Press release

Agentic Commerce Payments Market Hits New High |Visa, Stripe, PayPal

Agentic Commerce Payments Market

Key Players in This Report Include:

Visa, Mastercard, Stripe, PayPal, Adyen, Block, Fiserv, Worldpay, Checkout.com, Razorpay, Klarna, Amazon Pay, Google Pay, Apple Pay, Shopify

Consider how these insights might influence your strategic decisions 👉

https://www.htfmarketreport.com/sample-report/4419543-agentic-commerce-payments-market

Most discussions around agentic commerce focus on the intelligence of the agent. That is the wrong place to look. The true battleground lies within trust architecture. Intelligence creates decisions; trust authorizes execution. The institutions that dominate the next decade of payments will not necessarily be those with the most advanced AI models. They will be the organizations capable of creating verifiable trust frameworks that allow machines to transact safely at scale.

A useful way to understand the market is through what can be described as the Three Layers of Agentic Financial Trust.

The first layer is Identity Tokenization. Traditional digital identity systems were built for humans. Agentic commerce requires machine-verifiable identities that represent users, businesses, devices, software agents, and delegated permissions simultaneously. Every autonomous purchasing action requires proof not only of who owns the agent but also what authority has been delegated to it. The market is therefore shifting from authentication toward authorization intelligence. Knowing who initiated a transaction is no longer sufficient; financial systems must understand whether the agent was permitted to make that specific decision under predefined conditions.

The second layer is Guardrail Orchestration. Autonomous spending cannot operate within binary approval frameworks. Enterprises and consumers need dynamic spending boundaries, policy engines, risk thresholds, merchant restrictions, procurement rules, and contextual transaction controls. The future payment stack will resemble an operating system more than a traditional authorization network. Agents will continuously negotiate within boundaries established by human principals, creating an entirely new category of financial governance software.

The third layer is Autonomous Settlement. Once an agent reaches a purchasing decision, execution speed becomes critical. Traditional payment rails were designed for human-paced commerce. Agent-driven ecosystems require settlement mechanisms capable of supporting machine-speed transactions, recurring micro-payments, dynamic pricing agreements, and continuous financial exchanges between autonomous systems. Settlement evolves from a back-office function into a real-time computational process.

Our Report Covers the Following Important Topics:

By Type

AI Payment Agents, Autonomous Checkout, Conversational Payments

By Application

Retail Commerce, Subscription Payments, Travel Booking, B2B Procurement

Have different Market Scope & Business Objectives; Enquire for customized study 👉https://www.htfmarketreport.com/enquiry-before-buy/4419543-agentic-commerce-payments-market

One of the most misunderstood aspects of this market is the assumption that existing authentication mechanisms can simply be extended to AI agents. They cannot.

Three-Domain Secure (3DS), one-time passwords, and conventional multi-factor authentication frameworks are fundamentally human-centric technologies. They were designed to interrupt transactions and verify user presence. Agentic commerce removes human presence from the transaction flow by design. An AI procurement agent cannot stop every few seconds to request a fingerprint scan, mobile approval, or SMS verification from its owner. Such interruptions eliminate the economic value of autonomy.

The market therefore demands a replacement architecture based on continuous trust validation rather than episodic authentication. Instead of asking whether a user approved a transaction, future systems must evaluate whether an autonomous action remains compliant with delegated authority, behavioral expectations, contextual risk profiles, and predefined financial constraints. Authentication becomes persistent rather than event-driven.

This transition creates profound challenges for existing card networks. Current payment infrastructure excels at discrete, high-value, human-triggered transactions. Agentic commerce increasingly favors machine-generated transactions that may occur continuously, autonomously, and in extremely small denominations.

Consider an AI travel agent negotiating hotel upgrades, transportation bookings, dining reservations, insurance adjustments, and local service purchases in real time. Hundreds of financial decisions may occur during a single customer journey. Legacy payment rails introduce authorization costs, latency constraints, and operational inefficiencies that become increasingly visible when machines transact with other machines.

This is precisely why programmable money has become strategically important. Stablecoins, tokenized deposits, central bank digital currencies, and other programmable settlement instruments are attracting attention not because they replace traditional payments, but because they align more naturally with machine-native economic activity.

Machines do not think in monthly billing cycles. Machines optimize continuously.

An autonomous logistics network may need to purchase computing resources, charging capacity, routing information, warehouse access, or carbon credits every few seconds. Traditional payment systems struggle under such transaction density. Programmable financial assets enable conditional execution, automated reconciliation, embedded compliance, and machine-speed settlement. As agentic commerce expands, the distinction between payment execution and software execution will steadily disappear.

Another underappreciated reality is that agentic commerce will force a complete reassessment of fraud management. Today's fraud detection systems primarily analyze human behavior. Tomorrow's fraud engines must analyze machine behavior.

The market is moving toward a future where distinguishing between legitimate autonomous activity and malicious autonomous activity becomes exponentially more complex. Fraudsters will deploy intelligent agents capable of mimicking purchasing patterns, negotiating with merchants, adapting to controls, and exploiting vulnerabilities dynamically. Defensive systems must therefore evolve into autonomous risk management platforms capable of countering machine-generated threats in real time.

This evolution inevitably raises one of the most important questions in the industry: liability.

When an AI agent makes a poor purchasing decision, responsibility becomes ambiguous. Is the consumer liable because they delegated authority? Is the software provider responsible because the recommendation engine malfunctioned? Does liability belong to the payment processor, merchant, identity provider, or financial institution?

Evaluate the potential benefits of these trends for your operational needs👉 https://www.htfmarketreport.com/buy-now?format=1&report=4419543

The answer will fundamentally reshape commercial relationships.

The most likely outcome is the emergence of layered liability frameworks. Financial institutions will underwrite transactional risk. AI providers will assume model-performance obligations. Merchants will carry transparency requirements regarding pricing and product representation. New insurance categories will emerge specifically to cover autonomous decision risk. Liability itself becomes a tradable and insurable asset class within the payment ecosystem.

Credit scoring will undergo a similar transformation. Traditional credit models evaluate human repayment behavior. Agentic commerce introduces autonomous spending entities capable of generating their own behavioral histories. Future underwriting systems will increasingly assess the quality of an agent's decision-making performance, purchasing efficiency, negotiation outcomes, compliance record, and risk discipline.

In practical terms, lenders may eventually evaluate not only the financial health of a business but also the operational intelligence of its autonomous agents. The performance of AI-driven procurement systems could become a measurable credit variable.

The downstream implications for merchant acquiring are equally significant.

Historically, acquirers focused on processing transactions. In an agentic economy, transaction processing becomes commoditized. Merchants will require infrastructure that allows agents to negotiate prices, verify inventory, validate credentials, execute contracts, and settle payments automatically.

Acquirers and payment gateways must evolve into commerce orchestration platforms. Their value proposition shifts from moving money to enabling trusted machine-to-machine commercial interactions. The winners will not be those offering the cheapest transaction processing fees. They will be those providing identity assurance, policy enforcement, autonomous dispute resolution, embedded compliance, and intelligent settlement services.

Perhaps the most consequential insight about the Global Agentic Commerce Payments Market is that payments themselves are becoming invisible. The payment is no longer the event. The payment becomes the outcome of an autonomous decision process occurring upstream.

This distinction matters enormously.

For decades, the payments industry optimized transaction completion. Agentic commerce demands optimization of transaction delegation. The center of gravity moves away from checkout experiences and toward trust frameworks, permission architectures, autonomous governance, and programmable settlement mechanisms.

The organizations that recognize this shift early will help define the operating system of machine-native commerce. Those that continue viewing payments as isolated financial events risk becoming utilities in a market increasingly governed by autonomous economic actors. The next chapter of global commerce will not be characterized by faster clicks, smoother checkout pages, or better payment buttons. It will be defined by intelligent agents that negotiate, decide, and transact on behalf of humans-and by the financial infrastructure capable of trusting them to do so

Contact Us:

Nidhi Bhawsar (PR & Marketing Manager)

HTF Market Intelligence Consulting Private Limited

Phone: +15075562445

sales@htfmarketintelligence.com

About Author:

HTF Market Intelligence is a leading market research company providing end-to-end syndicated and custom market page, consulting services, and insightful information across the globe. With over 15,000+ page from 27 industries covering 60+ geographies, value research page, opportunities, and cope with the most critical business challenges, and transform businesses. Analysts at HTF MI focus on comprehending the unique needs of each client to deliver insights that are most suited to their particular requirements.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Agentic Commerce Payments Market Hits New High |Visa, Stripe, PayPal here

News-ID: 4574653 • Views: …

More Releases from HTF Market Intelligence Consulting Private Limited

Dogecoin (DOGE) Market is Booming Worldwide | Major Giants Binance, Coinbase, Kr …

The most persistent misunderstanding surrounding Dogecoin is the belief that its longevity is a historical accident. That interpretation misses what has quietly unfolded over the last decade. Dogecoin has evolved into a permanent liquidity reservoir within the global digital asset ecosystem, not because of branding, memes, or internet culture alone, but because it occupies a unique intersection between network effects, accessibility, and investor psychology. Markets repeatedly eliminate assets that fail…

Precision Viticulture Market: Why Vineyard Intelligence Is Becoming More Valuabl …

The defining challenge facing the global wine industry is no longer confined to yield volatility or labor availability. It is the accelerating unpredictability of climate behavior that is reshaping the biological rhythm of vineyards. Traditional assumptions about seasonal progression, water availability, and harvest timing are becoming increasingly unreliable as heat accumulation, rainfall distribution, and frost exposure diverge from historical norms. Thermal zones are shifting, vine physiology is responding differently across…

Business Income Insurance Market: Why Revenue Protection Has Become a Liquidity …

For decades, business interruption was treated as a straightforward consequence of physical destruction. A manufacturing plant burned, a warehouse flooded, or a production line collapsed, and insurance stepped in to replace lost income while the asset was rebuilt. That framework is steadily losing relevance. Today's corporate balance sheet is increasingly dependent on digital infrastructure, outsourced ecosystems, cloud-based operations, intellectual property, regulatory permissions, and globally distributed supplier networks. Revenue can disappear…

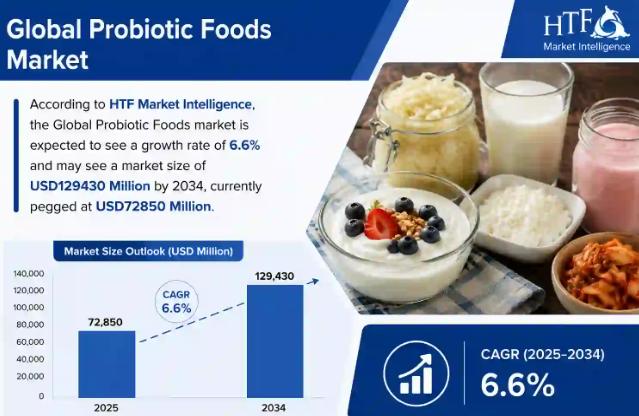

Probiotic Foods Market: The Next Competitive Advantage Will Be Biological Precis …

The most important shift in the probiotic foods market is not that consumers have become more interested in digestive wellness. That transition occurred years ago. The structural transformation underway is far more consequential: consumers are beginning to view everyday food as a mechanism for maintaining physiological resilience before dysfunction emerges. Preventative nutrition is gradually replacing episodic health interventions, and probiotic foods are evolving from a niche functional category into a…

More Releases for Pay

Digital Wallets Market Size Surging at 21.4% CAGR | By Key Players: PayPal, Appl …

The escalation of geopolitical instability triggered by a potential US-Iran conflict is reshaping cross-border payment ecosystems, accelerating the shift toward digital financial infrastructure. Sanctions, currency volatility, and restricted banking channels are pushing both consumers and enterprises toward decentralized and mobile-first payment solutions. Digital wallets are emerging as strategic financial instruments, enabling frictionless transactions, bypassing traditional banking bottlenecks, and ensuring liquidity continuity in volatile markets. Institutional capital is increasingly rotating toward…

Digital Wallets Market to See Thriving Worldwide | PayPal • Apple Pay • Goog …

The latest study by Coherent Market Insights, titled "Digital Wallets Market Size, Share & Trends Forecast 2026-2033," offers an in-depth analysis of the global and regional dynamics shaping this rapidly evolving industry. This comprehensive report highlights the competitive landscape, key market segments, value chain analysis, and emerging technological and regulatory trends expected between 2026 and 2033. The report provides actionable insights for business leaders, policymakers, investors, and new market entrants…

Mobile Payment Market to See Thriving Worldwide| Apple Pay • Google Pay • Sa …

Latest Report, titled Mobile Payment Market 2025-2032 Trends, Share, Size, Growth, Opportunity and Forecast 2025-2032, by Coherent Market Insights offers a comprehensive analysis of the industry, which comprises insights on the market analysis. As part of our Black Friday Limited-Time Discount, this premium research report is now available at up to 60% off, offering an exceptional opportunity for businesses, analysts, and stakeholders to access high-value insights at a significantly reduced…

Unified Payments Interface (UPI) Market Is Booming Worldwide | Google Pay, Amazo …

The latest study released on the Global Unified Payments Interface (UPI) Market by AMA Research evaluates market size, trend, and forecast to 2028. The Unified Payments Interface (UPI) market study covers significant research data and proofs to be a handy resource document for managers, analysts, industry experts and other key people to have ready-to-access and self-analyzed study to help understand market trends, growth drivers, opportunities and upcoming challenges and about…

Unified Payments Interface (UPI) Market May See a Big Move | Major Giants Samsun …

The latest study released on the Global Unified Payments Interface (UPI) Market by AMA Research evaluates market size, trend, and forecast to 2027. The Unified Payments Interface (UPI) market study covers significant research data and proofs to be a handy resource document for managers, analysts, industry experts and other key people to have ready-to-access and self-analyzed study to help understand market trends, growth drivers, opportunities and upcoming challenges and about…

Samsung Pay Market is Booming Worldwide with Samsung Pay, Apple Pay, Google Pay

HTF Market Intelligence released a new research report of 23 pages on title 'Samsung Pay - Competitor Profile' with detailed analysis, forecast and strategies. The study covers key regions that includes North America, LATAM, United States, GCC, Southeast Asia, Europe, APAC, United Kingdom, India or China etc and important players such as Samsung Pay, Apple Pay, Google Pay, Alipay, Tenpay, Samsung Electronics, Visa, Mastercard.

Request a sample report @ https://www.htfmarketreport.com/sample-report/3587660-samsung-pay-competitor-profile

Summary

Samsung…