Press release

Forensic Accounting Market: Why Financial Truth Has Become a Continuous Investigation Rather Than an Annual Audit

Forensic Accounting Market

Consider how these insights might influence your strategic decisions 👉https://www.htfmarketintelligence.com/sample-report/global-finance-accounting-outsourcing-market

The Major Players Covered in this Report: Deloitte (UK), EY (Ernst & Young) (UK), KPMG (Netherlands), PwC (UK), Genpact (United States), Capgemini (France), Cognizant Technology Solutions (United States), Wipro (India), TCS (Tata Consultancy Services) (India), Infosys (India)

The organizations redefining forensic accounting understand a simple reality: financial fraud is no longer confined to accounting entries. It exists within business processes, digital identities, procurement ecosystems, tax structures, ESG disclosures, intellectual property valuations, cryptocurrency movements, and increasingly, machine-generated documentation. Every new layer of digital transformation expands legitimate business capability while simultaneously increasing the surface area available for financial deception. As enterprises automate operations, they also automate opportunities for sophisticated misconduct.

This shift explains why the forensic accounting market has moved beyond investigations into continuous financial intelligence. Boards are no longer asking whether fraud has occurred; they are asking where hidden vulnerabilities are accumulating before they become visible to regulators, investors, or counterparties. That subtle change in perspective is reshaping investment priorities across advisory firms, financial institutions, multinational corporations, and regulatory agencies alike.

Definition:

Finance and Accounting Outsourcing (FAO) refers to the practice of hiring external service providers to handle various financial and accounting functions of a business. These functions can include bookkeeping, payroll processing, tax preparation, financial reporting, accounts payable and receivable, and auditing.

Market Trends:

• Adoption of Cloud-Based Solutions: The shift towards cloud-based financial management systems is making it easier for businesses to outsource their finance and accounting functions. Cloud platforms offer real-time data access, enhanced security, and seaml

Market Drivers:

• Need for Operational Efficiency: Businesses are increasingly outsourcing finance and accounting tasks to streamline operations, reduce overhead costs, and improve overall efficiency.

Market Opportunities:

• Expansion into Emerging Markets: The growing demand for finance and accounting outsourcing services in emerging markets presents significant opportunities for service providers to expand their client base and tap into new revenue streams.

Market Challenges:

• Data Security and Privacy Concerns: The risk of data breaches and concerns about the confidentiality of financial information are major challenges in finance and accounting outsourcing, especially when dealing with sensitive financial data.

Perhaps the greatest challenge confronting modern forensic professionals is the widening capability gap between sophisticated bad actors and legacy investigative methodologies. Financial criminals increasingly exploit decentralized financial networks, digital asset ecosystems, layered international entities, AI-generated documentation, and synthetic identities to construct transactions that appear economically rational while concealing entirely different intentions.

Meanwhile, many investigative environments continue to depend on historical sampling techniques, periodic reconciliations, and manually defined risk thresholds developed for a far less dynamic financial environment. This mismatch creates a dangerous illusion of oversight. Organizations often possess enormous quantities of financial data yet lack meaningful visibility into emerging behavioral patterns that indicate manipulation before losses occur.

Future market leadership will belong to forensic platforms capable of analyzing behavior rather than simply validating transactions. That distinction is profound. Traditional forensic accounting focused on proving what happened. Next-generation forensic accounting seeks to understand why behaviors evolve, how manipulation propagates through organizational systems, and where emerging patterns suggest future misconduct.

This transformation is being accelerated by the convergence of generative accounting models and predictive behavioral analytics. As artificial intelligence becomes embedded throughout financial operations, investigators will increasingly evaluate financial intent rather than isolated accounting outcomes. Fraud detection is gradually shifting from identifying numerical inconsistencies toward recognizing behavioral inconsistencies.

A journal entry may be technically correct. A contract may comply with every documented approval workflow. Supporting evidence may appear authentic. Yet predictive behavioral models can identify subtle deviations in timing, communication patterns, approval sequences, transaction clustering, supplier evolution, or executive decision pathways that collectively reveal hidden intent.

If you have questions about the data, reflect on how it may impact your sector👉https://www.htfmarketintelligence.com/enquiry-before-buy/global-finance-accounting-outsourcing-market

Intent itself is becoming measurable through probability rather than confession.

This represents one of the most significant philosophical shifts the forensic accounting profession has experienced in decades.

Organizations relying exclusively on historical data sampling remain fundamentally exposed because sophisticated financial manipulation rarely announces itself through arithmetic errors. Instead, it emerges through changing behavioral relationships that conventional audit methodologies were never designed to evaluate. Sampling confirms historical accuracy. Behavioral intelligence anticipates future misconduct.

A practical way to understand today's threat landscape is through what can be described as the Three Layers of Modern Financial Exposure.

Layer One: Cross-Border Transaction Velocity

Global businesses increasingly operate across jurisdictions with different regulatory expectations, reporting standards, taxation frameworks, and digital payment infrastructures. The speed at which capital now moves creates investigative blind spots that traditional jurisdiction-by-jurisdiction reviews cannot effectively monitor. Exposure arises not from transaction size alone but from transaction velocity combined with fragmented oversight.

Layer Two: Algorithmic Anomalies

Automation has introduced an entirely new category of financial risk. AI-assisted invoice generation, automated procurement, dynamic pricing engines, predictive forecasting systems, and machine-driven reconciliation tools produce vast quantities of financially significant decisions with minimal human intervention. Detecting fraud increasingly requires distinguishing between legitimate algorithmic optimization and deliberate algorithmic manipulation.

Layer Three: Internal Narrative Manipulation

Perhaps the least understood-and most dangerous-layer involves controlling the organizational story rather than altering the accounting records. Executives, operational leaders, finance teams, and external stakeholders may each possess internally consistent versions of reality while collectively reinforcing assumptions that no longer reflect actual business performance. This disconnect often precedes the largest corporate failures because governance begins validating narratives instead of testing operational truth.

Among experienced investigators, one lesson consistently separates ordinary accounting irregularities from enterprise-threatening fraud.

The most damaging corporate frauds are rarely mathematical.

They are narrative frauds.

Narrative fraud occurs when financial statements reconcile perfectly while operational reality steadily diverges from the story management tells investors, regulators, lenders, employees, or even itself. Revenue appears justified because contracts exist. Inventory appears balanced because systems reconcile. Cash flow projections appear credible because assumptions remain internally consistent.

Yet customer demand weakens.

Supply chains deteriorate.

Margins erode.

Risk concentrations accumulate.

Operational evidence quietly contradicts financial storytelling.

By the time numerical inconsistencies emerge, the strategic damage has often become irreversible.

This is why modern forensic accounting increasingly incorporates operational intelligence, digital forensics, behavioral science, communications analysis, cybersecurity signals, procurement analytics, and governance assessment alongside traditional accounting expertise. Financial truth can no longer be extracted from ledgers alone; it must be reconstructed across entire organizational ecosystems.

The competitive landscape is therefore shifting from investigation capacity toward investigative architecture. Firms differentiating themselves over the coming years will not simply employ more forensic accountants. They will integrate multidisciplinary intelligence capabilities capable of monitoring financial ecosystems continuously rather than examining isolated incidents retrospectively.

This evolution also changes the role of governance. Audit committees, compliance leaders, chief risk officers, and boards increasingly require real-time visibility into emerging financial behaviors instead of retrospective assurance that historical controls functioned as intended. Continuous forensic capability is becoming a strategic governance asset rather than an emergency response function.

The organizations that recognize this transition early will gain advantages extending well beyond fraud prevention. They will strengthen investor confidence, improve capital allocation decisions, accelerate regulatory readiness, enhance acquisition due diligence, and create operational transparency that supports long-term resilience.

The direction of the global forensic accounting market is becoming unmistakable. Competitive advantage will belong to enterprises capable of embedding forensic thinking into every significant financial decision, every critical operational workflow, and every governance process. The discipline is evolving from an investigative specialty into an enterprise-wide operating philosophy.

Commercial access details for related research 👉https://www.htfmarketintelligence.com/buy-now?format=1&report=12124

Organizations that continue to treat forensic accounting as an occasional compliance exercise or a post-crisis investigative service misunderstand both the speed and sophistication of modern financial risk. Over the next 24 to 36 months, forensic capability will increasingly define corporate credibility itself. Enterprises that fail to build continuous forensic intelligence into their governance architecture will not merely experience higher compliance exposure-they will face declining stakeholder confidence, mounting regulatory scrutiny, diminished strategic flexibility, and, in the most severe cases, catastrophic reputational collapse from which recovery may prove impossible.

Nidhi Bhawsar (PR & Marketing Manager) https://www.linkedin.com/in/nidhibhawsar/

HTF Market Intelligence Consulting Private Limited

Phone: +15075562445

sales@htfmarketintelligence.com

About Author:

HTF Market Intelligence is a leading market research company providing end-to-end syndicated and custom market page, consulting services, and insightful information across the globe. With over 15,000+ page from 27 industries covering 60+ geographies, value research page, opportunities, and cope with the most critical business challenges, and transform businesses. Analysts at HTF MI focus on comprehending the unique needs of each client to deliver insights that are most suited to their particular requirements.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Forensic Accounting Market: Why Financial Truth Has Become a Continuous Investigation Rather Than an Annual Audit here

News-ID: 4574812 • Views: …

More Releases from HTF Market Intelligence Consulting Private Limited

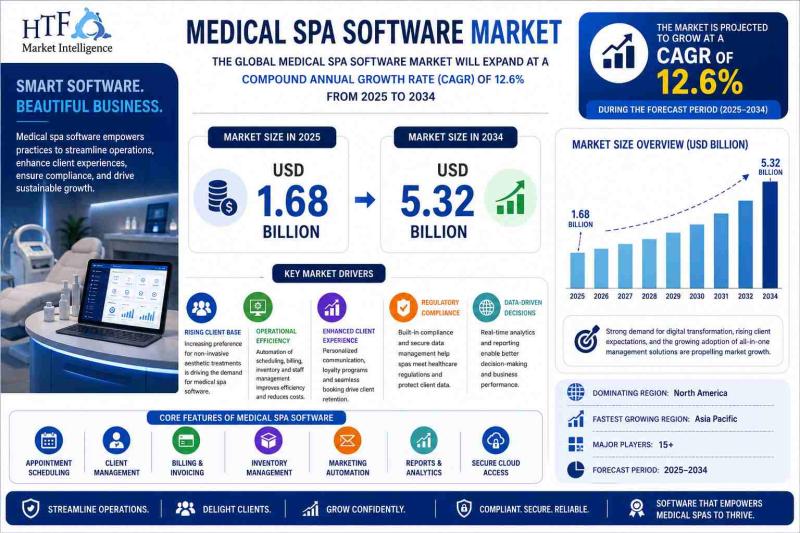

Medical Spa Software Market: Why the Next Competitive Advantage Is No Longer Cli …

Modern medical aesthetics has entered a phase where clinical excellence alone is no longer sufficient to sustain growth. The industry now operates at the intersection of healthcare delivery, luxury consumer experience, recurring retail commerce, and highly regulated patient management. That convergence has fundamentally changed the role of software. Medical spa software is no longer an operational convenience used to schedule appointments or process payments-it has become the central nervous system…

Dogecoin (DOGE) Market is Booming Worldwide | Major Giants Binance, Coinbase, Kr …

The most persistent misunderstanding surrounding Dogecoin is the belief that its longevity is a historical accident. That interpretation misses what has quietly unfolded over the last decade. Dogecoin has evolved into a permanent liquidity reservoir within the global digital asset ecosystem, not because of branding, memes, or internet culture alone, but because it occupies a unique intersection between network effects, accessibility, and investor psychology. Markets repeatedly eliminate assets that fail…

Agentic Commerce Payments Market Hits New High |Visa, Stripe, PayPal

The Global Agentic Commerce Payments Market is not merely introducing a new payment method; it is dismantling one of the oldest assumptions in digital commerce-that every transaction begins with a human click. The next era of commerce is being built around delegated intent, where individuals and enterprises authorize intelligent agents to discover, negotiate, compare, purchase, settle, and optimize transactions autonomously. This shift is not being driven by consumer convenience alone.…

Precision Viticulture Market: Why Vineyard Intelligence Is Becoming More Valuabl …

The defining challenge facing the global wine industry is no longer confined to yield volatility or labor availability. It is the accelerating unpredictability of climate behavior that is reshaping the biological rhythm of vineyards. Traditional assumptions about seasonal progression, water availability, and harvest timing are becoming increasingly unreliable as heat accumulation, rainfall distribution, and frost exposure diverge from historical norms. Thermal zones are shifting, vine physiology is responding differently across…

More Releases for Forensic

Forensic Swab Market Growing with Rising Crime Investigation and Forensic Scienc …

Forensic Swab Market Overview

The forensic swab market is estimated to be valued at USD 4.98 Bn in 2025 and is expected to reach USD 7.40 Bn by 2032, exhibiting a compound annual growth rate (CAGR) of 5.8% from 2025 to 2032.

Coherent Market Insights has published a detailed report offering a comprehensive analysis of the Forensic Swab Market for the forecast period 2025 to 2032. This report provides reliable global and…

Why Digital Forensic Lab is Irreplaceable by Single Forensic Tools?

When it comes to digital forensics, there are always tricks being played by law enforcement agencies who are limited by public sector budget to employ single functionality digital forensic tools instead of bidding and installing an integrate all-function digital forensic lab.

It's not unusual for those medium-small scale countries and political blocked counties.

However, in essence, to equip a complete and scientific digital forensics lab has gradually been a consensus for countries…

Forensic Technologies Market Pegged for Robust Expansion by 2027 | Forensic Tech …

This Forensic Technologies market report is compact however gives precise information in straightforward language. It gives greatest data in least words and this is the strength of this Forensic Technologies market report. It covers everything, which is significant and fundamental for present right data. This Forensic Technologies market report expresses the discoveries, clears the reasons, characterizes sources and gives essential proposals as well.

Get Sample Copy of Forensic Technologies Market Report…

Computer Forensic Technologies and Services Market is Booming Worldwide | Agilen …

Latest released the research study on Global Computer Forensic Technologies and Services Market, offers a detailed overview of the factors influencing the global business scope. Computer Forensic Technologies and Services Market research report shows the latest market insights, current situation analysis with upcoming trends and breakdown of the products and services. The report provides key statistics on the market status, size, share, growth factors of the Computer Forensic Technologies and…

Forensic Technology Market to Witness Superior Growth Along with Agilent Technol …

Forensic Technology Market Overview:

This market research report provides a comprehensive picture on “Forensic Technology Market”, from the global viewpoint, offering a forecast and statistic in terms of revenue during the forecast period. The report covers a descriptive analysis with detailed segmentation, complete research and development history, latest news and press releases. Furthermore, the study explains the future opportunities and a sketch of key players operating in the “Forensic Technology Market”.

Forensic…

Computer Forensic Technologies and Services Market || Key Players Of Market Agil …

CMI released a new market study on 2017-2025 Computer Forensic Technologies and Services Market with 100+ market data Tables, Pie Chat, Graphs & Figures spread through Pages and easy to understand detailed analysis. At present, the market is developing its presence. The Research report presents a complete assessment of the Market and contains a future trend, current growth factors, attentive opinions, facts, and industry validated market data. The research study…