Press release

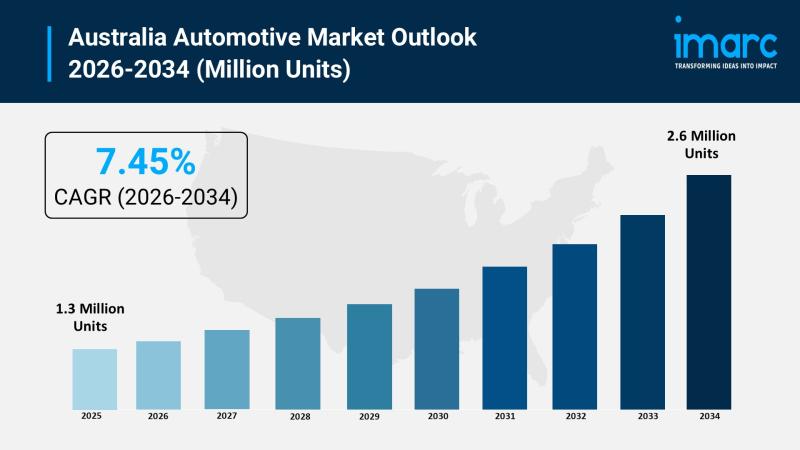

Australia Automotive Market Anticipated to Hit 2.6 Million Units During 2026-2034

The Australia automotive market size reached 1.3 Million Units in 2025. Looking forward, the market is expected to reach 2.6 Million Units by 2034, exhibiting a growth rate (CAGR) of 7.45% during 2026-2034. Australia represents one of the most dynamic automotive markets in the Asia-Pacific region, driven by robust consumer demand for passenger and commercial vehicles, accelerating electric vehicle adoption, and a highly competitive multi-brand landscape. The convergence of government emissions regulations, expanding EV infrastructure, rising demand for SUVs and light commercial vehicles, and growing influence of Chinese automakers is reshaping the competitive dynamics and creating significant opportunities for innovation across all vehicle segments and drivetrain technologies.

Request for a sample report PDF: https://www.imarcgroup.com/australia-automotive-market/requestsample

Australia Automotive Market Summary:

• Australia's automotive market continues to benefit from strong consumer demand across both passenger and commercial vehicle segments, with SUVs accounting for approximately 60.7% of total new vehicle sales, reflecting deep consumer preference for versatile, family-oriented, and off-road capable vehicles suited to the country's diverse geography and lifestyle needs.

• Electric vehicle adoption is accelerating rapidly, with EV sales reaching approximately 157,000 units representing 13.1% of the total market, driven by expanding model availability from both established automakers and new Chinese entrants, growing charging infrastructure, and increasing consumer awareness of environmental benefits and total cost of ownership advantages.

• Toyota maintains market leadership with approximately 19.8% market share and 239,863 units sold, followed by Ford, Mazda, Kia, and Hyundai, while Chinese brands including BYD, MG/SAIC, and GWM are rapidly gaining ground through competitively priced electric and hybrid offerings that challenge the traditional dominance of Japanese and Korean manufacturers.

• The Australian government's New Vehicle Efficiency Standard (NVES), effective January 2025, is creating regulatory momentum for cleaner vehicles by establishing CO2 emission targets for new vehicle sales, incentivizing manufacturers to accelerate the introduction of electric, hybrid, and more fuel-efficient models across their Australian product portfolios.

• BYD has emerged as the leading electric vehicle brand in Australia with 35.8% EV market share, demonstrating the transformative impact of affordable, feature-rich Chinese EVs on a market historically dominated by Japanese, Korean, and European manufacturers, and signaling a structural shift in competitive dynamics.

• Plug-in hybrid electric vehicles doubled to 53,484 units, indicating growing consumer acceptance of electrified drivetrains as a transitional technology, particularly among buyers who seek the environmental benefits of electric driving combined with the range flexibility of conventional combustion engines for longer journeys.

• The competitive landscape features over 60 brands spanning Japanese leaders, Korean challengers, European premium marques, and fast-growing Chinese entrants, creating a highly fragmented and innovation-driven marketplace that benefits consumers through diverse product choices, competitive pricing, and continuous technological advancement.

• Market segmentation covers two vehicle types (passenger, commercial vehicles), three applications (personal use, municipal use, business use), and five regional markets across Australia.

Key Trends Shaping the Australia Automotive Market:

• Rapid electric vehicle mainstreaming and charging infrastructure expansion: Australia is experiencing a significant acceleration in electric vehicle adoption as expanding public and private charging networks, growing model availability across all price segments, and increasing consumer familiarity with EV technology combine to move electric vehicles from niche early-adopter status toward mainstream consumer acceptance. The growing presence of affordable Chinese EVs alongside established premium electric offerings from Tesla, BMW, and Mercedes-Benz is creating a comprehensive EV product landscape that addresses diverse consumer budgets and use cases.

• Chinese automaker disruption and market share gains: Chinese automotive brands are fundamentally reshaping Australia's competitive landscape by offering feature-rich, competitively priced vehicles-particularly in the electric and hybrid segments-that challenge the decades-long dominance of Japanese and Korean manufacturers. BYD, MG/SAIC, GWM, and Geely are expanding dealership networks, launching new models, and building brand awareness at an unprecedented pace, forcing established players to accelerate their own electrification strategies and pricing competitiveness.

• SUV dominance and light commercial vehicle strength: The Australian automotive market continues to be characterized by overwhelming consumer preference for SUVs and light commercial vehicles, reflecting the country's unique combination of urban lifestyles, rural distances, and outdoor recreation culture. This structural demand pattern drives product development priorities for all manufacturers operating in Australia and creates opportunities for brands that can deliver versatile, durable, and technology-rich vehicles suited to both city commuting and off-road adventure applications.

• Government emissions regulation and NVES implementation: The introduction of Australia's New Vehicle Efficiency Standard is establishing a regulatory framework that progressively tightens CO2 emission limits for new vehicle sales, creating a structural incentive for manufacturers to expand their electric and hybrid vehicle offerings while improving the efficiency of remaining internal combustion models. This policy framework is accelerating the automotive industry's transition toward cleaner drivetrains and aligning Australia with global automotive decarbonization trends.

• Autonomous and connected vehicle technology integration: Advanced driver assistance systems, connected vehicle features, and early autonomous vehicle applications are becoming increasingly prominent in the Australian automotive market, with manufacturers differentiating through technology offerings that enhance safety, convenience, and driving experience. Applied EV's development of autonomous electric vehicles for municipal applications such as street sweeping and garbage collection represents the emerging commercial potential of autonomous technology beyond passenger vehicles.

Market Growth Drivers:

Accelerating Electric Vehicle Adoption and Expanding Model Availability

The rapid expansion of electric vehicle availability across all price points and vehicle segments is a primary driver of automotive market growth in Australia. The entry of competitively priced Chinese EVs from BYD, MG/SAIC, GWM, and Geely alongside established offerings from Tesla, BMW, Mercedes-Benz, and Hyundai has created a comprehensive electric vehicle marketplace that addresses diverse consumer needs from affordable city commuters to premium luxury SUVs. Growing public and workplace charging infrastructure, state-level EV incentive programs, and declining battery costs are reducing adoption barriers, while the Australian government's New Vehicle Efficiency Standard creates regulatory push for manufacturers to expand their electrified product portfolios-collectively driving incremental vehicle sales volume and market value growth.

Strong Consumer Demand for SUVs and Light Commercial Vehicles

Australia's unique geographic and lifestyle characteristics continue to drive sustained demand for SUVs and light commercial vehicles, with SUVs accounting for approximately 60.7% of all new vehicle sales. The country's vast rural distances, extensive highway network, and deeply embedded outdoor recreation culture create structural demand for versatile, capable vehicles that can serve both urban commuting and regional travel needs. Ute and pickup truck models remain essential for Australia's mining, agriculture, and construction industries, while lifestyle-oriented SUVs appeal to families and adventure-seeking consumers. This broad-based demand across both passenger and commercial segments provides a resilient foundation for market growth that transcends economic cycles and supports sustained investment from manufacturers seeking to capture share in Australia's vehicle-dependent economy.

Intensifying Multi-Brand Competition and New Market Entrants

The rapid influx of Chinese automotive brands into the Australian market is intensifying competition and driving innovation across all vehicle categories. With over 60 brands competing for consumer attention, the Australian automotive market is experiencing unprecedented product diversity, competitive pricing pressure, and accelerated technology adoption as established Japanese, Korean, and European manufacturers respond to the challenge posed by feature-rich, affordably priced Chinese vehicles. This competitive intensity benefits consumers through greater choice, more aggressive pricing, and faster adoption of advanced safety, connectivity, and electrification technologies-while expanding overall market volume as new brands attract previously unserved customer segments and stimulate replacement demand through compelling new product offerings.

Browse the full report with TOC and list of figures: https://www.imarcgroup.com/australia-automotive-market

Porter's Five Forces Analysis - Australia Automotive Market

The Australia automotive market, valued at 1.3 Million Units in 2025 and projected to reach 2.6 Million Units by 2034 (CAGR 7.45%), reflects a structurally dynamic and innovation-driven industry environment.

Bargaining Power of Suppliers - Moderate

• Australia sources vehicles primarily from Japan, China, Thailand, South Korea, and Germany; this diversified import base limits supplier concentration and reduces the leverage of any single manufacturing country over the Australian market.

• In February 2026, Chinese vehicles surpassed Japanese imports for the first time in 28 years in a single month, demonstrating shifting supply dynamics and the growing diversification of Australia's vehicle sourcing landscape.

• Australia's critical mineral reserves including lithium, nickel, and cobalt position it favorably for domestic EV battery supply chain development, potentially reducing future dependence on imported battery components.

Bargaining Power of Buyers - Moderate to High

• Consumers benefit from over 60 brands competing across passenger and commercial segments, providing extensive choice across price points, vehicle types, and drivetrain technologies that strengthen buyer negotiating position.

• Toyota leads with approximately 19.8% market share (239,863 units in 2025), followed by Ford, Mazda, Kia, and Hyundai, but no single brand dominates decisively, giving buyers significant flexibility in brand selection.

• Price-sensitive buyers are driving demand for affordable Chinese EVs, with BYD growing 180.1%, increasing competitive pressure on legacy brands and compelling industry-wide pricing discipline that benefits consumers.

Threat of New Entrants - Moderate to High

• Chinese brands including BYD, GWM, MG/SAIC, and Geely are entering the Australian market aggressively with affordable EVs; BYD has already secured 35.8% EV market share, demonstrating rapid consumer acceptance of new entrants.

• Geely Auto committed to establishing new dealerships across Australia and launching the EX5 EV in early 2025, illustrating the continued pipeline of new market participants investing in Australian distribution infrastructure.

• Low import tariffs and the absence of local manufacturing barriers facilitate new market entry, enabling international brands to access Australian consumers with relatively low regulatory and logistical hurdles.

Threat of Substitutes - Low to Moderate

• Strong public transport networks in Melbourne and Sydney provide alternatives for urban commuters, but vast rural distances across Australia make personal vehicles essential for the majority of the population outside major metropolitan centers.

• Ride-sharing services including Uber and DiDi, along with emerging subscription models, offer partial substitution in urban areas, though these remain complementary to rather than replacements for personal vehicle ownership for most Australian households.

• SUVs dominate at 60.7% of total sales, reflecting deep consumer preference for personal vehicles that serve multiple lifestyle functions including family transport, recreation, and work-limiting the practical threat of substitution.

Competitive Rivalry - High (Healthy)

• Multi-tier competition spans Japanese leaders (Toyota 19.8%, Mazda 7.6%), Korean challengers (Kia, Hyundai), European premium brands (BMW, Mercedes, Porsche), and fast-growing Chinese entrants (BYD, MG, GWM), creating a vibrant and innovation-driven competitive landscape.

• Plug-in hybrids doubled to 53,484 units in 2025, intensifying drivetrain competition as manufacturers compete to offer the most compelling electrification solutions across conventional, hybrid, and fully electric powertrains.

• The government's New Vehicle Efficiency Standard (NVES), effective January 2025, creates regulatory push for cleaner vehicles across all brands, leveling the competitive playing field and rewarding manufacturers that invest in low-emission technology.

Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Australia automotive market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on type, application, and region.

By Type:

• Passenger

• Commercial Vehicles

By Application:

• Personal Use

• Municipal Use

• Business Use

By Region:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Key Players:

The Australia automotive market features a competitive landscape comprising global automotive manufacturers, established regional leaders, and fast-growing new entrants. The market research report provides a comprehensive analysis of the competitive landscape including key player positioning, market structure, top winning strategies, competitive dashboards, and detailed company profiles. Some of the major players include Toyota, Ford, Mazda, Kia, Hyundai, BYD, MG/SAIC, Nissan, Volkswagen, BMW, Mercedes-Benz, Tesla, Mitsubishi, Subaru, and other domestic and international participants competing across passenger, commercial, electric, and hybrid vehicle segments throughout Australia.

Key Aspects Required for the Australia Automotive Market:

• Australia's New Vehicle Efficiency Standard (NVES) requires manufacturers to meet progressively tightening CO2 emission targets for new vehicle sales, creating a regulatory framework that shapes product portfolio decisions and incentivizes the introduction of electric, hybrid, and more fuel-efficient vehicles across all brands operating in the Australian market.

• Vehicle safety standards governed by the Australian Design Rules (ADRs) mandate compliance with crashworthiness, electronic stability control, autonomous emergency braking, and other safety technology requirements that ensure all vehicles sold in Australia meet stringent safety benchmarks valued by Australian consumers.

• Charging infrastructure availability and reliability are becoming critical market requirements as electric vehicle adoption accelerates, with manufacturers increasingly partnering with charging network operators and investing in proprietary charging solutions to address range anxiety concerns and support consumer confidence in EV ownership.

• Comprehensive dealership networks and after-sales service capabilities remain essential competitive requirements, with both established brands and new Chinese entrants investing heavily in physical retail presence, service centers, and parts availability to build consumer trust and support long-term brand loyalty in the Australian market.

• Connected vehicle technology, over-the-air software updates, and advanced driver assistance systems are becoming baseline consumer expectations across all price segments, requiring manufacturers to invest in digital capabilities and technology partnerships to remain competitive in an increasingly technology-driven automotive marketplace.

• Competitive pricing strategies that balance feature content, technology integration, and value proposition are critical for success in a market where over 60 brands compete for consumer attention and where the rapid growth of affordable Chinese vehicles is resetting consumer expectations regarding price-to-feature ratios.

Recent News and Developments:

May 2026: Prime Minister Anthony Albanese backed plans to revive Australia's automotive manufacturing capabilities through electric vehicle and battery production initiatives, emphasizing local component manufacturing and supply-chain resilience. Industry discussions highlighted that manufacturing's share of Australia's GDP had declined from approximately 14% in 1990 to 5% in 2025, increasing pressure for automotive industry revitalization.

May 2026: Australia's EV market accelerated sharply as electric vehicles accounted for approximately 14.6% of all new vehicle sales, nearly doubling year-on-year growth. NRMA Insurance also reported a 121% increase in EV insurance quote requests, while second-hand EV sales rose approximately 126% in March 2026.

May 2026: Australia's federal budget expanded clean transport support through additional EV infrastructure and transport electrification measures, while policy discussions continued around future EV road-user charging frameworks and automotive transition funding.

May 2026: Electric trucking adoption gained momentum across Australia as companies including Woolworths, Coles, and Ikea expanded electric truck deployments. Industry data showed more than half of Australia's diesel truck fleet was approaching replacement age, creating significant opportunities for commercial vehicle modernization.

April 2026: Australia's automotive financing and EV ecosystem expanded rapidly as banks and vehicle platforms reported major increases in EV loan demand and vehicle enquiries amid rising fuel prices and broader EV model availability.

February 2026: Australia implemented stricter New Vehicle Efficiency Standards (NVES), reshaping automaker strategies and accelerating low-emission vehicle adoption. EVs represented approximately 12% of new vehicle sales entering 2026 under the new compliance environment.

January 2026: Industry reports highlighted growing Chinese automotive investment and expansion in Australia as brands including BYD strengthened direct distribution and retail operations nationwide. BYD officially assumed direct control of Australian operations in 2025 to accelerate local growth and dealership expansion.

December 2025: The Australian Government continued implementation of the National Electric Vehicle Strategy, including approximately AUD 60 million over four years to help automotive dealers and repairers expand EV servicing and repair capabilities nationwide.

September 2025: Australia expanded EV charging infrastructure to approximately 1,272 fast-charging locations with more than 3,436 charging plugs, representing around 20% year-on-year growth. The government also announced approximately AUD 40 million for additional kerbside and fast-charging infrastructure expansion.

July 2025: Australia's automotive market experienced rapid growth in affordable EV adoption as Chinese manufacturers expanded market share through competitively priced electric SUVs, sedans, and hybrid vehicles. Industry reports highlighted increasing competition across both passenger and commercial vehicle segments.

2025: Global EV sales exceeded approximately 17 million units during 2024, accounting for more than 20% of global new car sales, while Australia continued accelerating EV adoption supported by infrastructure investment, policy incentives, and growing model availability.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

Speak to an analyst for a customized sample report PDF: https://www.imarcgroup.com/request?type=report&id=22065&flag=C

Contact Us:

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Australia Automotive Market Anticipated to Hit 2.6 Million Units During 2026-2034 here

News-ID: 4519572 • Views: …

More Releases from IMARC Group

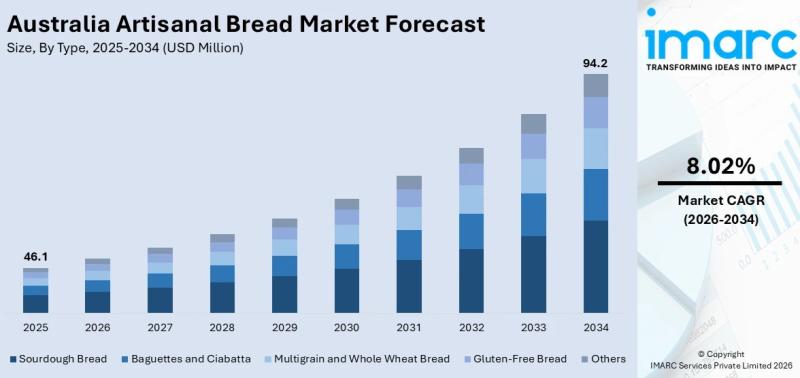

Australia Artisanal Bread Market is Expected to Reach US$ 94.2 Million by 2026-2 …

Australia Artisanal Bread Market Overview

According to IMARC Group's latest research report, the Australia artisanal bread market size reached USD 46.1 Million in 2025 and is projected to reach USD 94.2 Million by 2034, exhibiting a growth rate (CAGR) of 8.02% during 2026-2034. The market is driven by the broader Australian bakery products market valued at USD 8.2 billion providing a strong growth foundation, rising consumer preference for sourdough and naturally…

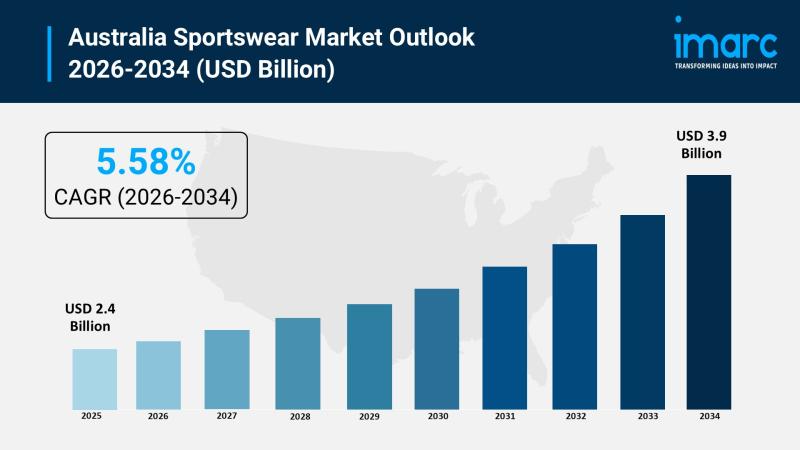

Australia Sportswear Market 2026 | Worth USD 3.9 Billion by 2034

Australia Sportswear Market Overview:

The Australia sportswear market size reached USD 2.4 Billion in 2025. Looking forward, the market is expected to reach USD 3.9 Billion by 2034, exhibiting a growth rate (CAGR) of 5.58% during 2026-2034. Australia represents one of the most vibrant sportswear markets in the Asia-Pacific region, driven by the country's deeply embedded fitness culture, growing athleisure adoption, and increasing consumer preference for performance-driven and sustainable activewear. The…

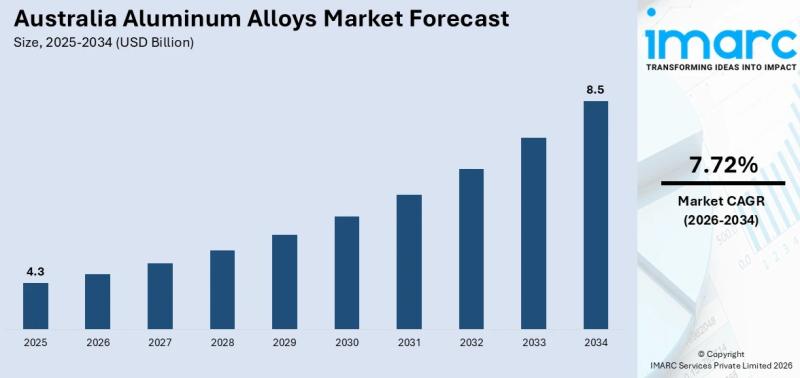

Australia Aluminum Alloys Market is Expected to Reach US$ 8.5 Billion by 2026-20 …

Australia Aluminum Alloys Market Overview

According to IMARC Group's latest research report, the Australia aluminum alloys market size reached USD 4.3 Billion in 2025 and is projected to reach USD 8.5 Billion by 2034, exhibiting a growth rate (CAGR) of 7.72% during 2026-2034. The market is driven by Australia's four operational aluminium smelters producing over 1.5 million tonnes annually, the government's AUD 1.2 billion Critical Minerals Strategic Reserve announced in the…

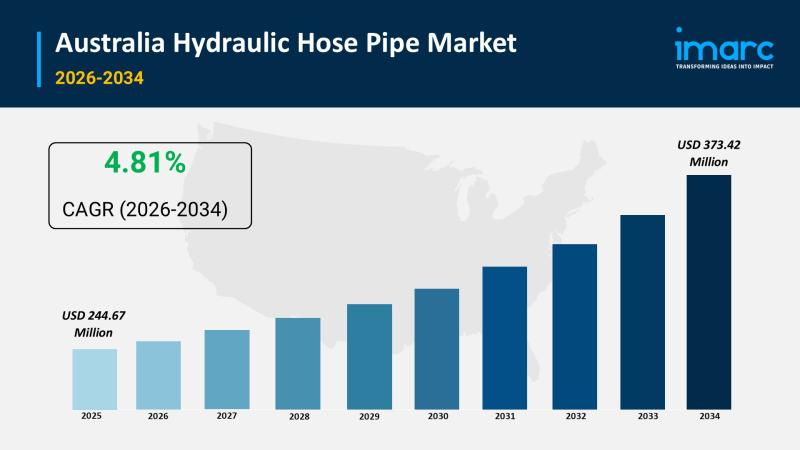

Australia Hydraulic Hose Pipe Market is Expected to Reach US$ 373.42 Million by …

Australia Hydraulic Hose Pipe Market Overview

According to IMARC Group's latest research report, the Australia hydraulic hose pipe market size reached USD 244.67 Million in 2025 and is projected to reach USD 373.42 Million by 2034, growing at a CAGR of 4.81% during 2026-2034. The market is driven by Australia's robust mining sector generating sustained demand for high-pressure hydraulic hoses across excavators, dump trucks, and drilling equipment, the construction machinery market…

More Releases for Australia

Derila Memory foam pillow Australia: Honest Reviews About Derila Australia

Derila is one of the best memory foam pillows sold in Australia today.

Priced at around 30 dollars (USD), derila is currently the most reviewed and the cheapest memory pillow available in Australia.

What is Derila? Is Derila Pillow the best in Australia? Keep reading to discover everything worth knowing about Derila Australia.

OVERVIEW

Recently, Memory foam pillow has been trending and there is a lot of brands to choose from. Which one is…

CeraCare Australia - Where to Buy Legit CeraCare Supplement in Australia?

CeraCare Australia - Ceracare is a glucose support supplement that proposes to augment cardiovascular prosperity and to stay aware of perfect glucose assimilation in Australia. CeraCare supplement is conceptualized and executed by a threesome – Christine, Dr. Jihn and Michael. It is a natural supplement that helps one stay aware of ideal glucose levels, cardiovascular prosperity, and glucose assimilation.

Take Advantage of 80% Discount Offer in Australia >> https://boostsxproaustralia.com/ceracare-new

The indications…

Glucofort Australia - Where to Buy Legit Glucofort Supplement in Australia?

Glucofort Australia - Glucofort is an efficient, all-natural progressive glucose support supplement in Australia. This formula is made out of 12 key ingredients, 7 nutrients, and minerals, and a little of Vanadium. This supplement upholds regulated glucose levels and glucose digestion. Glucofort prides itself as the most inventive supplements available in Oceania, accentuating its solidarity, wellbeing, and quality.

Take Advantage of 75% Discount Offer in Australia >> https://boostsxproaustralia.com/glucofort-new

Rather than simply…

Australia Agriculture Market, Australia Agriculture Industry, Australia Agricult …

Australia Agriculture has been as vital within the development of Australia, because it was within the United States. Australia's ancient dominance in wheat and sheep continues into the 21st century. Recently Australian agriculture has become more and more diversified. The considerable expanses of productive land have helped Australia to become a number one world exporter of grains, meats, and wool. Each grains (predominantly wheat and barley) and wool markets round…

Australia Conveyor Maintenance Analysis by Top Companies Habasit Australia Pty l …

Global Australia Conveyor Maintenance Market and Competitive Analysis

Know your current market situation! Not only a vital element for brand new products but also for current products given the ever-changing market dynamics. The study allows marketers to remain involved with current consumer trends and segments where they'll face a rapid market share drop. Discover who you actually compete against within the marketplace, with Market Share Analysis know market position, to push…

Australia Conveyor Maintenance Market Analysis By Manufacturers Rema Tip Top Aus …

A conveyor system is a common piece of mechanical handling device that moves materials/objects from one location. A conveyor is often lifeline to a company’s ability to effectively move its products in a timely manner. While it is used constantly in a manufacturing plant, proper maintenance from trained technicians can extend the lifespan of conveyor. Furthermore, conveyor maintenance is essential as it may be subjected to different types of failures…