Press release

High-Refresh, High-Margin: OLED Driver Board Market Transitions to Performance-Led Growth

Institutional capital is now gravitating toward companies that control critical upstream components such as OLED driver ICs and firmware ecosystems rather than low-margin board assembly. The transition is further reinforced by consolidation across the supply chain and rising capex requirements for automated production lines, where a single fully utilized production line typically delivers approximately 2.54.0 million units annually depending on board complexity and layer count. This structural shift favors scale, IP ownership, and regional manufacturing leverage particularly across Asia-Pacific.

Consumption Market

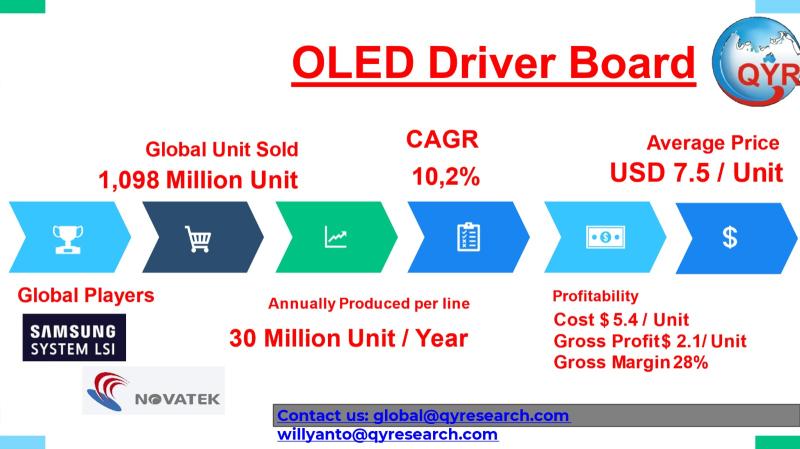

The global OLED driver board market is valued at USD 8,235 million in 2025 and is projected to reach USD 16,251 million by 2032, expanding at a CAGR of 10.2%. At an average selling price of approximately USD 7.5 per unit, total global shipments are estimated at roughly 1,098 million units in 2025, scaling to over 2,166 million units by 2032, reflecting strong downstream demand elasticity.

Core demand drivers include the rapid proliferation of OLED displays in smartphones and wearables, accelerated adoption in automotive cockpit displays and infotainment systems, increasing penetration of OLED in medical imaging and diagnostic devices, and the expansion of industrial HMI (human-machine interface) systems requiring low-power, high-contrast displays.

Regional Consumption Dynamics (APAC & SEA Focus)

Asia-Pacific accounts for over 72% of global OLED driver board consumption, driven by dominant panel manufacturing ecosystems in China, South Korea, and Japan. China continues to lead in volume consumption due to aggressive domestic display capacity expansions and state-backed semiconductor initiatives. South Korea remains a high-value consumption hub, particularly for premium driver boards integrated into flagship OLED panels.

Southeast Asia is emerging as a strategic demand and assembly hub under the China+1 manufacturing diversification strategy. Countries such as Indonesia and Vietnam are scaling electronics assembly operations, particularly for consumer electronics and automotive components, driving localized demand for driver boards. Malaysia and Thailand are strengthening their roles in semiconductor packaging and PCB assembly, while Singapore functions as a regional coordination hub for high-value design and supply chain management. Sovereign-backed initiatives in these countries are incentivizing local electronics ecosystems, thereby accelerating demand for mid-range and customizable OLED driver solutions.

Production and Supply Chain

Value capture within the OLED driver board supply chain is increasingly skewed toward upstream IC design and high-precision manufacturing. While traditional PCB assembly yields gross margins in the range of 18 to 28%, companies with integrated driver IC capabilities and proprietary firmware ecosystems achieve margins between 30 to 45%, with select niche players in high-performance automotive and medical segments approaching 50 to 55%.

China dominates large-scale production capacity, accounting for more than 50% of global output, supported by cost-efficient manufacturing and government incentives. South Korea and Japan retain leadership in high-end driver technologies, particularly for flexible OLED and high-refresh-rate applications. Taiwan plays a critical intermediary role in IC design and advanced packaging.

Within Southeast Asia, Vietnam and Thailand are rapidly scaling PCB assembly and final module integration, benefiting from labor cost advantages and trade diversification. Malaysia remains critical for semiconductor backend processes, while Indonesia is gradually building capabilities in electronics assembly, particularly for domestic consumption and regional exports.

Latest Technological Developments

Recent advancements in OLED driver boards reflect increasing system-level integration and performance optimization:

Integration of AI-driven telemetry modules enabling real-time display calibration and predictive maintenance in industrial and automotive applications.

Development of ultra-low power driver architectures optimized for wearable and IoT devices, reducing energy consumption by up to 20 to 30%.

Adoption of advanced thermal management solutions, including micro heat-dissipation layers and embedded cooling substrates for high-refresh-rate displays.

Transition toward MIPI DSI (Display Serial Interface) dominance, enabling higher bandwidth and lower latency in compact form factors.

Emergence of flexible and foldable display-compatible driver boards with enhanced mechanical durability and signal integrity.

Increasing use of high-density interconnect (HDI) PCB technology to support miniaturization and higher circuit complexity.

Market Breakdown Categories

OLED Driver Board by Technology type segmentation reflects interface standards that define communication efficiency and bandwidth. SPI interface driver boards are widely used in low-power, cost-sensitive applications such as wearables due to their simplicity, while I2C variants serve compact embedded systems requiring moderate data rates. Parallel interface boards are deployed in legacy and industrial systems requiring stable throughput, whereas MIPI interface driver boards dominate high-performance applications such as smartphones and automotive displays due to superior data transfer capabilities.

OLED Driver Board by Product categories differentiate based on performance characteristics. Standard driver boards cater to general-purpose displays with balanced cost-performance ratios. High refresh rate driver boards are designed for gaming, AR/VR, and automotive displays where motion clarity is critical. High grayscale and color accuracy boards are essential for medical imaging and professional displays. Programmable and expandable boards provide flexibility for industrial and custom applications, enabling firmware-level customization.

OLED Driver Board by Size segmentation is defined by display dimensions. OLED Driver Board by Small-size driver boards (≤1.5 inch) are primarily used in wearables and compact IoT devices. Medium-size boards (1.5-5 inch) dominate smartphones and handheld devices, representing the largest volume segment. Large-size boards (>5 inch) are increasingly used in automotive dashboards, industrial panels, and specialized medical equipment.

Application segmentation highlights end-use industries. Consumer electronics remains the largest segment, driven by smartphones and wearables. Automotive applications are the fastest-growing segment due to digital cockpit adoption. Medical applications require high precision and reliability, while industrial applications focus on durability and long lifecycle performance.

Product Pricing Variations

Pricing varies significantly based on interface type, performance specification, size, and end-use requirements. Entry-level SPI-based small OLED driver boards, such as modules supplied by companies like Raystar Optronics, typically range from USD 2.5 to USD 5.0 per unit, reflecting their use in simple wearable and IoT devices with limited resolution requirements.

Mid-range I2C and parallel interface boards produced by manufacturers such as Truly International or WiseChip Semiconductor generally fall within the USD 5.0 to USD 9.0 range, commonly used in consumer electronics and basic industrial displays where moderate performance is sufficient.

High-performance MIPI interface driver boards from companies such as Samsung Display or LG Display are priced between USD 9.0 and USD 15.0, driven by their use in smartphones, automotive displays, and high-resolution applications requiring fast data transfer and superior image quality.

Specialized high-refresh-rate or high-color-accuracy driver boards, particularly those designed for automotive or medical applications by firms such as Japan Display Inc. or BOE Technology Group, can command prices between USD 15.0 and USD 25.0 per unit, reflecting stringent performance, reliability, and certification requirements.

Global Top 30 Key Companies in the OLED Driver Board Market

Samsung Electronics (Gyeonggi, South Korea)

Novatek Microelectronics (Hsinchu. Taiwan)

Synaptics Incorporated (California, US)

Himax Technologies (Tainan. Taiwan)

Silicon Works (Daejon, South Korea)

MagnaChip Semiconductor (Seoul. South Korea)

Fitipower Integrated Technology (Hsinchu, Taiwan)

Raydium Semiconductor (Hsinchu. Taiwan)

Solomon Systech (Hong Kong)

Parade Technologies (Taipei. Taiwan)

MediaTek Inc. (Hsinchu. Taiwan)

ROHM Semiconductor (Kyoto, Japan)

Analog Devices Inc. (Massachusetts, US)

Ilitek Technology Corp (Hsinchu, Taiwan)

FocalTech Systems Co., Ltd. (Hsinchu. Taiwan)

BOE Technology Group (Beijing, China)

TCL CSOT (Guangdong, China)

Chipone Technology Corp. (Beijing, China)

EverDisplay Optronics (Shanghai, China)

Beijing Chiponeic Technology Co., Ltd. (Beijing, China)

LG Display Co., Ltd. (Seoul, South Korea)

LX Semicon (Daejeon. South Korea

Japan Display Inc. (JDI) (Tokyo. Japan)

Sharp Corporation (Osaka. Japan)

Sony Group Corporation (Tokyo. Japan)

Visionox Technology (Jiangsu. China)

Sitronix Technology (Hsinchu, Taiwan)

Tohoku Pioneer Corporation (Yamagata, Japan)

Lumiotec (Yamagata, Japan)

Mixel Inc (California, US)

Chapter Outline

Chapter 1: Introduces the report scope of the report, executive summary of different market segments (by region, product type, application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the market and its likely evolution in the short to mid-term, and long term.

Chapter 2: key insights, key emerging trends, etc.

Chapter 3: Manufacturers competitive analysis, detailed analysis of the product manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc.

Chapter 4: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc.

Chapter 5 & 6: Sales, revenue of the product in regional level and country level. It provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and market size of each country in the world.

Chapter 7: Provides the analysis of various market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 8: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 9: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 10: The main points and conclusions of the report.

Related Report Recommendation

Global OLED Driver Board Market Research Report 2026

https://www.qyresearch.com/reports/6266791/oled-driver-board

Global OLED Driver Board Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/6266792/oled-driver-board

Global OLED Driver Board Market Outlook, InDepth Analysis & Forecast to 2032

https://www.qyresearch.com/reports/6266793/oled-driver-board

OLED Driver Board- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

https://www.qyresearch.com/reports/6266794/oled-driver-board

Global OLED Bias Driver ICs Market Research Report 2026

https://www.qyresearch.com/reports/6264397/oled-bias-driver-ics

Global OLED Display Driver IC Market Research Report 2026

https://www.qyresearch.com/reports/6011864/oled-display-driver-ic

Global OLED Driver IC Foundry Market Research Report 2026

https://www.qyresearch.com/reports/5692228/oled-driver-ic-foundry

Global LCD & OLED Driver IC Testers Market Research Report 2026

https://www.qyresearch.com/reports/6247046/lcd---oled-driver-ic-testers

Global Flexible OLED Panel Driver IC Market Research Report 2026

https://www.qyresearch.com/reports/5882745/flexible-oled-panel-driver-ic

Global OLED Driver IC Packaging and Testing Market Research Report 2026

https://www.qyresearch.com/reports/6247121/oled-driver-ic-packaging-and-testing

About QY Research

QY Research has established close partnerships with over 71,000 global leading players. With more than 20,000 industry experts worldwide, we maintain a strong global network to efficiently gather insights and raw data.

Our 36-step verification system ensures the reliability and quality of our data. With over 2 million reports, we have become the world's largest market report vendor. Our global database spans more than 2,000 sources and covers data from most countries, including import and export details.

We have partners in over 160 countries, providing comprehensive coverage of both sales and research networks. A 90% client return rate and long-term cooperation with key partners demonstrate the high level of service and quality QY Research delivers.

More than 30 IPOs and over 5,000 global media outlets and major corporations have used our data, solidifying QY Research as a global leader in data supply. We are committed to delivering services that exceed both client and societal expectations.

Contact Information:

Tel: +1 626 2952 442 (US) ; +86-1082945717 (China)

+62 896 3769 3166 (Whatsapp)

Email: willyanto@qyresearch.com; global@qyresearch.com

Website: www.qyresearch.com

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release High-Refresh, High-Margin: OLED Driver Board Market Transitions to Performance-Led Growth here

News-ID: 4438465 • Views: …

More Releases from QY Research

Structural Inflection in High-Barrier Films: Why Investors Are Repricing PVC/PCT …

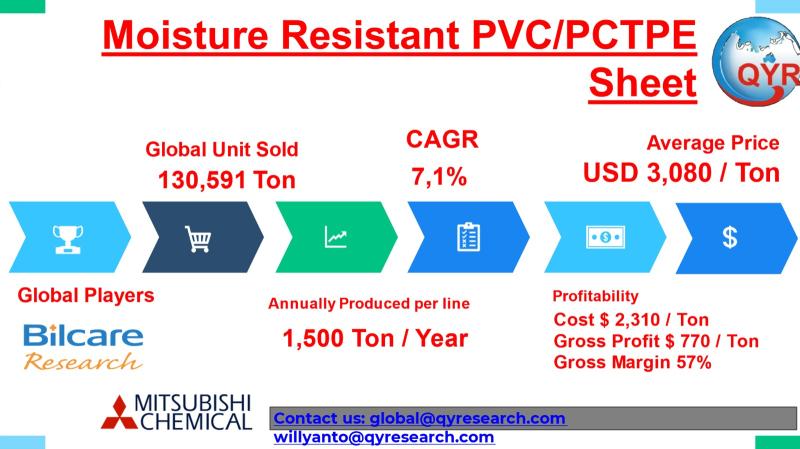

The global moisture-resistant PVC/PCTFE sheet market is entering a non-linear value inflection, shifting from a historically volume-driven commodity plastics segment into a capital-intensive, performance-materials category. This transition is underpinned by increasingly stringent pharmaceutical stability requirements, particularly for moisture-sensitive solid-dose drugs, where high-barrier films are becoming mandatory rather than optional. As a result, pricing power is consolidating among technologically capable producers, with average selling prices reaching approximately USD 3,080 per ton…

Natural Colorants at Scale: How Betanin Is Transitioning into a Capital-Intensiv …

The global betanin food color market is undergoing a non-linear value inflection, transitioning from a historically volume-driven agricultural derivative into a capital-intensive, specification-led specialty ingredient. This shift is anchored in tightening regulatory frameworks on synthetic dyes (notably across the EU and parts of Asia), combined with downstream FMCG reformulation cycles led by multinational food and beverage companies. The result is a repricing mechanism where purity, stability, and certification (organic, non-GMO)…

Top 30 Indonesian E-Commerce Public Companies Q3 2025 Revenue & Performance

1) Overall companies performance (Q3 2025 snapshot)

GoTo Gojek Tokopedia Tbk

Bukalapak.com Tbk

Global Digital Niaga Tbk

Matahari Putra Prima Tbk

Erajaya Swasembada Tbk

Sumber Alfaria Trijaya Tbk

Mitra Adiperkasa Tbk

Metrodata Electronics Tbk

Multipolar Technology Tbk

Multipolar Tbk

Global Mediacom Tbk

Elang Mahkota Teknologi Tbk

Surya Citra Media Tbk

DCI Indonesia Tbk

Telkom Indonesia Tbk

XL Axiata Tbk

Indosat Tbk

Sarana Menara Nusantara Tbk

Link Net Tbk

Kioson Komersial Indonesia Tbk

NFC Indonesia…

Top 30 Indonesian Copper Public Companies Q3 2025 Revenue & Performance

1) Overall companies performance (Q3 2025 snapshot)

PT Amman Mineral Internasional Tbk (AMMN)

PT Merdeka Copper Gold Tbk (MDKA)

PT Bumi Resources Minerals Tbk (BRMS)

PT Freeport Indonesia

PT Aneka Tambang Tbk (ANTM)

PT Vale Indonesia Tbk (INCO)

PT Bukit Asam Tbk (PTBA)

PT Adaro Energy Indonesia Tbk (ADRO)

PT Bayan Resources Tbk (BYAN)

PT Indo Tambangraya Megah Tbk (ITMG)

PT Harum Energy Tbk (HRUM)

PT Indika Energy Tbk (INDY)

PT…

More Releases for OLED

OLED Display Tester Market

OLED Display Tester Market Overview

The OLED display tester is a specialized device used to evaluate and test various performance parameters and functions of OLED (Organic Light Emitting Diode, organic light emitting diode) displays. Such testers typically include hardware and software components designed to provide comprehensive testing and analysis capabilities to ensure the quality, performance and reliability of OLED displays.

This report provides a deep insight into the global OLED Display Tester…

OLED ACF Market

The "OLED ACF Market" is expected to reach USD xx.x billion by 2031, indicating a compound annual growth rate (CAGR) of xx.x percent from 2024 to 2031. The market was valued at USD xx.x billion In 2023.

Growing Demand and Growth Potential in the Global OLED ACF Market, 2024-2031

Verified Market Research's most recent report, "OLED ACF Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2023-2030," provides an in-depth examination…

Major Trends in OLED

How the ncreased demand for AR/VR headsets acts as an opportunity for the market?

OLED displays are lighter, thinner, and more flexible as compared to displays based on existing technologies. They emit bright colors. These displays are used in different applications in different sectors. They are used in mobile phones, TVs, wearable devices, etc. Samsung Galaxy series, Huawei P9 Plus, Oppo R9 Plus, Vivo X7 Plus, Xiaomi Redmi 3S, Lenovo Phab2…

Rising Usage of OLED in Mobile Phones to Surge Demand in Global OLED Lighting De …

The surging demand for OLED innovation in the car market is probably going to push the OLED market development in the coming years. The car makers are experiencing a gigantic change concerning the utilization of OLED innovation in display and lighting items in vehicles. These producers are sending OLED dashboards for the purpose of navigation and OLED video displays for entertainment in vehicles for better picture quality. Additionally, with the…

Global OLED Lighting Market Research Report 2017- OLED, Konica Minolta, LG Chem, …

Global OLED Lighting Market Report 2017 presents a professional and deep analysis on the present state of OLED Lighting Market 2017.

In the first part, OLED Lighting Market study deals with the comprehensive overview of the OLED Lighting market, which consists of definitions, a wide range of applications, classifications and a complete OLED Lighting industry chain structure. The global OLED Lighting market analysis further consists…

OLED Display Market - Inherent Advantages of OLED Displays to Override Higher Co …

The competitive landscape of the global OLED displays market is highly oligopolistic in nature, according to Transparency Market Research (TMR). Samsung Electronics, which has been one of the pioneers when it comes to advances in LED and OLED technology, held over 70% of the market in 2011 and collectively accounted for 84.4% of the market along with Visionox and WiseChip.

The wide-ranging operation spectrum of Samsung Electronics has allowed the…