Press release

Philippines Data Center Chip Market 2026 | Projected to Grow to USD 74.8 Million by 2034

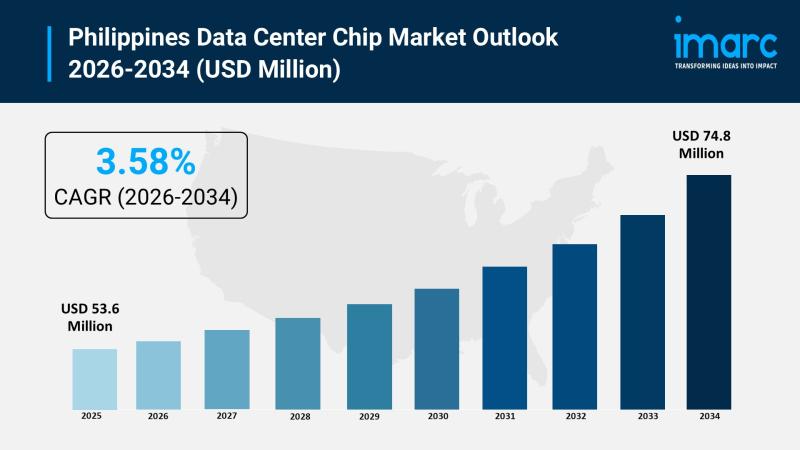

The Philippines data center chip market size reached USD 53.6 Million in 2025. Looking forward, the market is expected to reach USD 74.8 Million by 2034, exhibiting a growth rate (CAGR) of 3.58% during 2026-2034. The market encompasses GPUs, ASICs, FPGAs, CPUs, and other chip types deployed across small and medium size and large size data centers serving BFSI, manufacturing, government, IT and telecom, retail, transportation, energy and utilities, and other industry verticals across Luzon, Visayas, and Mindanao. The Philippines' rapidly expanding cloud adoption supported by the amended Public Service Act allowing full foreign ownership in telecommunications and data services, national data center capacity projected to triple from 150 MW to nearly 500 MW by 2028, the launch of the country's first AI-ready hyperscale data center VITRO Sta. Rosa with 50 MW capacity and NVIDIA GPU-as-a-Service offerings, Equinix's market entry through acquisition of three data center facilities for approximately USD 180 million, Alibaba Cloud opening its second Philippine data center in October 2025, and ENDECGROUP's USD 2.7 billion Narra Technology Park in New Clark City are among the key factors shaping the market throughout the forecast period.

Request for a sample report PDF: https://www.imarcgroup.com/philippines-data-center-chip-market/requestsample

Philippines Data Center Chip Market Summary:

• PLDT launched VITRO Sta. Rosa (VSR) in April 2025-the Philippines' first AI-ready hyperscale data center-offering 50 MW of IT capacity and the country's first GPU-as-a-Service (GPUaaS) powered by NVIDIA, allowing enterprises to access advanced AI computing capabilities without major capital expenditure, with plans to scale the facility to 500 MW and positioning the Philippines as a regional hub for AI-driven digital infrastructure.

• National data center capacity is on track to triple from approximately 150 MW to nearly 500 MW by 2028, driven by a pipeline of 13 upcoming facilities across eight cities-with the Department of Information and Communications Technology (DICT) projecting total capacity could reach 1.5 GW by 2028 as developer commitments and foreign investment in AI, cloud computing, and enterprise workload infrastructure accelerate across Luzon, Visayas, and Mindanao.

• Equinix entered the Philippine market in 2025 by opening three data center facilities in Cavite and Makati-acquired from Total Information Management (TIM) for approximately USD 180 million-providing about 35,000 square feet of colocation space and 1,000 data cabinets, with plans to expand capacity to meet rising demand from hyperscalers and multinational enterprises seeking carrier-neutral, globally connected data center infrastructure in Southeast Asia.

• STT GDC Philippines topped off STT Fairview 1 in December 2024-the first building of the country's largest carrier-neutral, AI-ready data center campus-scheduled for Phase 1 operations by Q2 2025 and contributing to a national portfolio exceeding 150 MW IT capacity across seven sites, all powered by 100% renewable energy, with the company also launching the Philippines' first Liquid Cooling Technology Showroom in May 2025 to demonstrate direct-to-chip cooling capable of removing up to 80% of server heat.

• The amended Public Service Act-allowing up to 100% foreign ownership in telecommunications and data center operations-has unlocked a wave of foreign direct investment, attracting global operators including Equinix, Digital Edge, ENDECGROUP, and Alibaba Cloud to establish or expand Philippine data center operations, with ENDECGROUP securing a 50-year lease for its USD 2.7 billion, 300 MW Narra Technology Park in New Clark City targeted for Q4 2026 operation.

• The Philippine semiconductor industry-valued at approximately USD 7.21 billion with integrated circuits holding 62.74% market share-provides a domestic manufacturing ecosystem for chip packaging, testing, and assembly, with Samsung Electro-Mechanics allocating PHP 50.65 billion to its Calamba plant for automotive multilayer capacitors and EMS Group securing USD 1.6 billion from foreign investors for automotive power IC manufacturing in Luzon, creating a supportive supply chain environment for data center chip procurement.

• Market segmentation covers five chip types (GPU, ASIC, FPGA, CPU, others), two data center sizes (small and medium size, large size), eight industry verticals (BFSI, manufacturing, government, IT and telecom, retail, transportation, energy and utilities, others), and three regions (Luzon, Visayas, Mindanao).

Key Trends Shaping the Philippines Data Center Chip Market:

• AI workload demand driving GPU and accelerator chip adoption in Philippine data centers: The surge in artificial intelligence and machine learning workloads across Philippine enterprises-from BPO operations deploying generative AI chatbots to financial institutions running real-time fraud detection models-is driving unprecedented demand for GPU and specialized accelerator chips in data center environments. PLDT's VITRO Sta. Rosa facility exemplifies this trend, deploying NVIDIA GPU servers and offering the Philippines' first GPU-as-a-Service (GPUaaS) platform that allows businesses to access AI computing power on-demand without procuring expensive hardware. With the Philippines' AI sector projected to reach USD 3.5 billion by 2030 and growing at roughly 29% annually, data center operators are increasingly designing facilities around high-density GPU racks that require advanced power delivery and cooling solutions. The shift from traditional CPU-centric data center architectures toward heterogeneous computing environments combining GPUs, FPGAs, and ASICs reflects a fundamental transformation in chip procurement patterns as Philippine data centers evolve from general-purpose hosting toward AI-optimized infrastructure.

• Hyperscaler market entry accelerating data center capacity and chip demand: Global hyperscalers and colocation providers are making substantial commitments to the Philippine data center market, each new facility representing millions of dollars in chip procurement for servers, networking equipment, and storage systems. Equinix's entry through a USD 180 million acquisition of three facilities, Alibaba Cloud's second data center opening in October 2025, ENDECGROUP's USD 2.7 billion Narra Technology Park, and STT GDC's expansion to over 150 MW across seven sites collectively represent a dramatic increase in installed chip capacity. These operators deploy the latest generation processors-including NVIDIA H100 and A100 GPUs, AMD EPYC server CPUs, custom ASICs for networking, and Intel Xeon Scalable processors for general-purpose workloads-creating sustained demand for high-performance data center chips. As national capacity triples toward 500 MW by 2028 and the DICT projects a potential 1.5 GW trajectory, the volume of chips required to equip these facilities with compute, networking, and storage hardware scales proportionally, positioning the Philippines as an increasingly significant chip consumption market in Southeast Asia.

• Liquid cooling adoption enabling higher-density chip deployments: The Philippines' tropical climate and the rising power density of modern data center chips-particularly GPUs drawing 700W or more per unit-are driving rapid adoption of advanced liquid cooling technologies that enable operators to deploy more powerful processors per rack without exceeding thermal limits. STT GDC Philippines' launch of the country's first Liquid Cooling Technology Showroom in May 2025, demonstrating direct-to-chip cooling that removes up to 80% of server heat, signals the industry's transition from air-cooled facilities toward liquid-cooled environments capable of supporting next-generation AI accelerators. This cooling evolution directly impacts chip procurement decisions: operators can deploy higher-TDP (thermal design power) processors like NVIDIA's latest GPU architectures and high-core-count server CPUs that deliver superior performance per watt, justifying the higher per-chip cost through improved computational efficiency and reduced overall facility cooling costs.

• Cloud adoption and digital transformation expanding enterprise chip consumption: The accelerating adoption of cloud computing, over-the-top (OTT) content services, and enterprise digital transformation across Philippine sectors including BFSI, e-commerce, healthcare, and education is driving broad-based demand for data center chips beyond AI-specific workloads. Traditional enterprise workloads-database management, virtualization, web hosting, content delivery, and business applications-continue to require large volumes of server CPUs, networking ASICs, and storage controllers as Philippine businesses migrate from on-premises infrastructure to colocation and cloud environments. The country's rising internet penetration, expanding 5G coverage, and growing digital economy create sustained demand for compute capacity that translates directly into chip procurement. With 28 operational colocation facilities and 13 upcoming developments across eight cities, each requiring thousands of server processors, networking chips, and storage controllers, the aggregate chip demand from non-AI enterprise workloads represents the market's foundational volume upon which AI-specific accelerator demand is layered.

• Regulatory liberalization and foreign investment unlocking next-generation infrastructure: The amendment of the Public Service Act allowing full foreign ownership in telecommunications and data center operations has fundamentally reshaped the Philippine data center landscape by enabling global operators to invest directly in building and operating facilities that deploy cutting-edge chip technologies. Before the amendment, foreign investment was capped at 40%, limiting the scale and sophistication of data center buildouts. The regulatory change has attracted operators like Equinix, Digital Edge, and ENDECGROUP who bring global procurement relationships with chip manufacturers, access to the latest hardware generations, and engineering expertise in deploying high-density computing environments. The government's complementary launch of the Semiconductor and Electronics Industry Advisory Council in April 2025-composed of public and private sector representatives tasked with strengthening the Philippines' position in the global semiconductor value chain-further supports the ecosystem by addressing domestic chip manufacturing, testing, and packaging capabilities that can serve data center operators' maintenance and replacement needs.

Market Growth Drivers:

Rapid Data Center Capacity Expansion and Hyperscaler Investment

The Philippines is experiencing an unprecedented wave of data center construction and expansion that directly drives demand for processors, accelerators, networking chips, and storage controllers. National data center capacity is projected to triple from approximately 150 MW to nearly 500 MW by 2028, with the DICT projecting a potential 1.5 GW trajectory driven by developer commitments across Metro Manila, Cavite, Laguna, and emerging zones like Clark and Quezon. Each megawatt of IT capacity deployed translates into thousands of server processors, GPUs, networking ASICs, and storage chips procured and installed. PLDT's VITRO Sta. Rosa campus alone offers 50 MW with plans to scale to 500 MW, while ENDECGROUP's USD 2.7 billion Narra Technology Park targets 300 MW. Equinix's three-facility entry, STT GDC's seven-site portfolio exceeding 150 MW, Alibaba Cloud's second data center, and Digital Edge's operations in Laguna collectively represent billions of pesos in chip procurement over the buildout period. The competitive intensity among operators drives continuous hardware refresh cycles as each provider seeks to attract hyperscaler and enterprise tenants with the latest-generation compute infrastructure, sustaining chip demand beyond initial facility buildout through ongoing technology upgrades and capacity expansions.

Enterprise Cloud Migration and Digital Transformation Across Key Sectors

The Philippines' accelerating digital transformation-spanning BFSI, e-commerce, healthcare, education, government, and the country's massive BPO sector-is driving sustained enterprise demand for cloud computing, managed hosting, and colocation services that require continuous deployment of data center chips. Philippine enterprises are migrating workloads from aging on-premises infrastructure to modern cloud and colocation environments, each migration creating demand for new server processors, networking equipment, and storage systems. The BFSI sector's real-time transaction processing, fraud detection, and regulatory compliance requirements drive demand for high-performance CPUs and specialized accelerators. The IT-BPM industry-employing 1.8 million workers and generating USD 38 billion in annual revenue-requires massive compute capacity for AI-powered customer service automation, analytics, and content generation. The government's e-governance initiatives, the education sector's growing use of AI-powered learning platforms, and the retail and logistics sectors' demand for real-time inventory management and route optimization all converge to create broad-based chip demand that spans CPUs for general workloads, GPUs for AI applications, FPGAs for specialized processing, and networking ASICs for the high-bandwidth interconnections between compute resources.

AI Infrastructure Build-Out Requiring Specialized High-Performance Chips

The growing deployment of AI applications across Philippine industries is creating a distinct demand segment for high-performance GPU accelerators, AI-specific ASICs, and FPGA-based inference engines that command premium prices and drive the data center chip market's value growth. PLDT's launch of the Philippines' first GPU-as-a-Service platform powered by NVIDIA at VITRO Sta. Rosa represents the beginning of a fundamental shift in Philippine data center chip mix-from predominantly CPU-based infrastructure toward GPU-dense configurations that support machine learning model training, large language model inference, and computer vision applications. Philippine enterprises in BFSI, healthcare, telecommunications, and BPO are adopting AI solutions that require dedicated GPU clusters for model training and inference workloads. The country's AI sector-growing at approximately 29% annually toward a projected USD 3.5 billion by 2030-represents a rapidly expanding addressable market for AI-optimized chips. Data center operators are responding by designing new facilities with liquid cooling, high-density power distribution, and fiber interconnects specifically engineered for GPU rack deployments, ensuring that AI infrastructure requirements directly influence chip procurement strategies and facility design specifications across the Philippine data center ecosystem.

Browse the full report with TOC and list of figures: https://www.imarcgroup.com/philippines-data-center-chip-market

How AI is Reshaping the Philippines Data Center Chip Market:

• AI-driven workload optimization reshaping chip selection and procurement: Data center operators in the Philippines are deploying AI-powered workload management systems that analyze computing demand patterns in real time, dynamically allocating tasks across GPUs, CPUs, and FPGAs based on performance requirements and energy efficiency-enabling operators to optimize chip utilization rates, reduce idle compute capacity, and make more informed procurement decisions about the optimal mix of processor types for their specific tenant workload profiles.

• AI-powered predictive maintenance extending chip and server lifespan: Machine learning models deployed across Philippine data center facilities are continuously monitoring chip temperatures, power consumption, error rates, and performance degradation patterns to predict hardware failures before they occur-enabling proactive component replacement that minimizes downtime, extends the operational lifespan of expensive GPU and CPU installations, and optimizes the timing of technology refresh cycles across large-scale deployments.

• AI-optimized cooling systems enabling higher-density chip deployments: Artificial intelligence algorithms are managing the advanced liquid cooling systems being deployed in Philippine data centers-including the direct-to-chip cooling demonstrated at STT GDC's Liquid Cooling Technology Showroom-by dynamically adjusting coolant flow rates, temperatures, and fan speeds based on real-time chip thermal data, allowing operators to safely push GPU and CPU power densities higher while maintaining optimal operating temperatures in the Philippines' tropical climate.

• AI inference demand driving edge-to-core chip architecture evolution: The growing need for low-latency AI inference across Philippine applications-from BPO chatbot responses to financial fraud detection and e-commerce recommendation engines-is driving a architectural shift toward deploying inference-optimized chips (including FPGAs and custom ASICs) closer to end users at edge locations, while maintaining GPU-dense training clusters in centralized hyperscale facilities, creating a distributed chip demand pattern across the Philippines' expanding data center geography.

• AI-powered energy management optimizing chip power consumption and sustainability: Philippine data center operators are implementing AI-driven power management systems that monitor and optimize energy consumption across thousands of chips in real time-dynamically adjusting processor frequencies, voltage levels, and workload scheduling to minimize power draw during low-demand periods while maintaining performance during peak loads, supporting operators' sustainability commitments including STT GDC's 100% renewable energy-powered portfolio and the broader industry push toward green data center operations.

Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Philippines data center chip market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on chip type, data center size, and industry vertical.

By Chip Type:

• GPU

• ASIC

• FPGA

• CPU

• Others

By Data Center Size:

• Small and Medium Size

• Large Size

By Industry Vertical:

• BFSI

• Manufacturing

• Government

• IT and Telecom

• Retail

• Transportation

• Energy and Utilities

• Others

By Region:

• Luzon

• Visayas

• Mindanao

Key Players:

The Philippines data center chip market features a competitive landscape comprising global semiconductor manufacturers, data center chip designers, and server OEMs supplying the country's expanding data center ecosystem. The market research report provides a comprehensive analysis of the competitive landscape including key player positioning, market structure, top winning strategies, competitive dashboards, and detailed company profiles. Some of the major players include NVIDIA Corporation, Intel Corporation, Advanced Micro Devices (AMD), Broadcom Inc., Qualcomm, Xilinx (AMD), Marvell Technology, Samsung Electronics, SK Hynix, Micron Technology, and other global semiconductor participants competing across GPUs, CPUs, ASICs, FPGAs, memory chips, and networking processors supplied to data center operators throughout the Philippines.

Key Aspects Required for the Philippines Data Center Chip Market:

• Demand encompasses hyperscale data center operators procuring thousands of high-performance GPUs and CPUs for AI and cloud workloads, colocation providers equipping facilities with diverse chip configurations to serve multi-tenant environments, enterprise data centers upgrading on-premises infrastructure with latest-generation processors, telecommunications operators deploying edge computing chips for 5G network functions, and managed service providers building out AI inference platforms-all accelerated by the tripling of national data center capacity toward 500 MW.

• Luzon-particularly Metro Manila, Cavite, Laguna, and the emerging Clark Special Economic Zone-dominates data center chip demand due to its concentration of operational and upcoming facilities, submarine cable landing stations, and proximity to enterprise customers, while Visayas (Cebu) and Mindanao (Davao) represent emerging markets as operators explore geographic diversification for disaster resilience and to serve growing regional enterprise demand.

• The national target of reaching 1.5 GW of data center capacity and the projected tripling of installed capacity by 2028 demonstrate that chip demand will scale substantially-requiring sustained supply chain relationships with global semiconductor manufacturers, strategic procurement planning to navigate chip allocation constraints, and potential development of regional chip distribution hubs to serve the Philippines' growing data center ecosystem.

• Power availability and cooling infrastructure represent critical constraints on chip deployment density-with the Philippines' tropical climate and island geography requiring data center operators to invest in advanced cooling solutions including liquid cooling and immersion cooling to support the 700W+ per-GPU power densities of latest-generation AI accelerators, while grid capacity and renewable energy procurement challenges influence facility sizing and chip procurement decisions.

• The Philippines' established semiconductor back-end ecosystem-with major OSAT (outsourced semiconductor assembly and test) operations from companies including Samsung Electro-Mechanics, Texas Instruments, and Analog Devices-provides local chip packaging, testing, and quality assurance capabilities that could support data center chip supply chain requirements, though the country does not currently manufacture the advanced logic chips (GPUs, CPUs) used in data center servers, creating dependence on global supply chains for primary chip procurement.

• The competitive landscape features NVIDIA dominating the GPU accelerator segment through its A100 and H100 deployments at facilities like VITRO Sta. Rosa, AMD competing on both CPU (EPYC) and GPU (Instinct) fronts, Intel defending server CPU market share with Xeon Scalable processors, Broadcom and Marvell supplying networking and custom ASICs, and emerging AI chip startups seeking to offer cost-effective inference alternatives-with procurement decisions driven by workload requirements, power efficiency, software ecosystem compatibility, and total cost of ownership across the facility lifecycle.

Recent News and Developments:

May 2026: The Philippines data center chip market continued accelerating alongside rapid AI and hyperscale infrastructure expansion across Southeast Asia. Industry analysts highlighted that the country's data center capacity is expected to grow significantly as AI-driven workloads, cloud computing, and semiconductor demand increase across the region.

April 2026: The United States and the Philippines announced plans to develop a 4,000-acre industrial hub in New Clark City focused on AI, semiconductor manufacturing, advanced computing, and digital infrastructure. The initiative is expected to strengthen the Philippines' role in global semiconductor and data center chip supply chains.

March 2026: The Philippines data center sector entered a strong expansion phase, with installed capacity projected to increase from approximately 632.8 MW in 2025 to 852.8 MW by 2030. Growth is being driven by hyperscale deployments, AI adoption, enterprise cloud migration, and increasing semiconductor-related digital infrastructure demand.

March 2026: Converge ICT Solutions announced development of a PHP 5 billion data center project in Pampanga, reflecting increasing domestic investment in cloud computing, enterprise storage, and AI-enabled digital infrastructure. Industry participants noted rising demand for high-performance data center chips and semiconductor systems supporting hyperscale facilities.

January 2026: The Philippines semiconductor market reached approximately USD 7.21 billion in 2026 and is projected to approach USD 9.92 billion by 2031, supported by AI-enabled data center growth, automotive electronics, and expanding 5G infrastructure. Integrated circuits accounted for nearly 62.74% of semiconductor market share in 2025.

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Speak to an analyst for a customized sample report PDF: https://www.imarcgroup.com/request?type=report&id=41876&flag=C

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel. No.: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Philippines Data Center Chip Market 2026 | Projected to Grow to USD 74.8 Million by 2034 here

News-ID: 4510588 • Views: …

More Releases from IMARC Group

Latin America Organic Skincare Market Growth Outlook for Beauty and Cosmetics Br …

Latin America Organic Skincare Market Summary:

• The Latin America Organic Skincare Market size reached USD 989.2 Million in 2025.

• Market is projected to reach USD 1,938.4 Million by 2034.

• Brazil dominates with a significant market share.

• Growth driven by rising consumer preference for natural beauty products, increasing awareness regarding harmful chemicals in conventional cosmetics, and expanding demand for sustainable and cruelty-free skincare solutions.

IMARC Group, a leading market research company, has…

South Africa Health and Wellness Market Set to Surge to USD 42.5 Billion by 2034 …

South Africa Health and Wellness Market Overview

Market Size in 2025: USD 27.9 Billion

Market Size in 2034: USD 42.5 Billion

Market Growth Rate 2026-2034: 4.56%

According to IMARC Group's latest research publication, "South Africa Health and Wellness Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2026-2034", the South Africa health and wellness market size reached USD 27.9 Billion in 2025. Looking forward, the market is expected to reach USD 42.5 Billion by…

India Electric Vehicle Charging Station Market to Reach USD 1,105.2 Million by 2 …

India's electric vehicle (EV) charging station market is undergoing a transformative growth phase, driven by an unprecedented surge in EV adoption, robust government policy support, and aggressive infrastructure expansion across the country. As India accelerates its transition towards sustainable mobility under national decarbonization goals, the demand for accessible, reliable, and fast-charging networks is expanding rapidly across both public and private domains.

Behind this market momentum lies a powerful convergence of government-backed…

Philippines Electric Vehicle Market Expected to Hit USD 20.57 Billion by 2034 at …

Philippines Electric Vehicle Market Overview:

The Philippines electric vehicle market size reached USD 3.40 Billion in 2025. Looking forward, the market is expected to reach USD 20.57 Billion by 2034, exhibiting a growth rate (CAGR) of 19.73% during 2026-2034. The market encompasses battery cells and packs, on-board chargers, and fuel stacks across slow charging and fast charging types, spanning battery electric vehicles (BEVs), fuel cell electric vehicles (FCEVs), plug-in hybrid electric…

More Releases for Philippine

Kantar Group - Entering the Philippine Market in 2024

Kantar Group is an international market research company headquartered in London, UK, founded in 1992. Over the years, the company has become a pioneer in the market research industry through continuous innovative ideas and technological development. Through a series of mergers and acquisitions, Kantar has rapidly expanded globally. Since July 2019, Kantar is majority owned by Bain Capital Private Equity. Kantar currently has offices in 90 markets around the world,…

Boosting Philippine E-commerce with E-Signature Technology

Introduction

In the era of digital transformation, e-signature Philippines plays a pivotal role in modernizing business operations. Recognized under Republic Act No. 8792, electronic signatures and digital signatures offer a secure and efficient alternative to traditional paper-based processes. This guide explores the intricacies of e-signature Philippines, including its legal standing, benefits, and the top solutions driving this digital evolution.

Legal Framework for E-Signatures in the Philippines

Republic Act No. 8792: The E-Commerce Act

Enacted…

New Era in Consumer Lending Market is growing in Huge Demand in 2020 | Philippin …

The Consumer Lending Market is expected to reach +19% CAGR during forecast period 2020-2026.

Consumer lending provides financing for personal, family, or household purposes. The loans can come from a variety of places, including financial institutions or lending platforms, like the aforementioned Prosper and Lending Club. Increase in government initiative toward Consumer lending, and surge in need of reduced loan management time among borrowers and lenders have boosted the growth of…

Global Consumer Lending Market is Booming Across the Globe Explored in Latest Re …

The Consumer Lending Market is expected to reach +19% CAGR during forecast period 2020-2026.

Consumer lending provides financing for personal, family, or household purposes. The loans can come from a variety of places, including financial institutions or lending platforms, like the aforementioned Prosper and Lending Club. Increase in government initiative toward Consumer lending, and surge in need of reduced loan management time among borrowers and lenders have boosted the growth of…

SOFITEL PHILIPPINE PLAZA MANILA WINS MULTIPLE AWARDS IN THE 2018 PHILIPPINE CULI …

Sofitel Philippine Plaza Manila won several awards spanning various categories in the recently concluded Philippine Culinary Cup 2018 (PCC). Held at the SMX Convention Center last August 1 – 4, 2018, Sofitel Philippine Plaza Manila’s master chefs secured multiple awards in the PCC’s Professional Division.

Led by Executive Chef Nicholas Shadbolt and under the instruction of team leaders Chinese Chef Michale Tai and Sous Chef Regine Lee, the Sofitel culinary…

Sourcing Destination Snapshot: The Emerging Philippine Value Proposition

“The Philippines offers many opportunities as an offshore sourcing destination as well as being well positioned as a regional hub for Asia Pacific.” - Ralph Schonenbach (CEO, Trestle Group)

In designing sourcing models, IT and BPO decision-makers literally have a “world” to choose from when it comes to competitive country locations. The unique needs of a business will clearly drive managers to seek out sites capable of satisfying a range…