Press release

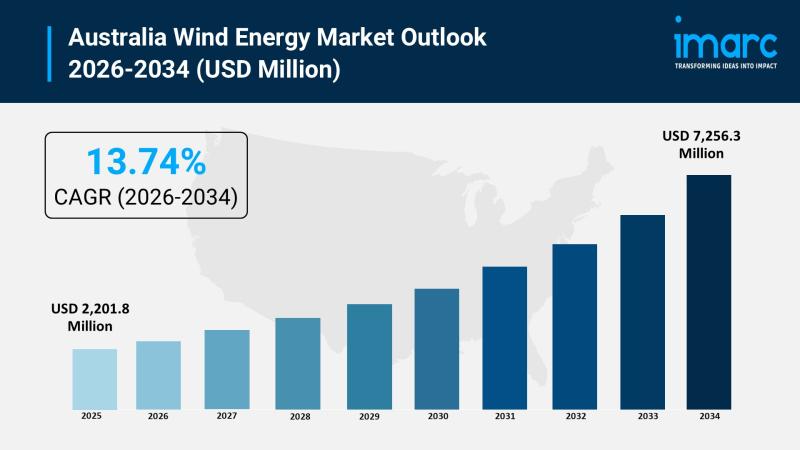

Australia Wind Energy Market 2026 | Anticipated to Reach USD 7,256.3 Million by 2034 | CAGR: 13.74%

The Australia wind energy market size reached USD 2,201.8 Million in 2025. Looking forward, the market is expected to reach USD 7,256.3 Million by 2034, exhibiting a growth rate (CAGR) of 13.74% during 2026-2034. The market encompasses turbines, support structures, electrical infrastructure, and other components across offshore and onshore installations with horizontal axis and vertical axis turbine types, serving utility, industrial, commercial, and residential applications in Australia Capital Territory and New South Wales, Victoria and Tasmania, Queensland, Northern Territory and Southern Australia, and Western Australia. Australia's ambitious 82% renewable energy target by 2030, massive onshore wind farm pipeline exceeding 17 GW in development, emerging offshore wind sector with 25 GW potential across twelve declared zones, declining turbine capital costs, state-level renewable energy zones backed by billions in network investment, and growing corporate power purchase agreement demand are among the key factors driving market growth throughout the forecast period.

Request for a sample report PDF: https://www.imarcgroup.com/australia-wind-energy-market/requestsample

Australia Wind Energy Market Summary:

• Australia approved 6.9 GW of onshore wind capacity in 2025, with the country's wind project pipeline exceeding 17.3 GW in various stages of development and 5.99 GW of projects actively under construction-demonstrating accelerating momentum toward the federal government's 82% renewable energy target by 2030 that requires massive wind generation build-out.

• The 923 MW MacIntyre Wind Farm in Queensland's Southern Downs region commenced full operations as Australia's largest wind farm, featuring 162 turbines approximately 50 kilometers southwest of Warwick-setting a new benchmark for utility-scale onshore wind development and demonstrating that Queensland's wind resources can support projects rivaling traditional strongholds in South Australia and Victoria.

• Australia's offshore wind sector advanced significantly with twelve declared offshore wind zones offering potential generation capacity of up to 25 GW, while Star of the South-the country's most advanced offshore wind project at 2.2 GW-submitted its Environmental Impact Statement in December 2025, and Victoria announced its first offshore wind auction for August 2026 targeting an initial 2 GW.

• The Australian government offered three new offshore wind licenses off Western Australia's coast in January 2026 with projects expected to add up to 4 GW of clean energy capacity, while ten new renewable energy projects totaling 1.886 GW were approved for Western Australia including the 470 MW Parron Maam Marang Wind Farm and 240 MW Tathra Wind Farm.

• Vestas secured a 577 MW contract for Stage 2 of the 1.3 GW Golden Plains Wind Farm in Victoria featuring 93 V162-6.2 MW EnVentus turbines-making it the company's largest onshore wind project globally and demonstrating the scale of individual Australian wind investments that attract world-leading turbine manufacturers.

• New South Wales leads the state-level pipeline with 8.1 GW targeted across Central-West Orana and New England Renewable Energy Zones backed by AUD 5.45 billion in network investment and up to AUD 20 billion in anticipated private sector capital deployment for wind generation and supporting infrastructure.

• Market segmentation covers four components (turbine, support structure, electrical infrastructure, others), six rating categories (≤2 MW through >12 MW), two installation types (offshore, onshore), two turbine types (horizontal axis, vertical axis), four applications (utility, industrial, commercial, residential), and five regions (ACT and NSW, Victoria and Tasmania, Queensland, Northern Territory and Southern Australia, Western Australia).

Key Trends Shaping the Australia Wind Energy Market:

• Mega-scale onshore wind farms becoming the norm: Australian onshore wind development has shifted decisively toward gigawatt-scale projects that deliver economies of scale in procurement, construction, and grid connection. The 1.3 GW Golden Plains Wind Farm, 923 MW MacIntyre Wind Farm, and multiple proposed projects exceeding 500 MW represent a fundamental evolution from the sub-200 MW developments that characterized the previous decade. These mega-projects leverage larger turbine platforms (6+ MW onshore) that reduce the number of foundations, access roads, and grid connection points per megawatt while accessing higher and more consistent wind resources through taller hub heights. The CSIRO projects a 5% drop in wind capital costs in the current financial year, making these large-scale developments increasingly competitive against gas-fired generation and even solar at equivalent capacity factors, while delivering the firm renewable generation volumes required to replace retiring coal-fired power stations.

• Offshore wind transitioning from planning to procurement: Australia's offshore wind sector is rapidly advancing from feasibility declarations to commercial procurement, with Victoria announcing its first offshore wind auction for August 2026 targeting 2 GW of initial capacity, and Western Australia receiving three new offshore wind license areas in January 2026 offering up to 4 GW. Star of the South's Environmental Impact Statement submission in December 2025 represents the most advanced project progressing toward construction decision, while Ocean Winds' 1.3 GW High Sea Wind project secured through Australia's first offshore wind tender demonstrates international developer confidence. The twelve declared offshore zones with combined potential exceeding 25 GW position Australia for a transformative offshore wind build-out through the 2030s-with individual projects targeting capacities above 2 GW that will require local supply chain development, port infrastructure upgrades, and specialized installation vessel access.

• Renewable Energy Zones concentrating development and investment: State-designated Renewable Energy Zones (REZs) are creating concentrated corridors of wind development where coordinated network investment de-risks individual project grid connections. NSW's Central-West Orana and New England REZs-backed by AUD 5.45 billion in transmission infrastructure and attracting up to AUD 20 billion in private investment-represent the model being replicated across Victoria, Queensland, and South Australia. These zones provide planning certainty, streamlined approvals, shared grid infrastructure, and community benefit frameworks that accelerate development timelines compared to standalone projects requiring individual transmission solutions. The REZ approach addresses the critical bottleneck that has historically constrained Australian wind development: grid connection capacity and the cost of building dedicated transmission lines from high-resource wind areas to demand centers.

• Investment drought breaking as financial close activity accelerates: After several years of subdued wind farm financial closures in Australia, 2025-2026 is showing signs of recovery with the 108 MW Waddi Wind Farm becoming the first wind project to reach financial close in 2025, followed rapidly by the 288 MW Palmer Wind Farm in South Australia. KKR's AUD 603 million injection into HMC Capital's 5.7 GW battery and wind development pipeline signals that institutional capital is returning to Australian wind at scale. The investment recovery reflects improving policy certainty, higher wholesale electricity prices driven by coal plant retirements, growing corporate PPA demand from technology companies and manufacturers seeking renewable energy, and declining capital costs that restore project economics after a period of supply chain inflation and interest rate increases that had stalled investment decisions.

• Western Australia emerging as the next wind energy frontier: Western Australia is positioning itself as a major wind energy market with ten new renewable energy projects approved delivering 1.886 GW of generation capacity, three new offshore wind licenses offered in January 2026 targeting up to 4 GW, and individual onshore projects including the 470 MW Parron Maam Marang Wind Farm and 240 MW Tathra Wind Farm advancing toward construction. The state's development momentum is driven by its unique circumstances-an isolated grid requiring self-sufficient generation, massive mining and industrial electricity demand suited to long-term corporate PPAs, world-class wind resources along the southern and western coastlines, and growing hydrogen production ambitions that require abundant renewable generation as feedstock for green hydrogen electrolysis.

Market Growth Drivers:

Federal 82% Renewable Energy Target Driving Unprecedented Wind Build-Out

Australia's federal government target of 82% renewable electricity generation by 2030 creates a policy-driven imperative for massive wind energy deployment, with industry analysis indicating that achieving this target requires approximately 30 GW of new wind and solar capacity to be built within the decade. Wind energy-delivering higher capacity factors than solar and generating during evening peak demand periods-is essential to meeting this target, particularly as aging coal-fired power stations retire and leave generation gaps that require firm renewable replacement. The current pipeline of 17.3 GW in onshore wind development and 25 GW of offshore potential represents the investment response to this policy signal, with state governments reinforcing federal targets through their own renewable energy commitments, Renewable Energy Zone designations, and transmission investment programs. The target's credibility is supported by AUD billions in public infrastructure investment and institutional frameworks including the Clean Energy Finance Corporation and Australian Renewable Energy Agency that reduce private sector risk.

Coal-Fired Power Station Retirements Creating Generation Replacement Demand

The accelerating retirement schedule of Australia's coal-fired power stations-with multiple large generators announcing earlier-than-planned closure dates-creates urgent demand for replacement generation capacity that wind energy is uniquely positioned to fill at scale. Australia's National Electricity Market requires approximately 50 GW of new generation to replace retiring coal capacity and meet growing electricity demand from electrification of transport, industry, and buildings. Wind farms delivering 6.9 GW of approved capacity in 2025 alone, combined with 5.99 GW under construction, demonstrate the sector's ability to deploy at the pace required, while the combination of onshore wind's competitive economics (with CSIRO projecting 5% capital cost reductions) and offshore wind's ability to access consistent maritime resources ensures that wind can provide both economic baseload-equivalent generation and geographic diversity that enhances grid reliability across multiple states simultaneously.

Corporate Power Purchase Agreements Providing Revenue Certainty for Developers

Growing corporate demand for renewable electricity-driven by ESG commitments, net-zero targets, and economic advantages of fixed-price clean energy-is providing the revenue certainty that enables wind farm developers to secure project financing and reach construction decisions. Major technology companies, manufacturers, miners, and industrial consumers are signing long-term power purchase agreements (PPAs) with wind farms that guarantee revenue streams for 10-15 years, making projects bankable independently of volatile wholesale electricity market prices. KKR's AUD 603 million investment in HMC Capital's 5.7 GW wind and battery pipeline reflects institutional confidence that corporate PPA demand will continue growing as more companies establish science-based emissions reduction targets. The emergence of multi-buyer PPAs-where multiple corporate off-takers share capacity from a single large wind farm-is further expanding the addressable market by enabling mid-sized companies to access wind energy without committing to entire project volumes.

Browse the full report with TOC and list of figures: https://www.imarcgroup.com/australia-wind-energy-market

How AI is Reshaping the Australia Wind Energy Market:

• AI-powered predictive maintenance reducing turbine downtime: Machine learning systems continuously monitoring thousands of data points per turbine-including vibration patterns, temperature readings, oil particle counts, and generator winding resistance-are enabling predictive maintenance that reduces unplanned downtime by up to 30% at Australian wind farms like Hornsdale in South Australia, with Transformer-based anomaly detection models achieving 94.7% accuracy in identifying component degradation before failure occurs, shifting maintenance from reactive schedule-based approaches to data-driven interventions that maximize turbine availability.

• AI-driven wind forecasting optimizing energy dispatch and trading: Advanced neural networks are processing satellite imagery, weather model outputs, and real-time SCADA data to forecast wind generation at individual turbine, farm, and portfolio levels with unprecedented accuracy-enabling Australian wind farm operators to optimize their bidding strategies in the National Electricity Market's five-minute dispatch intervals, reduce balancing costs, and maximize revenue by accurately predicting generation hours to days ahead rather than relying on simplified meteorological forecasts.

• AI-optimized turbine control maximizing energy capture: Artificial intelligence algorithms are dynamically adjusting individual turbine pitch angles, yaw positions, and generator torque settings in real-time based on actual wind conditions and wake interactions between neighboring turbines-increasing annual energy production by 2-5% across Australian wind farms without hardware modifications, with farm-level AI controllers coordinating turbine operations to minimize destructive wake effects that reduce downstream generation in large-scale developments like Golden Plains and MacIntyre.

• AI-enhanced site assessment and micrositing for new developments: Machine learning models are processing years of mesoscale weather data, terrain topography, vegetation roughness maps, and existing operational wind farm performance records to optimize turbine placement at proposed development sites-improving energy yield predictions, reducing uncertainty margins in project financial models, and enabling developers to maximize generation from available land area while meeting noise, visual, and environmental constraints that constrain turbine positioning across Australia's expanding wind farm pipeline.

• AI-based fleet management optimizing multi-farm operations: Portfolio-level artificial intelligence platforms are coordinating maintenance scheduling, spare parts logistics, crew deployment, and performance optimization across multiple wind farms simultaneously-considering weather windows, turbine availability, crane schedules, and component inventory to minimize total cost of energy across growing Australian wind portfolios where operators manage thousands of turbines spanning multiple states and climate zones with varying maintenance needs and logistics challenges.

Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Australia wind energy market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on component, rating, installation, turbine type, application, and region.

By Component:

• Turbine

• Support Structure

• Electrical Infrastructure

• Others

By Rating:

• ≤ 2 MW

• >2 ≤ 5 MW

• >5 ≤ 8 MW

• >8 ≤ 10 MW

• >10 ≤ 12 MW

• >12 MW

By Installation:

• Offshore

• Onshore

By Turbine Type:

• Horizontal Axis

• Vertical Axis

By Application:

• Utility

• Industrial

• Commercial

• Residential

By Region:

• Australia Capital Territory and New South Wales

• Victoria and Tasmania

• Queensland

• Northern Territory and Southern Australia

• Western Australia

Key Players:

The Australia wind energy market features a competitive landscape comprising international energy developers, domestic renewable energy companies, global turbine manufacturers, infrastructure investors, and specialized wind farm operators. The market research report provides a comprehensive analysis of the competitive landscape including key player positioning, market structure, top winning strategies, competitive dashboards, and detailed company profiles. Some of the major players include RWE, BlueFloat Energy, Vestas, Goldwind, Acciona Energia, Tilt Renewables, Neoen, Squadron Energy, Iberdrola, the Clean Energy Finance Corporation (CEFC), and other domestic and international participants competing across onshore, offshore, utility-scale, and distributed wind energy solutions throughout Australia.

Key Aspects Required for the Australia Wind Energy Market:

• Demand encompasses utility-scale generation replacing retiring coal-fired power stations, industrial consumers seeking fixed-price renewable energy through corporate power purchase agreements, commercial operations pursuing net-zero emissions commitments, residential communities in Renewable Energy Zones benefiting from local generation, and emerging hydrogen production requiring abundant renewable electricity as electrolysis feedstock.

• The federal 82% renewable energy target by 2030 creates a policy-driven imperative requiring approximately 30 GW of new wind and solar capacity within the decade, with the current 17.3 GW onshore pipeline, 5.99 GW under construction, and 25 GW offshore potential representing the investment response to this ambitious but achievable national commitment.

• State-designated Renewable Energy Zones-particularly NSW's Central-West Orana and New England REZs with AUD 5.45 billion in transmission investment-are creating concentrated development corridors that de-risk grid connection, streamline approvals, and attract the private sector capital (up to AUD 20 billion in NSW alone) needed to deliver wind generation at the pace and scale required.

• The offshore wind sector's transition from declaration to procurement-with Victoria's August 2026 auction, Western Australia's 4 GW license offerings, and Star of the South's 2.2 GW project approaching construction decision-requires development of local supply chains, port infrastructure, installation vessel capacity, and workforce training that will define Australia's offshore wind cost competitiveness for decades.

• The competitive landscape spans global energy majors (RWE, Iberdrola, Acciona), international developers (BlueFloat, Ocean Winds, Neoen), domestic players (Squadron Energy, Tilt Renewables), and turbine manufacturers (Vestas, Goldwind)-with successful market participation requiring demonstrated capability in project development, community engagement, grid connection management, and long-term asset operation at increasingly large scale.

• Financial close activity accelerating in 2025-2026-with Waddi Wind Farm, Palmer Wind Farm, and KKR's AUD 603 million investment in HMC Capital's 5.7 GW pipeline-signals that the investment drought is breaking as improving policy certainty, higher wholesale prices from coal retirements, declining capital costs, and growing corporate PPA demand restore project economics across the Australian wind sector.

Recent News and Developments:

• January 2026: The Australian government offered three new offshore wind licenses off the coast of Western Australia, with projects expected to add up to 4 GW of clean energy capacity-expanding the national offshore wind opportunity beyond the initial Gippsland and Hunter regions to Australia's western coastline.

• January 2026: Victoria announced its first offshore wind auction scheduled for August 2026, targeting an initial 2 GW of capacity as the state moves to commercialize its declared offshore wind zone in the Bass Strait region and establish Australia's first operational offshore wind generation.

• December 2025: Star of the South, Australia's most advanced offshore wind project at 2.2 GW capacity, submitted its Environmental Impact Statement for approval-marking a critical milestone toward construction decision for a project that would power approximately 1.5 million homes from offshore wind resources in Bass Strait.

• October 2025: The 412 MW Goyder South Wind Farm near Burra in South Australia began operations, estimated to generate approximately 1.5 TWh of renewable energy per year-adding significant firm generation capacity to South Australia's wind-dominated electricity system.

• June 2025: The 400 MW Gawara Baya Wind Farm near Ingham in Queensland was approved for development, reflecting growing project activity in Queensland where the state's northern wind resources are attracting large-scale investment alongside established development regions in Victoria and South Australia.

• 2025: The 108 MW Waddi Wind Farm in Western Australia's Dandaragan region became the first wind project to reach financial close in 2025, with construction set to begin in 2026-signaling the end of a multi-year investment drought that had slowed new wind farm commitments across Australia.

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Speak to an analyst for a customized sample report PDF: https://www.imarcgroup.com/request?type=report&id=24691&flag=C

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel. No.: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Australia Wind Energy Market 2026 | Anticipated to Reach USD 7,256.3 Million by 2034 | CAGR: 13.74% here

News-ID: 4504554 • Views: …

More Releases from IMARC Group

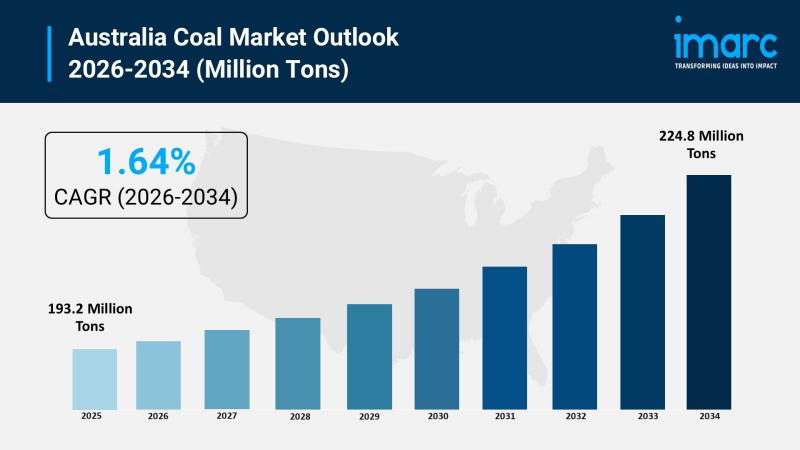

Australia Coal Market Projected to Reach 224.8 Million Tons During 2026-2034: IM …

Australia Coal Market Overview:

The Australia coal market reached a volume of 193.2 Million Tons in 2025. Looking forward, the market is expected to reach 224.8 Million Tons by 2034, exhibiting a growth rate (CAGR) of 1.64% during 2026-2034. The market encompasses bituminous coal, sub-bituminous coal, lignite coal, and anthracite coal produced through surface mining and underground mining technologies, serving power generation, steel, cement, residential and commercial, and other end-use industries…

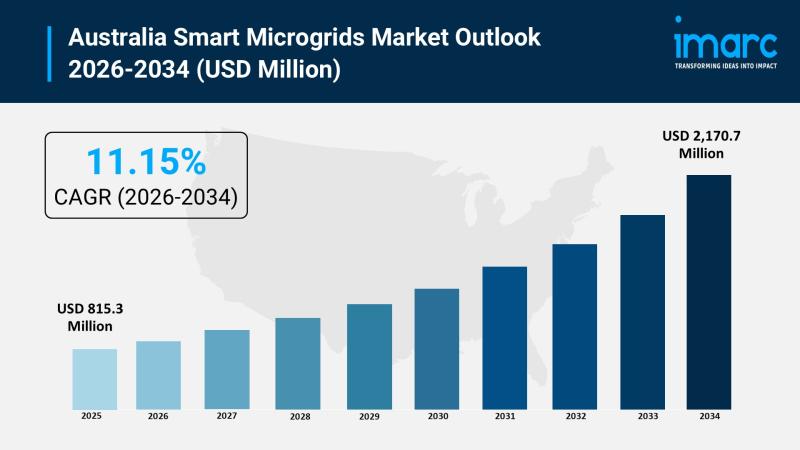

Australia Smart Microgrids Market 2026 | Worth USD 2,170.7 Million by 2034 | CAG …

Australia Smart Microgrids Market Overview:

The Australia smart microgrids market size reached USD 815.3 Million in 2025. Looking forward, the market is expected to reach USD 2,170.7 Million by 2034, exhibiting a growth rate (CAGR) of 11.15% during 2026-2034. The market encompasses hybrid, off-grid, and grid-connected microgrids integrating storage and inverter components with fuel cell and CHP power technologies, serving urban and rural consumers across campus, commercial, and defense applications in…

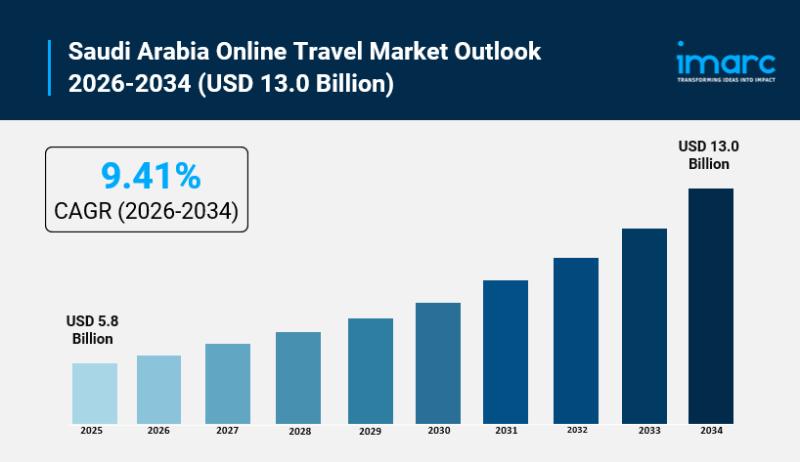

Saudi Arabia Online Travel Market Size to Hit USD 13.0 Billion by 2034, CAGR is …

Saudi Arabia Online Travel Market Overview

Market Size in 2025: USD 5.8 Billion

Market Forecast in 2034: USD 13.0 Billion

Market Growth Rate 2026-2034: 9.41%

According to IMARC Group's latest research publication, "Saudi Arabia Online Travel Market Size, Share, Trends and Forecast by Service Type, Platform, Mode of Booking, Age Group, and Region, 2026-2034", The Saudi Arabia online travel market size reached USD 5.8 Billion in 2025. Looking forward, IMARC Group expects the market…

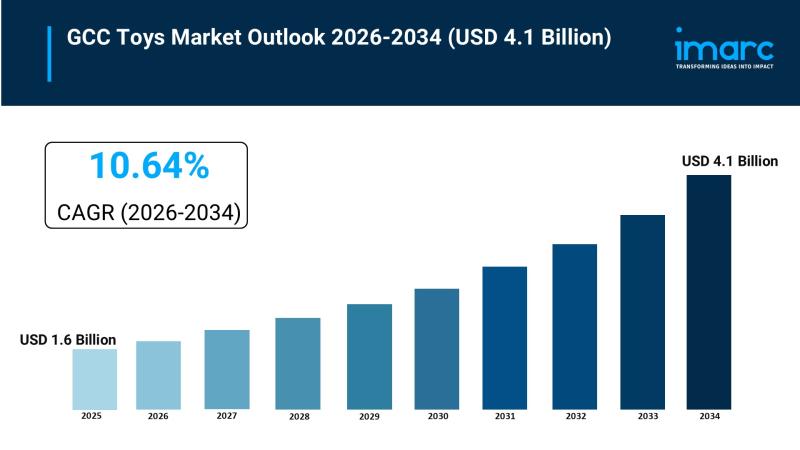

GCC Toys Market Size To Worth USD 4.1 Billion in 2034 | Grow CAGR by 10.64%

GCC Toys Market Overview

Market Size in 2025: USD 1.6 Billion

Market Size in 2034: USD 4.1 Billion

Market Growth Rate 2026-2034: 10.64%

According to IMARC Group's latest research publication, "GCC Toys Market Report by Product Type, Age Group, Sales Channel, and Country, 2026-2034," the GCC toys market size was valued at USD 1.6 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 4.1 Billion by 2034, exhibiting a CAGR…

More Releases for Australia

Derila Memory foam pillow Australia: Honest Reviews About Derila Australia

Derila is one of the best memory foam pillows sold in Australia today.

Priced at around 30 dollars (USD), derila is currently the most reviewed and the cheapest memory pillow available in Australia.

What is Derila? Is Derila Pillow the best in Australia? Keep reading to discover everything worth knowing about Derila Australia.

OVERVIEW

Recently, Memory foam pillow has been trending and there is a lot of brands to choose from. Which one is…

CeraCare Australia - Where to Buy Legit CeraCare Supplement in Australia?

CeraCare Australia - Ceracare is a glucose support supplement that proposes to augment cardiovascular prosperity and to stay aware of perfect glucose assimilation in Australia. CeraCare supplement is conceptualized and executed by a threesome – Christine, Dr. Jihn and Michael. It is a natural supplement that helps one stay aware of ideal glucose levels, cardiovascular prosperity, and glucose assimilation.

Take Advantage of 80% Discount Offer in Australia >> https://boostsxproaustralia.com/ceracare-new

The indications…

Glucofort Australia - Where to Buy Legit Glucofort Supplement in Australia?

Glucofort Australia - Glucofort is an efficient, all-natural progressive glucose support supplement in Australia. This formula is made out of 12 key ingredients, 7 nutrients, and minerals, and a little of Vanadium. This supplement upholds regulated glucose levels and glucose digestion. Glucofort prides itself as the most inventive supplements available in Oceania, accentuating its solidarity, wellbeing, and quality.

Take Advantage of 75% Discount Offer in Australia >> https://boostsxproaustralia.com/glucofort-new

Rather than simply…

Australia Agriculture Market, Australia Agriculture Industry, Australia Agricult …

Australia Agriculture has been as vital within the development of Australia, because it was within the United States. Australia's ancient dominance in wheat and sheep continues into the 21st century. Recently Australian agriculture has become more and more diversified. The considerable expanses of productive land have helped Australia to become a number one world exporter of grains, meats, and wool. Each grains (predominantly wheat and barley) and wool markets round…

Australia Conveyor Maintenance Analysis by Top Companies Habasit Australia Pty l …

Global Australia Conveyor Maintenance Market and Competitive Analysis

Know your current market situation! Not only a vital element for brand new products but also for current products given the ever-changing market dynamics. The study allows marketers to remain involved with current consumer trends and segments where they'll face a rapid market share drop. Discover who you actually compete against within the marketplace, with Market Share Analysis know market position, to push…

Australia Conveyor Maintenance Market Analysis By Manufacturers Rema Tip Top Aus …

A conveyor system is a common piece of mechanical handling device that moves materials/objects from one location. A conveyor is often lifeline to a company’s ability to effectively move its products in a timely manner. While it is used constantly in a manufacturing plant, proper maintenance from trained technicians can extend the lifespan of conveyor. Furthermore, conveyor maintenance is essential as it may be subjected to different types of failures…