Press release

Australia Aluminum Alloys Market is Expected to Reach US$ 8.5 Billion by 2026-2034

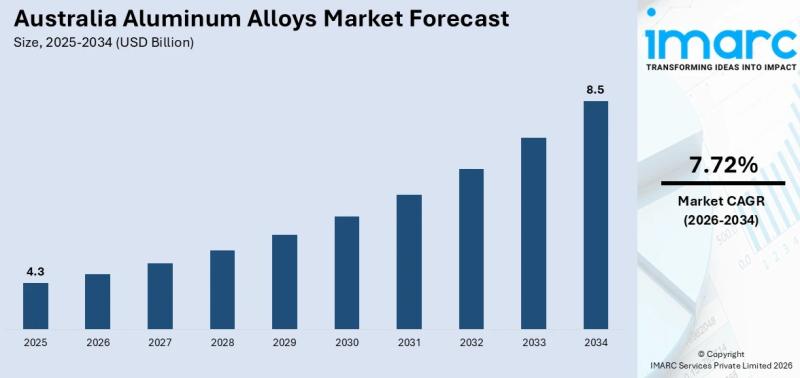

According to IMARC Group's latest research report, the Australia aluminum alloys market size reached USD 4.3 Billion in 2025 and is projected to reach USD 8.5 Billion by 2034, exhibiting a growth rate (CAGR) of 7.72% during 2026-2034. The market is driven by Australia's four operational aluminium smelters producing over 1.5 million tonnes annually, the government's AUD 1.2 billion Critical Minerals Strategic Reserve announced in the 2025-26 federal budget, the USD 4 billion Critical Minerals Facility financing strategic projects through Export Finance Australia, growing demand for lightweight alloys in electric vehicle battery housings and structural components, and expanding construction and infrastructure investment requiring high-performance aluminium products.

Get a sample copy of this report: https://www.imarcgroup.com/australia-aluminum-alloys-market/requestsample

Australia Aluminum Alloys Market Summary

• Australia operates four major aluminium smelters that form the backbone of domestic alloy supply. Tomago Aluminium in New South Wales is the country's largest single smelter with a nameplate capacity of 435,000 tonnes per year. Portland Aluminium in Victoria, a joint venture between Alcoa (55%), CITIC (22.5%), and Marubeni (22.5%), produces approximately 345,000 tonnes annually. Boyne Island in Queensland and Bell Bay in Tasmania complement the national smelting capacity, collectively positioning Australia among the world's top ten primary aluminium producers.

• The Australian Government allocated AUD 1.2 billion to establish a Critical Minerals Strategic Reserve in the 2025-26 federal budget, with the reserve becoming operational from the second half of 2026. This initiative, alongside the USD 4 billion Critical Minerals Facility administered through Export Finance Australia, underscores the strategic importance of aluminium and its alloys within the national economic framework, providing financing for projects aligned with Australia's Critical Minerals Strategy.

• The signing of the United States-Australia Framework for Securing Supply in the Mining and Processing of Critical Minerals and Rare Earths in October 2025 marked a significant milestone for the aluminium alloys market. This bilateral agreement strengthens international supply chain alignment, opening new export pathways for Australian aluminium alloy products while attracting foreign investment into domestic processing capabilities.

• Electric vehicle adoption is reshaping aluminium alloy demand specifications, with increasing requirements for high-strength, lightweight alloys suitable for battery housings, structural crash components, and thermal management systems. The automotive sector's transition toward electrification demands alloy formulations that balance strength-to-weight ratios with corrosion resistance and formability, driving innovation across 5000, 6000, and 7000 series aluminium alloys.

• Recycled aluminium requires 95% less energy than primary production, making secondary aluminium processing an increasingly attractive pathway for Australian manufacturers facing rising energy costs and decarbonization mandates. The circular economy approach to aluminium is gaining momentum, with recycling operations expanding to meet growing demand for low-carbon aluminium alloy products across construction, automotive, and packaging sectors.

• Advances in aluminium alloy technology are opening new applications in high-performance sectors. Scandium additions of 0.1-0.6% by weight produce measurable improvements in tensile strength of 15-30% compared to conventional aluminium formulations, enabling applications in aerospace, defence, and advanced manufacturing where traditional aluminium alloys fall short of performance requirements.

• The Australian Government's AUD 15 billion National Reconstruction Fund targets investments in priority areas including renewables, advanced manufacturing, and defence capabilities, all of which rely heavily on aluminium alloy components. Defence sector modernization under the AUKUS partnership is generating specialized demand for high-strength aerospace-grade alloys used in naval vessel construction, military vehicle platforms, and aviation components.

• Building and construction represents the largest end-use segment, with aluminium alloys used extensively in window frames, curtain walls, roofing, structural cladding, and architectural applications across Australia's residential and commercial construction sectors. Major infrastructure projects including rail, road, bridge, and renewable energy installations generate additional demand for structural aluminium alloy products designed for long service life and corrosion resistance in Australian environmental conditions.

Key Trends Shaping the Australia Aluminum Alloys Market

• Low-carbon aluminium production is emerging as a major competitive differentiator in the Australian market, with smelters and alloy producers investing in renewable energy-powered operations to meet growing buyer demand for green aluminium. The global aluminium industry accounts for approximately 2% of worldwide CO2 emissions, and Australian producers are leveraging the country's abundant renewable energy resources to produce aluminium with a substantially lower carbon footprint, commanding premium pricing from sustainability-conscious buyers in automotive, construction, and packaging sectors.

• High-strength 7000-series aluminium alloys are seeing accelerated adoption in Australian aerospace and defence applications, driven by AUKUS partnership defence modernization programs and the country's growing space industry. These zinc-alloyed formulations deliver tensile strengths approaching 600 MPa, making them suitable for aircraft structural components, naval vessel fittings, and satellite launch infrastructure where weight reduction without strength compromise is essential.

• Aluminium-lithium alloys and scandium-enhanced formulations represent the premium growth frontier, with Australian rare earth and critical mineral producers positioning to supply specialty alloying elements domestically. Scandium additions of just 0.1-0.6% by weight improve tensile strength by 15-30% and enhance weldability, creating next-generation alloys for aerospace, high-performance automotive, and 3D printing applications that command significant price premiums.

• Additive manufacturing using aluminium alloy powders is gaining traction in Australian defence, aerospace, and medical device sectors, with 3D-printed aluminium components enabling complex geometries, reduced material waste, and rapid prototyping. This trend is driving demand for specialized atomized aluminium alloy powders with tightly controlled particle size distributions and alloy chemistry optimized for laser and electron beam melting processes.

• Closed-loop aluminium recycling partnerships between alloy producers, fabricators, and end-users are expanding across Australia as companies pursue circular economy objectives and carbon reduction targets. These partnerships ensure manufacturing and end-of-life aluminium products are recovered, re-melted, and reprocessed into specification-grade alloys, reducing dependence on primary aluminium and lowering the embodied carbon of finished products.

Porter's Five Forces Analysis - Australia Aluminum Alloys Market

The Australia aluminum alloys market, valued at USD 4.3 Billion in 2025 and projected to reach USD 8.5 Billion by 2034 (CAGR 7.72%), reflects a structurally significant, resource-rich industry environment with strong government backing and diversified end-use demand.

Bargaining Power of Suppliers - Moderate

• Australia is one of the world's largest bauxite miners and alumina producers, with Rio Tinto operating integrated bauxite-alumina-aluminium operations including the Yarwun Alumina Refinery (Gladstone) and multiple smelters, ensuring domestic supply chain stability for alloy feedstock.

• The presence of four operational smelters - Tomago (435,000 t/yr), Portland (345,000 t/yr), Boyne Island, and Bell Bay - provides multiple domestic sourcing options for alloy producers and fabricators.

• Global commodity pricing for primary aluminium on the London Metal Exchange introduces supply-side volatility, but long-term offtake agreements between smelters and industrial buyers moderate the impact on alloy pricing.

Bargaining Power of Buyers - Moderate to High

• Major construction, automotive, and defence buyers command significant purchasing volumes, with government-backed programs - the AUD 15 billion National Reconstruction Fund and AUKUS defence modernization - creating large-scale procurement that strengthens buyer negotiating positions.

• Growing availability of recycled aluminium alloys (requiring 95% less energy than primary production) gives buyers alternative supply options at competitive pricing while meeting decarbonization procurement mandates.

• The diversity of alloy series (1000 through 7000) and multiple domestic and international suppliers ensures competitive pricing dynamics, with buyers able to switch between suppliers for standard alloy specifications.

Threat of New Entrants - Low to Moderate

• Primary aluminium smelting requires massive capital investment and access to reliable, affordable electricity - Australia's four smelters collectively consume approximately 10% of the national electricity grid - creating substantial entry barriers for new primary producers.

• However, secondary (recycled) aluminium alloy production presents lower entry barriers, with the circular economy push and government incentives through the AUD 1.2 billion Critical Minerals Strategic Reserve encouraging new processing and value-adding investments.

• The USD 4 billion Critical Minerals Facility through Export Finance Australia is specifically designed to finance new and expanding projects, supporting strategic new entrants in downstream alloy processing and specialty manufacturing.

Threat of Substitutes - Low

• Aluminium alloys offer an unmatched combination of strength-to-weight ratio, corrosion resistance, recyclability, and formability that competing materials like steel, magnesium, or composites cannot replicate across such a broad range of applications.

• In lightweight automotive and aerospace applications, carbon fiber composites serve as partial substitutes but at 5-10x the cost of aluminium alloys, limiting substitution to ultra-premium applications where cost is secondary to performance.

• The growing electric vehicle market specifically favors aluminium alloys for battery enclosures and structural components due to their thermal conductivity, electromagnetic shielding properties, and crashworthiness - attributes not easily replicated by substitute materials.

Competitive Rivalry - Moderate to High (Healthy)

• Competition spans global integrated producers (Rio Tinto, Alcoa Corporation), specialty alloy manufacturers, and recycled aluminium processors - with Rio Tinto's record AUD 19.7 billion Australian supplier spend in 2025 illustrating the scale of industry activity.

• Differentiation centers on alloy performance specifications, low-carbon production credentials, recycled content, supply reliability, and technical support for end-use applications - driving innovation rather than commodity-style price erosion.

• The October 2025 US-Australia Critical Minerals Framework is intensifying strategic competition for value-added alloy processing investment, as producers position to capture growing demand from defence, EV, and clean energy supply chains.

Explore the full report with TOC & list of figures: https://www.imarcgroup.com/australia-aluminum-alloys-market

Market Growth Factors

Government Strategic Investment and Critical Minerals Policy

The Australian Government's comprehensive critical minerals policy framework is providing unprecedented support for the aluminium alloys sector. The AUD 1.2 billion Critical Minerals Strategic Reserve announced in the 2025-26 federal budget, operational from the second half of 2026, positions aluminium and its alloys as strategically important materials. The USD 4 billion Critical Minerals Facility through Export Finance Australia provides dedicated financing for projects aligned with Australia's Critical Minerals Strategy 2023-2030, while the AUD 15 billion National Reconstruction Fund targets priority investments in advanced manufacturing, renewables, and defence. The landmark United States-Australia Framework for Securing Supply in the Mining and Processing of Critical Minerals, signed in October 2025, opens new international partnership pathways. These combined government initiatives create a supportive investment environment for expanding domestic aluminium alloy processing, value-adding, and export capabilities.

Electric Vehicle and Lightweight Transportation Demand

The global automotive industry's accelerating transition toward electric vehicles is fundamentally reshaping aluminium alloy demand profiles. Battery enclosures, structural crash members, motor housings, and thermal management components all require high-strength, lightweight aluminium alloy formulations from the 5000, 6000, and 7000 series. Each electric vehicle uses approximately 30-40% more aluminium than a conventional internal combustion vehicle, creating a structural demand uplift as Australia's EV adoption rates climb. The National Electric Vehicle Strategy is accelerating this transition domestically, while Australian alloy producers are positioning to supply Asia-Pacific automotive manufacturing hubs. Recycled aluminium alloys are particularly favored by EV manufacturers seeking to minimize supply chain carbon footprints, as secondary aluminium requires 95% less energy than primary production, aligning with automotive OEM sustainability commitments and scope 3 emissions reduction targets.

Defence Modernization and Aerospace Applications

Australia's defence modernization program, anchored by the AUKUS trilateral security partnership, is generating sustained demand for high-performance aerospace-grade aluminium alloys. Naval vessel construction, military vehicle platforms, aviation components, and satellite launch infrastructure all require specialized alloy formulations delivering exceptional strength-to-weight ratios, fatigue resistance, and corrosion performance. The 7000-series zinc-alloyed formulations delivering tensile strengths approaching 600 MPa are increasingly specified for structural aircraft components and naval fittings. Australia's growing space industry further expands the addressable market for advanced aluminium alloys in launch vehicle structures and satellite components. The AUD 15 billion National Reconstruction Fund's defence priority area supports domestic manufacturing capability development, encouraging investment in alloy production facilities capable of meeting military specification requirements and supporting sovereign supply chain objectives.

Australia Aluminum Alloys Market Segmentation

IMARC Group provides an analysis of the key trends in each segment of the Australia aluminum alloys market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on alloy type, end use, and form.

By Alloy Type:

• 1000 Series Aluminum Alloy

• 2000 Series Aluminum Alloy

• 3000 Series Aluminum Alloy

• 5000 Series Aluminum Alloy

• 6000 Series Aluminum Alloy

• 7000 Series Aluminum Alloy

By End Use:

• Building and Construction

• Transportation

• Machinery and Equipment

• Consumer Durables

• Electrical

• Others

By Form:

• Flat Products (Sheets and Plates)

• Extrusions

• Castings

• Forgings

• Rod and Bar

• Others

By Region:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Key Players in the Australia Aluminum Alloys Market

The Australia aluminum alloys market is shaped by a competitive landscape comprising global integrated aluminium producers, specialty alloy manufacturers, and downstream fabricators with deep domestic presence. Rio Tinto, operating integrated bauxite-alumina-aluminium operations across Queensland, New South Wales, and Tasmania, is the largest player with smelting capacity across Boyne Island, Tomago, and Bell Bay facilities. Alcoa Corporation maintains a significant footprint through its 55% ownership of the Portland Aluminium smelter in Victoria (345,000 t/yr capacity) and alumina refining operations in Western Australia. Capral Aluminium, Australia's largest aluminium extrusion company, processes primary and recycled aluminium into extruded products for building, construction, and industrial applications. RYCO Metals and Ullrich Aluminium supply semi-finished alloy products to the fabrication and manufacturing sectors. Norsk Hydro, Aleris International (now part of Hindalco/Novelis), and Constellium SE supply specialty alloy products to Australian aerospace, automotive, and defence customers. The Australian Aluminium Council represents the industry's collective interests across policy, sustainability, and market development. Competition centers on alloy specification capabilities, low-carbon production credentials, recycled content, supply chain reliability, and technical support for demanding end-use applications.

Key Aspects Required for the Australia Aluminum Alloys Market Report

• Market Performance: An in-depth analysis of the Australia aluminum alloys market covering historical trends and current dynamics, with a focus on the USD 4.3 Billion valuation and projected growth trajectory reaching USD 8.5 Billion by 2034.

• Market Segmentation: Comprehensive breakdown across alloy types (1000 through 7000 series), end uses (building and construction, transportation, machinery and equipment, consumer durables, electrical), and forms (flat products, extrusions, castings, forgings, rod and bar).

• Regional Analysis: Detailed evaluation of aluminium alloy demand across ACT & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia, covering smelter locations, industrial concentration, and end-use sector distribution.

• Competitive Landscape: Profiling of major players including Rio Tinto, Alcoa, Capral Aluminium, and specialty alloy suppliers, covering production capacities, alloy portfolios, sustainability credentials, and downstream distribution strategies.

• Industry Trends and Drivers: Assessment of critical minerals policy support, electric vehicle lightweighting demand, defence modernization, low-carbon production, recycled aluminium growth, and advanced alloy innovation driving market expansion.

• Technology Analysis: Examination of 7000-series aerospace alloys, scandium-enhanced formulations, aluminium-lithium alloys, additive manufacturing powders, closed-loop recycling processes, and renewable energy-powered smelting technologies.

• Regulatory and Policy Analysis: Evaluation of the Critical Minerals Strategy 2023-2030, Critical Minerals Strategic Reserve, US-Australia supply framework, National Reconstruction Fund, carbon emission mandates, and trade policy impacts on market dynamics.

• Future Outlook: Forward-looking projections covering EV-driven alloy demand, defence procurement expansion, recycled aluminium growth, specialty alloy innovation, green aluminium premiums, and international supply chain partnerships.

Recent News and Developments

• 2026: Rio Tinto announced it will reduce production at the Yarwun Alumina Refinery in Gladstone by 40% from October 2026, lowering annual alumina output by approximately 1.2 million tonnes to extend the operation's life until 2035, while smelters continue at full capacity.

• 2025: The Australian Government allocated AUD 1.2 billion to establish a Critical Minerals Strategic Reserve in the 2025-26 federal budget, becoming operational from the second half of 2026 to strengthen domestic supply chains for strategic materials including aluminium.

• 2025: The United States-Australia Framework for Securing Supply in the Mining and Processing of Critical Minerals and Rare Earths was signed in October 2025, creating new bilateral investment and trade pathways for Australian aluminium alloy products.

• 2025: Rio Tinto spent a record AUD 19.7 billion with more than 6,000 Australian suppliers, representing a AUD 2 billion increase over the previous year, reflecting the scale of mining and aluminium industry procurement across the domestic supply chain.

• 2025: Rio Tinto approved a USD 1.8 billion investment to develop the Brockman Syncline 1 mine project in Western Australia's Pilbara, with first ore scheduled for 2027, supporting continued investment in the broader Australian minerals and metals value chain.

• 2025: The USD 4 billion Critical Minerals Facility through Export Finance Australia continued financing strategic projects aligned with Australia's Critical Minerals Strategy 2023-2030, supporting domestic aluminium value-adding and processing capabilities.

• 2025: Alcoa Corporation confirmed 2025 total Aluminum segment production guidance of 2.3-2.5 million metric tons globally, with Australian operations at Portland, Kwinana, and Pinjarra continuing as core production assets in the company's portfolio.

• 2025: The AUD 15 billion National Reconstruction Fund continued prioritizing investments in advanced manufacturing, renewables, and defence capabilities, all of which rely heavily on aluminium alloy components for structural and functional applications.

Ask an analyst for your customized sample: https://www.imarcgroup.com/request?type=report&id=35232&flag=C

Contact Us

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 611 7970

United States: +1-631-791-1145

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a great impact. The company provides a comprehensive suite of market entry and expansion services. IMARC's offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, and networking facilitation, among others.

The company has done projects in over 135 countries and has helped more than 2,500 clients across the globe. IMARC currently works from 11 offices across the world, including its headquarters in Noida, India. It has a team of over 600 people, including former industry executives, subject matter experts, and management professionals. IMARC is among the top 10 management consulting firms based in India.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Australia Aluminum Alloys Market is Expected to Reach US$ 8.5 Billion by 2026-2034 here

News-ID: 4519545 • Views: …

More Releases from IMARC Group

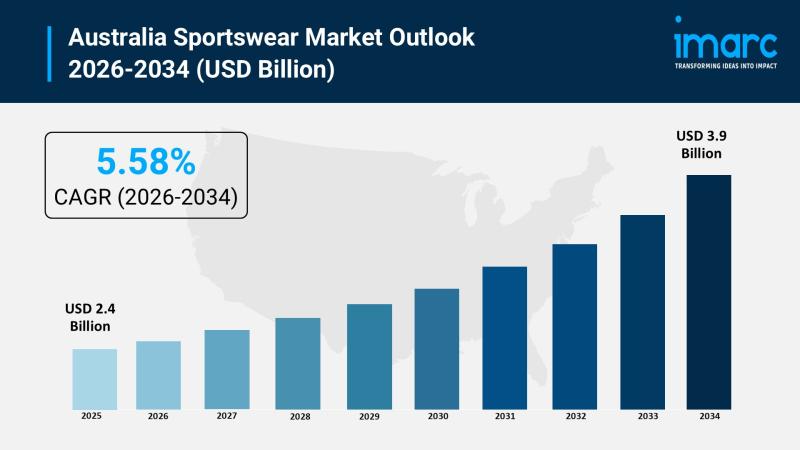

Australia Sportswear Market 2026 | Worth USD 3.9 Billion by 2034

Australia Sportswear Market Overview:

The Australia sportswear market size reached USD 2.4 Billion in 2025. Looking forward, the market is expected to reach USD 3.9 Billion by 2034, exhibiting a growth rate (CAGR) of 5.58% during 2026-2034. Australia represents one of the most vibrant sportswear markets in the Asia-Pacific region, driven by the country's deeply embedded fitness culture, growing athleisure adoption, and increasing consumer preference for performance-driven and sustainable activewear. The…

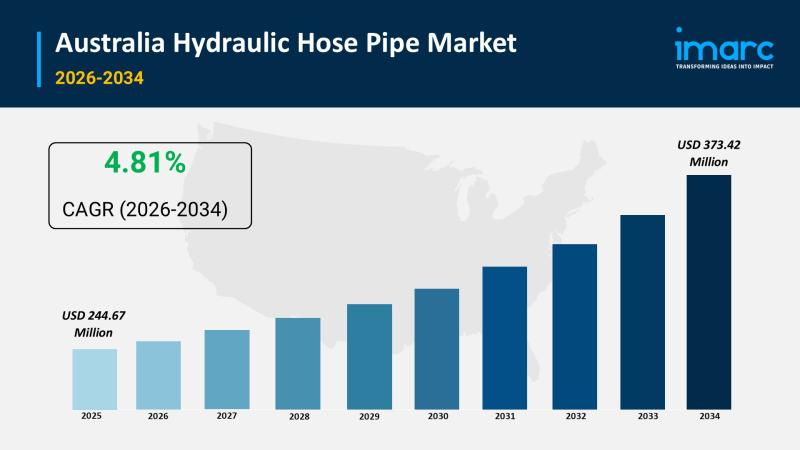

Australia Hydraulic Hose Pipe Market is Expected to Reach US$ 373.42 Million by …

Australia Hydraulic Hose Pipe Market Overview

According to IMARC Group's latest research report, the Australia hydraulic hose pipe market size reached USD 244.67 Million in 2025 and is projected to reach USD 373.42 Million by 2034, growing at a CAGR of 4.81% during 2026-2034. The market is driven by Australia's robust mining sector generating sustained demand for high-pressure hydraulic hoses across excavators, dump trucks, and drilling equipment, the construction machinery market…

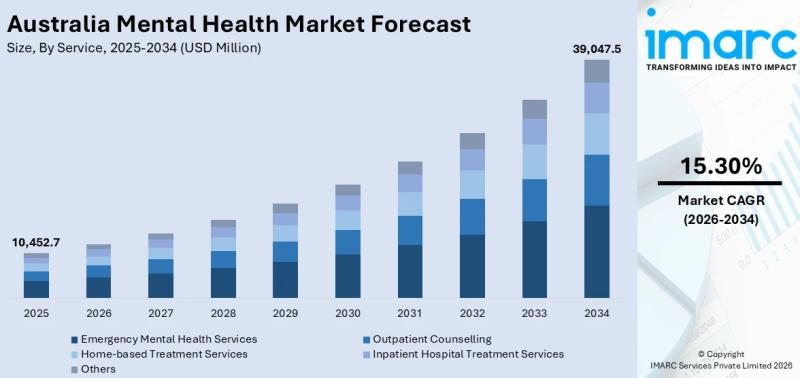

Australia Mental Health Market Projected to Reach USD 39,047.5 Million by 2034

Australia Mental Health Market Overview:

Australia's mental health market is experiencing rapid expansion, driven by rising awareness of psychological well-being, increasing prevalence of anxiety and depression, growing government investment in mental health infrastructure, and the permanent integration of telehealth into the national healthcare system. Mental health has become a national policy priority, with more than 2.7 million Australians utilizing nearly 13.2 million Medicare-subsidized mental health services annually - a figure that…

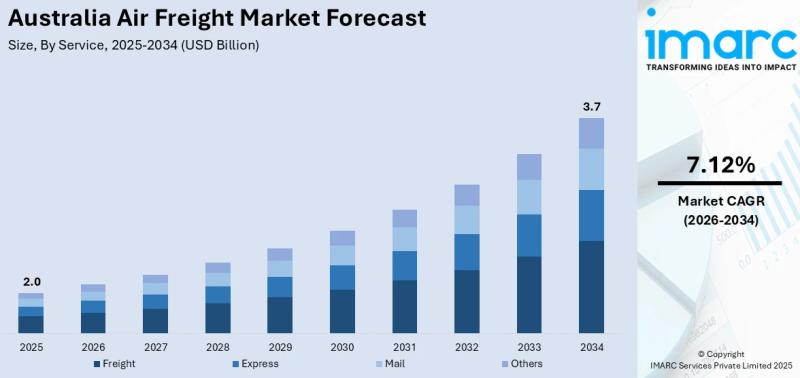

Australia Air Freight Market Projected to Reach USD 3.7 Billion by 2034

Australia Air Freight Market Overview:

Australia's air freight market is positioned for sustained expansion, driven by the country's geographic reliance on aviation for time-sensitive domestic and international logistics, booming e-commerce parcel volumes, and growing demand for temperature-controlled air transport of perishable exports and pharmaceuticals. As an island continent with major trading partners across Asia-Pacific, Europe, and North America, Australia depends heavily on airfreight to move premium goods including fresh seafood, premium…

More Releases for Australia

Derila Memory foam pillow Australia: Honest Reviews About Derila Australia

Derila is one of the best memory foam pillows sold in Australia today.

Priced at around 30 dollars (USD), derila is currently the most reviewed and the cheapest memory pillow available in Australia.

What is Derila? Is Derila Pillow the best in Australia? Keep reading to discover everything worth knowing about Derila Australia.

OVERVIEW

Recently, Memory foam pillow has been trending and there is a lot of brands to choose from. Which one is…

CeraCare Australia - Where to Buy Legit CeraCare Supplement in Australia?

CeraCare Australia - Ceracare is a glucose support supplement that proposes to augment cardiovascular prosperity and to stay aware of perfect glucose assimilation in Australia. CeraCare supplement is conceptualized and executed by a threesome – Christine, Dr. Jihn and Michael. It is a natural supplement that helps one stay aware of ideal glucose levels, cardiovascular prosperity, and glucose assimilation.

Take Advantage of 80% Discount Offer in Australia >> https://boostsxproaustralia.com/ceracare-new

The indications…

Glucofort Australia - Where to Buy Legit Glucofort Supplement in Australia?

Glucofort Australia - Glucofort is an efficient, all-natural progressive glucose support supplement in Australia. This formula is made out of 12 key ingredients, 7 nutrients, and minerals, and a little of Vanadium. This supplement upholds regulated glucose levels and glucose digestion. Glucofort prides itself as the most inventive supplements available in Oceania, accentuating its solidarity, wellbeing, and quality.

Take Advantage of 75% Discount Offer in Australia >> https://boostsxproaustralia.com/glucofort-new

Rather than simply…

Australia Agriculture Market, Australia Agriculture Industry, Australia Agricult …

Australia Agriculture has been as vital within the development of Australia, because it was within the United States. Australia's ancient dominance in wheat and sheep continues into the 21st century. Recently Australian agriculture has become more and more diversified. The considerable expanses of productive land have helped Australia to become a number one world exporter of grains, meats, and wool. Each grains (predominantly wheat and barley) and wool markets round…

Australia Conveyor Maintenance Analysis by Top Companies Habasit Australia Pty l …

Global Australia Conveyor Maintenance Market and Competitive Analysis

Know your current market situation! Not only a vital element for brand new products but also for current products given the ever-changing market dynamics. The study allows marketers to remain involved with current consumer trends and segments where they'll face a rapid market share drop. Discover who you actually compete against within the marketplace, with Market Share Analysis know market position, to push…

Australia Conveyor Maintenance Market Analysis By Manufacturers Rema Tip Top Aus …

A conveyor system is a common piece of mechanical handling device that moves materials/objects from one location. A conveyor is often lifeline to a company’s ability to effectively move its products in a timely manner. While it is used constantly in a manufacturing plant, proper maintenance from trained technicians can extend the lifespan of conveyor. Furthermore, conveyor maintenance is essential as it may be subjected to different types of failures…