Press release

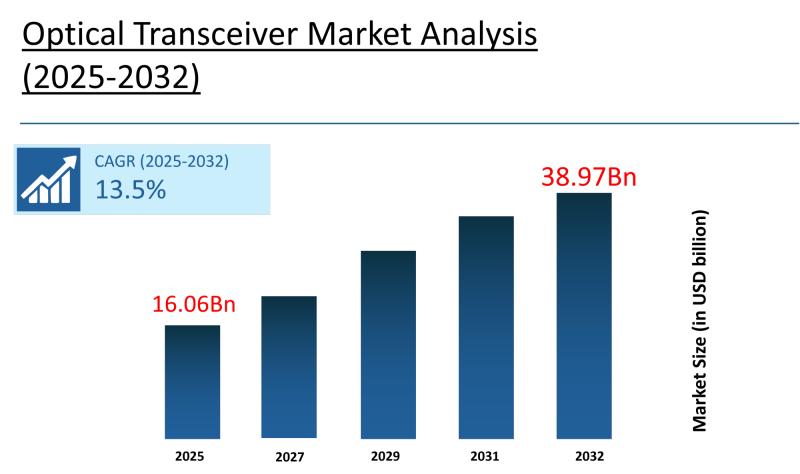

Optical Transceiver Market to Reach USD 38.97 Billion by 2032, Says Stratview Research

Stratview Research

This driver is structurally self-reinforcing. Each new hyperscale data center built by cloud operators requires thousands of optical transceivers for server-to-switch and switch-to-switch connectivity. As AI model complexity increases and inference workloads scale across distributed infrastructure, the bandwidth requirements per rack continue to rise - directly expanding the volume and speed tier of transceivers procured per deployment cycle. The optical transceiver market is therefore one of the most direct beneficiaries of the global AI infrastructure investment cycle.

Stratview Research, a global market research firm, has launched a report on the global market, which provides a comprehensive outlook of the global and regional industry forecast, current & emerging market trends, segment analysis, competitive landscape, & more.

The report covers the optical transceiver market across a study period of 2019-2032, with 2024 as the base year and 2025-2032 as the forecast period. It segments the market across eight dimensions - form type, data rate type, fiber type, distance type, wavelength type, connector type, application type, and region - providing granular demand intelligence across form factors from QSFP to CFP, data rates from sub-10 Gbps through 100+ Gbps, and applications spanning data centers, telecommunications, and enterprise networks. For transceiver manufacturers, network equipment OEMs, hyperscale operators, telecom infrastructure investors, and technology procurement teams, this report provides the analytical depth needed to navigate a rapidly evolving competitive and technology landscape.

Request a free sample report: https://www.stratviewresearch.com/Request-Sample/4284/optical-transceiver-market.html#form

Market Statistics

• Market size in 2024: USD 14.10 billion

• Forecast value by 2032: USD 38.97 billion

• CAGR (2025-2032): 13.5%

• Forecast period: 2025-2032

• Base year: 2024

• Total number of segments: 8

• Tables & figures: 100+

• Country-level market assessment: 20

Market Segmentation

Global Optical Transceiver Market, by Form Type

• SFF & SFP

• SFP+ and SFP28

• QSFP, QSFP+, QSFP-DD, QSFP28, and QSFP56

• CFP, CFP2, CFP4, and CFP8

• XFP

• CXP

Global Optical Transceiver Market, by Data Rate Type

• Less than 10 Gbps

• 10 Gbps - 40 Gbps

• 40 Gbps - 100 Gbps

• More than 100 Gbps

Global Optical Transceiver Market, by Fiber Type

• Single-Mode Fiber (SMF)

• Multimode Fiber (MMF)

Global Optical Transceiver Market, by Distance Type

• Less than 1 km

• 1 - 10 km

• 11 - 100 km

• More than 100 km

Global Optical Transceiver Market, by Wavelength Type

• 850 nm Band

• 1310 nm Band

• 1550 nm Band

• Others

Global Optical Transceiver Market, by Connector Type

• LC

• SC

• MPO

• RJ-45

Global Optical Transceiver Market, by Application Type

• Telecommunication

• Data Center

• Enterprise

Global Optical Transceiver Market, by Region

• North America (Country Analysis: The USA, Canada, and Mexico)

• Europe (Country Analysis: Germany, France, Italy, The UK, and Rest of Europe)

• Asia-Pacific (Country Analysis: Japan, China, India, and Rest of Asia-Pacific)

• Rest of the World (Country Analysis: Brazil, Saudi Arabia, and Others

Segment Analysis

Within the form type segmentation, the QSFP (Quad Small Form-factor Pluggable) segment is currently the leading segment in the optical transceiver market. QSFP's dominance reflects its structural alignment with the bandwidth demands of modern hyperscale and enterprise data center infrastructure: the QSFP form factor family - spanning QSFP+, QSFP28, QSFP-DD, and QSFP56 - supports data rates from 40G through 400G in a compact, hot-swappable module that is compatible with the high-density switch and router port configurations preferred by hyperscale operators. As cloud providers including Amazon, Microsoft, and Google continue deploying AI and high-performance computing clusters, QSFP-DD modules in particular are becoming the default interconnect choice for 400G and 800G deployments, making QSFP-family positioning the most commercially significant form factor decision for transceiver manufacturers.

Within the data rate type segmentation, the 10 Gbps to 40 Gbps segment is expected to grow at a faster pace during the forecast period. The driver is the ongoing network modernization cycle across enterprise and mid-tier telecom markets, where a large installed base of legacy sub-10 Gbps infrastructure is being upgraded to meet rising bandwidth demand from cloud access, video, and IoT applications. This speed tier hits an accessible price point for SME enterprise deployments and regional carrier upgrades, making it the highest-volume refresh opportunity in markets where 100G+ deployments are not yet economically justified. Component vendors with strong supply positions in this tier will benefit from the geographically broad and numerically large installed-base replacement cycle playing out through the forecast period.

Within the fiber type segmentation, Single-Mode Fiber (SMF) held the largest share of more than 50% of the optical transceiver market in 2024. SMF's dominant position is a direct consequence of its superior performance characteristics for the applications that drive the highest transceiver volumes: long-distance telecom backhaul, metro network interconnects, and data center interconnect links between campuses or cloud regions all require the low signal attenuation and high bandwidth capacity that only single-mode fiber can reliably provide at distances beyond a few hundred meters. As 5G network backhaul deployments and hyperscale inter-data-center connectivity continue to scale, SMF-compatible transceiver procurement will remain the volume anchor of the market.

Within the distance type segmentation, the Less than 1 km segment is expected to dominate the market during the forecast period. This reflects the architectural reality of hyperscale data centers: the majority of transceiver deployments occur within a single facility, connecting servers to top-of-rack switches, spine switches to core routers, and GPU clusters to storage systems - all within distances well under 1 km. As AI infrastructure density increases and more servers are packed into fewer, larger facilities, the ratio of short-reach intra-data-center transceivers to long-reach telecom transceivers continues to rise. For manufacturers, dominance in the short-reach segment means alignment with the fastest-growing end-use environment in the entire optical transceiver ecosystem.

Within the wavelength type segmentation, optical transceivers operating in the 1310 nm Band are expected to grow at the highest CAGR during the forecast period. The 1310 nm wavelength is the standard for single-mode fiber transmission at the distances relevant to data center interconnects, enterprise LAN backbones, and 5G fronthaul links - all of which are among the fastest-growing application segments in the market. Its compatibility with advanced silicon photonics-based transceiver designs and its ability to support coherent and direct-detect transmission schemes further positions 1310 nm as the wavelength of choice for next-generation 400G and 800G module architectures.

Within the connector type segmentation, the LC (Lucent Connector) segment is expected to hold the largest market share during the forecast period. LC connectors are the de facto standard for single-mode fiber connections in data center and telecom environments, prized for their small form factor, low insertion loss, and broad compatibility with QSFP and SFP module families. As data center deployments continue to standardize on QSFP-DD and OSFP modules for high-speed interconnects, the LC duplex connector's integration into transceiver designs and patch cord ecosystems ensures its continued dominance across the highest-volume procurement channels.

Within the application type segmentation, the Data Center segment is expected to hold the largest share of the optical transceiver market during the forecast period. The data center segment's structural leadership is driven by the simultaneous scaling of cloud computing, AI infrastructure, and big data processing - all of which require massive bandwidth between servers, switches, and storage systems within and between facilities. The expansion of hyperscale facilities globally is fueling adoption of 100G, 200G, 400G, and 800G transceiver modules, and the emergence of AI-optimized data center architectures requiring ultra-fast GPU cluster interconnects is accelerating the transition to even higher speed tiers. For transceiver vendors, the data center segment is not just the largest market by volume but the primary driver of the product innovation and speed-tier upgrade cycles that shape the entire industry

Regional Insights

Asia Pacific is expected to grow at the fastest CAGR in the optical transceiver market during the forecast period. The region's acceleration is driven by a convergence of structural factors that are unique in their scale and breadth: Asia Pacific is simultaneously the world's largest electronics manufacturing hub, home to some of the fastest-growing hyperscale data center markets, and the region with the most aggressive 5G network deployment programs across China, Japan, South Korea, and India. China-based transceiver manufacturers including INNOLIGHT, Accelink Technology, and Hisense Broadband have built globally competitive production capabilities, while rapid growth in domestic internet penetration, IoT adoption, and cloud service consumption is expanding the regional demand base at a pace that outstrips other markets. The combination of supply-side strength and demand-side expansion positions Asia Pacific as the highest-growth region in the global optical transceiver market through 2032.

Market Drivers

• Global 5G network rollout by major telecom operators requires dense fiber-based backhaul and fronthaul infrastructure connecting base stations and small cells to core networks, generating sustained demand for 25G, 100G, and 400G optical transceivers as each new cell site deployment requires multiple high-speed optical interfaces.

• Hyperscale data center capacity expansion by cloud providers including Amazon AWS, Microsoft Azure, and Google Cloud is driving continuous procurement of 100G through 800G transceivers for server interconnects, spine-leaf switching architectures, and AI GPU cluster connectivity - with each new facility requiring thousands of transceiver units across multiple speed tiers.

• The emergence of AI-optimized data center architectures - requiring ultra-low-latency, ultra-high-bandwidth interconnects between GPU clusters for model training and inference - is accelerating the adoption of 800G and emerging 1.6T transceiver modules, as demonstrated by Lumentum's launch of 800G ZR+ transceivers and Coherent Corp.'s 800G ZR/ZR+ modules in QSFP-DD and OSFP form factors.

• Rapid expansion of internet penetration and connected device adoption across Asia Pacific - including smartphone, IoT, and wearable device proliferation - is generating surging data traffic that requires continuous investment in high-speed optical backbone and access network infrastructure, creating sustained regional demand for transceivers across all data rate tiers.

• Enterprise network modernization driven by the shift to cloud-based applications and hybrid work infrastructure is compelling businesses globally to upgrade legacy copper and low-speed fiber networks to 10G, 25G, and 40G architectures, creating a large-scale equipment refresh cycle that drives volume demand for optical transceivers in the 10-40 Gbps tier across enterprise procurement channels.

Top Companies in the Market

• Coherent Corp. (US)

• INNOLIGHT (China)

• Accelink Technology Co. Ltd. (China)

• Cisco Systems, Inc. (US)

• Hisense Broadband, Inc. (China)

• Lumentum Operations LLC (US)

• Sumitomo Electric Industries, Ltd. (Japan)

• Broadcom Inc. (US)

• Fujitsu Optical Components Limited (Japan)

• Intel Corporation (US)

FAQs

1. What is the current size of the optical transceiver market and what is the growth forecast through 2032 ?

The optical transceiver market was valued at USD 14.10 billion in 2024 and is projected to reach USD 38.97 billion by 2032, growing at a CAGR of 13.5% during the 2025-2032 forecast period. The cumulative sales opportunity over this period is estimated at USD 209.29 billion, driven by simultaneous demand expansion from data center AI infrastructure, 5G network deployment, and enterprise network modernization.

2. What is driving demand for optical transceivers across the technology industry ?

The two primary structural drivers are the global expansion of 5G networks - which requires high-speed fiber-based backhaul and fronthaul optical modules at every cell site - and the accelerating build-out of hyperscale and AI-optimized data centers, which generate large-scale procurement of 100G through 800G transceivers for server interconnect and GPU cluster connectivity. Both forces are growing simultaneously and reinforcing each other through shared infrastructure investment cycles.

3. Which application segment and form factor are most critical for transceiver suppliers to prioritize ?

The Data Center segment is expected to hold the largest market share and generate the highest procurement volumes, driven by hyperscale cloud expansion and AI infrastructure build-out. The QSFP form factor family - particularly QSFP-DD for 400G and 800G deployments - is the leading form factor, making data center-oriented QSFP module production the strategically highest-priority segment for transceiver manufacturers.

4. Which region is growing the fastest in the optical transceiver market and what drives that growth ?

Asia Pacific is expected to grow at the fastest CAGR over the forecast period, driven by its position as the world's largest electronics manufacturing hub, aggressive 5G deployment programs in China, Japan, South Korea, and India, and rapidly expanding domestic data center and cloud service markets. China-based manufacturers including INNOLIGHT and Accelink Technology also give the region a structural supply-side advantage in global transceiver production.

5. What is the key challenge constraining adoption and interoperability in the optical transceiver market ?

The primary challenge is rising network complexity: as infrastructure evolves to support 5G, edge computing, AI workloads, and multi-cloud architectures simultaneously, transceiver vendors must ensure seamless interoperability across diverse platforms, protocols, and interface standards. Managing compatibility across software-defined, virtualized, and heterogeneous network environments increases integration costs and can slow deployment timelines, particularly for enterprise and mid-tier carrier customers without dedicated optical networking expertise.

Related Links:

Conveyor Belt Market:

https://payrchat.com/blogs/9372/conveyor-belt-market

Heat Exchangers Market:

https://logcla.com/blogs/839996/From-Plate-To-Air-Cooled-Segmentation-And-Regional-Dynamics-To

Medical Composites Market:

https://tiktiktalk.com/blogs/28308/Healing-Materials-Unlocking-New-Opportunities-in-Medical-Composites

Prepreg Market:

https://community.wongcw.com/blogs/1002970/Prepreg-Market-Trends-What-to-Expect-in-the-Next-Five

Surgical Tables Market:

https://payrchat.com/blogs/33305/surgical-tables-market-stratview-research

Titanium Alloys Market:

https://logcla.com/blogs/495346/Titanium-Alloys-Market-Forecast-What-to-Expect-in-the-Next

Natural Fiber Composites Market:

https://heyhey.icu/blogs/94219/Natural-Fiber-Composites-Driving-Sustainability-in-Manufacturing

Medical Packaging Films Market:

https://ayema.ng/blogs/212432/Sustainable-Solutions-in-the-Medical-Packaging-Films-Market

Metal Matrix Composite Market:

https://logcla.com/blogs/893572/Innovation-and-Sustainability-Propel-the-Metal-Matrix-Composite-Market-Forward

Nickel Alloys Market:

https://thebizbar.com/blogs/104272/Future-of-the-Nickel-Alloys-Industry

400 Renaissance Center, Suite 2600,

Detroit, Michigan, MI 48243

United States of America

Website: www.stratviewresearch.com

Mail Us: sales@stratviewresearch.com

Press: media@stratviewresearch.com

Stratview Research is a global market research firm that highly specializes in aerospace & defense, chemicals, and a few other industries.

It launches a limited number of reports annually on the above-mentioned specializations. Thorough analysis and accurate forecasts in this report enable the readers to take convincing business decisions.

Stratview Research has been helping companies meet their global and regional growth objectives by offering customized research services. These include market assessment, due diligence, opportunity screening, voice of customer analysis, market entry strategies, and more.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Optical Transceiver Market to Reach USD 38.97 Billion by 2032, Says Stratview Research here

News-ID: 4455961 • Views: …

More Releases from Stratview Research

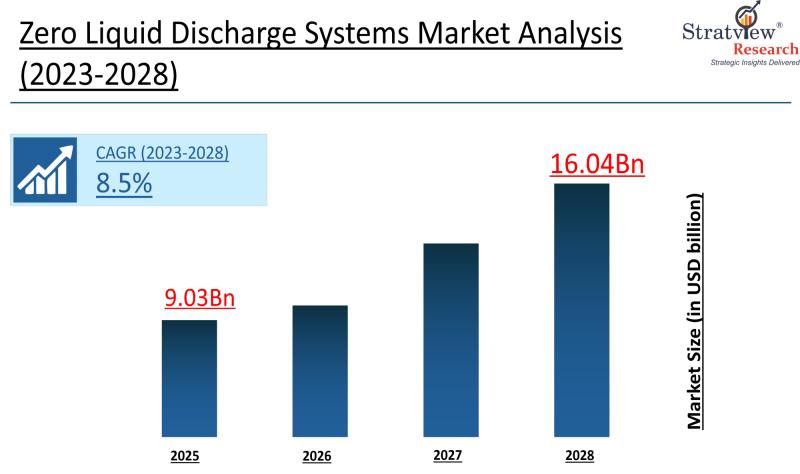

Zero Liquid Discharge Systems Market to Reach USD 16.04 Billion by 2032, Says St …

The global zero liquid discharge (ZLD) systems market was valued at USD 8.30 billion in 2024. It is projected to reach USD 16.04 billion by 2032, growing at a CAGR of 8.5% during the forecast period of 2025-2032. The single most important growth driver is rising water scarcity combined with tightening restrictions on industrial freshwater usage, which are compelling industries across multiple sectors to adopt ZLD systems as a near-total…

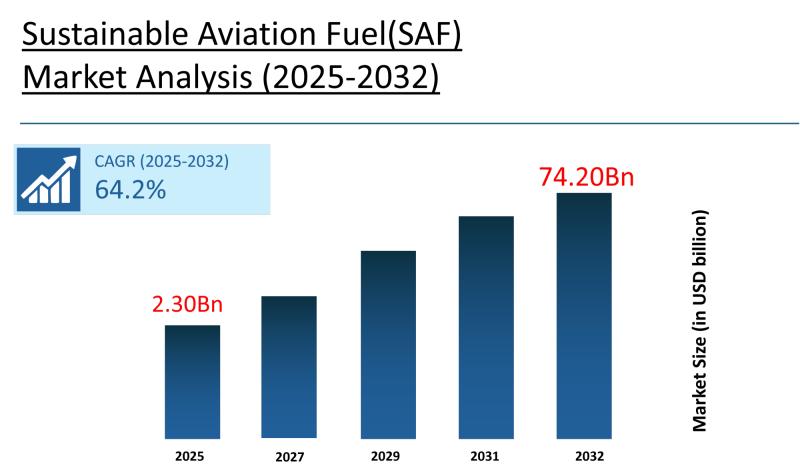

Sustainable Aviation Fuel Market to Reach USD 74.20 Billion by 2032, Says Stratv …

The global sustainable aviation fuel (SAF) market was valued at USD 1.40 billion in 2024. It is projected to reach USD 74.20 billion by 2032, growing at a CAGR of 64.2% during the forecast period of 2025-2032. The single most important growth driver is the convergence of stringent global emission targets and net-zero commitments - enforced through regulatory frameworks by ICAO, IATA, and major government bodies - which are making…

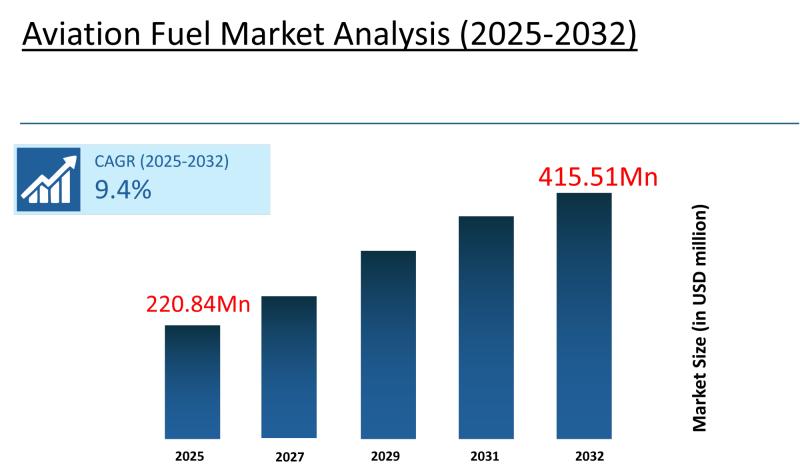

Aviation Fuel Market to Reach USD 415.51 Million by 2032, Says Stratview Researc …

The global aviation fuel market was valued at USD 201.40 million in 2024. It is projected to reach USD 415.51 million by 2032, growing at a CAGR of 9.4% during the forecast period of 2025-2032. The single most important growth driver is the surge in global air passenger and cargo traffic, which is directly and proportionally expanding aviation fuel consumption across both commercial and logistics networks.

This driver is structurally durable.…

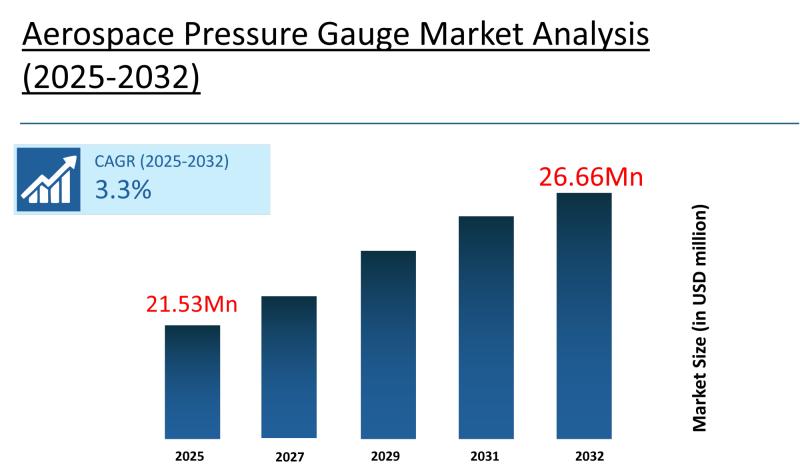

Aerospace Pressure Gauge Market to Reach USD 26.66 Million by 2032, Says Stratvi …

The global aerospace pressure gauge market was valued at USD 20.80 million in 2024. It is projected to reach USD 26.66 million by 2032, growing at a CAGR of 3.3% during the forecast period of 2025-2032. The single most important growth driver is the rising production and deployment of next-generation aircraft - including the Boeing 787 and Airbus A350 - which require high-performance, digital-compatible pressure monitoring systems across hydraulic, fuel,…

More Releases for SFP

Global SFP Transceiver Market Size,Growth Rate,Industry Opportunities 2025-2031

According to our (Global Info Research) latest study, the global SFP Transceiver market size was valued at US$ 95.9 million in 2024 and is forecast to a readjusted size of USD 130 million by 2031 with a CAGR of 4.5% during review period.

A Small Form-Factor Pluggable (SFP) transceiver is a compact, hot-pluggable optical transceiver module used in high-speed data communication and networking applications. It is commonly used in Ethernet, Fiber…

SFP Optical Transceiver Market Insights, Forecast to 2030 | Valuates Reports

SFP Optical Transceiver Market

The global SFP Optical Transceiver market was valued at US$ 3220.6 million in 2023 and is anticipated to reach US$ 5004.9 million by 2030, witnessing a CAGR of 6.5% during the forecast period 2024-2030.

View Sample Report

https://reports.valuates.com/request/sample/QYRE-Auto-3A12888/Global_SFP_Optical_Transceiver_Market_Research_Report_2022

Report Scope

The SFP Optical Transceiver market size, estimations, and forecasts are provided in terms of output/shipments (K Units) and revenue ($ millions), considering 2023 as the base year, with history and…

Perle releases SFP and XFP Optical Transceivers

Perle Systems, a global manufacturer of advanced Ethernet over Fiber and secure device networking hardware, adds SFP and XFP Optical Transceivers to its product portfolio.

These hot-swappable, compact media connectors provide instant fiber connectivity to networking gear like Media Converters, Switches and Routers. They are a cost effective way to connect a single network device to a wide variety of fiber cable distances and types.

"Optical Modules reduce the need for surplus…

SFP modules from UBF make fiber optic networks scalable

New technologies with higher bandwidths make demands also on the entire infrastructure between servers and end devices.

Autonegotiation - commonly between Ethernet switches and end devices with RJ-45 ports - is not available for fiber optic connections. Changing from Fast Ethernet to Gigabit Ethernet must be implemented on both sides of the fiber optic line. Already installed multimode cables can also be an obstacle for upgrades because of the reduced distance…

Embrionix Releases Industry’s First FPGA-Based SFP

Laval, Canada, February 20, 2012—Embrionix Design reached another milestone today with the introduction of the industry’s first FPGA-based SFP. This full-featured SFP allows Embrionix customers to integrate more functionality in the SFP, allowing them to do more in less space. Consequently, with emSFPTMuse, the customer will experience an unmatched performance, customized implementation and unparalleled flexibility.

“To meet the ever increasing signal diagnostics and miniaturization requirements in today’s high-end communications and…

OPTCORE Release 10GBase-ER SFP+ Optical Transceiver (10G SFP+ ER Optical Transce …

Optcore Technology, a professional fiber optical transceiver and fiber media converters supplier, is pleased to announce the 10GBase-ER SFP+ Transceiver for 10G Ethernet and OC-192/STM-64 SONET/SDH Transport.

OPTCORE's 10Gb/s SFP+ ER transceiver module complies with the 802.3ae 10GBASE-ER/EW electrical interface and the SFF-8431 specifications for 10 Gigabit SFP+ small form factor pluggable module. The SFP+ ER Transceiver module uses 1550nm cooled EML transmitter with TEC and PIN photo-detector for single mode…