Press release

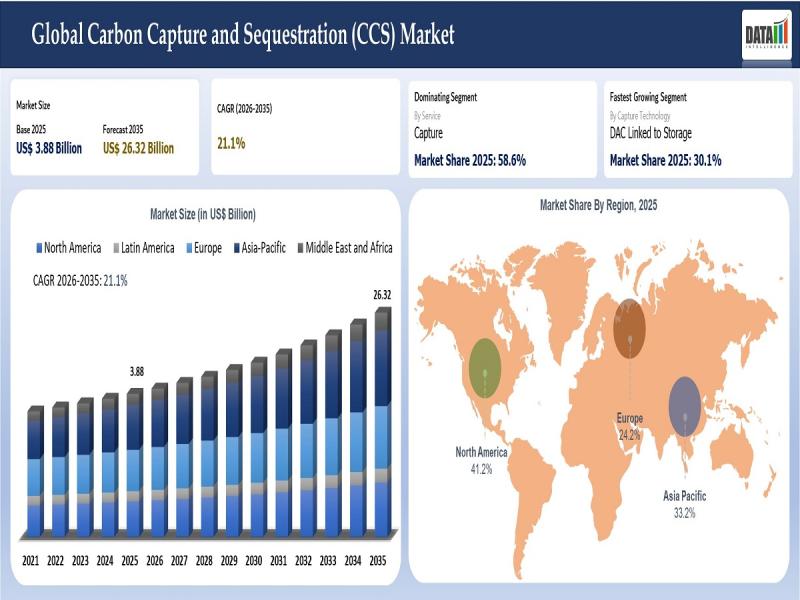

Carbon Capture and Sequestration Market to Reach US$ 26.32 Billion by 2035 at 21.1% CAGR; North America Leads with 39.5% Share - Key Players: ExxonMobil, Shell plc, Chevron Corporation

Carbon Capture and Sequestration Market

The market is also benefiting from strong regulatory support, expanding public and private funding initiatives, and increasing commercialization of advanced carbon capture technologies. Governments across North America and Europe are introducing tax incentives, emissions reduction policies, and large scale funding programs to accelerate CCS adoption and infrastructure development. Companies including Shell plc, ExxonMobil Corporation, Chevron Corporation, and Aker Carbon Capture ASA are actively investing in next generation carbon capture systems, direct air capture technologies, and integrated CO2 transportation and sequestration networks to strengthen their market position. Furthermore, increasing deployment of industrial decarbonization projects, advancements in carbon utilization technologies, and rising collaborations between energy companies and governments are creating substantial long term growth opportunities for the carbon capture and sequestration market worldwide.

Get a Free Sample PDF Of This Report (Get Higher Priority for Corporate Email ID): https://www.datamintelligence.com/download-sample/carbon-capture-and-sequestration-market?sai-v

Key Developments

February 2026: Rising investments in industrial decarbonization projects across North America and Europe accelerated deployment of large scale carbon capture and sequestration infrastructure for steel, cement, and chemical industries. Major companies including ExxonMobil, Shell plc, Equinor ASA, and TotalEnergies strengthened CCS partnerships supporting long term carbon storage capacity expansion.

January 2026: Increasing government funding and carbon reduction incentives across Germany, the United States, and the United Kingdom strengthened commercialization of CCS technologies in heavy industries and power generation facilities. Germany allocated €5 billion for industrial decarbonization projects including CCS integration and carbon contracts for difference programs.

December 2025: Growing expansion of CCS hubs and cross border CO2 transportation networks across the North Sea region accelerated development of large scale storage projects in Norway, Denmark, and the United Kingdom. Equinor, Shell plc, and TotalEnergies expanded the Northern Lights CCS project to increase annual storage capacity beyond 5 million tons by 2028.

November 2025: Rising adoption of CCS technologies across Asia-Pacific regions including China, Japan, and Australia strengthened deployment of carbon capture projects in coal power generation and industrial manufacturing sectors. Chinese state-owned enterprises accelerated CCUS project construction with significantly lower operational costs compared to European projects.

October 2025: Increasing advancements in low cost carbon capture technologies and AI-assisted CO2 storage monitoring improved operational efficiency and reduced carbon capture costs globally. Research institutions developed next generation pressure-induced carbon capture systems capable of capturing up to 99% of CO2 emissions at lower operational costs.

September 2025: Expansion of direct air capture and carbon utilization projects across the United States and Iceland accelerated innovation in atmospheric carbon removal technologies. Occidental Petroleum subsidiary 1PointFive and Climeworks strengthened investments in large scale direct air capture infrastructure supporting long term net zero initiatives.

August 2025: Increasing collaborations between energy companies, governments, and industrial manufacturers accelerated development of integrated CCUS ecosystems across Europe, North America, and Middle East regions. Mitsubishi Heavy Industries, Siemens Energy, and Linde plc expanded carbon capture technology portfolios supporting industrial emission reduction programs.

July 2025: Rising policy support, tax credits, and regulatory reforms across the Americas and Europe strengthened investor confidence in CCS deployment and storage infrastructure development. The United States maintained leadership in active CCS projects supported by the retention of 45Q tax credits and expanding Class VI permitting activity.

June 2025: Increasing focus on decarbonization of hard-to-abate industries including cement, refining, chemicals, and power generation supported strong growth in CCS market adoption worldwide. North America maintained market leadership, while Asia-Pacific emerged as the fastest growing regional market driven by industrial expansion and climate policy initiatives.

Key Players

ExxonMobil | Shell plc | Chevron Corporation | Equinor ASA | Siemens Energy | Aker Carbon Capture | Fluor Corporation | Mitsubishi Heavy Industries | Halliburton Company | Baker Hughes Company | TotalEnergies SE | SLB | Honeywell International Inc. | GE Vernova Inc. | Others

Key Highlights

ExxonMobil - Holds a 13.8% share, driven by large-scale carbon capture infrastructure projects, expanding low-carbon investments, and integrated carbon storage and transportation capabilities.

Shell plc - Holds a 12.4% share, supported by advanced carbon capture and storage project development, global decarbonization initiatives, and strong expertise in industrial emissions reduction technologies.

Chevron Corporation - Holds an 11.1% share, fueled by strategic CCS investments, expanding carbon sequestration partnerships, and integrated upstream carbon management solutions.

Equinor ASA - Holds a 9.2% share, driven by offshore carbon storage leadership, large-scale North Sea CCS projects, and strong renewable energy integration capabilities.

Siemens Energy - Holds an 8.0% share, supported by advanced carbon capture technologies, industrial decarbonization systems, and energy-efficient power generation infrastructure solutions.

Aker Carbon Capture - Holds a 6.7% share, powered by proprietary carbon capture technologies, modular capture plant solutions, and strong commercial deployment capabilities across industrial sectors.

Fluor Corporation - Holds a 5.9% share, driven by engineering and construction expertise, integrated CCS project execution capabilities, and large-scale industrial infrastructure development solutions.

Mitsubishi Heavy Industries - Holds a 5.0% share, supported by advanced CO2 capture technologies, industrial emissions reduction systems, and extensive thermal power plant decarbonization expertise.

Halliburton Company - Holds a 4.2% share, fueled by subsurface engineering capabilities, carbon storage site development expertise, and integrated energy transition solutions.

Baker Hughes Company - Holds a 3.8% share, driven by carbon capture process technologies, industrial gas handling systems, and expanding energy transition technology portfolio.

TotalEnergies SE - Holds a 3.2% share, supported by integrated carbon management projects, expanding low-carbon energy investments, and strategic CCS infrastructure partnerships.

SLB - Holds a 2.7% share, powered by subsurface carbon storage expertise, digital reservoir modeling technologies, and advanced well engineering solutions for CCS applications.

Honeywell International Inc. - Holds a 2.3% share, driven by industrial carbon capture process technologies, emissions monitoring systems, and advanced automation solutions for decarbonization projects.

GE Vernova Inc. - Holds a 1.9% share, supported by power generation decarbonization technologies, carbon capture integration systems, and advanced energy transition infrastructure solutions.

Others - Hold a combined 10.8% share, comprising regional energy companies, industrial engineering firms, and emerging carbon management technology providers advancing carbon capture, utilization, and long-term sequestration solutions globally.

Purchase Corporate License | Market Intelligence: https://www.datamintelligence.com/buy-now-page?report=carbon-capture-and-sequestration-market?sai-v

Market Drivers

Increasing global focus on carbon emission reduction and climate change mitigation is significantly driving demand for carbon capture and sequestration (CCS) technologies worldwide.

Growing implementation of stringent environmental regulations and net-zero emission targets across industrial sectors is accelerating adoption of CCS solutions.

Rising investments in decarbonization initiatives within power generation, cement, steel, oil & gas, and chemical industries are strengthening expansion of the CCS market globally.

Increasing government funding, tax incentives, and carbon credit programs are supporting commercialization and large-scale deployment of carbon capture infrastructure.

Growing demand for low-carbon industrial operations and sustainable energy transition strategies is boosting integration of CCS technologies with hydrogen production and industrial processing facilities.

Expansion of carbon utilization and storage projects, including enhanced oil recovery (EOR) and geological sequestration systems, is contributing to market growth.

Continuous advancements in direct air capture, post-combustion capture technologies, and carbon transportation infrastructure are further propelling innovation in the CCS industry worldwide.

Industry Developments

Rapid advancement in direct air capture and next-generation carbon absorption technologies improving carbon capture efficiency and reducing operational costs.

Increasing development of large-scale carbon transport and storage infrastructure including pipeline networks and offshore sequestration facilities.

Growing investments in blue hydrogen projects integrating carbon capture technologies to support low-emission hydrogen production.

Expansion of industrial carbon capture projects across cement, steel, refining, and chemical manufacturing sectors accelerating commercial deployment of CCS systems.

Rising collaborations among energy companies, governments, engineering firms, and technology providers supporting development of integrated carbon management ecosystems.

Strategic regulatory frameworks, carbon pricing mechanisms, and public-private partnerships encouraging global CCS project expansion and long-term investment.

Continuous innovation in AI-driven monitoring systems, carbon storage verification technologies, and advanced solvent-based capture methods improving operational efficiency and environmental safety.

Regional Insights

North America 39.5% share: "Leads the market due to strong government incentives, extensive carbon pipeline infrastructure, major CCS project deployments, and increasing investments in decarbonization technologies across the U.S. and Canada."

Europe 30.2% share: "Growth supported by stringent carbon reduction regulations, expanding offshore carbon storage projects, increasing renewable energy transition initiatives, and strong climate policy frameworks."

Asia Pacific 22.8% share: "Fastest-growing region driven by rapid industrialization, rising carbon emissions, increasing government decarbonization commitments, and expanding CCS investments in countries such as China, Japan, South Korea, and Australia."

Latin America 4.1% share: "Emerging growth supported by increasing carbon management initiatives, expanding oil & gas decarbonization projects, and growing interest in sustainable industrial development."

Middle East & Africa 3.4% share: "Gradual growth driven by rising investments in clean energy transition, expansion of enhanced oil recovery projects, and increasing adoption of carbon reduction technologies in the energy sector."

Speak to our analyst and get customization in the report as per your requirements:https://www.datamintelligence.com/customize/carbon-capture-and-sequestration-market?sai-v

Key Segments

➥ By Service

Capture: Represents the dominant segment, driven by increasing deployment of carbon capture technologies across high-emission industrial sectors and power generation facilities.

Compression and Dehydration: Represents a significant segment, supported by growing need for efficient CO2 processing prior to transportation and long-term storage.

Transportation: Represents a rapidly growing segment, fueled by expanding carbon transport infrastructure projects and rising investments in cross-border CO2 logistics networks.

Storage: Represents a substantial segment, driven by increasing development of geological sequestration sites and long-term carbon management initiatives.

➥ By Capture Technology

Post Combustion Capture: Represents the dominant segment, driven by widespread retrofitting of existing industrial plants and power stations with carbon capture systems.

Pre-Combustion Capture: Represents a significant segment, supported by increasing adoption in hydrogen production and integrated gasification combined cycle (IGCC) facilities.

Oxy Fuel Combustion: Represents a growing segment, fueled by rising demand for high-purity CO2 streams and advancements in clean combustion technologies.

Industrial Process Capture: Represents a rapidly growing segment, driven by increasing decarbonization efforts in cement, steel, and chemical manufacturing industries.

DAC Linked to Storage: Represents an emerging segment, supported by growing investments in direct air capture technologies and long-term climate mitigation strategies.

➥ By Source

Point Source Capture: Represents the dominant segment, driven by extensive deployment of CCS technologies at industrial facilities and fossil fuel-based power plants.

DAC to Storage: Represents a rapidly growing segment, fueled by increasing focus on carbon removal technologies and government support for net-zero emission initiatives.

➥ By Transportation Mode

Pipeline: Represents the dominant segment, driven by cost-effective large-scale CO2 transportation and expanding pipeline infrastructure networks globally.

Ship: Represents a growing segment, supported by increasing offshore carbon storage projects and cross-border CO2 transportation requirements.

Rail: Represents a moderate segment, fueled by limited but growing utilization in regions lacking dedicated pipeline infrastructure.

Truck: Represents a niche segment, driven by small-scale carbon transport applications and pilot CCS projects.

➥ By Storage Type

Saline Aquifers: Represents the dominant segment, driven by large storage capacity, widespread geological availability, and long-term carbon sequestration potential.

Depleted Oil Fields: Represents a significant segment, supported by existing infrastructure availability and increasing enhanced oil recovery integration projects.

Depleted Gas Fields: Represents a growing segment, fueled by rising utilization of mature gas reservoirs for secure underground CO2 storage.

EOR Linked Storage: Represents a substantial segment, driven by increasing adoption of enhanced oil recovery techniques combined with carbon sequestration operations.

Basalt and Reactive Rock Formations: Represents an emerging segment, supported by growing research into mineralization-based permanent carbon storage solutions.

Unmineable Coal Seams: Represents a moderate segment, fueled by ongoing exploration of alternative geological storage opportunities.

Other Geological Storage: Represents a developing segment, driven by continuous advancements in underground carbon sequestration technologies.

➥ By Facility Scale

Pilot and Demonstration: Represents a significant segment, driven by increasing research funding and validation of emerging carbon capture technologies.

Commercial Small Scale: Represents a growing segment, supported by rising adoption of modular CCS systems across mid-sized industrial facilities.

Commercial Large Scale: Represents the dominant segment, fueled by major government investments, industrial decarbonization targets, and expansion of large integrated CCS hubs.

➥ By Application

Oil and Gas: Represents the dominant segment, driven by increasing decarbonization initiatives and extensive use of CCS in upstream and downstream operations.

Power Generation: Represents a significant segment, supported by growing retrofitting of thermal power plants with carbon capture systems.

Natural Gas Processing: Represents a rapidly growing segment, fueled by rising need to reduce emissions during gas purification and processing operations.

Hydrogen: Represents an emerging high-growth segment, driven by increasing blue hydrogen production projects integrated with carbon capture technologies.

Ammonia and Fertilizers: Represents a growing segment, supported by rising focus on low-carbon fertilizer manufacturing processes.

Cement: Represents a substantial segment, fueled by increasing pressure to reduce hard-to-abate industrial emissions from cement production.

Iron and Steel: Represents a significant segment, driven by growing adoption of CCS technologies for industrial decarbonization in steel manufacturing.

Chemical and Petrochemical: Represents a rapidly growing segment, supported by increasing emission reduction initiatives across chemical production facilities.

Refineries: Represents a major segment, fueled by rising investments in low-carbon refining technologies and emission management systems.

Pulp and Paper: Represents a moderate segment, driven by increasing sustainability initiatives and bioenergy carbon capture projects.

Waste to Energy: Represents an emerging segment, supported by growing focus on negative emission technologies and sustainable waste management systems.

Others: Represents a developing segment, fueled by expanding CCS applications across various industrial sectors.

➥ By Project Stage

Announced: Represents a rapidly growing segment, driven by increasing global climate commitments and rising investments in future CCS infrastructure projects.

Engineering and Design: Represents a significant segment, supported by expanding feasibility studies and detailed planning activities for large-scale CCS developments.

Under Construction: Represents a growing segment, fueled by accelerating deployment of commercial carbon capture and storage facilities worldwide.

Operational: Represents the dominant segment, driven by increasing number of active CCS facilities supporting industrial emission reduction efforts.

➥ By End-User

Industrial Sector: Represents the dominant segment, driven by rising pressure on heavy industries to achieve emission reduction targets and comply with environmental regulations.

Energy and Utilities: Represents a significant segment, supported by increasing deployment of CCS technologies in power generation and energy production facilities.

Oil & Gas Companies: Represents a rapidly growing segment, fueled by strong investments in carbon management infrastructure and enhanced oil recovery projects.

Government and Public Sector: Represents a growing segment, driven by increasing policy support, funding initiatives, and national decarbonization strategies.

Others: Represents an emerging segment, supported by rising participation of research institutions, technology developers, and private investors in CCS projects.

Unlock 360° Market Intelligence with DataM Subscription Services: https://www.datamintelligence.com/reports-subscription

Power your decisions with real-time competitor tracking, strategic forecasts, and global investment insights all in one place.

✅ Competitive Landscape

✅ Sustainability Impact Analysis

✅ KOL / Stakeholder Insights

✅ Unmet Needs & Positioning, Pricing & Market Access Snapshots

✅ Market Volatility & Emerging Risks Analysis

✅ Quarterly Industry Report Updated

✅ Live Market & Pricing Trends

✅ Import-Export Data Monitoring

Have a look at our Subscription Dashboard: https://www.youtube.com/watch?v=x5oEiqEqTWg

Contact:

Fabian

DataM Intelligence 4market Research LLP

6th Floor, M2 Tech Hub, DataM Intelligence 4market Research LLP, Lalitha Nagar, Habsiguda, Secunderabad, Hyderabad, Telangana 500039

USA: +1 877-441-4866

UK: +44 161-870-5507

Email: fabian@datamintelligence.com

About Us -

DataM Intelligence is a Market Research and Consulting firm that provides end-to-end business solutions to organizations from Research to Consulting. We, at DataM Intelligence, leverage our top trademark trends, insights and developments to emancipate swift and astute solutions to clients like you. We encompass a multitude of syndicate reports and customized reports with a robust methodology.

Our research database features countless statistics and in-depth analyses across a wide range of 6300+ reports in 40+ domains creating business solutions for more than 200+ companies across 50+ countries; catering to the key business research needs that influence the growth trajectory of our vast clientele.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Carbon Capture and Sequestration Market to Reach US$ 26.32 Billion by 2035 at 21.1% CAGR; North America Leads with 39.5% Share - Key Players: ExxonMobil, Shell plc, Chevron Corporation here

News-ID: 4510495 • Views: …

More Releases from DataM intelligence 4 Market Research LLP

OEM Insulation Market (2026) | HVAC Growth, Heat Management Technologies, Therma …

DataM Intelligence has unveiled its latest research study, "OEM Insulation Market Size 2026," delivering strategic intelligence designed to identify high-growth opportunities, evaluate competitive positioning, and stay ahead of rapidly evolving market trends. The report provides a comprehensive analysis of market size, revenue performance, CAGR projections, regional growth patterns, and detailed segmentation insights, along with an in-depth assessment of the key factors driving industry expansion. It also highlights emerging opportunities, investment…

Neuromodulation Devices Market to Reach US$ 203.45 Billion by 2033 at 7.0% CAGR; …

The global neuromodulation devices market was valued at US$ 111.56 billion in 2025 and is expected to reach US$ 203.45 billion by 2033, growing at a CAGR of 7.0% during the forecast period from 2026 to 2033. The market is witnessing substantial growth driven by the increasing prevalence of neurological disorders, chronic pain conditions, epilepsy, Parkinson's disease, and depression, along with rising demand for minimally invasive treatment alternatives. Growing adoption…

Blood Warmer Devices Market (2025) | Fluid Warmers, Blood Warming Machine, Blood …

DataM Intelligence has unveiled its latest research study, "Blood Warmer Devices Market Size 2025," delivering strategic intelligence designed to identify high-growth opportunities, evaluate competitive positioning, and stay ahead of rapidly evolving market trends. The report provides a comprehensive analysis of market size, revenue performance, CAGR projections, regional growth patterns, and detailed segmentation insights, along with an in-depth assessment of the key factors driving industry expansion. It also highlights emerging opportunities,…

Nootropics Industry Projected to Hit USD 46,788.6 Million by 2033 at 14.3% CAGR, …

DataM Intelligence has released a new research report titled "Nootropics Market Size 2026". The report delivers in-depth insights into key market dynamics, including regional growth trends, market segmentation, CAGR projections, and the revenue performance of leading industry players. It also highlights major growth drivers shaping the market landscape. Designed to provide a clear and comprehensive perspective, the report offers a detailed view of the current market size in terms of…

More Releases for Represents

Caramanna, Friedberg LLP Represents Individuals in Domestic Assault Cases

Image: https://www.globalnewslines.com/uploads/2025/05/1747915647.jpg

Most of them, charges of domestic assaults usually arise from tense situations. Once the accused is arrested, often, there is nothing the complainant can do to reverse or mitigate the charges. Even if the partner wants to drop certain charges, the process of pressing criminal charges will still continue. When this happens, it is better to just leave the situation in the hands of a good lawyer. At Caramanna,…

Art US Nation represents Elena Ksanti - International Artist

Art US Nation Association unites personalities from the USA and abroad, from the worlds of art, creative NFT, culture and design. Association selects new Art Ambassador Members once a year as a result of the board meeting, analyzing the contribution of the participant to the USA and global art and considering artist's extraordinary abilities. Discover: Elena Ksanti - new AUN association member and ART US NATION Ambassador 2024.

Elena Ksanti began…

Hybrid Global’s New Singles Represents Exceptional Musical Blends

Hybrid Global was founded in 2009 with collaboration of Hybrid Entertainment. Roni Raxx, the American rapper is getting popular with his all new hip hop and rap sensations. On the opposite hand, Meezy’s versatile voice can blow your mind. Thereon, the new aspiring star Thrash Gatsby has created large contribution in hip hop genre. Hybrid Global has been dominating soundcloud for the past 5 years. Today, it has collected thousands…

Staticspaz’s “Bad Man” Represents Wonderful Rhythm –Verse Mix

Rap singer, StaticSpaz usually produces songs based on hip hop and rap. In contrast to other rap and hip hop artists, StaticSpaz is hard working and very proficient. This aspiring rockstar has already launched numerous songs in soundcloud. Amongst them “Bad Man” has purportedly collected large range of plays count. StaticSpaz expects his fans count to grow from thousands to millions. This song is gaining popularity in social media. His…

Steep Management, LLC Represents Medic52

Happy & Safe Customers

Warren, VT, USA

Contact: Bob Ackland

Steep Management and Medic52 have agreed to have Steep Management represent Medic52’s Suite of Ski Patrol management tools to the ski industry throughout North America effective as of October 10, 2016.

Medic52 has developed a seamless integrated suite of tools for modern risk and incident management. This suite of tools enables ski area managers to stay on top of the daily life of…

Area student represents TMI at Rotary conference

Dale Fastle of Boerne, a junior at TMI – The Episcopal School of Texas, was chosen to represent TMI at the Rotary Youth Leadership Assembly (RYLA) conference, Jan. 14-17, at the John Newcomb Tennis Ranch in New Braunfels.

Chosen by their schools on the basis of leadership potential, 160 juniors from more than 50 high schools attended the conference, sponsored by Rotary International District 5840 of Central Texas. An additional 32…