Press release

Beyond Volume Growth: Metallocene HDPEs Structural Shift Toward High-Performance Resins

The shift from volume-driven growth to capital-intensive expansion is particularly visible in Asia-Pacific, where new capacity investments are increasingly tied to downstream application ecosystems (e.g., food-grade packaging, medical-grade films, and high-strength industrial containers). With full production lines requiring 30K tons per year capacity and gross margins stabilizing around 25%, barriers to entry are rising. As a result, the investment thesis is evolving: scale alone is insufficient technology ownership, catalyst IP, and operational efficiency are now primary drivers of EBITDA expansion.

Global Overview

The global mHDPE market was valued at USD 9,082 million in 2025 and is projected to reach USD 14,104 million by 2032, reflecting a CAGR of 6.5%. Total global sales volume is approximately 5,676K tons, with an average selling price (ASP) of USD 1,600 per ton.

Core demand is anchored in structural shifts across packaging, infrastructure, and healthcare. First, the transition toward high-performance flexible packaging is accelerating, particularly in food and e-commerce logistics, where puncture resistance and seal integrity are critical. Second, infrastructure modernization in emerging economies is driving demand for durable piping and geomembranes. Third, regulatory pressure around recyclability is favoring mono-material solutions, where mHDPE offers superior compatibility. Finally, healthcare applicationsespecially sterile packagingare expanding due to stringent quality requirements.

Regional Consumption Dynamics (APAC / SEA)

Asia-Pacific accounts for the largest share of global consumption, underpinned by Chinas industrial base and Southeast Asias manufacturing expansion. Southeast Asia is transitioning from an import-dependent region to a hybrid production-consumption hub.

Indonesia is experiencing strong demand growth driven by its food packaging and FMCG sectors, supported by government-backed downstream petrochemical initiatives. Malaysia and Singapore are positioning as high-value production and trading hubs, leveraging advanced refining and logistics infrastructure. Vietnam and Thailand are emerging as key manufacturing relocation destinations, particularly for export-oriented packaging and consumer goods, increasing localized demand for mHDPE resins.

Sovereign investment strategies across the region are increasingly aligned with petrochemical self-sufficiency. Large-scale integrated complexes often combining refining, olefins, and polymer units are being deployed to capture more value domestically. This has led to a tightening of regional supply-demand balances and increased intra-Asia trade flows.

Production and Supply Chain

Value capture in the mHDPE market is concentrated upstream in catalyst technology and midstream in polymerization efficiency. Metallocene catalysts enable precise control over molecular weight distribution, resulting in superior mechanical properties. Producers with proprietary catalyst systems and integrated ethylene feedstock access consistently achieve gross margins in the 2030% range, with 25% as a stable benchmark.

Asia plays a central role in both supply expansion and cost optimization. China dominates capacity additions, but Southeast Asia is strategically important for feedstock diversification and export positioning. Singapore acts as a trading and pricing hub, while Malaysia and Thailand provide refining and petrochemical integration. Indonesia is increasingly relevant as a demand anchor with growing domestic conversion capacity.

Supply chain resilience is becoming a competitive differentiator. Producers are investing in backward integration into ethylene and forward integration into specialty applications to stabilize margins and reduce volatility.

Latest Technological Developments

Advanced metallocene catalyst systems are enabling narrower molecular weight distribution, improving tensile strength and film clarity for high-spec packaging applications.

AI-driven process control systems are being deployed in polymerization reactors to optimize temperature, pressure, and catalyst dosing in real time, increasing yield efficiency.

Dual-reactor configurations are being adopted to produce bimodal HDPE with enhanced stiffness and impact resistance.

Energy-efficient cooling and heat recovery systems are reducing operational costs in large-scale production lines.

Development of recyclable mono-material film structures using mHDPE is aligning with circular economy regulations.

Integration of digital twins in production facilities is improving predictive maintenance and reducing downtime.

Market Breakdown Categories

Processing Methods

Product

Catalyst

Grade

MFI

Injection Molding

Packaging

Zirconocene Based

Food Grade

Low MFI grades (10 g/10 min)

Healthcare

Shipment terms for metallocene HDPE are typically structured under standard international trade frameworks such as FOB, CFR, or CIF, depending on buyer location and supplier integration. Bulk volumes are transported via containerized shipments (20-foot or 40-foot containers) or bulk vessels for large contracts, with lead times ranging from 26 weeks within Asia-Pacific and longer for intercontinental routes. Producers with integrated logistics hubs in Singapore and Malaysia often provide shorter delivery cycles across Southeast Asia.

Packaging is standardized to preserve resin quality and handling efficiency. Most mHDPE is supplied in 25 kg polyethylene bags, jumbo bags (FIBCs) of 11.5 tons, or in bulk silo trucks for large industrial buyers. For export markets, palletized and shrink-wrapped configurations are common to ensure moisture protection and ease of handling during transit and warehousing.

Minimum order quantities (MOQ) vary by supplier scale and contract structure. Typical MOQs range from 1 full container load (approximately 2025 tons) for spot buyers to 100 to 300 tons for contract-based procurement. Large converters and distributors in Southeast Asia often negotiate annual offtake agreements with flexible call-off volumes to optimize inventory and pricing exposure.

Product Pricing Variations

Pricing varies significantly based on grade, application, and producer integration.

For high-performance film-grade products, ExxonMobils Enable mHDPE series is priced between USD 1,700 to 1,950/ton, reflecting superior sealing and puncture resistance used in food packaging. Similarly, Dows Elite enhanced polyethylene resins range from USD 1,650 to 1,900/ton, widely used in flexible packaging due to their processability and strength balance.

In injection molding applications, LyondellBasells Hostalen Advanced Cascade Process (ACP) HDPE grades are typically priced between USD 1,550 to 1,750/ton, optimized for rigidity and environmental stress fault resistance. Borealis BorSafe pipe-grade materials command higher prices, ranging from USD 1,800 to 2,100/ton, due to their long-term durability in infrastructure projects.

For blow molding, SABICs HDPE BM series ranges from USD 1,500 to 1,700/ton, widely used in industrial containers. INEOS HDPE blow molding grades are similarly priced but benefit from feedstock integration in Europe and Asia.

Lower-end industrial grades, including Sinopec and CNPC standard HDPE resins, are priced between USD 1,300 to 1,500/ton, targeting cost-sensitive applications in emerging markets.

Global Top 30 Key Companies in the Metallocene HDPE Market

Exxon Mobil Corporation (Texas, US)

Dow Inc. (Michigan, US)

SABIC (Saudi Arabia)

LyondellBasell Industries (Netherlands)

Chevron Phillips Chemical (Texas, US)

INEOS Olefins & Polymers (UK / Switzerland)

TotalEnergies (France)

Borealis AG (Austria)

Reliance Industries (Gujarat, India)

China Petroleum & Chemical Corporation Sinopec (Beijing, China)

CNPC / PetroChina (Beijing, China)

LG Chem (Seoul, South Korea)

Mitsui Chemicals (Tokyo, Japan)

SK Geo Centric (Seoul, South Korea)

Daelim Industrial (DL Chemical) (Seoul, South Korea)

Prime Polymer (Tokyo, Japan)

Japan Polyethylene Corporation (Tokyo, Japan)

NOVA Chemicals (Canada)

Westlake Corporation (Texas, US)

Braskem (Brazil)

Sibur (Moscow, Russia)

Sasol (South Africa)

Lotte Chemical (Seoul, South Korea)

Hanwha Solutions (Seoul, South Korea)

PTT Global Chemical (Bangkok, Thailand)

SCG Chemicals (Bangkok, Thailand)

Petronas Chemicals Group (Kuala Lumpur, Malaysia)

Formosa Plastics Corporation (Taiwan)

Repsol (Madrid, Spain)

Univation Technologies (Texas, US)

Chapter Outline

Chapter 1: Introduces the report scope of the report, executive summary of different market segments (by region, product type, application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the market and its likely evolution in the short to mid-term, and long term.

Chapter 2: key insights, key emerging trends, etc.

Chapter 3: Manufacturers competitive analysis, detailed analysis of the product manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc.

Chapter 4: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc.

Chapter 5 & 6: Sales, revenue of the product in regional level and country level. It provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and market size of each country in the world.

Chapter 7: Provides the analysis of various market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 8: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 9: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 10: The main points and conclusions of the report.

Related Report Recommendation

Global Metallocene HDPE Market Research Report 2026

https://www.qyresearch.com/reports/6605068/metallocene-hdpe

Metallocene HDPE- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

https://www.qyresearch.com/reports/6605067/metallocene-hdpe

Global Metallocene HDPE Market Outlook, InDepth Analysis & Forecast to 2032

https://www.qyresearch.com/reports/6605066/metallocene-hdpe

Global Metallocene HDPE Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/6605065/metallocene-hdpe

Global Metallocene PE Market Research Report 2026

https://www.qyresearch.com/reports/5520077/metallocene-pe

Global Metallocene PP Market Research Report 2026

https://www.qyresearch.com/reports/5520020/metallocene-pp

Global Metallocene EPDM Market Research Report 2026

https://www.qyresearch.com/reports/5701032/metallocene-epdm

Global Metallocene Catalyst Market Research Report 2026

https://www.qyresearch.com/reports/5532425/metallocene-catalyst

Global Metallocene Technology Market Research Report 2026

https://www.qyresearch.com/reports/6014038/metallocene-technology

Global Metallocene POE and POP Market Research Report 2026

https://www.qyresearch.com/reports/5871113/metallocene-poe-and-pop

About QY Research

QY Research has established close partnerships with over 71,000 global leading players. With more than 20,000 industry experts worldwide, we maintain a strong global network to efficiently gather insights and raw data.

Our 36-step verification system ensures the reliability and quality of our data. With over 2 million reports, we have become the world's largest market report vendor. Our global database spans more than 2,000 sources and covers data from most countries, including import and export details.

We have partners in over 160 countries, providing comprehensive coverage of both sales and research networks. A 90% client return rate and long-term cooperation with key partners demonstrate the high level of service and quality QY Research delivers.

More than 30 IPOs and over 5,000 global media outlets and major corporations have used our data, solidifying QY Research as a global leader in data supply. We are committed to delivering services that exceed both client and societal expectations.

Contact Information:

Tel: +1 626 2952 442 (US) ; +86-1082945717 (China)

+62 896 3769 3166 (Whatsapp)

Email: willyanto@qyresearch.com; global@qyresearch.com

Website: www.qyresearch.com

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Beyond Volume Growth: Metallocene HDPEs Structural Shift Toward High-Performance Resins here

News-ID: 4488162 • Views: …

More Releases from QY Research

Top 30 Indonesian Tissue Paper Public Companies Q3 2025 Revenue & Performance

1) Overall companies performance (Q3 2025 snapshot)

PT Indah Kiat Pulp & Paper Tbk (INKP)

PT Pabrik Kertas Tjiwi Kimia Tbk (TKIM)

PT Suparma Tbk (SPMA)

PT Fajar Surya Wisesa Tbk (FASW)

PT Alkindo Naratama Tbk (ALDO)

PT Kedawung Setia Industrial Tbk (KDSI)

PT Kertas Basuki Rachmat Indonesia Tbk (KBRI)

PT Primarindo Asia Infrastructure Tbk

PT Asia Pacific Investama Tbk

PT Star Paper Supply Tbk

PT Paperocks Indonesia Tbk…

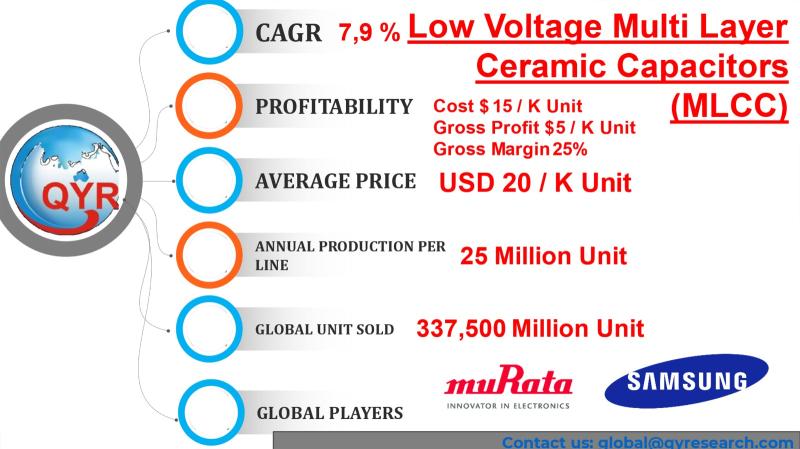

Low-Voltage MLCCs Enter a Structural Inflection: Capacity Discipline, AI Demand, …

The global low-voltage MLCC market is entering a non-linear value inflection driven by a transition away from pure shipment growth toward capital efficiency, yield optimization, and advanced node miniaturization. While historical cycles were dictated by consumer electronics volume particularly smartphones and PCs the current phase is increasingly shaped by structural demand from automotive electrification, AI infrastructure, and high-frequency communication modules. This transition is compressing supply elasticity, as scaling production is…

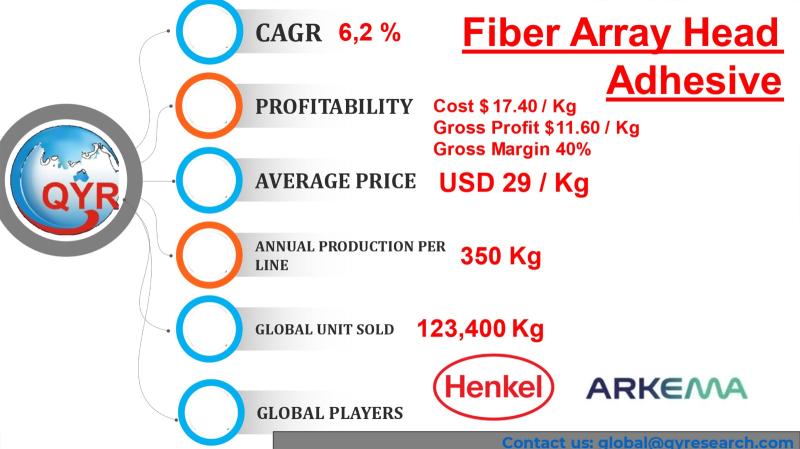

Optical Interconnect Scaling Drives Structural Repricing in Fiber Array Head Adh …

The global fiber array head adhesive market is entering a non-linear value inflection, driven less by volumetric expansion and more by precision-driven capital intensity. While total addressable demand remains niche in absolute terms, the transition toward high-density optical interconnects particularly in data centers, AI clusters, and 5G/6G backhaul has materially increased the performance requirements of adhesives used in fiber array alignment. This shift is forcing manufacturers to invest in higher-purity…

2026 Global NVMe Storage Enclosure Market Research Report

1. Product Definition

An NVMe Storage Enclosure is a dedicated hardware system designed to house and manage multiple NVMe (Non-Volatile Memory Express) solid-state drives (SSDs), providing high-speed storage expansion for servers, data centers, or enterprise storage systems.

The enclosure typically connects to host systems via PCIe or other high-bandwidth interfaces, supporting hot-swappable drives, efficient thermal management, and centralized storage control. NVMe storage enclosures are primarily used to deliver ultra-low latency and high…

More Releases for HDPE

Beyond Numbers: Understanding PCR HDPE Market Size

In this comprehensive report, analysts conduct an in-depth study of the global PCR HDPE market, delving into key factors such as drivers, challenges, recent trends, opportunities, advancements, and the competitive landscape. Utilizing research techniques like PESTLE and Porter's Five Forces analysis, the researchers provide a clear understanding of both the current and future scenarios within the global PCR HDPE industry. Accurate data on PCR HDPE production, capacity, price, cost, margin,…

Latest Trends In Global Recycled HDPE Market

Recycled HDPE, or High-Density Polyethylene, is a versatile and environmentally friendly material derived from the recycling of plastic products made from HDPE.

HDPE is a type of plastic commonly used for items like milk jugs, detergent bottles, and plastic bags. The recycling process for HDPE involves collecting, cleaning, and melting down these used plastic items to create new products.

Request for Sample@

https://mobilityforesights.com/contact-us/?report=20042

Recycled HDPE is valued for its durability, resistance…

Geomembrane manufacturer, HDPE geomembrane factory, geosynthetics supplier

MTTVS® Geosynthetics company specializes in research ,development,production,promotion and application of geosynthetics.And is the world's leading supplier of geosynthetics. Founded in 2014,located in Shandong China.With ISO9001,ISO14001,ISO45001 international authoritative management system certification of powerful large manufucture.We have more than 10 international advanced equipment production lines and a huge professional engineering and technical team.and has successfully consolideated and developed core markets to maximize value for customers.Through the processing of synthetic raw materials.we develop,manufacture…

hdpe geomembrane liner fabric manufacturer,geotextile manufacturer Company,HDPE …

GD Geosynthetics Company is a comprehensive processing enterprise of composite geosynthetics, geotextiles, geomembranes, geogrids, geounits, three-dimensional composite drainage nets, ecological bags, drainage boards. High-level management, high-level scientific research team, conform to the trend of domestic and international chemical fiber market, constantly innovate and update, cater to the market and meet the needs of consumers. Gained the trust of consumers.

Geosynthetics are widely used in anti-seepage treatment of roads, bridges, reservoirs, tunnels,…

Research Focuses on Global HDPE Geomembrane

HDPE Geomembrane Report by Material, Application, and Geography – Global Forecast to 2021 is a professional and in-depth research report on the world's major regional market conditions, focusing on the main regions (North America, Europe and Asia-Pacific) and the main countries (United States, Germany, united Kingdom, Japan, South Korea and China).

The report firstly introduced the HDPE Geomembrane basics: definitions, classifications, applications and market overview; product specifications; manufacturing processes; cost structures,…

Global HDPE Decking Market Research Report 2017

HDPE Decking Revenue, means the sales value of HDPE Decking This report studies HDPE Decking in Global market, especially in North America, Europe, China, Japan, Southeast Asia and India, focuses on top manufacturers in global market, with capacity, production, price, revenue and market share for each manufacturer, covering UPM Kymmene Universal Forest Products Advanced Environmental Recycling Technologies Fiberon Azek Building Products Cardinal Building Products Certainteed Corporation Duralife Decking and Railing…