Press release

Cancer Biomarkers Market to Reach $54.5B by 2036 at 13% CAGR, North America Leads Growth - Roche, Thermo Fisher, Illumina

Cancer Biomarkers Market

Get detailed market forecasts, competitive benchmarking, and pricing trends:

https://www.factmr.com/connectus/sample?flag=S&rep_id=4587

What makes the current cycle different from earlier growth phases is the structural shift underway in cancer management itself. Biomarker testing is no longer limited to confirming disease presence. It is increasingly embedded across the full oncology continuum-from risk stratification and early detection to treatment selection, therapy monitoring, recurrence assessment, and drug development. As healthcare systems globally prioritize personalized treatment pathways, biomarker-driven decision-making is becoming a foundational component of modern cancer care infrastructure.

Quick Stats: Cancer Biomarkers Market Snapshot

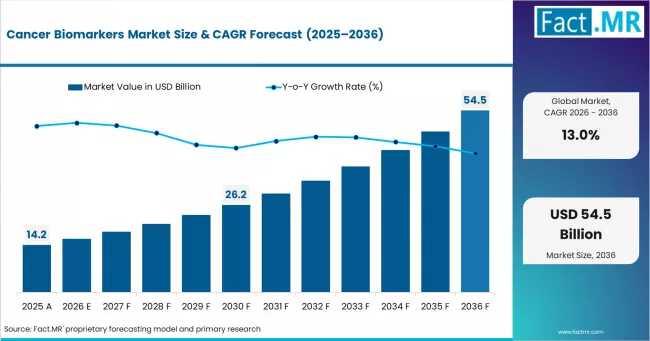

Market Value (2025): USD 14.2 billion

Projected Market Value (2036): USD 54.469 billion

Forecast CAGR (2026-2036): 13.0%

Incremental Opportunity: USD 38.423 billion

Leading Test Segment: PSA Tests with 35.4% market share

Largest Disease Indication: Breast Cancer with 24.9% share

Top Application Segment: Diagnostics at 31.5% share

Largest Revenue Market: United States

Fastest-Growing Region: East Asia

Leading Company: F. Hoffmann-La Roche Ltd. with 21.0% market share

Precision Oncology Is Turning Biomarker Testing Into a Standard Clinical Requirement

One of the strongest growth accelerators in the market is the global transition from empirical oncology treatment toward precision-guided therapy. Clinical guidelines issued by organizations such as the National Comprehensive Cancer Network (NCCN), the European Society for Medical Oncology (ESMO), and national healthcare authorities increasingly require biomarker validation before physicians prescribe targeted therapies.

This transformation is creating recurring and highly structured demand for companion diagnostics. Pharmaceutical developers launching targeted oncology drugs now depend on validated biomarker assays to secure regulatory approvals. As a result, the commercial trajectory of oncology therapeutics and cancer biomarkers has become deeply interconnected.

The market is also benefiting from rapid adoption of liquid biopsy technologies. Blood-based testing platforms are reducing dependence on invasive tissue biopsies while enabling repeat testing for disease monitoring and therapy response assessment. For clinicians, this improves workflow flexibility and expands access to patients who may not be eligible for surgical tissue extraction.

At the same time, healthcare systems are broadening cancer screening programs. Governments in the United States, China, Germany, and several other developed and emerging markets are integrating biomarker-based detection protocols into national screening frameworks, supporting long-term volume growth.

Multi-Cancer Early Detection Could Redefine the Addressable Market

Perhaps the most transformative development shaping the industry is the emergence of multi-cancer early detection (MCED) testing. Unlike traditional biomarker tests focused on specific cancer types, MCED platforms are designed to identify multiple cancers through a single blood sample.

These technologies analyze circulating tumor DNA, methylation signatures, protein biomarkers, and other molecular signals to identify early-stage disease in asymptomatic populations. If regulatory approvals and reimbursement pathways mature as expected, MCED testing could shift cancer biomarkers from a specialist oncology tool into a population-scale preventive screening category.

Companies including Illumina, Guardant Health, and Exact Sciences are investing aggressively in clinical validation studies aimed at supporting large-scale commercialization.

Industry analysts increasingly view MCED commercialization as a major inflection point for the sector after 2028. The opportunity is significant because it expands the testing population from diagnosed cancer patients to hundreds of millions of adults undergoing preventive health screening.

Diagnostics Remain the Core Revenue Engine

Diagnostic applications continue to account for the largest share of the market at 31.5% in 2025. This leadership position reflects the central role biomarkers now play in cancer detection, molecular subtyping, and treatment pathway selection.

Hospitals and diagnostic laboratories are increasingly integrating biomarker panels into standard oncology workflows. Companion diagnostics tied to immunotherapies and targeted drugs are becoming particularly important in lung, breast, colorectal, and blood cancers.

Predictive testing is also growing rapidly as clinicians seek molecular evidence to optimize therapy selection. Prognostic applications-used to estimate disease progression or recurrence risk-continue to expand alongside precision treatment models.

Drug discovery and development remains a comparatively smaller application area but is emerging as one of the fastest-growing segments. Pharmaceutical companies are incorporating biomarkers into clinical trial design to improve patient stratification and accelerate drug approval timelines.

PSA Testing Still Leads, but Growth Is Shifting Toward Multi-Gene Panels

PSA testing remains the largest individual test category, accounting for 35.4% of market demand in 2025. Its continued dominance reflects long-standing prostate cancer screening programs, broad physician adoption, and established reimbursement pathways in North America, Europe, and Japan.

However, future growth momentum is increasingly concentrated in genomic and mutation-focused assays such as HER2, BRCA, EGFR, KRAS, and ALK testing. These biomarkers are tightly linked to targeted therapy prescribing decisions, particularly in breast cancer and lung cancer treatment.

The market is also shifting toward consolidated multi-gene testing panels. Instead of conducting multiple standalone assays, laboratories are adopting sequencing-based workflows capable of evaluating several biomarkers simultaneously. This trend favors companies with integrated next-generation sequencing (NGS), analytics, and assay development capabilities.

Breast Cancer Leads Current Demand While Lung Cancer Shows Fastest Expansion

Breast cancer remains the largest disease indication segment, representing 24.9% of total market demand. Biomarker integration in breast cancer management is highly mature, particularly through HER2 testing, hormone receptor profiling, and BRCA mutation analysis.

Lung cancer, however, is emerging as the fastest-growing indication category. Expansion of immunotherapy and targeted kinase inhibitor treatments has dramatically increased demand for EGFR, ALK, PD-L1, and tumor mutational burden testing.

Colorectal cancer biomarker testing is also expanding steadily through KRAS and microsatellite instability assays, while ovarian and liver cancer applications are gaining traction as new biomarkers reach commercial adoption.

Regional Dynamics: China and India Are Becoming Major Growth Engines

North America remains the largest revenue-generating region, supported by advanced oncology infrastructure, reimbursement maturity, and high levels of precision medicine adoption. The United States alone contributes USD 6.035 billion in market value in 2025.

However, the most aggressive expansion is occurring across East Asia and South Asia.

China Accelerates Through Government-Led Screening Programs

China is forecast to record the highest CAGR globally at 16.7% between 2026 and 2036. The country's growth is being driven by government-backed cancer screening initiatives and major investments in genomics infrastructure.

Domestic companies such as BGI and Berry Oncology are scaling lower-cost sequencing platforms that improve affordability across secondary-care hospitals and regional screening centers.

India Emerges as a High-Growth Diagnostic Market

India is expected to grow at a CAGR of 15.5%, fueled by rising cancer incidence and rapid expansion of private diagnostic networks.

Laboratory chains including Metropolis Healthcare, SRL Diagnostics, and Thyrocare are expanding oncology testing capabilities beyond metropolitan areas into tier-2 and tier-3 cities.

The Indian market is particularly important because it demonstrates how biomarker adoption is transitioning from elite tertiary-care oncology centers toward broader community-level healthcare access.

Germany Strengthens Europe's Molecular Diagnostics Leadership

Germany continues to lead Europe through strong reimbursement support for NGS-based oncology testing and extensive university hospital infrastructure.

The country's molecular pathology ecosystem, supported by coordinated testing networks and statutory health insurance coverage, has enabled faster clinical integration of advanced biomarker assays than many neighboring European markets.

Competitive Landscape Is Becoming More Platform-Centric

The market remains moderately concentrated, with the five largest companies controlling more than half of total global share.

Hoffmann-La Roche Ltd. maintains leadership through its integrated diagnostics and pharmaceutical business model, allowing the company to align companion diagnostic development directly with oncology drug commercialization.

Platform-oriented competitors such as Thermo Fisher Scientific and Illumina are competing through sequencing ecosystem expansion, instrument installations, reagent revenue, and workflow integration.

Meanwhile, specialized firms including Natera and Guardant Health are intensifying competition in liquid biopsy and minimal residual disease monitoring.

An important competitive shift is emerging around data analytics capabilities. As biomarker testing evolves toward multi-omics profiling, companies capable of integrating genomic, proteomic, and metabolomic datasets into clinically actionable insights are expected to gain long-term strategic advantage.

Key Challenges Continue to Limit Broader Adoption

Despite strong growth fundamentals, several structural barriers remain.

Reimbursement inconsistency continues to slow adoption of advanced assays, especially multi-gene panels and MCED platforms. Coverage frameworks vary significantly across countries and payer systems, creating uncertainty for laboratories and healthcare providers.

Standardization also remains a major challenge. Variability in assay performance, reference ranges, and laboratory protocols can affect reproducibility and clinical confidence, particularly for newer biomarker technologies.

Additionally, many healthcare systems still lack the informatics infrastructure needed to convert large-scale multi-omics data into practical treatment decisions. This creates operational bottlenecks, especially in mid-sized hospitals and emerging-market healthcare environments.

Strategic Implications for Industry Stakeholders

For healthcare providers, biomarker testing is becoming a core infrastructure investment rather than a specialized oncology add-on. Hospitals that fail to expand molecular diagnostics capabilities may struggle to participate fully in precision oncology treatment ecosystems.

For pharmaceutical companies, companion diagnostics are increasingly essential to oncology commercialization strategy. Drug developers are likely to deepen partnerships with diagnostics firms to accelerate co-approval pathways and improve patient selection.

For investors, the highest-value opportunities may emerge in areas where diagnostics, data analytics, AI, and sequencing technologies converge. Companies positioned around integrated multi-omics platforms appear particularly well aligned with the next stage of market evolution.

For policymakers, reimbursement alignment and standardized testing frameworks will play a critical role in determining how quickly biomarker technologies move from specialist oncology settings into population-scale screening environments.

Outlook: The Market Is Moving Toward Predictive and Preventive Oncology

The cancer biomarkers industry is no longer defined solely by diagnostics. It is increasingly becoming a predictive intelligence layer for oncology decision-making.

Over the next decade, the market is expected to evolve from single-analyte testing toward highly integrated molecular profiling systems capable of identifying disease risk, predicting therapeutic response, monitoring recurrence, and supporting preventive screening initiatives.

The next major milestone will likely come through regulatory and reimbursement progress surrounding MCED testing. If blood-based screening platforms achieve large-scale clinical adoption, the cancer biomarkers market could expand far beyond its current oncology-centered boundaries and become a mainstream component of preventive healthcare.

For industry leaders, the strategic focus is shifting from isolated test development toward scalable ecosystem creation-combining sequencing technology, clinical evidence generation, AI-driven analytics, and payer integration into unified oncology intelligence platforms.

Full Report: Unlock 360° insights for strategic decision making and investment planning-

https://www.factmr.com/checkout/4587

To View Related Report:

Cancer Wounds Treatment Market https://www.factmr.com/report/cancer-wounds-treatment-market

Cancer Gene Therapy Market https://www.factmr.com/report/cancer-gene-therapy-market

Cancer Tumor Profiling Market https://www.factmr.com/report/cancer-tumor-profiling-market

Cancer and Tumor Biomarker-based Assay Market https://www.factmr.com/report/cancer-and-tumor-biomarker-based-assay-market

- Contact Us -

11140 Rockville Pike, Suite 400, Rockville,

MD 20852, United States

Tel: +1 (628) 251-1583 | sales@factmr.com

About Fact.MR

Fact.MR is a global market research and consulting firm, trusted by Fortune 500 companies and emerging businesses for reliable insights and strategic intelligence. With a presence across the U.S., UK, India, and Dubai, we deliver data-driven research and tailored consulting solutions across 30+ industries and 1,000+ markets. Backed by deep expertise and advanced analytics, Fact.MR helps organizations uncover opportunities, reduce risks, and make informed decisions for sustainable growth.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Cancer Biomarkers Market to Reach $54.5B by 2036 at 13% CAGR, North America Leads Growth - Roche, Thermo Fisher, Illumina here

News-ID: 4500442 • Views: …

More Releases from Fact MR

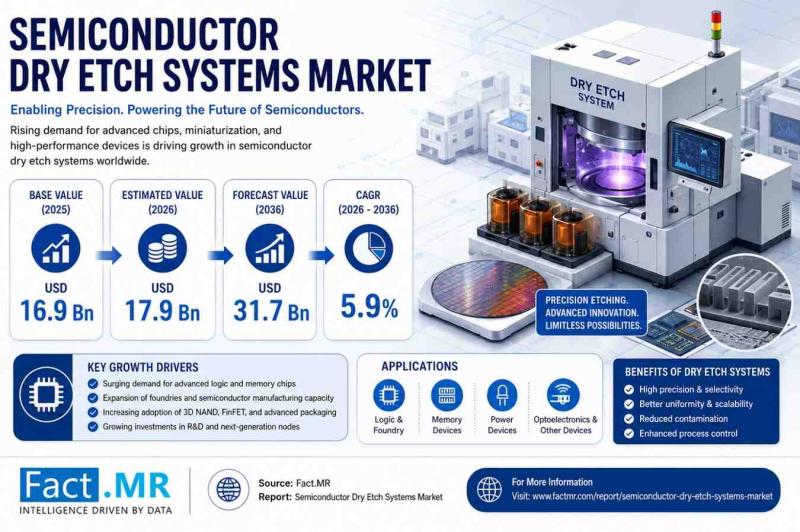

U.S. Semiconductor Dry Etch Systems Market Size to Reach USD 31.75 Billion by 20 …

According to a market study published by Fact.MR, The global semiconductor dry etch systems market was valued at USD 16.90 billion in 2025, is estimated at USD 17.90 billion in 2026, and is projected to reach USD 31.75 billion by 2036. the industry is expected to expand at a compound annual growth rate (CAGR) of 5.9% over the 2026 to 2036 forecast period.

Get detailed market forecasts, competitive benchmarking, and pricing…

Livestream Checkout Plugins Market Size to Reach USD 6.1 billion by 2036, Expand …

According to a market study published by Fact.MR, The global livestream checkout plugins market is estimated at USD 1.2 billion in 2026 and is projected to reach USD 6.1 billion by 2036. the market is forecast to expand at a compound annual growth rate (CAGR) of 17.7% over the 2026 to 2036 period. For e-commerce category managers, retail innovation heads, social commerce leads, and digital technology investors, livestream checkout plugins…

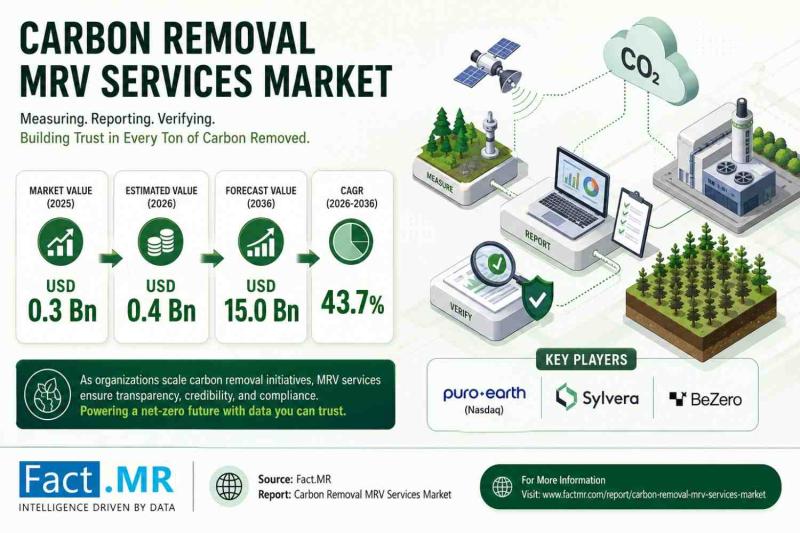

U.S. Carbon Removal MRV Services Market Size to Hit USD 15.0 Billion by 2036, Su …

According to a market study published by Fact.MR, The global carbon removal MRV services market crossed a valuation of USD 0.3 billion in 2025, is estimated at USD 0.4 billion in 2026, and is projected to reach USD 15.0 billion by 2036. the sector is forecast to expand at an extraordinary compound annual growth rate (CAGR) of 43.7% between 2026 and 2036.

Get detailed market forecasts, competitive benchmarking, and pricing trends:…

U.S. Post-Quantum Migration Services Market Size to Hit USD 55.0 billion by 2036 …

According to a market study published by Fact.MR, The global post-quantum migration services market is estimated at USD 2.3 billion in 2026 and is projected to expand rapidly, reaching USD 55.0 billion by 2036. the industry is expected to grow at a compound annual growth rate (CAGR) of 37.4% over the 2026 to 2036 forecast period.

Get detailed market forecasts, competitive benchmarking, and pricing trends: https://www.factmr.com/connectus/sample?flag=S&rep_id=15252

For enterprise decision-makers, chief information security…

More Releases for Cancer

Cancer Therapeutics Market New Business Opportunities to Hit $180.19 billion by …

Surge in geriatric population and rise in the number of collaborations & partnerships to facilitate drug development are the key drivers of the global cancer therapeutics market. In addition, heavy inflow of investment in R&D activities has enhanced the development of cancer therapeutics. Furthermore, favorable government regulations for cancer therapeutics and surge in cancer prevalence boost the market. The high demand for personalized medicine along with high potential of emerging…

Global Cancer Diagnostics Market Size, Trends & Growth Opportunity By Applicatio …

Cancer diagnostics is a process of detecting various proteins, biomarkers and certain symptoms that result in the detection of presence of cancerous tumour in patients. Detection of certain proteins and biomarkers which are prevalent in cancer disorder thereby results in diagnosis process. Cancer diagnostics includes usage of certain technology and devices for detection purpose.

Increase in incidence of target diseases like cancer is key driving factor which is expected to boost…

2019-2027 Oncology Nutrition Market is driven by Major Cancer Type - Head and Ne …

The "Global Oncology Nutrition Market Analysis to 2027" is a specialized and in-depth study with a special focus on the global market trend analysis. The report aims to provide an overview of oncology nutrition market with detailed market segmentation by cancer type and geography. The global oncology nutrition market is expected to witness high growth during the forecast period. The report provides key statistics on the market status of the…

Cancer Immunotherapy Market 2018 To 2025 - SWOT Analysis By Global Industry Reve …

The Cancer Immunotherapy Market research report provided by Crystal Market Research (CMR) is the most detailed study about Cancer Immunotherapy Market that is estimated to grow at a tremendous rate over the forecast period 2018-2025. This report contains precise and updated insights in respect with the leading market players and prevailing regions of the business.

Cancer Immunotherapy Market By Product and Cancer Type - Global Industry Analysis And Forecast To 2025:…

Oncology Nutrition Market by Cancer Type Breast Cancer, Liver Cancer, Lung Cance …

Lunch of new products for nutrition of oncology patients is expected to drive the oncology nutrition market growth. For instance, in 2016, Hormel Food Corporation, a U.S-based meat food products company, launched a line of packaged ready-to-eat meals for cancer patients, which are called as Hormel Vital Cuisine.

These meals consist of carbohydrates, proteins, and fats to help patients fight loss of muscle mass and energy during cancer treatment. Thus launch…

Tumor Ablation Global Market From 2014 - 2024: Segmented Into Liver Cancer, Lung …

Researchmoz added Most up-to-date research on "Tumor Ablation Global Market From 2014 - 2024: Segmented Into Liver Cancer, Lung Cancer, Kidney Cancer, Bone Cancer, Breast Cancer, Prostate Cancer, And Others" to its huge collection of research reports.

Tumor ablation is the removal of the tumor cells or tissue with minimally invasive procedure. Tumor ablation devices are consists of an applicator (catheter), which is introduced into the tumor under imaging guidance. For…