Press release

Australia Coal Market Projected to Reach 224.8 Million Tons During 2026-2034: IMARC Group

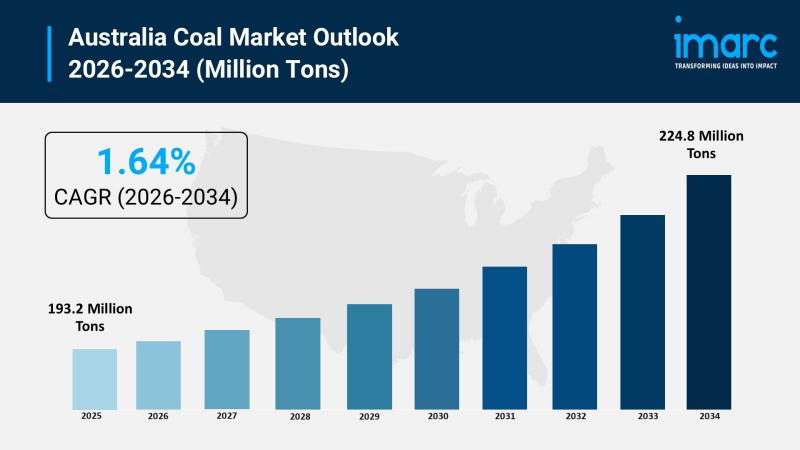

The Australia coal market reached a volume of 193.2 Million Tons in 2025. Looking forward, the market is expected to reach 224.8 Million Tons by 2034, exhibiting a growth rate (CAGR) of 1.64% during 2026-2034. The market encompasses bituminous coal, sub-bituminous coal, lignite coal, and anthracite coal produced through surface mining and underground mining technologies, serving power generation, steel, cement, residential and commercial, and other end-use industries across Australia Capital Territory and New South Wales, Victoria and Tasmania, Queensland, Northern Territory and Southern Australia, and Western Australia. Sustained Asian demand for high-quality metallurgical coal, India's expanding steel production capacity, strategic infrastructure investments in mining operations, Queensland and NSW production ramp-ups, and Australia's competitive positioning as a premium coal exporter to Asia-Pacific markets are among the key factors driving market growth throughout the forecast period.

Request for a sample report PDF: https://www.imarcgroup.com/australia-coal-market/requestsample

Australia Coal Market Summary:

• Australia's metallurgical coal exports are forecast to rise from 147 million metric tons in fiscal 2025 to approximately 152 million metric tons in fiscal 2026, driven by sustained steelmaking demand from India and Japan-reinforcing Australia's dominant position as the world's leading seaborne coking coal supplier with export earnings remaining resilient at AUD 36-37 billion annually.

• Coal remains New South Wales' number one export commodity, generating AUD 23.4 billion in export revenue and AUD 2.7 billion in royalties in 2025, with Japan (43%), China (27%), and Taiwan (10%) as the State's largest buyers-demonstrating the continued economic significance of coal mining to Australia's most populous state despite the broader energy transition narrative.

• Australia's total coal production is forecast to increase by 3.9% to 483.2 million tonnes in 2026, driven primarily by the continued ramp-up of the Maxwell Underground project in NSW and planned capacity increases at the Byerwen and Narrabri Underground mines-indicating active investment in expanding operational capacity despite long-term transition pressures.

• India has emerged as the critical growth market for Australian metallurgical coal, with Indian imports reaching record highs driven by capacity expansions at JSW Steel, Tata Steel, and JSPL-accounting for 29% of total Australian coal exports and offsetting declining volumes to advanced economies transitioning away from blast furnace steelmaking.

• Whitehaven Coal reported a 90-plus per cent increase in recoverable coal reserves at its Blackwater Mine in Queensland following an extensive drilling and modelling campaign, strengthening the company's long-term production outlook and underscoring continued investment in premium-quality metallurgical coal assets that serve steelmaking markets.

• The NSW Government released its Coal Industry 2026-50 policy in March 2026, announcing that the state will no longer accept applications for new greenfield coal mines while providing a framework for managed transition of existing operations-signaling regulatory clarity that enables long-term planning for current producers without expanding the mining footprint.

• Market segmentation covers four coal types (bituminous, sub-bituminous, lignite, anthracite), two mining technologies (surface mining, underground mining), five end-use industries (power generation, steel, cement, residential and commercial, others), and five regions (ACT and NSW, Victoria and Tasmania, Queensland, Northern Territory and Southern Australia, Western Australia).

Key Trends Shaping the Australia Coal Market:

• Metallurgical coal resilience amid energy transition: While thermal coal faces structural demand headwinds from renewable energy expansion, Australia's metallurgical coal sector is demonstrating remarkable resilience with export volumes forecast to grow from 147 to 152 million metric tons between fiscal 2025 and 2026. This divergence reflects the fundamental reality that steelmaking currently has no commercially viable alternative to coking coal at scale-green hydrogen-based direct reduced iron remains in pilot stages and cannot displace blast furnace production for decades. Australia's premium hard coking coal commands quality premiums that sustain profitability even as benchmark prices moderate, while the country's established logistics infrastructure, long-term supply contracts with Japanese and Korean steelmakers, and proximity to growing Indian demand create durable competitive advantages that differentiate metallurgical coal from the more vulnerable thermal segment.

• India's steel capacity expansion driving sustained import growth: India's ambitious steel production targets-aiming to reach 300 million tonnes annual capacity-are creating structural demand growth for Australian metallurgical coal that more than compensates for declining volumes to traditional markets like Japan and South Korea. Major Indian steelmakers including JSW Steel, Tata Steel, and JSPL are simultaneously expanding blast furnace capacity and increasing their reliance on premium Australian coking coal that delivers superior coke strength and lower ash content compared to alternatives from Mozambique, Russia, or domestic Indian sources. India now accounts for 29% of total Australian coal exports, with combined coking and pulverized coal injection imports reaching record monthly highs. This relationship positions Australia as the indispensable supplier to the world's fastest-growing major steel industry, providing demand visibility that underpins continued investment in Australian metallurgical coal mine development and infrastructure.

• Regulatory frameworks providing managed transition clarity: The NSW Government's Coal Industry 2026-50 policy released in March 2026-prohibiting new greenfield coal mines while supporting existing operations-represents an emerging regulatory approach that provides investment certainty for current producers without encouraging greenfield expansion. This policy framework enables mine operators to plan long-term production, invest in efficiency improvements, and manage workforce transitions with clear regulatory parameters rather than facing uncertain approval processes. Queensland continues to balance coal royalty revenue (a critical funding source for state services) against environmental commitments, while maintaining production support for metallurgical coal operations that serve steelmaking rather than power generation. This regulatory differentiation between thermal and metallurgical coal recognizes their distinct economic roles and transition timelines.

• Underground mining expansion and operational ramp-ups: Australia's coal production growth is increasingly driven by underground mining operations that offer lower surface disturbance and access to premium coal seams-with the Maxwell Underground project in NSW, Olive Downs Complex in Queensland (operational since June 2023), and Narrabri Underground expansion contributing to the forecast 3.9% production increase in 2026. Underground longwall mining technology delivers higher productivity per worker than traditional methods while accessing coal deposits beneath agricultural land without permanent surface disruption. Whitehaven Coal's 90%+ increase in recoverable reserves at Blackwater following advanced geological modelling demonstrates how technology investment is extending mine life and improving resource confidence without requiring new mine approvals-maximizing value from existing permitted operations.

• Workforce challenges and automation acceleration: Skill shortages in critical areas of mining engineering, drilling, heavy machinery operation, and geological services are constraining production ramp-ups across Queensland and NSW operations, with the talent gap expected to persist through 2026 and beyond. This labor market tightness is accelerating investment in automation, autonomous haulage systems, remote operations centers, and AI-driven maintenance optimization that reduces reliance on scarce specialized workers while improving safety and productivity. Mining companies are simultaneously investing in workforce attraction programs, FIFO arrangements, and regional community development to compete for available talent-but the structural shortage is fundamentally shifting the industry toward technology-intensive operations that require fewer but more highly skilled workers per tonne of coal produced.

Market Growth Drivers:

Sustained Asian Steelmaking Demand for Premium Metallurgical Coal

Australia's position as the world's dominant seaborne metallurgical coal supplier is underpinned by sustained demand from Asia's steel industry, where blast furnace production continues to expand in India and maintains substantial volumes in Japan, South Korea, and Southeast Asia. The quality premium commanded by Australian hard coking coal-characterized by high coke strength, low ash content, and consistent specifications-makes it the preferred feedstock for steelmakers producing high-grade structural steel, automotive sheet, and infrastructure materials. India's steel capacity expansion programs at JSW Steel, Tata Steel, and JSPL are creating incremental demand that directly benefits Australian exporters, with Indian imports reaching record monthly volumes and accounting for 29% of total Australian coal exports. This demand is structural rather than cyclical-India's urbanization, infrastructure development, and manufacturing growth require steel production expansion for decades, and blast furnace technology remains the dominant production route where coking coal quality directly determines output efficiency and product quality.

Strategic Infrastructure and Production Capacity Investments

Australian coal producers are investing in operational expansion and efficiency improvements that increase production capacity from existing permitted mining areas-with total output forecast to grow 3.9% to 483.2 million tonnes in 2026. The Maxwell Underground project ramp-up, Byerwen capacity increases, Narrabri Underground expansion, and continued development of the Olive Downs Complex represent billions in capital investment that will deliver production growth over the coming years. Whitehaven Coal's acquisition of BHP's Blackwater and Daunia mines and subsequent discovery of 90%+ additional recoverable reserves demonstrates consolidation-driven growth where experienced operators apply advanced geological techniques to maximize resource extraction from established mining districts. Rail and port infrastructure investments-particularly in the Hunter Valley and Queensland's Bowen Basin export corridors-ensure that production growth can reach export markets without logistics bottlenecks, maintaining Australia's reputation for reliable supply that underpins long-term offtake agreements with Asian buyers.

Competitive Cost Position and Geographic Proximity to Growth Markets

Australia's competitive advantages in coal supply extend beyond resource quality to encompass geographic proximity to the world's largest and fastest-growing coal import markets, established logistics infrastructure connecting mines to deep-water export terminals, and institutional stability that provides contract certainty for buyers requiring reliable long-term supply. Shipping distances from Queensland and NSW ports to Japan, South Korea, India, and Southeast Asia are substantially shorter than competing supply from the Americas, Russia, or Southern Africa-delivering cost advantages in freight that improve landed pricing competitiveness. Australia's coal export infrastructure-including the world's largest coal export terminal at Newcastle and purpose-built facilities at Gladstone, Hay Point, and Dalrymple Bay-provides the throughput capacity and vessel-loading efficiency that enable reliable just-in-time delivery schedules demanded by Asian steelmakers operating with minimal stockpile buffers. This infrastructure advantage compounds over time as competing regions face higher capital requirements to develop equivalent export capacity.

Browse the full report with TOC and list of figures: https://www.imarcgroup.com/australia-coal-market

How AI is Reshaping the Australia Coal Market:

• AI-powered predictive maintenance reducing equipment downtime: Machine learning systems are monitoring real-time sensor data from draglines, longwall shearers, continuous miners, and haul trucks to predict component failures before they cause unplanned stoppages-with BHP moving beyond pilot-stage AI deployment to daily operational integration across coal operations, enabling condition-based maintenance that extends equipment life, reduces repair costs, and maintains production continuity in operations where a single dragline breakdown can cost millions in lost output per day.

• AI-driven coal handling and preparation plant optimization: Artificial intelligence is transforming coal handling and preparation plant (CHPP) operations in Australia through real-time Asset Health Intelligence systems that replace time-based preventive maintenance with predictive analytics-monitoring vibration signatures, temperature profiles, and throughput variations across crushers, screens, dense medium cyclones, and conveyor systems to optimize processing efficiency, maximize coal recovery, minimize product quality variation, and reduce unscheduled maintenance interventions that disrupt mine-to-port logistics chains.

• Autonomous haulage and drilling systems improving productivity: AI-controlled autonomous haul trucks and drilling rigs are operating across Australian coal mines, removing operators from hazardous environments while delivering consistent 24-hour productivity improvements through optimized route planning, fuel-efficient speed management, and elimination of shift-change downtime-addressing critical workforce shortages in remote mining locations where up to 60% of Australian mines are projected to implement AI-powered autonomous solutions.

• AI-enhanced geological modelling and resource estimation: Machine learning algorithms are processing drilling data, geophysical surveys, and historical production records to create more accurate three-dimensional geological models that improve resource estimation confidence-as demonstrated by Whitehaven Coal's 90%+ reserve increase at Blackwater following AI-assisted modelling campaigns that identified commercially recoverable coal seams previously overlooked by conventional geological interpretation methods.

• AI-based emissions monitoring and environmental compliance: Artificial intelligence platforms are enabling real-time monitoring of methane emissions, dust dispersion, water quality, and rehabilitation progress across Australian coal mining operations-with the NSW Government approving AI-integrated technology at Illawarra Coal's Bulli Seam Operations that slashes emissions while supporting operational continuity, helping producers meet increasingly stringent environmental reporting requirements and demonstrating responsible resource extraction that maintains social license to operate.

Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Australia coal market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on type, mining technology, end use industry, and region.

By Type:

• Bituminous Coal

• Sub-Bituminous Coal

• Lignite Coal

• Anthracite Coal

By Mining Technology:

• Surface Mining

• Underground Mining

By End Use Industry:

• Power Generation

• Steel

• Cement

• Residential and Commercial

• Others

By Region:

• Australia Capital Territory and New South Wales

• Victoria and Tasmania

• Queensland

• Northern Territory and Southern Australia

• Western Australia

Key Players:

The Australia coal market features a competitive landscape comprising multinational mining conglomerates, domestic coal producers, diversified resource companies, and specialized metallurgical coal operators. The market research report provides a comprehensive analysis of the competitive landscape including key player positioning, market structure, top winning strategies, competitive dashboards, and detailed company profiles. Some of the major players include Stanmore Resources, South32 Ltd, Golden Energy and Resources Pte Ltd, M Resources Pty Ltd, Whitehaven Coal, BHP, Glencore, Anglo American, Yancoal Australia, Peabody Energy, and other domestic and international participants competing across bituminous, sub-bituminous, lignite, and anthracite coal production throughout Australia.

Key Aspects Required for the Australia Coal Market:

• Demand encompasses Asian steelmakers requiring premium metallurgical coal for blast furnace operations, domestic and international power generators utilizing thermal coal, cement manufacturers needing consistent calorific value fuel, and industrial consumers across the Asia-Pacific region served by Australia's established export infrastructure connecting Bowen Basin, Hunter Valley, and other mining districts to deep-water port terminals.

• India's position as Australia's largest coal export destination (29% of total exports) with record monthly import volumes driven by JSW Steel, Tata Steel, and JSPL capacity expansions creates structural demand growth that underpins mine investment decisions and long-term production planning across Queensland and NSW operations.

• The distinction between metallurgical coal (export earnings resilient at AUD 36-37 billion) and thermal coal (earnings declining from AUD 32 billion to AUD 27 billion by 2026-27) requires differentiated strategy approaches recognizing that coking coal demand is tied to steel production growth while thermal coal faces structural competition from renewable energy expansion in importing nations.

• Regulatory evolution including NSW's Coal Industry 2026-50 policy (no new greenfield mines) and Queensland's royalty regime creates a policy environment where growth must come from existing permitted operations, brownfield expansions, and resource optimization rather than new mining area approvals-favoring established operators with large resource bases and advanced geological knowledge.

• Workforce shortages in mining engineering, drilling, heavy machinery, and geological services are constraining production ramp-ups and accelerating automation investment-requiring companies to balance technology deployment, workforce attraction, FIFO logistics, and regional community development to maintain operational capacity in competitive labor markets.

• The competitive landscape features consolidation activity (Whitehaven acquiring BHP's Queensland assets, Argo Queensland consortium acquiring Fitzroy Resources) that concentrates production among fewer, larger operators with the scale and financial capacity to invest in automation, geological exploration, and long-term mine planning required to maintain competitiveness through the energy transition period.

Recent News and Developments:

March 2026: The NSW Government released its Coal Industry 2026-2050 policy, announcing that New South Wales will no longer accept applications for new greenfield coal mines while establishing a long-term transition framework for existing operations through 2050. The policy provided regulatory clarity for the state's coal sector, which generated approximately AUD 23.4 billion in export revenue during 2025.

February 2026: Australia's total coal production was projected to increase by approximately 3.9% to 483.2 million tonnes, driven mainly by the continued ramp-up of the Maxwell Underground project and planned capacity expansions at the Byerwen and Narrabri Underground mines. The increase highlighted continued production growth from existing operations despite the broader energy transition environment.

November 2025: Whitehaven Coal announced that recoverable coal reserves at its Blackwater Mine in Queensland had increased by more than 90% following an extensive drilling and geological modelling campaign. The reserve expansion significantly strengthened the long-term production outlook for one of Australia's major metallurgical coal operations acquired from BHP.

October 2025: Argo Queensland, backed by a consortium of European and Japanese investors, acquired a 70% stake in Fitzroy Australia Resources. The transaction reflected continued international investment confidence in Australian metallurgical coal assets despite increasing global focus on energy transition policies.

September 2025: The NSW Government approved a major modification at Illawarra Coal's Bulli Seam Operations mine, introducing AI-integrated methane reduction technology designed to lower emissions while maintaining production and supporting local employment. The project highlighted growing use of advanced technologies to improve operational sustainability in the coal industry.

December 2025: Australia's metallurgical coal exports were estimated to rise from approximately 147 million metric tons in fiscal 2025 to 152 million metric tons in fiscal 2026, according to the federal government's Resources and Energy Quarterly report. Export earnings were expected to remain resilient at around AUD 36-37 billion, supported by continued global steel production demand.

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Speak to an analyst for a customized sample report PDF: https://www.imarcgroup.com/request?type=report&id=24687&flag=C

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel. No.: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Australia Coal Market Projected to Reach 224.8 Million Tons During 2026-2034: IMARC Group here

News-ID: 4504544 • Views: …

More Releases from IMARC Group

Australia Wind Energy Market 2026 | Anticipated to Reach USD 7,256.3 Million by …

Australia Wind Energy Market Overview:

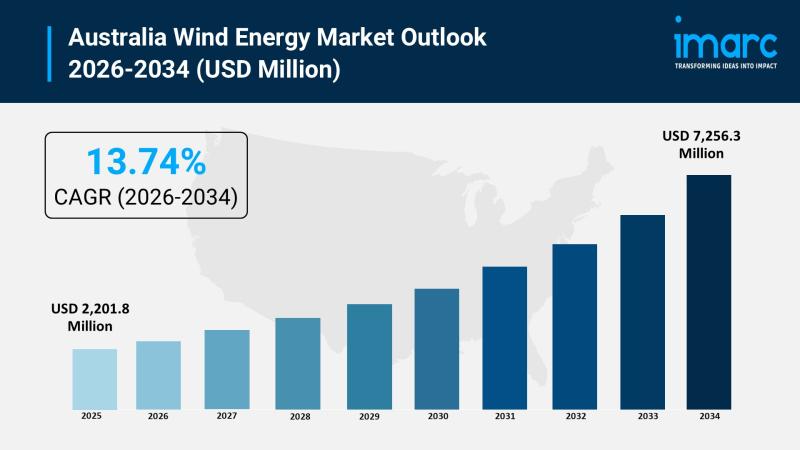

The Australia wind energy market size reached USD 2,201.8 Million in 2025. Looking forward, the market is expected to reach USD 7,256.3 Million by 2034, exhibiting a growth rate (CAGR) of 13.74% during 2026-2034. The market encompasses turbines, support structures, electrical infrastructure, and other components across offshore and onshore installations with horizontal axis and vertical axis turbine types, serving utility, industrial, commercial, and residential applications in…

Australia Smart Microgrids Market 2026 | Worth USD 2,170.7 Million by 2034 | CAG …

Australia Smart Microgrids Market Overview:

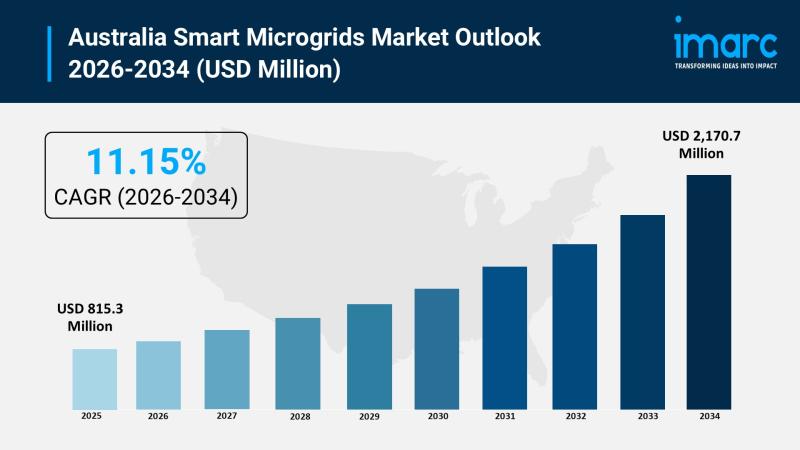

The Australia smart microgrids market size reached USD 815.3 Million in 2025. Looking forward, the market is expected to reach USD 2,170.7 Million by 2034, exhibiting a growth rate (CAGR) of 11.15% during 2026-2034. The market encompasses hybrid, off-grid, and grid-connected microgrids integrating storage and inverter components with fuel cell and CHP power technologies, serving urban and rural consumers across campus, commercial, and defense applications in…

Saudi Arabia Online Travel Market Size to Hit USD 13.0 Billion by 2034, CAGR is …

Saudi Arabia Online Travel Market Overview

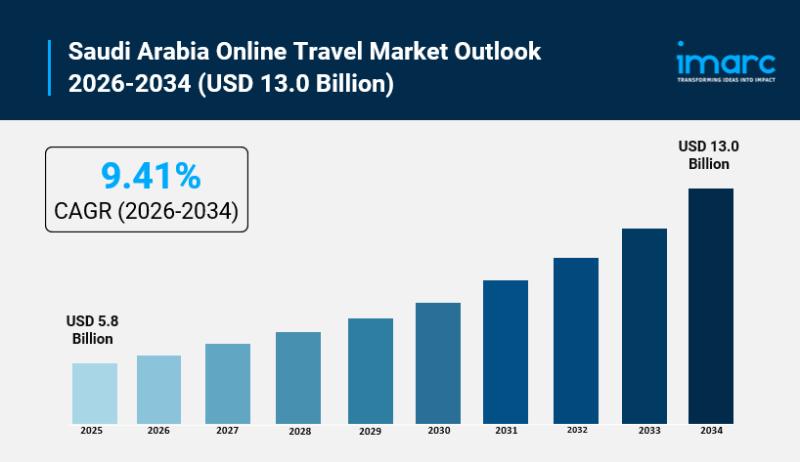

Market Size in 2025: USD 5.8 Billion

Market Forecast in 2034: USD 13.0 Billion

Market Growth Rate 2026-2034: 9.41%

According to IMARC Group's latest research publication, "Saudi Arabia Online Travel Market Size, Share, Trends and Forecast by Service Type, Platform, Mode of Booking, Age Group, and Region, 2026-2034", The Saudi Arabia online travel market size reached USD 5.8 Billion in 2025. Looking forward, IMARC Group expects the market…

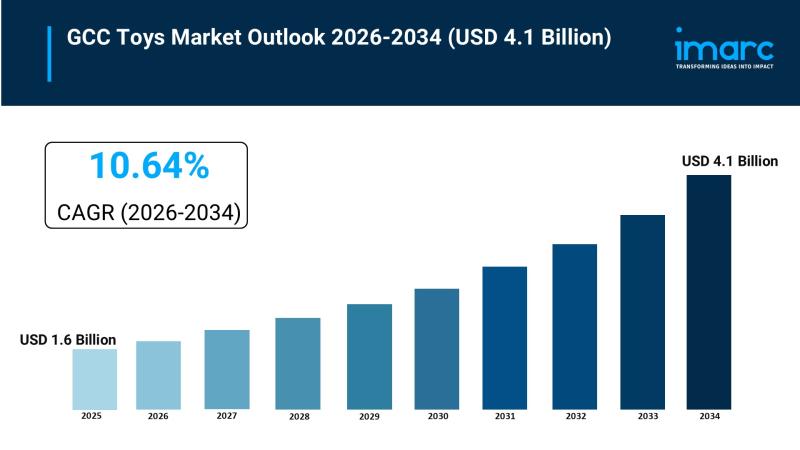

GCC Toys Market Size To Worth USD 4.1 Billion in 2034 | Grow CAGR by 10.64%

GCC Toys Market Overview

Market Size in 2025: USD 1.6 Billion

Market Size in 2034: USD 4.1 Billion

Market Growth Rate 2026-2034: 10.64%

According to IMARC Group's latest research publication, "GCC Toys Market Report by Product Type, Age Group, Sales Channel, and Country, 2026-2034," the GCC toys market size was valued at USD 1.6 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 4.1 Billion by 2034, exhibiting a CAGR…

More Releases for Australia

Derila Memory foam pillow Australia: Honest Reviews About Derila Australia

Derila is one of the best memory foam pillows sold in Australia today.

Priced at around 30 dollars (USD), derila is currently the most reviewed and the cheapest memory pillow available in Australia.

What is Derila? Is Derila Pillow the best in Australia? Keep reading to discover everything worth knowing about Derila Australia.

OVERVIEW

Recently, Memory foam pillow has been trending and there is a lot of brands to choose from. Which one is…

CeraCare Australia - Where to Buy Legit CeraCare Supplement in Australia?

CeraCare Australia - Ceracare is a glucose support supplement that proposes to augment cardiovascular prosperity and to stay aware of perfect glucose assimilation in Australia. CeraCare supplement is conceptualized and executed by a threesome – Christine, Dr. Jihn and Michael. It is a natural supplement that helps one stay aware of ideal glucose levels, cardiovascular prosperity, and glucose assimilation.

Take Advantage of 80% Discount Offer in Australia >> https://boostsxproaustralia.com/ceracare-new

The indications…

Glucofort Australia - Where to Buy Legit Glucofort Supplement in Australia?

Glucofort Australia - Glucofort is an efficient, all-natural progressive glucose support supplement in Australia. This formula is made out of 12 key ingredients, 7 nutrients, and minerals, and a little of Vanadium. This supplement upholds regulated glucose levels and glucose digestion. Glucofort prides itself as the most inventive supplements available in Oceania, accentuating its solidarity, wellbeing, and quality.

Take Advantage of 75% Discount Offer in Australia >> https://boostsxproaustralia.com/glucofort-new

Rather than simply…

Australia Agriculture Market, Australia Agriculture Industry, Australia Agricult …

Australia Agriculture has been as vital within the development of Australia, because it was within the United States. Australia's ancient dominance in wheat and sheep continues into the 21st century. Recently Australian agriculture has become more and more diversified. The considerable expanses of productive land have helped Australia to become a number one world exporter of grains, meats, and wool. Each grains (predominantly wheat and barley) and wool markets round…

Australia Conveyor Maintenance Analysis by Top Companies Habasit Australia Pty l …

Global Australia Conveyor Maintenance Market and Competitive Analysis

Know your current market situation! Not only a vital element for brand new products but also for current products given the ever-changing market dynamics. The study allows marketers to remain involved with current consumer trends and segments where they'll face a rapid market share drop. Discover who you actually compete against within the marketplace, with Market Share Analysis know market position, to push…

Australia Conveyor Maintenance Market Analysis By Manufacturers Rema Tip Top Aus …

A conveyor system is a common piece of mechanical handling device that moves materials/objects from one location. A conveyor is often lifeline to a company’s ability to effectively move its products in a timely manner. While it is used constantly in a manufacturing plant, proper maintenance from trained technicians can extend the lifespan of conveyor. Furthermore, conveyor maintenance is essential as it may be subjected to different types of failures…