Press release

Phosphorus Scarcity Meets Circularity: Scaling a 10.9% CAGR Opportunity in Recovered Fertilizers

This shift is particularly visible in the increasing deployment of municipal-scale nutrient recovery systems and industrial symbiosis models, where wastewater treatment plants, livestock operations, and food processing facilities are integrated into phosphorus recovery networks. Capital expenditure per facility has increased significantly, but so has the ability to capture higher-value granulated end-products with consistent nutrient profiles and lower contaminants.

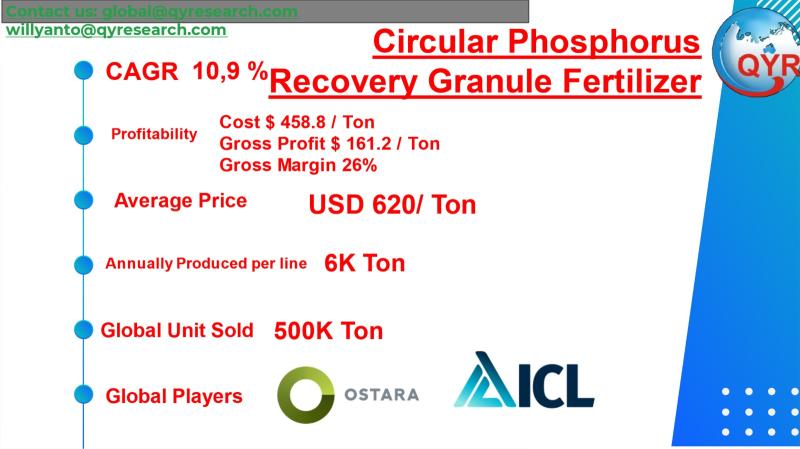

For institutional investors, the investment thesis is anchored in three structural levers: regulatory compulsion (especially in Europe and parts of Asia), supply security amid phosphate rock concentration risks, and premium pricing for sustainable fertilizers. With gross margins stabilizing around 26% and scalable production lines reaching 6,000 tons annually, the sector is increasingly aligned with infrastructure-like returns rather than traditional agri-input volatility.

Global Overview

The global circular phosphorus recovery granule fertilizer market was valued at USD 310 million in 2025 and is projected to reach USD 640 million by 2032, expanding at a CAGR of 10.9%. Total global sales volume is estimated at approximately 500,000 tons, with an average selling price (ASP) of USD 620 per ton.

Core demand drivers are centered on regulatory enforcement of phosphorus discharge limits, increasing volatility in phosphate rock supply (dominated by a few countries such as Morocco and China), rising demand for sustainable agriculture inputs, and municipal investment in wastewater nutrient recovery infrastructure.

A critical driver is the tightening of nutrient runoff regulations, particularly in regions facing eutrophication challenges. Additionally, carbon accounting frameworks are increasingly recognizing circular fertilizers as lower-emission alternatives, further supporting adoption among large-scale agricultural operators.

Regional Consumption Dynamics (APAC & SEA Focus)

Asia-Pacific is emerging as the fastest-growing consumption hub, driven by structural fertilizer demand and increasing waste management investments. China leads in installed phosphorus recovery capacity, supported by central government mandates on wastewater reuse and sludge treatment. Japan and South Korea are early adopters of struvite-based fertilizers due to stringent nutrient discharge standards.

In Southeast Asia, the market is at an earlier stage but accelerating. Indonesia is investing in municipal wastewater upgrades and palm oil waste valorization, creating a large addressable feedstock base. Vietnam and Thailand are integrating circular nutrient strategies into agricultural modernization programs, particularly in rice and horticulture sectors. Malaysia is leveraging livestock and palm biomass streams for nutrient recovery, while Singapore is focusing on high-efficiency urban wastewater recycling systems, positioning itself as a technology hub rather than a volume producer.

The regions structural inflection is tied to import dependency on phosphate fertilizers, making circular recovery a strategic priority rather than purely an environmental initiative.

Production and Supply Chain

Value capture in the circular phosphorus fertilizer chain is concentrated at three nodes: feedstock aggregation (waste streams), recovery technology systems, and granulation/upgrading processes. Among these, the highest margin expansion occurs at the granulation and product standardization stage, where recovered phosphorus is converted into market-ready fertilizers with consistent nutrient content.

Gross margins typically range between 22% and 28%, with leading operators achieving around 26%, supported by controlled input costs (often negative-cost waste streams) and premium pricing for sustainable products.

Asia plays a central role in scaling production. China dominates equipment manufacturing and system integration, reducing capital costs globally. Japan leads in high-purity recovery technologies, particularly struvite crystallization. Southeast Asia contributes primarily through feedstock availabilityespecially agricultural residues, palm oil waste, and municipal sludgemaking countries like Indonesia and Malaysia critical upstream suppliers in the global value chain.

Latest Technological Developments

Recent advancements are focused on improving recovery efficiency, reducing contaminants, and enabling scalable deployment across diverse waste streams.

Integration of AI-driven process control systems in wastewater treatment plants to optimize phosphorus precipitation and recovery yield in real time

Development of advanced struvite crystallization reactors with improved crystal size control for direct granulation compatibility

Thermal ash processing technologies enabling phosphorus recovery from sewage sludge incineration with reduced heavy metal content

Modular recovery units designed for decentralized deployment in agricultural and livestock operations

Hybrid bio-chemical recovery systems combining microbial digestion with chemical precipitation to increase yield efficiency

Enhanced granulation techniques using binders that improve nutrient release profiles and storage stability

Market Breakdown Categories

Technology Type includes struvite crystallization, thermal ash recovery, wet chemical extraction, and bio-based recovery systems. Struvite-based systems dominate due to scalability and compatibility with wastewater treatment infrastructure, while ash-based technologies are gaining traction in regions with high sludge incineration rates.

Product Category is segmented into struvite-based, ash-based, bio-based, and other hybrid formulations. Struvite-based granules are widely adopted due to their slow-release properties, while ash-based products are positioned as substitutes for conventional phosphate fertilizers.

Market Segment spans agriculture, municipal, landscaping, and horticulture. Agriculture accounts for the largest share, but municipal applications are growing rapidly as cities seek to close nutrient loops within urban ecosystems.

Application includes soil application, foliar spraying, fertigation, seed coating, and other specialized uses. Soil application dominates due to compatibility with existing farming practices, while fertigation is expanding in high-value crops.

Feedstock Source Segmentation includes animal manure, food waste, wastewater sludge, and crop residue. Wastewater sludge remains the primary source due to consistent volume and centralized collection systems.

Nutrient Concentration Level categorizes products into low, medium, high, and ultra-high phosphorus content, influencing application efficiency and pricing.

End-User Scale differentiates between smallholder farms, commercial agriculture, municipal utilities, and industrial agriculture operators.

Distribution Channel includes direct industrial supply, agricultural cooperatives, government procurement programs, and specialty fertilizer distributors.

Product Pricing Variations

Pricing varies significantly depending on purity, nutrient concentration, and production technology. Struvite-based fertilizers such as those produced by Ostara (e.g., Crystal Green) typically range from USD 550 to 750 per ton, reflecting high purity and controlled nutrient release, making them suitable for premium agriculture markets.

Ash-based phosphorus fertilizers from companies like Outotec (Metso) range between USD 400 to 600 per ton, as they are derived from sludge incineration and require additional processing to reduce contaminants, positioning them closer to conventional phosphate fertilizers in pricing.

Bio-based recovered phosphorus products developed by companies such as Veolia are priced between USD 600 to 800 per ton, supported by integrated waste management systems and higher environmental compliance standards.

Lower-grade recovered phosphorus fertilizers from municipal sludge applications in emerging markets can range from USD 300 to 500 per ton, reflecting variability in nutrient composition and limited processing.

High-purity specialty granules used in horticulture and controlled-environment agriculture can exceed USD 800 to 1,000 per ton, particularly when produced with advanced crystallization and coating technologies.

Global Top 30 Key Companies in the Circular Phosphorus Recovery Granule Fertilizer Market

OCP (Casablanca, Morocco)

ICL Group (Israel, Tel Aviv)

The Mosaic Company (Florida, US)

Ostara Nutrient Recovery Technologies (Vancouver, Canada)

Veolia Environment (Paris, France)

Suez Group (Paris, France)

Yara International (Oslo, Norway)

Kurita Water Industries (Tokyo, Japan)

Hitachi Zosen Corporation (Osaka, Japan)

Mitsubishi Chemical Group (Tokyo, Japan)

Sumitomo Chemical (Tokyo, Japan)

EasyMining (Stockholm, Sweden)

Kemira Oyj (Helsinki. Finland)

SusPhos B.V. (Friesland. Netherlands)

Kubota Corporation (Osaka. Japan)

Nutrient Recovery and Upcycling (NRU) LLC (Wisconsin. US)

Gelsenwasser AG (North Rhine-Westphalia. Germany)

CNP-Technology Water and Biosolids (North Rhine-Westphalia. Germany)

Multiform Harvest Inc. (Washington. US)

Yuntianhua Group (Yunnan, China)

Guizhou Phosphate Chemical Group (Guizhou, Italy)

Hubei Xinyangfeng Fertilizer Co., Ltd. (Hubei, China)

Hubei Xingfa Chemicals Group Co., Ltd. (Hubei, China)

China Everbright Environment Group (Hong Kong, China)

Remondis (Lunen, Germany)

Toshiba Infrastructure Systems (Japan, Tokyo).

Veolia (Aubervillers, France)

Seraplant (Saxony Anhalt, Germany)

Metso Outotec (Finland, Helsinki)

Italmatch (Genoa, Italy)

Chapter Outline

Chapter 1: Introduces the report scope of the report, executive summary of different market segments (by region, product type, application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the market and its likely evolution in the short to mid-term, and long term.

Chapter 2: key insights, key emerging trends, etc.

Chapter 3: Manufacturers competitive analysis, detailed analysis of the product manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc.

Chapter 4: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc.

Chapter 5 & 6: Sales, revenue of the product in regional level and country level. It provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and market size of each country in the world.

Chapter 7: Provides the analysis of various market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 8: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 9: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 10: The main points and conclusions of the report.

Related Report Recommendation

Global Circular Phosphorus Recovery Granule Fertilizer Market Research Report 2026

https://www.qyresearch.com/reports/6455985/circular-phosphorus-recovery-granule-fertilizer

Global Circular Phosphorus Recovery Granule Fertilizer Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/6455986/circular-phosphorus-recovery-granule-fertilizer

Global Circular Phosphorus Recovery Granule Fertilizer Market Outlook, InDepth Analysis & Forecast to 2032

https://www.qyresearch.com/reports/6455987/circular-phosphorus-recovery-granule-fertilizer

Circular Phosphorus Recovery Granule Fertilizer- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

https://www.qyresearch.com/reports/6455988/circular-phosphorus-recovery-granule-fertilizer

Global Phosphorus Fertilizer Market Research Report 2026

https://www.qyresearch.com/reports/6264034/phosphorus-fertilizer

Global Phosphorus Starter Fertilizer Market Research Report 2026

https://www.qyresearch.com/reports/5532976/phosphorus-starter-fertilizer

Global Nitrogen, Phosphorus and Potassium Water Soluble Fertilizer Market Research Report 2026

https://www.qyresearch.com/reports/5703283/nitrogen--phosphorus-and-potassium-water-soluble-fertilizer

Global Fertilizers Market Research Report 2026

https://www.qyresearch.com/reports/5536038/fertilizers

Global Dry Fertilizer Market Research Report 2026

https://www.qyresearch.com/reports/5981130/dry-fertilizer

Global Bio-Fertilizers Market Research Report 2026

https://www.qyresearch.com/reports/5522211/bio-fertilizers

About QY Research

QY Research has established close partnerships with over 71,000 global leading players. With more than 20,000 industry experts worldwide, we maintain a strong global network to efficiently gather insights and raw data.

Our 36-step verification system ensures the reliability and quality of our data. With over 2 million reports, we have become the world's largest market report vendor. Our global database spans more than 2,000 sources and covers data from most countries, including import and export details.

We have partners in over 160 countries, providing comprehensive coverage of both sales and research networks. A 90% client return rate and long-term cooperation with key partners demonstrate the high level of service and quality QY Research delivers.

More than 30 IPOs and over 5,000 global media outlets and major corporations have used our data, solidifying QY Research as a global leader in data supply. We are committed to delivering services that exceed both client and societal expectations.

Contact Information:

Tel: +1 626 2952 442 (US) ; +86-1082945717 (China)

+62 896 3769 3166 (Whatsapp)

Email: willyanto@qyresearch.com; global@qyresearch.com

Website: www.qyresearch.com

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Phosphorus Scarcity Meets Circularity: Scaling a 10.9% CAGR Opportunity in Recovered Fertilizers here

News-ID: 4475161 • Views: …

More Releases from QY Research

Top 30 Indonesian Chewing Gum Public Companies Q3 2025 Revenue & Performance

1) Overall companies performance (Q3 2025 snapshot)

PT Yupi Indo Jelly Gum Tbk (YUPI)

PT Mayora Indah Tbk (MYOR)

PT Indofood CBP Sukses Makmur Tbk (ICBP)

PT Indofood Sukses Makmur Tbk (INDF)

PT Garudafood Putra Putri Jaya Tbk (GOOD)

PT Siantar Top Tbk (STTP)

PT Sekar Laut Tbk (SKLT)

PT Campina Ice Cream Industry Tbk (CAMP)

PT Akasha Wira International Tbk (ADES)

PT Sariguna Primatirta Tbk (CLEO)

PT Ultrajaya Milk Industry Tbk (ULTJ)

PT Multi Bintang Indonesia Tbk (MLBI)

PT Delta Djakarta Tbk…

From Waste Treatment to Value Capture: The Industrialization of Bio-Enzymatic Od …

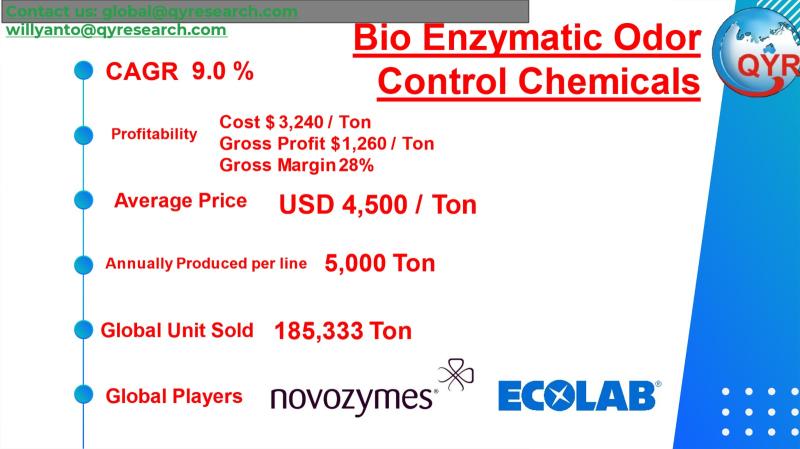

The global Bio Enzymatic Odor Control Chemicals market is undergoing a structural inflection as it transitions from low-cost, volume-driven commodity deodorization toward higher-value, bioengineered formulations. While the market remains relatively small at USD 834 million in 2025, its trajectory toward USD 1,521 million by 2032 (9.0% CAGR) reflects a shift in capital allocation from bulk chemical production into fermentation-based, IP-driven enzyme systems. This shift introduces higher barriers to entry, longer…

Capital Intensity Rising: How Engineered Rubber Systems Are Redefining Industria …

The global abrasion-resistant rubber products market is entering a non-linear value inflection phase as procurement shifts from commoditized bulk materials toward engineered, lifecycle-optimized solutions. Historically driven by tonnage demand from mining and cement sectors, the market is increasingly defined by performance metrics such as wear life, downtime reduction, and total cost of ownership. This transition is structurally favoring producers with compounding expertise in formulation chemistry, precision curing, and application-specific design.

The…

Top 30 Indonesian Ethanol Public Companies Q3 2025 Revenue & Performance

1) Overall companies performance (Q3 2025 snapshot)

PT Molindo Raya Industrial Tbk (MRIN)

PT Indo Acidatama Tbk (SRSN)

PT Tunas Baru Lampung Tbk (TBLA)

PT Astra Agro Lestari Tbk (AALI)

PT Sinar Mas Agro Resources and Technology Tbk (SMAR)

PT Wilmar Cahaya Indonesia Tbk (CEKA)

PT Japfa Comfeed Indonesia Tbk (JPFA)

PT Bakrie Sumatera Plantations Tbk (UNSP)

PT Dharma Satya Nusantara Tbk (DSNG)

PT PP London Sumatra Indonesia Tbk (LSIP)

PT Salim Ivomas Pratama Tbk (SIMP)

PT BISI International Tbk (BISI)

PT Eagle…

More Releases for Fertilizer

Organic Waste-to-Fertilizer: Europe's Quiet Revolution in Decentralized Organic …

The organic fertilizer market has experienced steady growth in recent years, driven by increasing environmental regulations, consumer preference for chemical-free produce, and a robust shift toward regenerative agriculture. While traditional market insights often emphasize the role of large-scale composting and commercial bio-based fertilizers, a quieter revolution is taking shape-decentralized organic fertilizer production from urban and agri-industrial waste. This lesser-discussed segment is reshaping local supply chains, supporting circular economy goals, and…

Rising Fertilizer Production Sparks Growth In The Fertilizer Catalyst Market: A …

The Fertilizer Catalyst Market Report by The Business Research Company delivers a detailed market assessment, covering size projections from 2025 to 2034. This report explores crucial market trends, major drivers and market segmentation by [key segment categories].

What Is the Current Fertilizer Catalyst Market Size and Its Estimated Growth Rate?

Over recent years, the fertilizer catalyst market has seen significant growth. The market, which was worth $3.03 billion in 2024, is projected…

Key Influencer in the Fertilizer Catalyst Market 2025: Rising Fertilizer Product …

Which drivers are expected to have the greatest impact on the over the fertilizer catalyst market's growth?

The growth of the fertilizer catalyst market is anticipated to be driven by the rising production of fertilizers. Fertilizers, which are chemical substances provided to crops to enhance their yield, incorporate catalysts in their production process to minimize cost and increase quantity. In the context of the fertilizer industry, catalysts prove advantageous. For example,…

Agriculture Potassium Fertilizer Market Industry Research Report| Koch Fertilize …

‘Agriculture Potassium Fertilizer Market’ study by “Reportsweb” provides details about the market dynamics affecting the market, Market scope, Market segmentation and overlays shadow upon the leading market players highlighting the favorable competitive landscape and trends prevailing over the years.

Based on the Agriculture Potassium Fertilizer market development status, competitive landscape and development model in different regions of the world, this report is dedicated to providing niche markets, potential risks and comprehensive…

Ammonium Thiosulfate Fertilizer Market Future Trends to 2027 – Juan Messina S. …

Ammonium thiosulfate is an inorganic compound which is a nitrification inhibitor, reducing nitrogen loss by inhibiting or slowing the nitrification process of ammonium converting to nitrate. Ammonium thiosulfate fertilizer is an excellent source of ammoniacal nitrogen that is quickly absorbed by the plant. This results in greener turf, even at low soil temperatures. It is used when a liquid type of ammoniacal nitrogen source and sulfur are required for the…

Soluble Fertilizer Market Report 2018 Companies included Agrium Inc., Israel Che …

We have recently published this report and it is available for immediate purchase. For inquiry Email us on: jasonsmith@marketreportscompany.com *********

This market study includes data about consumer perspective, comprehensive analysis, statistics, market share, company performances (Stocks), historical analysis 2012 to 2017, market forecast 2018 to 2025 in terms of volume, revenue, YOY growth rate, and CAGR for the year 2018 to 2025, etc. The report also provides…