Press release

Data Center CPU Market to Reach $42.6B by 2035 at 8.7% CAGR, North America Leads Growth - Intel, AMD, ARM

Data Center CPU Market

Get detailed market forecasts, competitive benchmarking, and pricing trends:

https://www.factmr.com/connectus/sample?flag=S&rep_id=11154

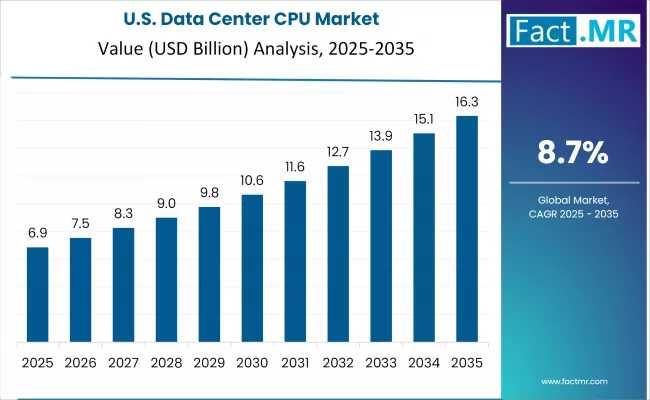

According to Fact.MR analysis, the global data center CPU market is projected to grow from USD 18.5 billion in 2025 to USD 42.6 billion by 2035, expanding at a CAGR of 8.7%. More than half of the market's ten-year expansion is expected to occur between 2030 and 2035, reflecting the accelerating commercialization of AI-integrated processors, edge computing infrastructure, and advanced heterogeneous computing architectures.

As enterprises scale generative AI deployments and cloud providers race to improve performance-per-watt economics, CPUs are no longer viewed as commodity infrastructure. They are increasingly becoming strategic assets that determine operational efficiency, sustainability targets, workload agility, and long-term infrastructure competitiveness.

Quick Stats: Data Center CPU Market Snapshot

Metric

Value

Market Size (2025E)

USD 18.5 Billion

Forecast Value (2035F)

USD 42.6 Billion

CAGR (2025-2035)

8.7%

Dominant Processor Type

x86 Processors

Leading End User

Hyperscale Data Centers

Hyperscale Market Share

50.0%

x86 Processor Share

75.0%

AI Workloads Are Reshaping the Economics of Data Center Processing

The next growth cycle in the data center CPU market is being driven less by traditional enterprise IT refreshes and more by structural shifts in computational demand.

Artificial intelligence training, real-time inference, high-performance analytics, cloud gaming, cybersecurity automation, and edge orchestration are creating increasingly diverse workload requirements. As a result, data center operators are demanding processors capable of balancing computational density, thermal efficiency, scalability, and application flexibility.

This transformation is particularly visible in hyperscale environments, where infrastructure operators are under pressure to reduce operational costs while simultaneously expanding compute capacity. CPU vendors are responding with architectures optimized for AI-assisted workloads, intelligent resource allocation, and integrated acceleration capabilities.

The market's expansion also reflects broader cloud transformation initiatives across industries including finance, healthcare, telecommunications, manufacturing, retail, and government services. As organizations modernize digital infrastructure, CPU performance is becoming closely tied to business continuity, application responsiveness, and operational resilience.

Hyperscale Expansion Continues to Anchor Demand

Hyperscale data centers remain the single largest demand center for advanced CPU systems, accounting for 50% of global market demand in 2025.

Cloud service providers are investing aggressively in processor technologies capable of supporting:

Massive parallel computing

AI inference workloads

Containerized applications

Real-time analytics

Multi-tenant virtualization

Edge-to-cloud orchestration

The scale of these deployments is altering procurement priorities. Infrastructure buyers are increasingly evaluating CPUs not only on peak performance benchmarks, but also on energy consumption profiles, software ecosystem compatibility, and lifecycle operating costs.

The result is a market environment where processing efficiency is becoming just as important as computational power.

x86 Architecture Maintains Dominance - But Competitive Pressure Is Rising

x86 processors are projected to maintain a commanding 75% market share in 2025, supported by deep software compatibility, mature ecosystems, and established enterprise adoption.

For most cloud operators and enterprise data centers, x86 remains the preferred architecture because it simplifies integration across existing applications, middleware environments, and virtualization frameworks.

However, the competitive landscape is shifting.

ARM-based architectures are steadily gaining traction in cloud-native deployments and energy-sensitive environments where efficiency and scalability are prioritized over legacy compatibility. This trend is particularly visible in hyperscale deployments focused on optimizing cost-per-compute metrics.

The growing diversification of workloads is encouraging infrastructure operators to adopt multi-architecture strategies rather than relying exclusively on traditional processor ecosystems.

Industry analysts increasingly view the market as evolving from a single-architecture model toward a heterogeneous computing environment where x86, ARM, AI accelerators, and custom silicon coexist.

Energy Efficiency Is Becoming a Board-Level Infrastructure Metric

Power consumption is emerging as one of the most influential variables shaping CPU procurement decisions.

As data center energy costs rise and environmental regulations tighten globally, operators are under pressure to improve performance-per-watt efficiency across infrastructure environments.

This shift is especially important because AI workloads consume significantly more power than traditional enterprise applications. Large-scale AI inference and model training operations can dramatically increase cooling demands, operational expenditure, and sustainability risks.

Consequently, processor manufacturers are investing heavily in:

Advanced manufacturing nodes

AI-integrated architectures

Dynamic power management systems

Specialized acceleration engines

Intelligent workload optimization

Chiplet-based modular designs

The emphasis on sustainability is also influencing government policy and capital allocation decisions. Many infrastructure investment programs now prioritize energy-efficient computing systems as part of broader digital modernization strategies.

Regional Markets Reflect Different Infrastructure Priorities

United States Leads Through Cloud Scale and AI Infrastructure

The United States is projected to register the fastest growth among major markets, with a CAGR of 10.2% through 2035.

Growth is being driven by:

Expansion of hyperscale cloud infrastructure

Aggressive AI deployment strategies

Semiconductor innovation leadership

Enterprise digital transformation

Federal investment in domestic chip manufacturing

Major technology hubs including Silicon Valley, Seattle, Austin, and Northern Virginia continue to attract large-scale infrastructure investment, reinforcing the country's leadership position in cloud computing and advanced processor deployment.

The U.S. market also benefits from strong collaboration between cloud providers, semiconductor manufacturers, AI developers, and enterprise software companies.

Germany Strengthens Europe's Processing Leadership

Germany is emerging as Europe's most influential market for advanced data center processing technologies, supported by its semiconductor expertise, industrial computing infrastructure, and engineering-led digital transformation initiatives.

The country is expected to grow at a CAGR of 9.8% through 2035.

German infrastructure operators are prioritizing:

High-performance enterprise computing

AI-enabled industrial applications

Energy-efficient infrastructure

Advanced processor validation

Long-term operational reliability

Berlin, Munich, and Frankfurt continue to serve as major regional hubs for cloud infrastructure investment and advanced semiconductor collaboration.

Japan Prioritizes Precision Computing and Compatibility

Japan's market growth is being shaped by advanced computing applications and a strong preference for reliable, highly compatible processing ecosystems.

x86 processors account for 78.5% of deployments in Japan, reflecting the country's emphasis on application continuity, operational precision, and infrastructure stability.

Demand is particularly strong across:

Financial services

Industrial automation

Advanced manufacturing

Telecommunications

Enterprise cloud modernization

Japanese operators are also increasingly integrating ARM-based systems for specialized applications requiring lower power consumption and scalable cloud-native capabilities.

South Korea Builds Momentum Through Semiconductor Innovation

South Korea is leveraging its semiconductor leadership position to accelerate adoption of advanced data center processing systems.

The market is forecast to grow at a CAGR of 9.0% through 2035, supported by:

Semiconductor innovation

Infrastructure modernization

AI-driven cloud expansion

Government-backed technology initiatives

Advanced manufacturing ecosystems

South Korean operators are increasingly deploying AI-optimized infrastructure designed for large-scale automation, smart computing environments, and next-generation telecommunications networks.

AI Integration Is Expanding the Definition of the Modern CPU

The distinction between CPUs, GPUs, and AI accelerators is gradually becoming less rigid.

Modern processors increasingly integrate:

Neural processing units

Vector acceleration engines

AI inference capabilities

Advanced memory hierarchies

Intelligent scheduling systems

This convergence reflects the growing need for processors capable of handling mixed workloads without relying exclusively on separate accelerator hardware.

For enterprise operators, integrated AI functionality offers several advantages:

Reduced infrastructure complexity

Lower latency

Improved energy efficiency

Simplified deployment models

Better workload orchestration

This architectural evolution is expected to become one of the defining competitive factors in the next generation of data center infrastructure.

Competitive Landscape Intensifies Across Traditional and Emerging Players

The competitive environment is becoming increasingly dynamic as established semiconductor leaders face growing pressure from specialized processor developers and cloud-native infrastructure companies.

Major participants include:

Intel Corporation

AMD

ARM Holdings

IBM

Marvell Technology

Ampere Computing

Qualcomm

MediaTek

Broadcom

NVIDIA

Competition is increasingly centered on:

AI acceleration capabilities

Performance-per-watt efficiency

Cloud-native optimization

Software ecosystem maturity

Security integration

Specialized workload performance

The rise of custom silicon initiatives among hyperscale cloud providers is also reshaping competitive dynamics, introducing new strategic considerations for traditional CPU manufacturers.

Strategic Implications for Infrastructure Leaders

For C-level executives and infrastructure decision-makers, the market's evolution carries several strategic implications.

Infrastructure Planning Must Become More Flexible

Static infrastructure strategies are becoming increasingly risky as workload requirements evolve rapidly. Organizations are likely to adopt hybrid processing environments combining x86, ARM, and AI-specific acceleration systems.

Energy Economics Will Influence Competitive Positioning

Power efficiency is transitioning from a technical consideration to a financial and regulatory imperative. Infrastructure decisions increasingly affect sustainability reporting, operational margins, and long-term scalability.

AI Readiness Will Shape Procurement Decisions

Organizations are prioritizing processors capable of supporting AI workloads even if immediate deployment needs remain modest. Future-proofing infrastructure has become a central procurement objective.

Supply Chain Diversification Is Becoming Critical

Geopolitical tensions and semiconductor concentration risks are encouraging enterprises and governments to diversify sourcing strategies and invest in regional manufacturing resilience.

Future Outlook: From Compute Infrastructure to Intelligent Processing Ecosystems

The next decade is likely to redefine how processing infrastructure is designed, managed, and monetized.

By 2035, the data center CPU market will increasingly revolve around intelligent compute ecosystems where processors dynamically optimize workloads, integrate AI acceleration natively, and coordinate seamlessly across cloud, edge, and enterprise environments.

Rather than competing solely on clock speed or core count, future market leaders will differentiate through:

Intelligent orchestration

AI-native architecture

Sustainability performance

Cloud-scale adaptability

Security resilience

Ecosystem interoperability

As AI adoption accelerates globally, the role of CPUs is evolving from foundational hardware to strategic infrastructure intelligence.

Executive Takeaways

The global data center CPU market is projected to grow from USD 18.5 billion in 2025 to USD 42.6 billion by 2035.

AI workloads, cloud expansion, and edge computing are fundamentally reshaping processor demand patterns.

Hyperscale data centers remain the dominant demand center, accounting for 50% of market consumption.

x86 architectures continue to lead, but ARM-based adoption is accelerating in energy-sensitive cloud environments.

Performance-per-watt efficiency is becoming a critical procurement metric alongside raw computational capability.

Integrated AI acceleration and heterogeneous computing architectures are redefining processor design strategies.

The United States, Germany, Japan, and South Korea are emerging as the market's most influential innovation hubs.

Competitive intensity is rising as semiconductor leaders face pressure from cloud-native and AI-focused challengers.

Infrastructure modernization strategies increasingly require multi-architecture flexibility and AI readiness planning.

Full Report: Unlock 360° insights for strategic decision making and investment planning-

https://www.factmr.com/checkout/11154

To View Related Report:

Data As A Service (DaaS) Market https://www.factmr.com/report/1469/data-as-a-service-market

Data Mining Tools Market https://www.factmr.com/report/data-mining-tools-market

Data Protection Software Market https://www.factmr.com/report/1326/data-protection-software-market

Data Labeling Solution and Services Market https://www.factmr.com/report/data-labeling-solution-and-services-market

- Contact Us -

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Data Center CPU Market to Reach $42.6B by 2035 at 8.7% CAGR, North America Leads Growth - Intel, AMD, ARM here

News-ID: 4500450 • Views: …

More Releases from Fact MR

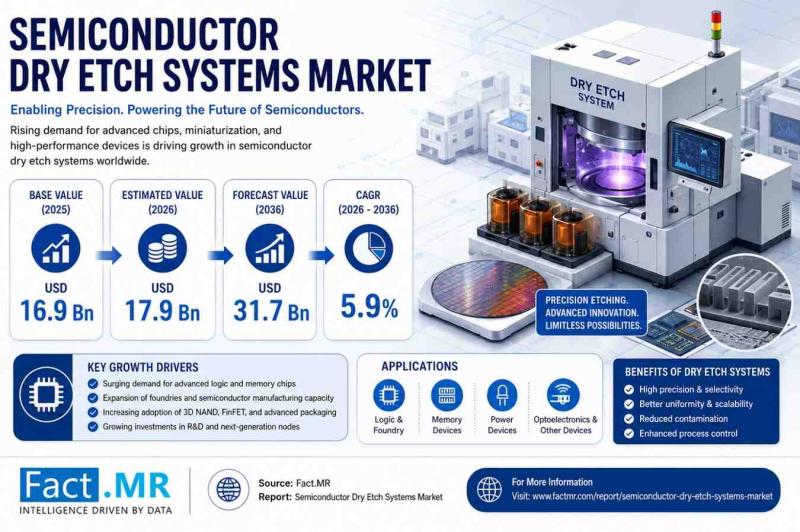

U.S. Semiconductor Dry Etch Systems Market Size to Reach USD 31.75 Billion by 20 …

According to a market study published by Fact.MR, The global semiconductor dry etch systems market was valued at USD 16.90 billion in 2025, is estimated at USD 17.90 billion in 2026, and is projected to reach USD 31.75 billion by 2036. the industry is expected to expand at a compound annual growth rate (CAGR) of 5.9% over the 2026 to 2036 forecast period.

Get detailed market forecasts, competitive benchmarking, and pricing…

Livestream Checkout Plugins Market Size to Reach USD 6.1 billion by 2036, Expand …

According to a market study published by Fact.MR, The global livestream checkout plugins market is estimated at USD 1.2 billion in 2026 and is projected to reach USD 6.1 billion by 2036. the market is forecast to expand at a compound annual growth rate (CAGR) of 17.7% over the 2026 to 2036 period. For e-commerce category managers, retail innovation heads, social commerce leads, and digital technology investors, livestream checkout plugins…

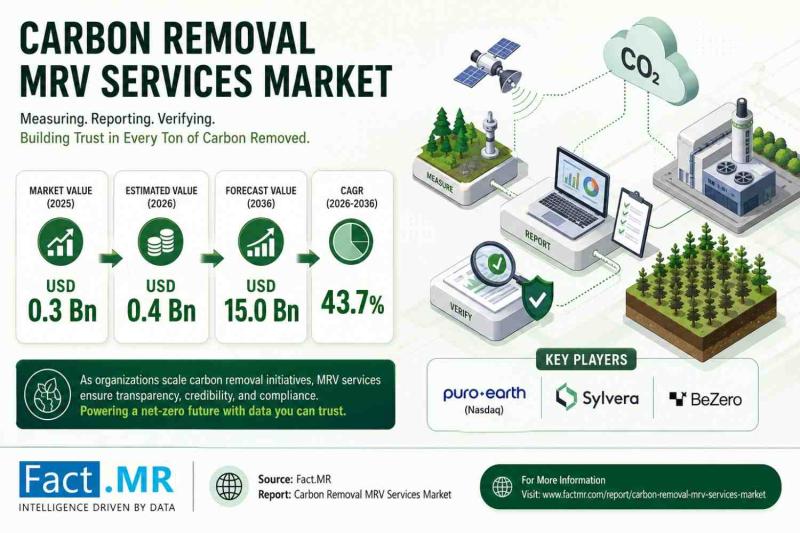

U.S. Carbon Removal MRV Services Market Size to Hit USD 15.0 Billion by 2036, Su …

According to a market study published by Fact.MR, The global carbon removal MRV services market crossed a valuation of USD 0.3 billion in 2025, is estimated at USD 0.4 billion in 2026, and is projected to reach USD 15.0 billion by 2036. the sector is forecast to expand at an extraordinary compound annual growth rate (CAGR) of 43.7% between 2026 and 2036.

Get detailed market forecasts, competitive benchmarking, and pricing trends:…

U.S. Post-Quantum Migration Services Market Size to Hit USD 55.0 billion by 2036 …

According to a market study published by Fact.MR, The global post-quantum migration services market is estimated at USD 2.3 billion in 2026 and is projected to expand rapidly, reaching USD 55.0 billion by 2036. the industry is expected to grow at a compound annual growth rate (CAGR) of 37.4% over the 2026 to 2036 forecast period.

Get detailed market forecasts, competitive benchmarking, and pricing trends: https://www.factmr.com/connectus/sample?flag=S&rep_id=15252

For enterprise decision-makers, chief information security…

More Releases for CPU

Global CPU Sockets Market

CPU Sockets Market Overview

A CPU socket is a physical interface on a motherboard that allows a central processing unit (CPU) to be securely connected to the computer's electrical system. It provides the necessary connections for data transfer, power supply, and cooling, enabling the CPU to communicate with other components of the system. CPU sockets are designed to fit specific CPU architectures and ensure compatibility between the processor and the motherboard.

CPU…

CPU And GPU Market Size Analysis by Application, Type, and Region: Forecast to C …

USA, New Jersey- According to Market Research Intellect, the global CPU And GPU market in the Internet, Communication and Technology category is projected to witness significant growth from 2025 to 2032. Market dynamics, technological advancements, and evolving consumer demand are expected to drive expansion during this period.

The CPU and GPU market is experiencing significant growth, driven by advancements in computing, gaming, artificial intelligence (AI), and cloud computing. The increasing demand…

The difference between CPU thermal conductive silicone sheet and CPU thermal con …

Why does the CPU need thermal pad? How to choose thermal pad?

Both thermal silicone sheets and thermal grease are used to assist CPU heat dissipation, so as to maximize the heat dissipation capacity of the CPU fan. So what is the difference between the two? Which one is better to use?

Thermal conductive silicone sheets/Thermal pad [https://www.cmaisz.com/odm-custom-diverse-thermal-pad-designs-product/] are generally used in places where it is inconvenient to apply thermal conductive silicone…

CPU Heatsink Market Size 2024 to 2031.

Market Overview and Report Coverage

A CPU heatsink is a component used to dissipate heat away from a computer's central processing unit (CPU) to prevent overheating and maintain optimal performance. As technology advances and CPUs become more powerful, the demand for efficient and effective CPU heatsinks is expected to increase.

The future outlook of the CPU heatsink market looks promising, with a projected growth rate of 3.90% during the forecasted…

FastComet Introduces New Dedicated CPU Servers

San Francisco, CA, June 25, 2019 --(OpenPR.com)-- FastComet is a web hosting provider from San Francisco, California, that was established in 2013. After reinventing their whole brand identity earlier this year, FastComet is keeping up the pace, introducing the Dedicated CPU Servers. These Servers are backed by AMD EPYC 7501 processor, designed to meet the requirements of specific applications that can take advantage of the higher clock speeds. The Dedicated…

United States CPU Processors Market Report 2017

Summary

This report studies sales (consumption) of CPU Processors in United States market, focuses on the top players, with sales, price, revenue and market share for each player, covering

Intel

Toshiba

Broadcom

MediaTek

Ineda

Marvell

NXP

STMicroelectronics

Market Segment by States, covering

California

Texas

New York

Florida

Illinois

Split by product types, with sales, revenue, price, market share and growth rate of each type, can be divided into

Type I

Type II

Split by applications, this report focuses on sales, market share and growth rate of CPU Processors in…