Press release

Retail market of cosmetics and drugstore items in Poland 2009

Drugstore chains have rapidly gained a PLN 20bn share of the cosmetics and drugstore products market in Poland. In spite of the economic crisis they plan to open even more stores in 2009 than they did in previous years.According to PMR estimates, which are included in latest report “Retail market of cosmetics and drugstore items in Poland 2009. Market analysis and development forecasts for 2009-2011”, Poland’s cosmetics and drugstore products market was worth PLN 20bn (€5.7bn) in 2008, which translates into growth of 13% in comparison with 2007. We expect the growth rate to slow down in the coming years and in 2009 will be in the region of 5%. The tempo will slow down as Poles adopt more cautious spending habits in the face of rising unemployment, slower wage growth and more pessimistic consumer moods, all of which in turn are a consequence of the financial and economic crisis impacting both Poland and the world.

In spite of these dangers the cosmetics market will be one of the most resistant to the current recession – “Appearance is very important for women, hence even in the most difficult times they will want to be able to purchase cosmetics, especially mid-priced items, which represent the bulk of the assortments offered by drugstore chains. Moreover, cosmetics are heavily dependent on advertising and brand image, and once customers become attached or accustomed to a given product or a certain standard they find it difficult to abandon it”, according to Patrycja Nalepa, Retail Analyst at PMR.

Chains flexing their muscles

Drugstores as a whole account for the lion’s share of sales on Poland’s cosmetics and drugstore products market. Their share of the market has risen steadily in recent years to stand at 33% in 2008. The second and third biggest distribution channels are hypermarkets and supermarkets (including discount stores) – their combined share amounted to 32% w 2008. In the last few years the share of hypermarkets has declined while supermarkets have grown in importance.

The principal factor driving up the sales and market share of drug-cosmetics stores in general are drugstore chains, which are developing rapidly and increasing in popularity. In the last few years, their growth has been helped by a robust economy and rising consumer demand. Stores in such chains have increasingly become the place of choice for consumers when it comes to buying cosmetics owing to, among other advantages, their convenient location (in shopping centres, on high streets, in shopping arcades and stations), broad and varied assortment, generous supply of medium-range cosmetics, attractive prices and numerous promotions. Other advantages that drugstores in general have over, for example, hypermarkets include qualified and well-trained staff who are willing to offer customers advice, as well as their willingness to stock new items and innovative products.

As a result, drugstore chains are not only rapidly building up their share of the drug-cosmetics segment in Poland, both with respect to store count and sales, but they are also increasing their share of the cosmetics and drugstore products market – up by 6 p.p. in 2006-2008.

Even more stores in the pipeline this year

We predict that the share of chains in sales, both in the segment and on the cosmetics and drugstore products market as whole, will continue to increase in the coming years, thanks both to the opening of brand new stores and the incorporation of existing individual outlets into chains on a franchising basis.

According to calculations of PMR, the current year will be even more favourable for drugstore chains than the previous two years thanks to higher store counts. The biggest chains will add approximately 270 new outlets to their store counts this year, in comparison with 170 units in 2008 and 190 in 2007. This trend will partly be helped by the planned opening of many new shopping centres , rescheduled for 2009, in which drugstore chains have leased space (e.g. Galeria Malta in Poznan, Bonarka in Krakow, Galeria Jurajska in Czestochowa and DTC Renoma in Wroclaw).

A second contributing factor is the current economic downturn and the much greater inclination of independent stores to enter chains in which they will have a greater chance of survival than if they continued to operate as individual businesses. Confirmation of this trend lies in the fact that many franchise chains predict a significant jump in their store counts this year: Drogerie Koliber (store count up from 75 at the end of 2008 to 85-90 outlets by the end of 2009), Drogerie Brawo (from 99 to 120-130) and Drogerie Aster (from 29 to 50-60).

Thirdly, during the current recession it will be easier for chains to obtain high street locations, which until now have been the preserve of banks willing to pay high rents for such locations. There is also a chance that this trend will bring down high street rents.

Rossmann the biggest performer

The undisputed leader on the Polish cosmetics and drugstore products market , both in terms of sales and number of outlets, is Rossmann. According to PMR estimates, in 2008 the Rossmann chain boosted its sales by 36% up to PLN 2.38bn, as a result of which its market share reached almost 12%. During 2008, the chain opened 64 new shops, bringing its total store count up to 342 outlets by the end of last December. The second biggest player is the perfumery chain Sephora, whose revenues are several times below those of Rossmann. The third biggest chain – Drogerie Natura – is simultaneously the second largest chain in terms of store count (262 at the end of 2008).

In 2008 the 10 largest drugstore chains accounted for 21.7% of the market, as compared with 16% in 2006. We expect this share to surpass 24% in 2009.

This press release is based on information contained in the latest PMR report entitled “Retail market of cosmetics and drugstore items in Poland 2009. Market analysis and development forecasts for 2009-2011”.

For more information on the report please contact:

tel. /48/ 12 618 90 00

e-mail: marketing@pmrcorporate.com

About PMR

PMR Publications (www.pmrpublications.com) is a division of PMR, a company providing market information, advice and services to international businesses interested in Central and Eastern European countries and other emerging markets. PMR key areas of operation include market research (through PMR Research), consultancy (through PMR Consulting) and business publications (through PMR Publications). With over 13 years of experience, highly skilled international staff and coverage of over 20 countries, PMR is one of the largest companies of its type in the region.

PMR

ul. Supniewskiego 9, 31-527 Krakow, Poland

tel. /48/ 12 618 90 00, fax /48/ 12 618 90 08

www.pmrcorporate.com

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Retail market of cosmetics and drugstore items in Poland 2009 here

News-ID: 80388 • Views: …

More Releases from PMR Publications

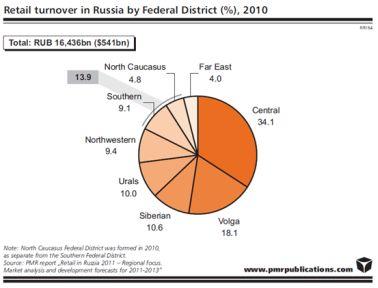

Russian retail market recovered after the economic slowdown

Retail markets in all Russian Federal Districts increased in 2010 by total $80bn

In 2010, Russian retail market recovered after the economic slowdown observed in the previous year and increased by 12.6% to RUB 16.4tr ($541bn). However, the latest PMR report „Retail in Russia 2011 – Regional focus. Market analysis and development forecasts for 2011-2013” shows that particular regional retail markets still reveal differences in their development due to their unique…

Construction output in Poland up by 10% in 2011

The forthcoming year 2011 can be a breakthrough year for the construction industry in terms of construction output. Provided that the winter weather conditions are relatively favourable, the 2011 average annual growth rate can be up to 10%, driven by large civil engineering projects and major improvement in the building construction sector.

According to a report prepared by research company PMR, which is entitled "Construction sector in Poland, H2 2010 -…

Russian construction industry recovers after the downturn

For the first time this decade, in 2009 the construction industry in Russia, which was severely affected by the global economic downturn, shrank in comparison with the preceding year. In the current year, a recovery has begun, prompted by the numerous projects supported or directly funded by the government. In the next few months, growth in the construction industry will be driven by the civil engineering and residential construction subdivisions…

Retail market in Russia to grow by almost 10% in 2010

The growth rate of the Russian retail sector dropped severely last year due to worsening economic conditions, weakening purchasing power growth and the depreciating rouble. As a result, the retail market's value increased by only 5% in 2009 after several years of roughly 25% annual growth. Nevertheless, the situation has improved this year, and the retail market is expected to once again reach double-digit growth rates in subsequent years.

According to…

More Releases for Poland

Poland Agriculture Market, Poland Agriculture Industry, Agriculture Livestock Ma …

Poland is a significant European and global producer of numerous agricultural products. The agricultural land market in country is divided in two parts: privately owned farms and land owned farms by the State Treasury. Privately owned farm is an enterprise to cultivate various agricultural products under the control of one or more investor. Poland is among the world's primary producers of potatoes, rye, and apples, as well as pork and…

MAUSER Poland Celebrates 5th Anniversary

Bruehl/Germany, June 27, 2017

MAUSER Group, a worldwide leading company in industrial packaging, celebrates the 5th anniversary of its factory in Gliwice, Poland. Ideally located in the industrial heartland of Upper Silesia, and operated by a strong local management team, the plant offers high-quality industrial packaging solutions and services.

MAUSER Poland serves customers with a comprehensive product range of Composite Intermediate Bulk Containers (CIBCs) and plastic tight-head drums. In line with…

Agrochemicals Market in Poland

ReportsWorldwide has announced the addition of a new report title Poland: Agrochemicals: Market Intelligence (2016-2021) to its growing collection of premium market research reports.

The report “Poland: Agrochemicals: Market Intelligence (2016-2021)” provides market intelligence on the different market segments, based on type, active ingredient, formulation, crop, and pest. Market size and forecast (2016-2021) has been provided in terms of both, value (000 USD) and volume (000 KG) in the report. A…

A+ ratings on Poland

Jelenia Gora/Poland, 20.09.2011 - In August 2011 two rating agencies i.e. Standard & Poor's and Moody's Investors Service affirmed their A+ rating on Poland with a stable outlook. Both agencies noted that the Polish economy is competitive and increasingly diversified. Moody's evaluated Poland as relatively well placed to withstand global turmoil with its relatively resilient economy. Both agencies stressed that the Polish economy continued to expand in 2009, in contrast…

IT market in Poland

IT providers in Poland are starting the post-crisis period in actually quite good moods and are already beginning to predict what solutions will be most sought after by their customers during prosperity.

However last year hardware distributors recorded significant reduction in the number of orders placed, especially by business customers, software and IT services providers performed far better. A majority of them had similar sales as in previous periods, while some…

VoIP in Poland

At the end of 2008 the Polish VoIP telephony market was worth PLN 440m, with CaTV operators having generated the largest share of revenue in the segment. In recent years also fixed-line operators have included VoIP services into their offer.

According to research and consulting company PMR Polish VoIP market continues to represent a small share of the fixed-line telecommunications market. In 2008 it accounted for approximately five percent of the…