Press release

Germany Leads as B100 Commands Largest Share, Fuel Leads Application: Europe Biodiesel Market at 5.25% CAGR Through 2034

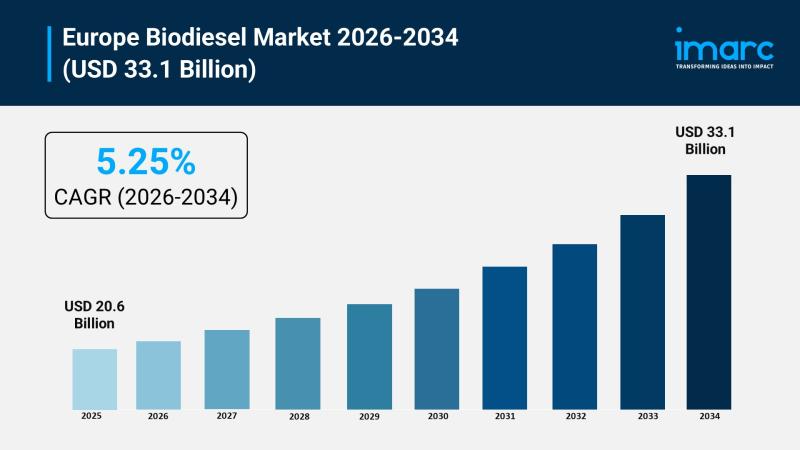

Europe Biodiesel Market Graph 2026

Read The Full Report With The List Of TOC: https://www.imarcgroup.com/europe-biodiesel-market

Within Europe‚ the biodiesel industry is not an experimental clean energy project‚ it is a full-scale industrial undertaking which grows‚ sources‚ chemically processes‚ distributes and blends‚ and makes biodiesel available for use in power generation in five major country markets. For producers‚ feedstock suppliers‚ fuel distributors‚ investors and fleet owners‚ the market opportunity offered by the USD 12.5 Billion in absolute value added over the forecast period is one of the key growth opportunities in European clean energy.

Market Snapshot

Market Size (2025): USD 20.6 Billion

Forecast (2034): USD 33.1 Billion

CAGR (2026-2034): 5.25%

Leading Country: Germany

Leading Feedstock: Vegetable Oils

Leading Application: Fuel

Leading Blend Type: B100

Leading Production Technology: Conventional Alcohol Trans-esterification

For Expert Analysis on European Industry: https://www.imarcgroup.com/europe-market-research

Key Growth Drivers: Three Forces Sustaining the Market

1. Stringent EU Environmental Regulations and CO2 Reduction Targets

The single most powerful driver of Europe's biodiesel market is the EU's regulatory framework on carbon emissions, which has established binding, time-phased reduction targets across the transport sector.

The updated EU CO2 emission standards for new trucks establish a clear mandatory trajectory:

15% CO2 reduction required by 2025 compared to 2019 reporting year levels

45% CO2 reduction required by 2030

65% CO2 reduction required by 2035

90% CO2 reduction required by 2040

The targets create a structural demand floor for biodiesel‚ insulated from fluctuations in market pricing. Transport operators and fleet owners that cannot meet standards through electrification alone‚ particularly in heavy freight where battery technology is still nascent‚ are already moving to higher blend ratios of biodiesel as an immediately deployable pathway.

The carbon savings of biodiesel can be important; according to the European Biodiesel Board‚ biodiesel generates 65 to 90% less CO2 compared to diesel. Biodiesel reduces CO2 emissions by 3 kg for every kg consumed. In addition‚ biodiesel combustion results in reduced exhaust particulate matter‚ carbon monoxide and hydrocarbons‚ thus offering an improvement in air quality as well.

2. Rising Renewable Energy Targets and REPowerEU

Europe's renewable energy targets are another demand pull for biodiesel. The European Parliament has approved a target of 42.5% of total energy demand from renewable energy sources by 2030. EU countries are encouraged to reach a 45% share‚ as targeted in European Commission's REPowerEU plan‚ which seeks to end the continent's dependence on Russian fossil fuel imports. The target includes 45% share of renewable energy in electricity‚ industry‚ buildings and transport by 2030.

Because biodiesel is made from renewable sources like vegetable oils and animal fats‚ it is a potential candidate to satisfy government renewable fuel mandates for transportation‚ as one of the few low-carbon fuel options that can be used immediately in existing diesel engines‚ and distributed through the existing diesel fuel supply infrastructure without the need for a large fleet turnover.

Many European countries combine this with fiscal incentives including tax exemptions‚ subsidies for biodiesel production and blending‚ and grants for second generation (2G) biofuel research and development. Such incentives improve the economics of biodiesel relative to fossil diesel‚ especially at high blending levels where the cost of biodiesel has always been at its most unattractive.

3. Circular Economy Practices and Feedstock Diversification

In Europe‚ the recent shift to circular economy approaches has meant a move away from first generation virgin vegetable oils for biodiesel production‚ towards waste-derived feedstocks which provide environmental and economic advantages.

Used cooking oil has become one of the most commercially important biodiesel feedstocks in Europe. The use of used cooking oil as a biodiesel feedstock more than doubled from 2015 through the early 2020s‚ with much of it going to biodiesel to power cars and trucks across Europe. This is in line with the EU waste reduction targets and EU sustainability requirements for advanced biofuel certification schemes.

Hydrotreated Vegetable Oil (HVO) technology is considered the best route for producing a high quality renewable diesel through the hydrogenation of vegetable oils. HVO can produce fuel with better properties and with a higher degree of compatibility with diesel engines compared to other processes. Repsol is heavily investing in advanced biofuels. Repsol plans on building a 250‚000 tonnes per year advanced biofuels plant in Cartagena‚ Spain‚ the largest new capacity for waste-based and advanced biodiesel in Europe.

Access Deeper Insights into the Europe Biodiesel Market Report: https://www.imarcgroup.com/europe-biodiesel-market/requestsample

Market Segmentation: Four Dimensions of Commercial Structure

By Feedstock: Vegetable Oils Lead, Waste Streams Gaining

Vegetable oils‚ particularly canola (rapeseed)‚ sunflower and soybean oils‚ constitute the largest proportion of feedstocks used for biodiesel. In Europe‚ high domestic agriculture enables easy access to local supply chains‚ therefore‚ reducing import use and helping farm incomes. Vegetable oils contain relatively high levels of unsaturation‚ and therefore are suitable feedstocks for customary transesterification‚ with established supply chains that can be integrated into biodiesel production.

Animal fats and other waste feedstocks‚ such as used cooking oil and crop residues‚ are the fastest growing feedstocks. Waste inputs are favored by the EU's Renewable Energy Directive (RED)‚ which incentivizes the use of waste-based and sustainably produced feedstocks. The European Biodiesel Board have requested that the RED's Annex IX be expanded to include other feedstocks‚ to allow other waste- and residue-based feedstocks to be eligible for advanced biofuel credit which benefits biodiesel producers.

By Application: Fuel Dominates Across Transportation Sectors

The largest market for biodiesel is in fuel. Biodiesel is mainly used directly as a replacement for diesel in vehicles‚ including on-road freight‚ passenger cars and public transport fleets. It is being increasingly used in the marine and aviation bunker industries. Since existing engines can burn it and existing fuel distribution systems can deliver it‚ there is no initial capital cost barrier to adoption at the fleet or national fuel supply level.

The second application is in power generation. Biodiesel is a potential backup fuel for distributed generation assets‚ and may be a renewable power source for industrial and commercial electricity users trying to reduce their grid carbon footprint.

The use of biodiesel is spurred by business sustainability efforts. Businesses and fleet owners set blending requirements as part of a formal carbon reduction strategy‚ and corporate procurement requirements scaled beyond the regulated biodiesel blending requirements have resulted in increased demand for biodiesel.

By Type: B100 Holds the Largest Share

B100 (the pure form of biodiesel) accounts for the biggest share of the EU biodiesel market by product category. As a 100% renewable unblended product‚ it represents the most direct decarbonization potential of biodiesel and is the biodiesel product that corresponds best to the highest EU renewable energy and decarbonization ambitions.

B100 is compatible with diesel engine technology‚ distribution‚ storage and dispensing facilities‚ and offers the highest GHG emission reduction benefit compared to fossil diesel fuel. The blending flexibility of B100 can be used to produce blended fuels (biodiesel blends) of varying biodiesel content‚ including B20‚ B10 or B5 biodiesel. This flexibility allows producers and distributors to meet a wide variety of requirements between fleets and jurisdictions.

B20 and B10 blends are widely used in the middle of the market‚ where fleet operators seek to optimize emissions performance against the price of the blend‚ and B5 blends are the standard low level biodiesel blends that are a requirement for mandatory blending in many European countries.

By Production Technology: Conventional Transesterification Dominates

The conventional process for the production of biodiesel is transesterification of vegetable oils or animal fats. This is the most common production technology as it is the standard pathway of the conventional industry. Transesterification is the conversion of vegetable oils or animal fats to biodiesel via reaction with an alcohol‚ usually methanol or ethanol‚ yielding glycerol. It is often employed for its long tradition of process optimization‚ compatibility with existing production plants and ability to produce biodiesel conforming to EU standards.

Hydro heating (HVO) is the fastest growing production technology‚ with superior fuel quality for cold weather use and shelf life compared to customary FAME-grade biodiesel. HVO is growing in use because consumers prefer it‚ and it is increasingly used for premium blends where performance requirements cannot be achieved with customary transesterification products.

Pyrolysis is used in specialized production applications‚ to process feedstocks with heterogeneous qualities‚ such as non-food-grade wastes from agriculture and contaminated waste oils.

Country Analysis: Germany Leads Five National Markets

Germany has the most dominant country market share in Europe's biodiesel market partly due to the EEG law (Renewable Energy Sources Act)‚ which is the main legal instrument requiring use of biofuels in transportation fuels and guarantees domestic demand stability for biodiesel products. Its geographic location is also convenient to distribute biodiesel throughout the rest of Europe. The demand for liquid biofuels from circular economy resources (waste resources) is also high in Germany.

The four additional country markets each contribute distinct demand dynamics:

France combines strong agricultural feedstock production capacity with active government support for biofuels as part of its national energy transition strategy, making it a significant both production and consumption market.

United Kingdom maintains its biodiesel market through domestic blending mandates and growing corporate sustainability procurement requirements across major fleet operators.

Italy is an active biodiesel market with strong processing industry presence and growing renewable fuel adoption in road transport.

Spain is expanding its advanced biofuels production base, exemplified by Repsol's major Cartagena facility investment, positioning itself as a significant future biodiesel production hub within the European supply chain.

Competitive Landscape and Industry Players

The European biodiesel market is fragmented‚ consisting of integrated energy companies‚ biodiesel producers and commodity traders involved in production‚ blending and distribution of biodiesel.

The largest players in the market are Trafigura Group‚ who entered the European biodiesel market following the acquisition of Greenergy's European activities‚ which had given them a large road fuel supply and biodiesel production platform in the UK. The Spanish oil company Repsol also has a biofuels plant in Cartagena with the capacity of 250‚000 tonnes of biofuels per annum. Bunge and Repsol together have plans to meet the increasing demand for low carbon feedstock for renewable fuels in Europe. OMV Petrom‚ an integrated energy group in the south east of Europe‚ acquired a stake in an used cooking oil collection company to de-risk the supply of waste-based feedstocks for the production of HVO. Vopak has built more dedicated storage capacity at their Vlaardingen terminal in Rotterdam for supply from waste-based biodiesel feedstocks.

Competition in this market is increasingly centered on:

Access to certified waste and residue feedstocks that qualify for advanced biofuel status under EU RED

Investment in HVO production technology to serve premium fuel market segments

Distribution network coverage across Europe's major port and road logistics corridors

Compliance with EU sustainability certification requirements (ISCC, RSB) that gate access to government-supported blending mandates and renewable energy credit markets

Request Customization: https://www.imarcgroup.com/request?type=report&id=2850&flag=E

Europe Biodiesel Market Outlook

Large increases in the Europe biodiesel market from USD 20.6 Billion in 2025 to USD 33.1 Billion in 2034 are supported by a mutually reinforcing and interlocking set of policy‚ technology and commercial drivers. The EU mandated CO2 reduction schedule for transportation is the minimum market demand floor for biodiesel. Next‚ REPowerEU renewable energy targets have turned political ambition into procurement obligation‚ while the widening availability of feedstocks from waste through circular economy supply chains is improving biofuels' sustainability and economics in the process.

At a projected CAGR of 5.25%‚ the EU biodiesel market is expected to provide stable growth opportunities for biodiesel feedstock aggregators‚ processing technology providers‚ blenders‚ distributors and fleet operators spanning the biodiesel value chain from transportation applications‚ including heavy road freight and marine shipping‚ through to power generation in a market which has structural depth‚ regulatory certainty and an ambitious policy framework that is rigorously enforced.

Media & Sales Contact

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201971-6302

About IMARC Group

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Germany Leads as B100 Commands Largest Share, Fuel Leads Application: Europe Biodiesel Market at 5.25% CAGR Through 2034 here

News-ID: 4539402 • Views: …

More Releases from IMARC Group

India Security Market Report 2026-2034: Industry Reaching USD 14.82 Billion at 1 …

According to the latest research report titled "India Security Market Size, Share, Trends and Forecast by System, Service, End User, and Region, 2026-2034", the report offers a comprehensive analysis of the industry, including India security market analysis, size, growth trends, key drivers, and regional insights.

How Big is the India Security Market?

The India security market size was valued at USD 5.50 Billion in 2025 and is projected to reach USD 14.82…

United States Automotive Connectors Market Set to Reach USD 5.21 Billion by 2034

The United States automotive connectors market reached USD 3.74 Billion in 2025 and is projected to reach USD 5.21 Billion by 2034, growing at a CAGR of 3.76% during 2026-2034, according to IMARC Group. Automotive connectors are electrochemical elements that transmit electric signals between a vehicle's power source and its electronic systems including safety, powertrain, infotainment, and body control modules making them indispensable components in every vehicle produced in the…

R-PET Prices Surge Across Key Markets: Latest Trends, Demand Outlook, and 2026 F …

The global recycled polyethylene terephthalate (R-PET) market experienced noticeable price shifts during the first quarter of 2026, driven by changing virgin PET trends, fluctuating recycling facility operations, and shifting demand from downstream sectors like packaging, textiles, consumer goods, and industrial manufacturing. Stakeholders closely tracked supply chain health, as collection expenses, raw material availability, and regional trade patterns heavily dictated pricing across major international markets. While certain regions saw modest supply…

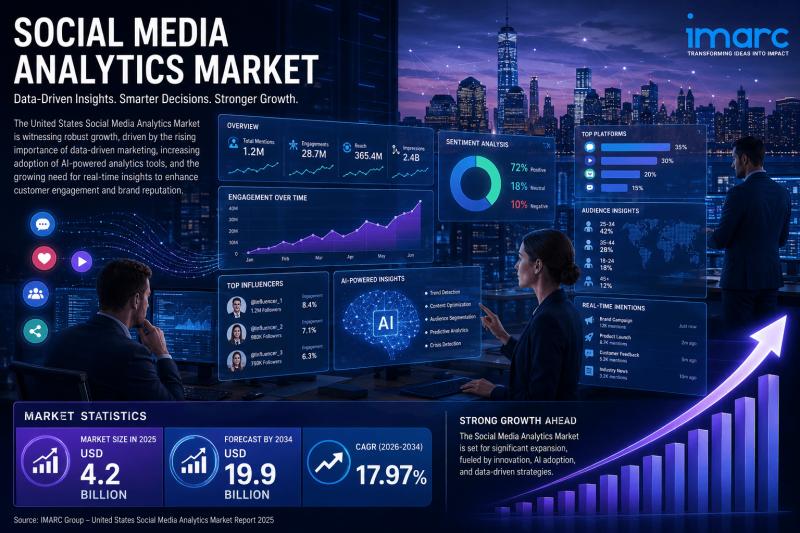

United States Social Media Analytics Market Set to Reach USD 19.9 Billion by 203 …

The United States social media analytics market is experiencing one of the most dynamic growth phases in the technology sector, propelled by the convergence of artificial intelligence, real-time data intelligence, influencer marketing proliferation, and the accelerating shift of brand strategy toward data-driven decision-making. According to IMARC Group, the market reached USD 4.2 Billion in 2025 and is projected to reach USD 19.9 Billion by 2034, growing at a CAGR of…

More Releases for Europe

2019 Strategy Consulting Market Analysis | McKinsey, The Boston Consulting Group …

Strategy Consulting Market reports also offer important insights which help the industry experts, product managers, CEOs, and business executives to draft their policies on various parameters including expansion, acquisition, and new product launch as well as analyzing and understanding the market trends

Need for strategic planning in highly competitive environment and to develop business capabilities to meet & exceed the emerging requirements are the major drivers which help in surging…

Strategy Consulting Market 2025 | Analysis By Top Key Players: Booz & Co. , Rola …

Global Strategy Consulting Market 2019-2025, has been prepared based on an in-depth market analysis with inputs from industry experts. This report covers the market landscape and its growth prospects over the coming years. The report also includes a discussion of the key vendors operating in this market.

The key players covered in this study

McKinsey , The Boston Consulting Group , Bain & Company , Booz & Co. , Roland Berger Europe…

Digital Strategy Consulting Market is Thriving Worldwide with Deloitte, McKinsey …

A Digital Strategy is a form of strategic management and a business answer or response to a digital question, often best addressed as part of an overall business strategy. A digital strategy is often characterized by the application of new technologies to existing business activity and focus on the enablement of new digital capabilities to their business.

A new report as a Digital Strategy Consulting market that includes a comprehensive analysis…

Strategy Consulting Market 2019: By McKinsey, The Boston Consulting Group, Bain …

This report studies the global Strategy Consulting market, analyzes and researches the Strategy Consulting development status and forecast in United States, EU, Japan, China, India and Southeast Asia. This report focuses on the top players in global market, like

• McKinsey

• The Boston Consulting Group

• Bain & Company

• Booz & Co.

• Roland Berger Europe

• Oliver Wyman Europe

• A.T. Kearney Europe

• Deloitte

• Accenture Europe

Get Sample Report@ https://www.reporthive.com/enquiry.php?id=1247388&req_type=smpl&utm_source=AB

Market segment by Type, the product can be split into

• Operations Consultants

• Business Strategy Consultants

• Investment Consultants

• Sales and…

Strategy Consulting Market Analysis 2018: McKinsey, The Boston Consulting Group, …

Orbis Research Present’s “Global Strategy Consulting Market” magnify the decision making potentiality and helps to create an effective counter strategies to gain competitive advantage.

The global Strategy Consulting status, future forecast, growth opportunity, key market and key players. The study objectives are to present the Strategy Consulting development in United States, Europe and China.

In 2017, the global Strategy Consulting market size was million US$ and it is expected to reach million…

Influenza Vaccination Market Global Forecast 2018-25 Estimated with Top Key Play …

UpMarketResearch published an exclusive report on “Influenza Vaccination market” delivering key insights and providing a competitive advantage to clients through a detailed report. The report contains 115 pages which highly exhibits on current market analysis scenario, upcoming as well as future opportunities, revenue growth, pricing and profitability. This report focuses on the Influenza Vaccination market, especially in North America, Europe and Asia-Pacific, South America, Middle East and Africa. This…