Press release

United States Automotive Connectors Market Set to Reach USD 5.21 Billion by 2034

Key Statistics at a Glance

• Base Year: 2025

• Historical Years: 2020-2025

• Forecast Years: 2026-2034

• Market Size in 2025: USD 3.74 Billion

• Market Forecast in 2034: USD 5.21 Billion

• Market Growth Rate (2026-2034): 3.76% CAGR

• Leading Connection Type: Wire to Board Connection

• Leading Connector Type: PCB Connectors

• Leading System Type: Sealed Connector System

• Leading Vehicle Type: Passenger Cars

• Leading Application: Safety and Security System

• Key Regions: Northeast, Midwest, South, West

Explore Opportunities in the United States Automotive Connectors Market Download the IMARC Sample Report: https://www.imarcgroup.com/united-states-automotive-connectors-market/requestsample

Latest News: US Automotive Connectors Market (2024-2026)

January 2025: TE Connectivity Raises EUR 750 Million to Expand Automotive Connector Portfolio

TE Connectivity, the world's largest automotive connector manufacturer, raised EUR 750 million in senior notes in January 2025 to fund acquisitions aimed at expanding its automotive connector and sensor product lines. The capital raise reflects TE Connectivity's strategic confidence in long-term EV and ADAS connector demand, with specific focus on high-voltage power connectors, 48V system architecture components, and sensor-integrated connector assemblies for next-generation vehicle platforms. The company reported automotive segment revenue of USD 1.79 Billion in Q4 FY2025, growing 4% year-on-year, underscoring the resilience of connector demand even amid broader automotive production variability.

January 2025: Amphenol Completes USD 2.025 Billion Acquisition of CIT to Broaden Automotive Reach

Amphenol, one of the leading global connector manufacturers with significant US automotive market presence, completed its USD 2.025 billion acquisition of CIT (Custom Interconnects Technologies) in January 2025 to broaden its end-market reach across automotive, industrial, and defence connector segments.

The acquisition adds complementary high-reliability connector families and manufacturing capabilities to Amphenol's existing automotive product range, strengthening its competitive position against TE Connectivity and Molex in EV powertrain and ADAS connector sourcing programmes at major US OEMs including Ford, GM, and Stellantis.

2025-2026: EV High-Voltage Connector Standards Driving Platform-Level Design Changes

The accelerating adoption of 800V battery architectures in premium and mainstream electric vehicles is driving fundamental design changes in US automotive high-voltage connector specifications, as OEMs transition from 400V to 800V platform standards to enable faster DC charging and improved powertrain efficiency.

High-voltage connectors for 800V systems require enhanced insulation materials, liquid-cooled contact interfaces, and zero-wear gold plating on contact surfaces to meet the demanding thermal and electrical requirements of next-generation EV powertrains. Suppliers including TE Connectivity, Aptiv, Molex, and Yazaki are accelerating development of 800V-rated connector systems to secure design wins on the next wave of US EV platform launches from GM's Ultium platform, Ford's second-generation EV architecture, and new entrants targeting the US market.

2025-2026: Fiber Optic Connector Adoption Accelerating in ADAS and Infotainment Systems

The shift from traditional copper cable harnesses to plastic optical fiber (POF) and glass optical fiber connectors is accelerating in US vehicle production as OEMs prioritise weight reduction, electromagnetic interference immunity, and the multi-gigabit data transmission speeds required by advanced ADAS sensor fusion systems and over-the-air (OTA) update architectures.

Fiber optic connectors enable data transmission speeds exceeding 10 Gbps essential for connecting LiDAR, radar, camera, and AI processing unit data streams in autonomous and semi-autonomous vehicle platforms while simultaneously reducing harness weight by up to 30% compared to equivalent copper cable solutions. Leading suppliers are investing in miniaturised, high-density fiber optic connector designs optimised for the space-constrained packaging requirements of EV platforms where battery pack architecture limits available wiring routing space.

2026 Outlook: Key Drivers Shaping the Market

Electric Vehicle Adoption Elevating Connector Content Per Vehicle

Every electric vehicle produced in the United States contains significantly more connectors than a comparable internal combustion engine vehicle with high-voltage battery management systems, onboard chargers, DC-DC converters, and motor control units all requiring dedicated, safety-certified connector assemblies that have no equivalent in ICE drivetrains.

As US EV sales are projected to continue growing through 2026 despite near-term tariff headwinds, the structural increase in connector content per EV estimated at 2-3 times the connector count of equivalent ICE vehicles provides durable volume uplift for US connector suppliers regardless of overall vehicle production levels.

ADAS and Autonomous Driving Expanding Safety Connector Demand

The mandatory rollout of advanced driver assistance systems including automatic emergency braking, lane-keep assist, adaptive cruise control, and blind-spot monitoring across new US vehicle lines driven by NHTSA regulations and Euro NCAP safety rating requirements is creating sustained demand for high-reliability, sealed connector systems in safety-critical applications. Each ADAS sensor node requires multiple connector interfaces between radar, camera, LiDAR, and ultrasonic sensor units and the vehicle's central processing architecture, multiplying connector count per vehicle as safety feature content continues to expand with every new model year.

Miniaturisation and High-Speed Data Connector Innovation

The convergence of vehicle electrification, software-defined vehicle architectures, and over-the-air update requirements is driving strong demand for miniaturised, high-speed data connectors capable of handling multi-gigabit Ethernet, USB 4.0, and automotive-grade fiber optic data transmission within compact vehicle packaging. Leading manufacturers including TE Connectivity, Aptiv, and Molex are prioritising zero-wear plating technologies, multi-gigabit data path connectors, and high-density modular connector systems to address the growing bandwidth requirements of next-generation vehicle electronic architectures without adding weight or bulk to the vehicle's wiring infrastructure.

Speak to An Analyst: https://www.imarcgroup.com/request?type=report&id=2855&flag=C

United States Automotive Connectors Market Segment Analysis

By Connection Type

• Wire to Board Connection: The leading connection type, widely used across powertrain control modules, ADAS processing units, infotainment systems, and body control modules where secure, space-efficient PCB mounting is required.

• Wire to Wire Connection: Extensively used in vehicle harness construction for connecting power and signal cables across distributed vehicle subsystems, particularly in engine bay and underbody applications requiring durable, sealed connections.

• Board to Board Connection: A growing category driven by the increasing density of electronic control units in EV battery management, ADAS, and domain controller architectures requiring compact, high-pin-count interconnection between PCB layers.

By Connector Type

• PCB Connectors: The dominant connector type, used across virtually every electronic control unit in modern vehicles from engine management and transmission control to infotainment, ADAS, and battery management systems.

• Fiber Optic Connectors: The fastest-growing connector type, driven by automotive infotainment (MOST standard), ADAS sensor data networks, and high-speed vehicle communication backbones requiring EMI-immune, high-bandwidth connectivity.

• RF Connectors: Critical for vehicle-to-everything (V2X) communication, cellular connectivity, GPS, and radar-based ADAS systems, with demand growing alongside the proliferation of connected vehicle features.

• IC and Others: Integrated circuit connectors and specialty types serve specific powertrain, safety system, and sensor interface applications across passenger, commercial, and electric vehicle platforms.

By System Type

• Sealed Connector System: The dominant system type, essential for engine bay, underbody, exterior lighting, and battery pack applications where connectors must withstand moisture, dust, temperature extremes, and vibration throughout the vehicle's operational life.

• Unsealed Connector System: Used in protected interior applications including dashboard electronics, infotainment, interior lighting, and cabin control modules where environmental exposure is limited and IP-rating requirements are less stringent.

By Vehicle Type

• Passenger Cars: The largest vehicle segment by connector volume, driven by high production volumes, increasing electronic content per vehicle, and expanding ADAS and infotainment feature requirements across all price segments.

• Electric Vehicles: The fastest-growing vehicle segment for connector demand, with EVs requiring specialised high-voltage power connectors, battery management system connector arrays, and onboard charging interfaces not present in ICE vehicles.

• Commercial Vehicles: A growing segment for heavy-duty sealed connector systems in truck and fleet electrification, telematics, advanced braking systems, and Class 8 truck powertrain management applications.

By Application

• Safety and Security System: The largest application segment, encompassing ADAS sensor connectors, airbag system interfaces, anti-theft and keyless entry connectors, and adaptive cruise control wiring all requiring high-reliability, vibration-resistant sealed connector designs.

• Body Control and Interiors: A high-volume segment covering interior lighting, power windows, seat adjustment, climate control, and door module connectors across all vehicle categories.

• Infotainment, Navigation & Instrumentation: A fast-growing application driven by increasing screen size, multi-zone audio, wireless connectivity, and digital instrument cluster feature content requiring high-speed data connector solutions.

• Engine Control, Powertrain, and Fuel Systems: Critical sealed connector applications for engine management units, transmission control, cooling system management, and (in EVs) battery thermal management and high-voltage power distribution.

By Region

• Midwest (Michigan, Ohio, Indiana): The dominant US automotive connector market region, anchored by the Detroit OEM and Tier 1 supplier ecosystem encompassing Ford, GM, Stellantis, and their primary connector and harness supply chains.

• South (Kentucky, Tennessee, Alabama, Texas): A rapidly growing connector demand region driven by Toyota, BMW, Volkswagen, Hyundai, and Tesla manufacturing facilities, along with expanding EV battery gigafactory supply chain development.

• West (California): Home to Tesla's Fremont assembly operations and Silicon Valley's automotive software and sensor companies, driving premium EV connector and high-speed data connector demand.

• Northeast: Supports connector distribution, aftermarket, and speciality automotive electronics manufacturing serving the region's dense vehicle service and fleet management sectors.

Key Market Trends

• High-Voltage EV Connector Demand Surging: The transition to 800V EV platform architectures across US OEMs is driving premium-priced, safety-certified high-voltage connector demand, with average connector revenue per EV significantly exceeding that of equivalent ICE vehicles.

• Copper to Fiber Optic Transition Accelerating: Leading US OEMs are actively replacing copper wiring with POF cables to reduce harness weight - a critical factor in maximising EV range - and enable the multi-gigabit data transmission required by ADAS and OTA update systems.

• Sealed Connector Dominance in Safety Applications: NHTSA safety mandates and ADAS proliferation are structurally shifting the connector mix toward higher-value sealed systems in safety-critical applications, improving average selling prices for connector manufacturers.

• Miniaturisation Without Compromising Reliability: Manufacturers are developing increasingly compact, high-pin-density connector formats that meet the space constraints of EV battery packs and ADAS sensor module housings while maintaining the vibration resistance and IP ratings required for automotive qualification.

• Supply Chain Vertical Integration: Leading US connector suppliers are investing in in-house stamping, over-moulding, and precision plating capabilities to reduce supply chain vulnerability, improve quality control, and protect margins against raw material cost volatility.

Frequently Asked Questions (FAQs)

Q1. What was the size of the US automotive connectors market in 2025?

The United States automotive connectors market reached USD 3.74 Billion in 2025, according to IMARC Group. The market is driven by the accelerating adoption of electric vehicles, government road safety mandates requiring ADAS integration, and growing demand for high-speed data and high-voltage power connector solutions across all vehicle categories.

Q2. What is the projected growth rate and forecast value of the market?

The US automotive connectors market is projected to grow at a CAGR of 3.76% during 2026-2034, reaching USD 5.21 Billion by 2034. Growth is supported by expanding EV production, increasing connector content per vehicle, fiber optic adoption in vehicle communication systems, and the proliferation of ADAS applications across passenger and commercial vehicle platforms.

Q3. Which connection type leads the US automotive connectors market?

Wire to board connection currently holds the largest share of the US automotive connectors market, driven by its widespread use in PCB-mounted electronic control units across engine management, infotainment, ADAS, and body control module applications. Board to board connections are the fastest-growing type as EV domain controller architectures and multi-layer ECU designs drive demand for compact, high-density PCB interconnection solutions.

Q4. Which vehicle type is the fastest growing in the US automotive connectors market?

Electric vehicles represent the fastest-growing vehicle type for connector demand in the US market, driven by the significantly higher connector content required for high-voltage battery management systems, onboard charging units, motor control inverters, and thermal management systems that have no equivalent in internal combustion engine vehicles. Each EV platform is estimated to contain 2-3 times the connector count of a comparable ICE vehicle, providing durable volume and revenue uplift for connector suppliers as EV production scales.

Q5. Who are the key players in the US automotive connectors market?

The US automotive connectors market is led by TE Connectivity - the world's largest automotive connector manufacturer - alongside Amphenol, Aptiv, Molex, Yazaki, Sumitomo Electric, and JAE Electronics. TE Connectivity raised EUR 750 million in January 2025 to fund connector and sensor portfolio expansion, while Amphenol completed the USD 2.025 billion acquisition of CIT in the same month to broaden its automotive and industrial connector capabilities.

Q6. What is driving the adoption of fiber optic connectors in US automotive applications?

Fiber optic connectors are gaining rapid adoption in US vehicles due to their ability to deliver multi-gigabit data transmission speeds - essential for connecting LiDAR, radar, camera, and AI processing units in ADAS architectures - while simultaneously reducing harness weight by up to 30% compared to copper cable equivalents. The MOST (Media Oriented Systems Transport) fiber optic standard is widely deployed in premium vehicle infotainment networks, and automotive-grade POF and glass fiber connectors are increasingly being specified for ADAS sensor fusion backbone applications across mainstream vehicle platforms.

Q7. What are the biggest growth opportunities in the US automotive connectors market through 2034?

The largest growth opportunities include high-voltage connector systems for 800V EV platform architectures, miniaturised high-speed data connectors for software-defined vehicle and OTA update architectures, sealed ADAS sensor connectors driven by mandatory safety system rollout, and fiber optic connector systems for vehicle communication backbones. The commercial vehicle electrification segment - including Class 8 electric truck platforms from Freightliner, Peterbilt, and Kenworth - represents an emerging high-value connector opportunity as fleet electrification accelerates through the late 2020s.

Author IMARC Group

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA,

Email: sales@imarcgroup.com,

United States: +1-201971-6302

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release United States Automotive Connectors Market Set to Reach USD 5.21 Billion by 2034 here

News-ID: 4538344 • Views: …

More Releases from IMARC Group

R-PET Prices Surge Across Key Markets: Latest Trends, Demand Outlook, and 2026 F …

The global recycled polyethylene terephthalate (R-PET) market experienced noticeable price shifts during the first quarter of 2026, driven by changing virgin PET trends, fluctuating recycling facility operations, and shifting demand from downstream sectors like packaging, textiles, consumer goods, and industrial manufacturing. Stakeholders closely tracked supply chain health, as collection expenses, raw material availability, and regional trade patterns heavily dictated pricing across major international markets. While certain regions saw modest supply…

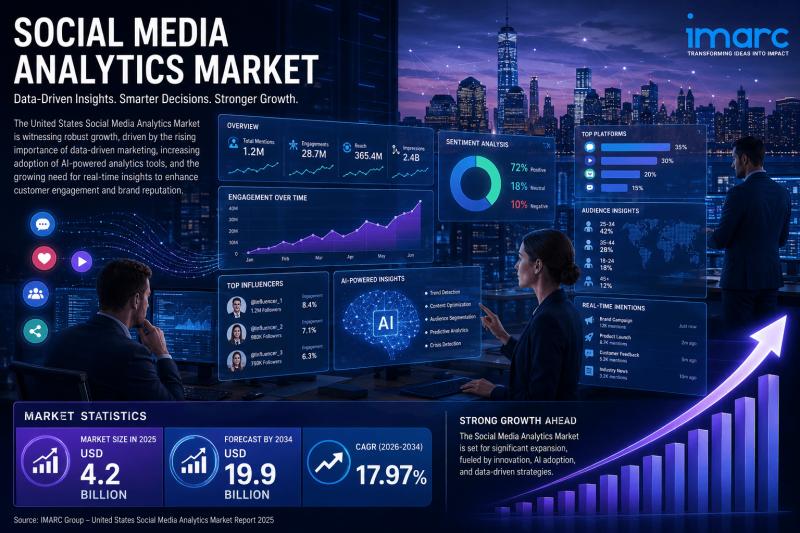

United States Social Media Analytics Market Set to Reach USD 19.9 Billion by 203 …

The United States social media analytics market is experiencing one of the most dynamic growth phases in the technology sector, propelled by the convergence of artificial intelligence, real-time data intelligence, influencer marketing proliferation, and the accelerating shift of brand strategy toward data-driven decision-making. According to IMARC Group, the market reached USD 4.2 Billion in 2025 and is projected to reach USD 19.9 Billion by 2034, growing at a CAGR of…

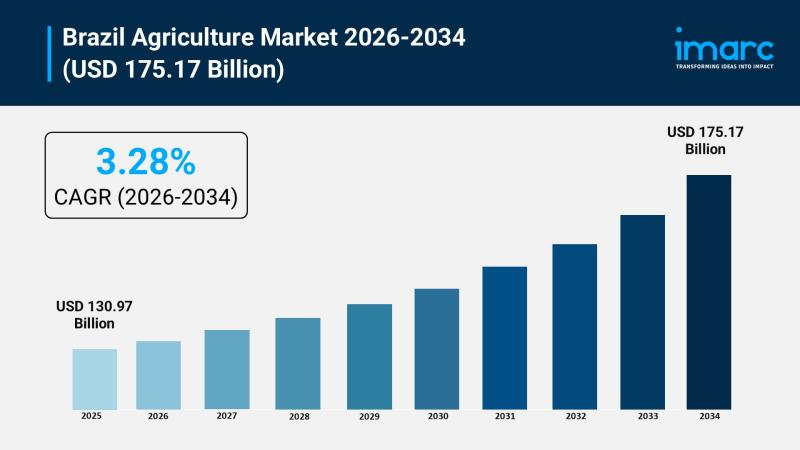

Brazil Agriculture Market Valued at USD 130.97 Billion in 2025, Targeting USD 17 …

Brazilian agriculture is influential in world food security and is considered a core part of the economy of Brazil. In 2025‚ the agriculture market of Brazil was valued at USD 130.97 billion. The market is forecasted to reach a size of USD 175.17 billion by 2034‚ at a CAGR of 33.6% in absolute terms. It is expected to be driven by a CAGR of 3.28% between 2026 and 2034‚ along…

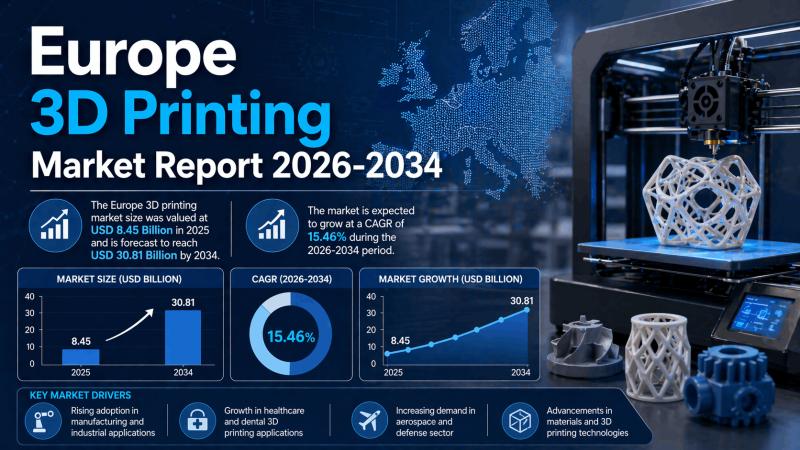

Europe 3D Printing Market Surge: USD 8.45 Billion Industry Expanding at 15.46% C …

The European 3D printing market is at an inflection point as it evolves from an emerging technology to one that is becoming a standard part of the manufacturing value chain. The European market is forecast to grow from USD 8.45 billion in 2025 to USD 30.81 billion in 2034. This corresponds to an annualized growth of 15.46% for 2026-2034‚ faster than the growth of the wider European manufacturing sector which…

More Releases for Connector

Automotive Sector's Expansion Boosts Connector Market Prospects: Strategic Insig …

Use code ONLINE30 to get 30% off on global market reports and stay ahead of tariff changes, macro trends, and global economic shifts.

How Large Will the Connector Market Size By 2025?

The size of the connector market has seen significant growth in the past few years. It is projected to increase from a valuation of $86.07 billion in 2024 to about $90.87 billion in 2025, marking a compound annual growth rate…

Global Micro-D Connector Market is Thriving Worldwide with ITT Cannon, Bel Fuse …

The global Micro-D Connector Market size reached 256.21 USD Million in 2024. Looking forward, marketsglob expects the market to reach 391.17 USD Million by 2031, exhibiting a growth rate (CAGR) of 6.14% during 2025-2031.

The global market research report for Micro-D Connector presents a thorough examination of the market environment. This includes a detailed evaluation of prominent industry leaders, pricing patterns, as well as the broader factors influencing the market, both…

Liquid Cooling Connector Quick Connector for RDHx Research:CAGR of 12.7% during …

QY Research Inc. (Global Market Report Research Publisher) announces the release of 2025 latest report "Liquid Cooling Connector Quick Connector for RDHx- Global Market Share and Ranking, Overall Sales and Demand Forecast 2025-2031". Based on current situation and impact historical analysis (2020-2024) and forecast calculations (2025-2031), this report provides a comprehensive analysis of the global Wire Drawing Dies market, including market size, share, demand, industry development status, and forecasts for…

Glass Sealed Connector Market

Glass Sealed Connector Market Overview

Glass-to-metal sealed connector (GTMS connector) is a high-performance electrical connector that uses sealing technology between glass and metal to achieve electrical insulation and airtightness while ensuring reliable connection in extreme environments.

This report provides a deep insight into the global Glass Sealed Connector market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape,…

Loadbreak Connector: Power Up with ANHUANG's 24kV 400A Loadbreak Separarable Con …

Today, we are exploring the realm of load break connectors, especially the remarkable 24kV 400A load break separable connector from ANHUONG. You'll have fun if you've ever wondered how underground cables link to our critical distribution power networks. Let's dissect it understandably together.

Image: https://c861.goodao.net/uploads/%E5%9B%BE%E7%89%8722.png

Loadbreak Connector [https://www.ahelek.com/400a-24kv-loadbreak-separable-connector-product/] Description

Let's begin with the fundamentals. In electrical engineering, a load break connector is an essential component. Consider it as the superhero tying underground lines…

Automotive and Transportation Connector Market Report 2018: Segmentation by Prod …

Global Automotive and Transportation Connector market research report provides company profile for JAE, KET, JST, Rosenberger, LUXSHARE, AVIC Jonhon, TE Connectivity, Yazaki, Delphi Automotive, Amphenol, Molex, Sumitomo and Others.

This market study includes data about consumer perspective, comprehensive analysis, statistics, market share, company performances (Stocks), historical analysis 2012 to 2017, market forecast 2018 to 2025 in terms of volume, revenue, YOY growth rate, and CAGR for the year 2018 to…