traffic violations will be significantly increased. MPU expert Markus Gerber from MPU-Doktor explains why aligning e-scooter rules more closely with bicycle traffic brings greater freedom, yet the risk of losing a driver's license due to alcohol or drug use remains unchanged.

The latest reform of the Small Electric Vehicles Ordinance (Elektrokleinstfahrzeuge Verordnung, eKFV)…

Mpu System On Modules Market to Expand with a CAGR of 7.83% by 2032

The MPU System on Modules (SoM) Market was valued at USD 57.69 billion in 2023 and is projected to grow to USD 62.2 billion in 2024, eventually reaching USD 113.66 billion by 2032. This robust growth corresponds to a compound annual growth rate (CAGR) of 7.83% during the forecast period from 2024 to 2032. The increasing demand for compact, integrated systems that deliver high computational performance while maintaining low power…

Embedded Mpu Market Growing with a Healthy CAGR of 5.45% by 2032

The Embedded Microprocessor Unit (MPU) market is on a steady growth trajectory, driven by the increasing demand for embedded systems across various industries. As of 2023, the market was valued at approximately USD 21.14 billion and is projected to reach around USD 34.1 billion by 2032, reflecting a compound annual growth rate (CAGR) of about 5.45% during the forecast period from 2024 to 2032. This article explores the key trends,…

Aerospace Mpu Market Expansion at 4.49% CAGR by 2032

The Aerospace Microprocessing Unit (MPU) market, while relatively smaller compared to other aerospace segments, is exhibiting consistent growth due to the increasing reliance on advanced avionics and autonomous systems. Valued at USD 1.55 billion in 2023, the market is projected to reach USD 2.3 billion by 2032, registering a Compound Annual Growth Rate (CAGR) of 4.49% during the forecast period (2024-2032).

Key Companies in the Aerospace Mpu Market Include: Woodward, Inc.…

Server Microprocessor Unit (MPU) Market Analysis and Forecast to 2026| Intel, AM …

In a recent study published by QY Research, titled "Global Server Microprocessor Unit (MPU) Market Research Report", analysts offer an in-depth analysis of the global Server Microprocessor Unit (MPU) market. The study analyzes the various aspects of the market by studying its historic and forecast data. The research report provides a Porters five force model, SWOT analysis, and PESTEL analysis of the Server Microprocessor Unit (MPU) market. The different areas…