Press release

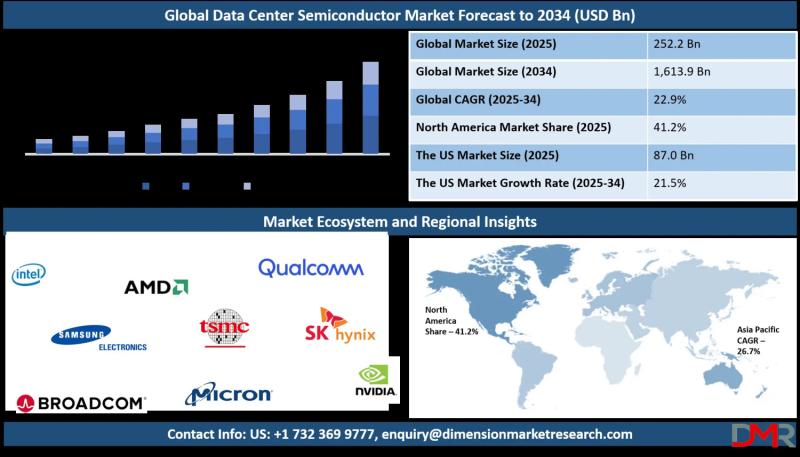

Data Center Semiconductor Market to Surge from 252.2 billion in 2025 to 1.6 Trillion by 2034 as AI Workloads and Heterogeneous Compute Reshape Infrastructure

Data Center Semiconductor Market Size, Share, Trends & Outlook Report 2034

Data center semiconductors-encompassing processors, memory, storage controllers, networking chips, and power management ICs-are the foundational enablers of modern digital infrastructure. According to Dimension Market Research, the U.S. market alone is projected to reach USD 87.0 billion in 2025 and grow to USD 560.0 billion by 2034 at a CAGR of 21.5% , driven by the CHIPS Act's support for domestic advanced-node manufacturing and aggressive investment by hyperscale cloud providers. With Japan's market growing at 23.3% (reaching USD 15.1 billion in 2025) and Europe at 20.2% (USD 55.5 billion), the sector is witnessing a global acceleration that positions semiconductors as the critical bottleneck-and opportunity-in the AI-driven computing era.

📄 Get Your Sample Report Today → https://dimensionmarketresearch.com/request-sample/data-center-semiconductor-market/

🔷 The News Angle: The AI Workload Revolution-From CPU-Centric to Heterogeneous Compute

The dominant narrative reshaping the data center semiconductor market is the fundamental transition from traditional CPU-centric architectures to heterogeneous compute systems that integrate GPUs, ASICs, FPGAs, and AI-specific accelerators for dramatically higher efficiency. This shift is not incremental-it represents a complete re-architecting of how data centers are designed, built, and operated.

AI workload expansion is the primary catalyst. The explosion of generative AI, deep learning, and large-scale inference/training workloads is forcing data centers to upgrade semiconductor architectures at an unprecedented pace. High-performance GPUs, ASICs, and accelerators are increasingly required for parallel compute, pushing demand for semiconductors optimized for throughput, bandwidth, and power efficiency. As software models grow larger and more complex-with large language models now exceeding trillions of parameters-hardware must evolve rapidly, driving semiconductor adoption across compute, memory, and networking domains.

Memory bandwidth bottlenecks are creating parallel opportunities. AI workloads are increasingly memory-bound rather than compute-bound, pushing adoption of high-bandwidth memory (HBM) and memory-centric semiconductor architectures. According to the report, DRAM remains essential for in-memory processing and high-throughput environments like analytics and AI, while HBM is gaining rapid traction for AI/ML workloads that require simultaneous high-speed data streams. Persistent memory innovations are enabling hybrid solutions bridging DRAM and storage, enhancing performance in caching, edge compute, and real-time data analytics.

Architectural innovation is accelerating beyond legacy server designs. Traditional CPU-centric architectures are giving way to heterogeneous systems incorporating GPUs, FPGAs, ASICs, and AI-specific accelerators for higher efficiency in data center workloads-particularly AI. Advanced packaging (3D stacking, chiplets, integrated interposers) is becoming mainstream, enabling faster deployment of highly customized semiconductor modules for AI clusters and high-density racks. Emerging architectures such as CXL (Compute Express Link), memory pooling, photonic interconnects, and modular data center racks are creating opportunities for new semiconductor solutions across memory, networking, and power domains.

🔷 Key Insights: Data Points Defining the Semiconductor Revolution

North America Leads (41.2% Share in 2025): Major hyperscale cloud providers, AI research hubs, advanced semiconductor firms, and CHIPS Act support drive regional dominance.

Processors Dominate Component Type (43.5% Share): CPUs for general-purpose compute, GPUs for parallel workloads, ASICs for AI inference, and FPGAs for workload flexibility remain indispensable.

Compute Leads Function (46.2% Share): AI model training, big data analytics, and virtualized computing drive massive investment in scalable compute infrastructures.

14nm Node Leads Technology Node (41.8% Share): Maturity, reliability, and cost-effectiveness for mainstream server components make 14nm optimal for I/O-heavy and general-purpose processing.

Hyperscale Data Centers Lead Application (48.9% Share): Massive facilities operated by tech giants and cloud providers require continuous upgrades in processing, memory, storage, and networking.

Memory Fastest-Growing Component: DRAM, NAND Flash, HBM, and persistent memory innovation driven by exponential data growth and AI model size expansion.

Networking Fastest-Growing Function: 200G/400G Ethernet, InfiniBand for HPC, and smart NICs address data movement demands between compute nodes and storage units.

Sub-7nm Nodes Fastest-Growing Technology Segment: AI accelerators, high-performance GPUs, and custom ASICs increasingly designed at advanced nodes for superior performance-per-watt.

Cloud Service Providers Fastest-Growing Application: Digital transformation and shift toward scalable, on-demand infrastructure drive demand for flexible, modular semiconductor solutions.

🔷 Market Dynamics: Drivers, Restraints, and Strategic Opportunities

Drivers: AI Workload Expansion & Cloud Infrastructure Growth

The primary driver is the explosion of generative AI, deep learning, and large-scale inference/training workloads. High-performance GPUs, ASICs, and accelerators are increasingly required for parallel compute, pushing demand for semiconductors optimized for throughput, bandwidth, and power efficiency. As software models grow larger and more complex, hardware must evolve rapidly, driving semiconductor adoption across compute, memory, and networking.

Simultaneously, the expansion of hyperscale cloud data centers, along with the growing importance of edge computing and distributed data center footprints, is prompting operators to deploy more advanced semiconductors to manage latency, interconnect, power density, and scalability. Telecom, IoT, and mobile workloads expanding into edge nodes further amplify demand for data center-grade semiconductors outside conventional facilities.

Restraints: Node Migration Complexity & Supply Chain Constraints

Despite momentum, significant barriers remain. Advanced process nodes and packaging techniques (3D stacking, chiplets) are required to deliver next-generation performance and efficiency. However, migrating to sub-7nm or advanced packaging increases cost, development time, and supply chain risk, hampering adoption for all but the largest players.

Additionally, the semiconductor ecosystem is subject to constrained foundry capacity, export controls, and regionalization pressures. These factors affect availability of high-end chips-especially GPUs and accelerators-for data centers, delaying roll-out and increasing cost.

Opportunities: Specialized Accelerators & Memory/Compute Disaggregation

As operators seek efficiency gains and differentiation, the design and deployment of ASICs and disaggregated accelerator chips tailored to workloads (inference, memory bandwidth) represent significant growth opportunities for chipset vendors. Domain-specific chips optimized for TOPS-per-watt in data centers are increasingly attractive.

Emerging architectures such as CXL, memory pooling, HBM, photonic interconnects, and modular data center racks create opportunities for new semiconductor solutions across memory, networking, and power domains. Chiplet architectures and advanced packaging allow for modular, high-bandwidth designs central to supporting energy-aware computing at scale.

📄 Get the Insights You Need to Drive Real Impact → https://dimensionmarketresearch.com/request-sample/data-center-semiconductor-market/

🔷 Selective Segmentation: Where the Growth is Concentrated

By Component Type (Processors-43.5% Share): Processors account for the largest share, reflecting their indispensable role in powering compute-intensive operations. The category includes CPUs for general-purpose compute, GPUs for parallel workloads, ASICs for specialized tasks like AI inference, and FPGAs for workload flexibility. Hyperscale and enterprise data centers rely on these chips to handle cloud services, AI training, virtualization, and container orchestration. Processor innovation is driven by advanced packaging and chiplet designs, enabling modular scalability. Memory is the fastest-growing segment, driven by data explosion and demand for higher storage speed and lower latency. DRAM, NAND Flash, and HBM are critical for AI/ML workloads requiring high-speed data streams.

By Function (Compute-46.2% Share): Compute leads, encompassing processors and memory elements that execute and support critical workloads including AI model training, big data analytics, and virtualized computing. Data centers invest heavily in scalable compute infrastructures with emphasis on high-performance processors and tightly integrated memory systems. AI and HPC workloads require massive parallel processing, fueling demand for CPUs, GPUs, and custom accelerators. The transition to heterogeneous compute environments-where multiple processor types work in tandem-is reshaping how compute functions are fulfilled. Networking is the fastest-growing function, powered by increasing demand for data movement between compute nodes, storage units, and cloud edges. Deployment of 200G/400G Ethernet, InfiniBand for HPC environments, and smart NICs for offloading network functions addresses bottlenecks and latency.

By Technology Node (14nm-41.8% Share): The 14nm node leads due to its maturity, reliability, and cost-effectiveness for mainstream server components. Many CPUs, controllers, analog ICs, and networking chips continue to be manufactured on this node, balancing performance and yield stability. While not suitable for the most advanced AI chips, 14nm remains optimal for I/O-heavy and general-purpose processing tasks. The well-established design ecosystem allows faster time-to-market. Sub-7nm nodes are the fastest-growing segment as demand intensifies for more powerful and energy-efficient chips. AI accelerators, high-performance GPUs, and custom ASICs for data center use are increasingly designed at these advanced nodes, delivering significantly higher transistor density, better performance-per-watt, and superior integration capabilities.

By Application (Hyperscale Data Centers-48.9% Share): Hyperscale data centers dominate semiconductor demand, operated by tech giants and cloud providers requiring continuous upgrades in processing, memory, storage, and networking capabilities. From hosting AI applications to running SaaS platforms, hyperscale environments demand the highest density, speed, and energy efficiency, consuming large volumes of CPUs, GPUs, memory modules, smart NICs, and power-efficient chips. Custom silicon development allows hyperscalers to optimize infrastructure for proprietary workloads. Cloud Service Providers (CSPs) are the fastest-growing category, driven by rapid digital transformation and shift toward scalable, on-demand infrastructure. CSPs require flexible, modular, cost-efficient semiconductor solutions supporting diverse workloads from simple web hosting to complex AI model deployment, with AI-as-a-Service (AIaaS) boosting demand for accelerators and HBM components.

🔷 Regional Analysis: North America Leads, Asia-Pacific Emerges as Fastest-Growing

North America (41.2% Revenue Share in 2025): North America stands as the leading region, anchored by major hyperscale cloud providers, AI research hubs, and advanced semiconductor firms. The region hosts some of the world's largest data centers operated by cloud and tech giants, driving continuous investment in cutting-edge chips for compute, memory, networking, and storage. North American data centers are among the first to adopt AI accelerators, sub-7nm processors, and custom-designed silicon tailored for specific workloads. Government support for domestic semiconductor manufacturing-including the CHIPS Act-and research initiatives further strengthens the region's ecosystem. Early adoption of edge computing, hybrid cloud models, and modular data centers fuels consistent demand across all semiconductor functions.

The U.S. Market (USD 87.0 billion in 2025, 21.5% CAGR): The U.S. market continues to lead in data center semiconductor development and infrastructure build-out. Advanced-node manufacturing (chips sub-7nm) is receiving strong investment and policy support, making the U.S. a key base for next-generation processors and accelerators tailored to AI/data center workloads. Domestic firms and foundries are ramping power-and-analog semiconductor solutions, recognizing that compute density and power constraints are increasingly critical. Hyperscale cloud providers and AI infrastructure operators are investing heavily in both chips and facility upgrades, accelerating hardware refresh cycles. The CHIPS Act further supports semiconductor supply chain localization.

Asia-Pacific (Fastest-Growing Region): Asia Pacific is the fastest-growing region, driven by rapid digital transformation, rising cloud adoption, and increasing investments in hyperscale and telecom data centers. China, India, South Korea, and Singapore are expanding data infrastructure to meet growing demand from AI services, 5G, and data localization policies. This regional expansion is prompting aggressive deployment of advanced processors, memory technologies, and networking silicon across both cloud-native and enterprise facilities. The region benefits from a strong semiconductor manufacturing base, positioning it to scale production of both mature and advanced node chips. Japan's market is growing at 23.3% CAGR, with government collaboration between industry and infrastructure players as a key strength, alongside development of data centers using renewable energy and high-efficiency power/analog devices.

Europe (USD 55.5 billion in 2025, 20.2% CAGR): Europe's semiconductor-data-center ecosystem is evolving under a dual constraint: strong regulatory and sustainability frameworks combined with rising demand for high-performance infrastructure. European governments and the EU are committing major funds to build AI data centers and support semiconductor manufacturing capacity. While traditional European strength in automotive and industrial semiconductors remains, the shift to data-center-grade processors, memory, and networking chips is gaining pace. Regulatory support, infrastructure development, and cross-border collaboration among EU member states are accelerating projects.

📄 Get the Full Premium Report Now- https://dimensionmarketresearch.com/checkout/data-center-semiconductor-market/

🔷 Competitive Landscape: Processor Giants, Memory Leaders, and Accelerator Specialists

The competitive landscape is characterized by major manufacturers of processors, memory, and networking semiconductors, as well as niche accelerator and power/analog suppliers.

Processor and Accelerator Leaders: Intel Corporation, Advanced Micro Devices (AMD), NVIDIA Corporation, and Arm Holdings plc dominate the compute segment. NVIDIA's collaboration with TSMC on the "Blackwell" AI chip wafer manufactured in the United States (October 2025) marks a milestone in onshore advanced-node production, reinforcing the alignment of AI, data center acceleration, and domestic manufacturing. AMD continues to gain share in server CPUs and GPUs for AI workloads.

Memory and Storage Giants: Samsung Electronics Co., Ltd., Micron Technology, Inc., SK hynix Inc., Western Digital Corporation, Kioxia Corporation, and Seagate Technology Holdings plc lead in DRAM, NAND Flash, HBM, and storage controllers. Memory is the fastest-growing segment, driven by AI's insatiable demand for bandwidth.

Networking and Connectivity Specialists: Broadcom Inc., Marvell Technology, Inc., and Qualcomm Technologies Inc. dominate networking chips, smart NICs, and interconnect solutions critical for distributed computing environments.

Foundry and Manufacturing: Taiwan Semiconductor Manufacturing Company (TSMC) remains the critical enabler of advanced-node production, with GlobalFoundries announcing raised investment plans (June 2025) to support emerging technologies including advanced packaging and silicon photonics.

Analog, Power, and Embedded Leaders: Texas Instruments Incorporated, Infineon Technologies AG, Analog Devices, Inc., NXP Semiconductors N.V., Microchip Technology Inc., and Renesas Electronics Corporation provide essential power management ICs and analog/mixed-signal semiconductors for data center infrastructure.

Recent Developments Highlighting Market Momentum:

October 2025: NVIDIA and TSMC unveiled the first "Blackwell" AI chip wafer manufactured in the United States, marking a milestone in onshore advanced-node production.

June 2025: GlobalFoundries announced a raised investment plan (capex and R&D) to support emerging semiconductor technologies critical for data center infrastructure, including advanced packaging and silicon photonics.

🔷 The Road Ahead: What Decision-Makers Need to Know

For B2B decision-makers-chief technology officers, data center architects, semiconductor procurement leaders, investors, and infrastructure strategists-the strategic imperative is unequivocal: the data center semiconductor market is the critical bottleneck and opportunity in the AI-driven computing era. The 22.9% CAGR reflects not incremental growth but a fundamental restructuring of how compute, memory, and networking resources are architected.

Key strategic imperatives include:

Prioritize heterogeneous compute architectures. Traditional CPU-centric designs are obsolete for AI workloads. Investment must span GPUs, ASICs, accelerators, and custom silicon.

Address memory bandwidth as a first-order constraint. AI models are increasingly memory-bound. HBM, persistent memory, and memory pooling technologies are strategic differentiators.

Accelerate adoption of sub-7nm nodes for AI inference and training. While 14nm remains optimal for general-purpose workloads, performance-per-watt advantages at advanced nodes justify the investment for AI-focused infrastructure.

Plan for continued supply chain constraints. Geopolitical tensions, export controls, and foundry capacity limitations will persist. Diversification and long-term supply agreements are essential.

Leverage the CHIPS Act and regional incentives. For U.S. and European operators, government support for domestic semiconductor manufacturing and R&D provides strategic and financial advantages.

The full report from Dimension Market Research provides granular segmentation by component type (processors-CPUs, GPUs, ASICs, FPGAs-memory, storage controllers, networking chips, power management ICs, analog & mixed-signal semiconductors), function (compute, storage, networking, power management, security), technology node (sub-7nm, 7nm-14nm, 14nm), application (hyperscale data centers, enterprise data centers, cloud service providers, telecom data centers), and 20+ regional markets, offering actionable intelligence for strategic planning.

📄 Explore the Report with TOC → https://dimensionmarketresearch.com/report/data-center-semiconductor-market/

For Sales or Inquiries, Contact

Robert John

957 Route 33, Suite 12 #308 Hamilton Square, NJ-08690 USA

Email: enquiry@dimensionmarketresearch.com

United States: (+1 732 369 9777)

Tel No: +91 88267 74855

Dimension Market Research (DMR) is a market research and consulting firm based in India & US, with its headquarters located in the USA. The company believes in providing the best and most valuable data to its customers using the best resources and analysts to work on, to create unmatchable insights into the industries and markets while offering in-depth results of over 30 industries, and all major regions across the world. We also believe that our clients don't always want what they see, so we provide customized reports as well, as per their specific requirements, to create the best possible outcomes for them and enhance their business through our data and insights in every possible way.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Data Center Semiconductor Market to Surge from 252.2 billion in 2025 to 1.6 Trillion by 2034 as AI Workloads and Heterogeneous Compute Reshape Infrastructure here

News-ID: 4502432 • Views: …

More Releases from Dimension Market Research

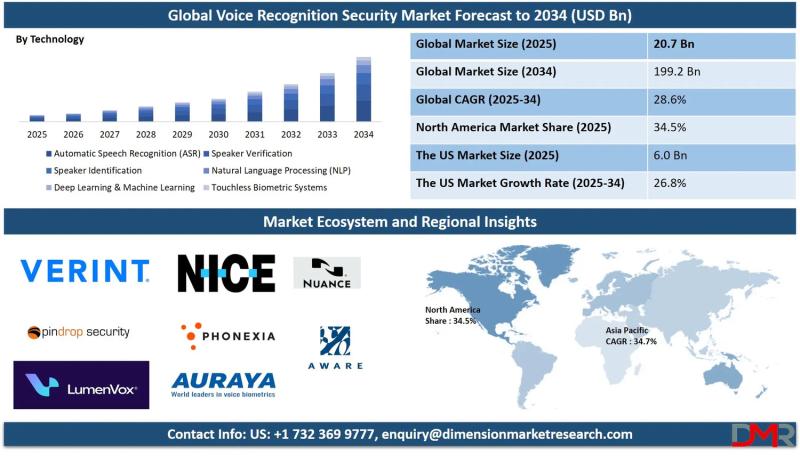

Voice Recognition Security Market to Surge from 20.7 billion in 2025 to 199.2 Bi …

The global Voice Recognition Security Market is poised for explosive growth, with market valuation projected to surge from an estimated USD 20.7 billion in 2025 to USD 199.2 billion by 2034, registering a remarkable compound annual growth rate (CAGR) of 28.6%. According to Dimension Market Research, this extraordinary expansion is being driven by three converging forces: escalating cyber threats and identity fraud across BFSI and telecommunications, the post-pandemic surge in…

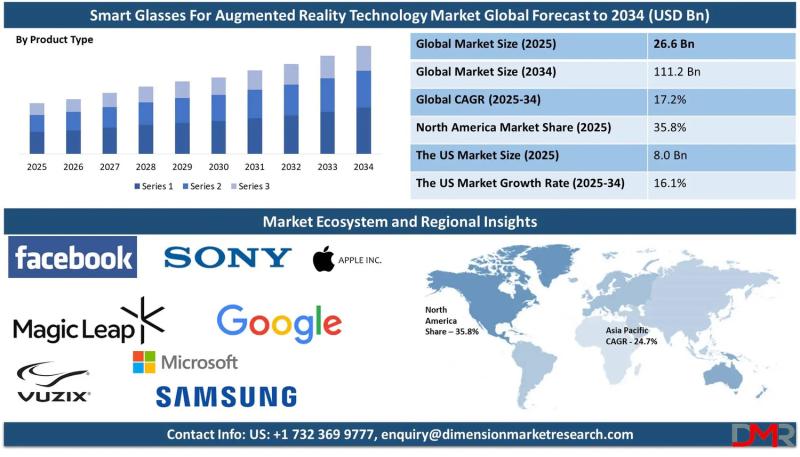

Smart Glasses for Augmented Reality Market to Reach $111.2 Billion by 2034 as En …

The global Smart Glasses for Augmented Reality (AR) Technology market is poised for remarkable growth, with market valuation projected to surge from an estimated USD 26.6 billion in 2025 to USD 111.2 billion by 2034, registering a strong compound annual growth rate (CAGR) of 17.2%. According to Dimension Market Research, this expansion is being driven by three transformative forces: rapid advancements in microdisplay and waveguide optics, surging enterprise adoption across…

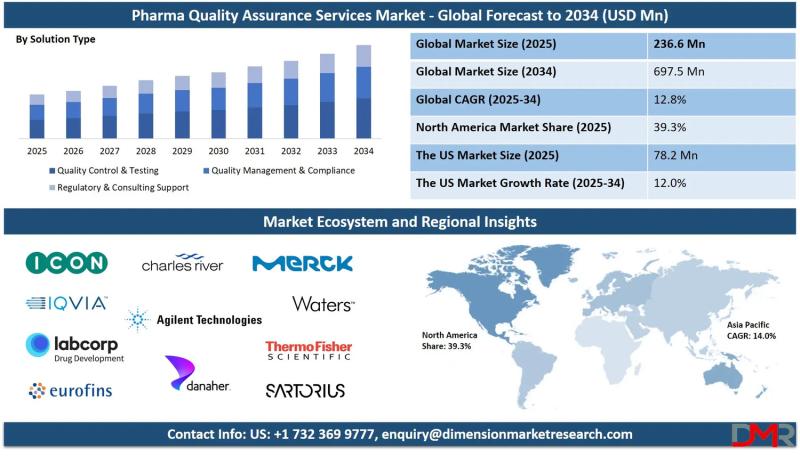

Pharma Quality Assurance Services Market to Reach $697.5 Million by 2034 as Drug …

The global Pharma Quality Assurance Services Market is on a steady growth trajectory, with market valuation projected to rise from an estimated USD 236.6 million in 2025 to USD 697.5 million by 2034, registering a compound annual growth rate (CAGR) of 12.8%. According to Dimension Market Research, this expansion is being fundamentally driven by three converging forces: escalating drug recalls and regulatory scrutiny across major markets, the rapid expansion of…

Automated Cooking Systems Market to Skyrocket from 5.0 Billion in 2025 to 34.1 B …

The global Automated Cooking Systems Market is poised for explosive growth, with market valuation projected to surge from an estimated USD 5.0 billion in 2025 to USD 34.1 billion by 2034, registering a remarkable compound annual growth rate (CAGR) of 23.8%. According to Dimension Market Research, this extraordinary expansion is being driven by three converging forces: acute labor shortages across the global foodservice industry, rapid advancements in AI-powered robotics and…

More Releases for ICs

Unveiling the MacSonik ICS Converter Tool

A next-generation utility for seamless ICS file conversion across different formats on both Windows and macOS systems.

November 05, 2025 - MacSonik Software, 2880 Zanker Road, Suite 203, San Jose, California, US

MacSonik Software, a globally trusted name in secure and innovative data management solutions, continues to deliver excellence with a comprehensive range of tools in Data Migration, Email Management, File Conversion, Backup, and Cloud Optimization. With a commitment to reliability and…

Battery Authentication ICs Market

Battery Authentication ICs Market Analysis:

The global Battery Authentication ICs Market size was estimated at USD 635 million in 2023 and is projected to reach USD 1183.35 million by 2030, exhibiting a CAGR of 9.30% during the forecast period.

North America Battery Authentication ICs market size was USD 165.46 million in 2023, at a CAGR of 7.97% during the forecast period of 2025 through 2030.

To Read Full Market Report -

https://semiconductorinsight.com/report/battery-authentication-ics-market/

Battery Authentication ICs…

Magnetic Position Sensor ICs Market

Magnetic position sensor ICs are tiny integrated circuits that detect the location of a magnet. They use the magnetic field to determine the magnet's position, either linear or rotary, without physically touching it. Magnetic position sensor ICs represent a transformative technology that is revolutionizing position sensing across various industries. As companies embrace automation, electrification, and innovation, magnetic position sensor ICs are poised to play an increasingly pivotal role in…

Phased Array Beamforming ICs Market: Advanced ICs Enabling Precise Beamforming i …

Global Phased Array Beamforming ICs Market Overview:

The Phased Array Beamforming ICs market is a broad category that includes a wide range of products and services related to various industries. This market comprises companies that operate in areas such as consumer goods, technology, healthcare, and finance, among others.

In recent years, the Phased Array Beamforming ICs market has experienced significant growth, driven by factors such as increasing consumer demand, technological advancements, and…

Global Industrial Control Systems (ICS) Security Market

As per latest findings on ICS security components and solutions conducted by Global Market Estimates, the Industrial Control Systems (ICS) Security Market will have a growth rate of 8.2% during the forecast period. Factors responsible for its growth are the increasing number of cybercrimes on the ICS system and initiatives taken by the government to adopt new gird technology across the globe to utilize energy and technology to its fullest…

Global Ethernet ICs Market Demand 2020-2025

This report also researches and evaluates the impact of Covid-19 outbreak on the Ethernet ICs�industry, involving potential opportunity and challenges, drivers and risks. We present the impact assessment of Covid-19 effects on Ethernet ICs�and market growth forecast based on different scenario (optimistic, pessimistic, very optimistic, most likely etc.).

�

Scope of the Report:

The report presents the market outlook for the Indian Phospho Gypsum product from the year 2019 to the year 2025.…