Press release

Fabric Waste Recycling Plant DPR & Unit Setup - 2026: Demand Analysis and Project Cost

Market Overview and Growth Potential:

The global fabric waste recycling market is primarily driven by rising textile waste generation and increasing regulatory pressure to divert textiles from landfills. According to UNEP, around 92 million tons of textile waste are generated worldwide each year. Governments are implementing extended producer responsibility (EPR) frameworks and mandatory separate textile collection systems, encouraging the development of organized recycling infrastructure. Growing sustainability commitments from fashion and apparel brands are also accelerating demand for recycled fibers, particularly textile-to-textile recycled polyester and regenerated cellulosic materials. Asia Pacific holds the largest market share at 45.2%, reflecting the concentration of textile manufacturing, waste generation, and recycling capacity in the region. Consumers' preference for environmentally responsible clothing and circular products further strengthens market momentum. Additionally, volatility in virgin fiber prices and concerns over resource depletion are prompting manufacturers to adopt recycled feedstocks to improve supply chain resilience and reduce procurement exposure to commodity price cycles.

Request for Sample Report: https://www.imarcgroup.com/fabric-waste-recycling-plant-project-report/requestsample

Fabric waste recycling is the conversion of pre-consumer textile waste (cutting scraps, off-spec fabric, and yarn waste) and post-consumer textiles (discarded clothing and household textiles) into reusable materials such as fibers, yarns, nonwovens, insulation, wiping cloths, or regenerated polymer and cellulose feedstocks for new textiles. Recycling routes are commonly grouped into mechanical recycling and chemical or regenerative recycling. Key quality determinants include feedstock composition covering mono-material versus blends, contamination from dyes, finishes, and elastane, fiber length retention, and the ability to sort by material type. Modern systems increasingly combine automated identification and sorting, controlled pre-treatment, and closed-loop recovery to produce consistent outputs that meet textile-grade specifications.

Separate textile collection requirements and producer responsibility frameworks are increasing organized collection and sorting volumes, improving feedstock security for recyclers. Large brands are shifting from bottle-based recycled polyester toward textile-to-textile solutions and signing supply partnerships, helping recyclers de-risk demand and scale plants. New facilities and technology hubs are moving from pilot to industrial scale, improving confidence in sorting, purification, and regeneration technologies for complex textile waste streams. Local recycling reduces dependency on virgin raw materials, improves lead times, and supports compliance documentation across apparel and industrial supply chains - all of which are creating durable commercial tailwinds for well-positioned fabric waste recycling operators.

Plant Capacity and Production Scale:

The proposed fabric waste recycling facility is designed with an annual processing capacity ranging between 10,000-50,000 MT of post-industrial and post-consumer textile waste, enabling economies of scale while maintaining operational flexibility across recycled fiber, recycled polyester and nylon feedstock, regenerated cellulosic fiber, nonwoven felt, insulation panel, automotive acoustic and thermal felt, and wiping cloth product lines for apparel and fashion, home textiles, nonwovens and hygiene, construction and insulation, automotive interiors, industrial wiping and packaging, and fiber and yarn manufacturing end-market applications. This production range supports supply to both large apparel and fashion brands requiring high-volume, certified recycled fiber and textile-to-textile recycled polyester or regenerated cellulose for garment production sustainability targets, and the industrial and construction markets requiring cost-competitive, specification-grade recycled nonwoven felts, insulation panels, and acoustic materials. The capacity range accommodates both mechanical recycling operations producing recycled fibers and yarns for blended textile applications and more advanced chemical recycling and regeneration operations for production of higher-purity, textile-grade recycled polymer and cellulosic fiber outputs.

Speak to an Analyst for Customized Report: https://www.imarcgroup.com/request?type=report&id=45332&flag=C

Financial Viability and Profitability Analysis:

The fabric waste recycling business demonstrates healthy profitability potential under normal operating conditions. The financial projections reveal:

• Gross Profit: 35-45%

• Net Profit: 18-28%

These margins reflect the waste-to-value economics of fabric waste recycling, where low-cost post-industrial and post-consumer textile waste feedstock is converted through collection, sorting and grading, removal of trims and contaminants, shredding and opening, fiber cleaning and blending, carding, spinning and nonwoven forming, and finishing and packaging processes into higher-value recycled fibers, yarns, polymer feedstocks, nonwoven felts, and specialty materials that command meaningful price premiums over incoming waste feedstock cost. Margins are supported by strong and growing demand driven by brand sustainability commitments creating commercially bankable offtake demand for certified circular fiber outputs; the ability to access zero or negative-cost feedstock through brand take-back partnerships and EPR-funded collection programs; growing price premiums for certified textile-to-textile recycled polyester and regenerated cellulose in fashion and apparel markets; and moderate capital investment requirements relative to virgin fiber production creating attractive return on capital metrics. The project demonstrates solid return on investment (ROI) potential with comprehensive financial analysis covering income projections, expenditure projections, break-even points, net present value (NPV), internal rate of return, and detailed profitability and sensitivity analysis. Feedstock quality and composition consistency, sorting accuracy for material type separation, and fiber length retention through mechanical processing are the primary operational variables impacting both recycling process yields and the value grade of finished recycled fiber outputs.

Cost of Setting Up a Fabric Waste Recycling Plant:

Understanding the operating expenditure (OpEx) is crucial for effective financial planning and cost management.

Operating Cost Structure:

The cost structure for a fabric waste recycling plant is primarily driven by:

• Raw Materials: 40-50% of total OpEx

• Utilities: 20-25% of OpEx

• Other Expenses: Including transportation, packaging, salaries and wages, depreciation, taxes, and other expenses

Raw materials - particularly post-industrial and post-consumer textile waste - account for approximately 40-50% of total operating expenses, making feedstock sourcing strategy, collection network development, brand partnership and EPR program participation, and long-term textile waste supply agreement management the central raw material cost management priorities. Feedstock composition - whether pre-consumer cutting scraps with known fiber content and minimal contamination, or post-consumer mixed garments requiring extensive sorting for material type separation - directly determines the achievable recycled fiber quality, process yield, and finished product value grade, with raw material selection and sorting accuracy critically impacting both fabric waste recycling process economics and the ability to produce consistent-quality outputs meeting apparel, industrial, or construction customer specifications. Utilities represent 20-25% of OpEx - driven by the energy requirements of industrial shredding and fiber opening equipment, carding and blending machinery, chemical pre-treatment systems where applied for color removal or contamination reduction, and washing, drying, and finishing operations for cleaned fiber and nonwoven products. In the first year of operations, costs cover raw materials, utilities, depreciation, taxes, packing, transportation, and repairs and maintenance. By the fifth year, the total operational cost is expected to increase substantially due to factors such as inflation, market fluctuations, and potential rises in the cost of key materials.

Capital Investment Requirements:

Setting up a fabric waste recycling plant requires capital investment across baling, sorting, shredding and opening, washing and rinsing, blending and carding, chemical reactor systems where applicable, repolymerization units for chemical recycling routes, spinning or nonwoven forming, and finishing and packaging infrastructure. The total capital investment depends on plant capacity, recycling technology route, and location, covering land acquisition, site preparation, and textile processing infrastructure.

Land and Site Development: The location must offer easy access to key raw materials such as post-industrial and post-consumer textile waste. Proximity to target markets will help minimize distribution costs. The site must have robust infrastructure, including reliable transportation, utilities, and waste management systems. Compliance with local zoning laws and environmental regulations must also be ensured. The site must support textile recycling facility requirements including large covered feedstock receiving and sorting areas with adequate ventilation and dust suppression for textile fiber handling, separate storage zones for sorted feedstock categories and finished recycled fiber and product inventory, wastewater treatment for washing and wet processing effluent streams, and fire suppression systems for textile fiber storage areas.

Machinery and Equipment: Equipment costs for baling systems, sorting units, shredders, washing and rinsing units, blending and carding machines, chemical reactors, and repolymerization units represent a significant capital expenditure category. High-quality machinery tailored for fabric waste recycling must be selected. Essential equipment includes:

• Baling systems - hydraulic baling presses for compaction of collected textile waste into standardized bales for efficient storage, handling, and transportation, with bale weight and density monitoring for consistent feedstock logistics and inventory management across pre-consumer and post-consumer textile waste streams

• Sorting units - manual sorting conveyors, near-infrared (NIR) spectroscopy-based automated fiber identification systems, color sorting cameras, and robotically assisted sorting platforms for classification of incoming textile waste by fiber type (polyester, cotton, nylon, wool, and blends), color, and contamination level to produce sorted feedstock streams suitable for targeted downstream recycling processes

• Shredders and fiber opening machines - industrial rotary shredders for size reduction of textile waste bales to manageable fiber lengths, followed by multi-stage willowing, tearing, and opening machinery for progressive mechanical opening of shredded textile material to individual fiber level while maximizing fiber length retention for downstream carding and spinning applications

• Washing and rinsing units - industrial washer-extractors, continuous open-width washing ranges, or countercurrent rinsing systems for removal of surface contamination, dyes, finishes, and processing aids from opened fiber mass, with chemical pre-treatment dosing for color reduction or decoating where required for production of higher-grade cleaned fiber outputs

• Blending and carding machines - precision gravimetric blending systems for controlled mixing of cleaned recycled fibers at defined composition ratios for product quality consistency, followed by industrial flat or roller carding machines for fiber alignment, further opening, nep removal, and production of continuous fiber web or sliver for downstream spinning or nonwoven forming

• Chemical reactors and dissolution systems - for chemical recycling routes: glycolysis or hydrolysis reactor vessels for depolymerization of polyester waste to monomer intermediates, or dissolution and filtration systems for cellulosic fiber streams using lyocell or viscose process chemistry to produce regenerated fiber-grade polymer or cellulose solution for spinning

• Repolymerization units - polycondensation reactor systems for repolymerization of recycled PET or polyamide monomers from chemical depolymerization to produce recycled polymer chip at defined intrinsic viscosity and color specifications suitable for fiber spinning or as chemical recycling feedstock for virgin polymer replacement

• Spinning and nonwoven forming lines - open-end or ring spinning frames for production of recycled fiber yarns from carded sliver for textile and industrial applications; or airlaid, needlepunch, or thermobond nonwoven production lines for conversion of opened recycled fiber webs into nonwoven felts, insulation batts, and industrial nonwoven products

• Finishing and packaging systems - heat-setting, cutting, baling, or winding equipment for finishing of recycled fiber, yarn, or nonwoven products to customer specification; automated packaging and labeling systems with recycled content certification documentation for supply to apparel, industrial, and construction customers

All machinery must comply with textile processing and recycling industry standards for safety, dust and fire control, and environmental compliance. The recycling technology route selection - between mechanical recycling for lower-cost, higher-volume fiber recovery and chemical or regenerative recycling for higher-purity, textile-grade polymer and cellulosic fiber outputs - will significantly determine the capital investment profile, process technology complexity, and the quality and value of finished recycled material outputs.

Civil Works: Building construction and plant layout should be optimized to enhance workflow efficiency, safety, and minimize material handling. Separate areas for raw material storage, production, quality control, and finished goods storage must be designated. Space for future expansion should be incorporated to accommodate business growth. Large covered receiving and sorting halls with adequate ceiling height for bale handling equipment, ventilated shredding and fiber opening areas with industrial dust extraction and collection systems to manage textile fiber dust, washroom and wet processing areas with waterproof flooring and drainage connected to wastewater treatment, fire-rated storage areas for textile fiber inventory, and effluent treatment plant infrastructure for washing and chemical processing wastewater management are essential civil infrastructure requirements for a fabric waste recycling facility.

Other Capital Costs: Costs associated with land acquisition, construction, and utilities including electricity, water, and effluent treatment infrastructure must be considered in the financial plan. Pre-operative expenses including textile recycling facility operating permits, environmental impact assessment and clearance, GRS (Global Recycled Standard) or equivalent recycled content certification preparation and audit costs, initial working capital for textile waste feedstock procurement and sorted inventory buffer, fiber analysis laboratory instrumentation for incoming feedstock quality verification and finished product quality testing, and brand customer qualification audits are important components of total fabric waste recycling project investment planning.

Buy Now: https://www.imarcgroup.com/checkout?id=45332&method=2175

Major Applications and Market Segments:

Fabric waste recycling outputs serve critical functions across multiple textile, industrial, and construction end-market sectors:

Apparel and Fashion: Recycled fibers and textile-to-textile outputs - including recycled polyester suitable for new garments and regenerated cellulose fibers for apparel blends - are used by fashion and apparel brands to meet recycled content targets and circular product commitments. The apparel and fashion sector is the highest-value end-market for fabric waste recycling outputs, with major brands increasingly specifying textile-to-textile recycled polyester and regenerated cotton or cellulosic fiber to replace bottle-based recycled polyester and virgin cotton in product ranges, supporting growing offtake demand for certified circular fiber from dedicated fabric waste recycling facilities.

Home Textiles: Recycled yarns and nonwovens are converted for use in blankets, rugs, upholstery underlays, and filling materials. The home textiles sector applies mechanically recycled fiber blends and nonwoven products as cost-competitive, sustainable alternatives to virgin fiber inputs in a wide range of household textile products, with growing retailer sustainability procurement requirements driving increasing specification of recycled fiber content in home textile product ranges.

Nonwovens and Hygiene: Recycled fibers are used for industrial nonwovens including wipes and felts, and selected durable nonwoven applications. The nonwovens sector represents a high-volume outlet for mechanically recycled fiber that does not meet apparel-grade fiber length or purity specifications, with recycled fiber nonwoven felts and wipes providing cost-effective performance in industrial cleaning, filtration, and protective packaging applications where recycled fiber content reduces material cost compared to virgin fiber nonwovens.

Construction and Insulation: Mechanically recycled fibers are widely suited for thermal and acoustic insulation and cushioning layers in building construction applications. The construction sector provides a large-volume, growing demand channel for lower-grade recycled fiber that is unsuitable for textile applications, with recycled fiber insulation batts and acoustic panels offering environmental certification benefits under green building rating systems while providing cost-competitive thermal and acoustic performance compared to glass fiber or mineral wool insulation alternatives.

Automotive and Transportation: Recycled textile fibers are used in acoustic felts, trunk liners, headliners, and insulation layers in automotive interior applications. The automotive sector applies needlepunch and thermobond nonwoven felts produced from recycled fiber in a range of interior trim, acoustic management, and thermal insulation applications, with automotive OEMs increasingly specifying recycled fiber content in interior components to support vehicle lifecycle carbon footprint reduction commitments and circular economy product design requirements.

Why Invest in Fabric Waste Recycling?

Several compelling strategic and commercial factors make fabric waste recycling an attractive investment:

Policy-Driven Feedstock Availability: Separate textile collection requirements and producer responsibility frameworks increase organized collection and sorting volumes, improving feedstock security for recyclers. Extended producer responsibility (EPR) legislation being implemented across Europe and other markets is creating financially supported textile collection infrastructure that increases the availability of organized, sorted textile waste feedstock at predictable cost - directly reducing the feedstock procurement risk for fabric waste recycling operations.

Brand Demand for Circular Inputs: Large brands are shifting from bottle-based recycled polyester toward textile-to-textile solutions and signing supply partnerships, helping recyclers de-risk demand and scale plants. The shift by major apparel brands from post-consumer PET bottle recycled polyester to genuine textile-to-textile circular fiber sourcing represents a structural demand transition that creates commercially bankable offtake agreements enabling fabric waste recycling facilities to secure project financing and scale to commercial production with demand certainty.

Waste-to-Value Economics: Recycling converts low-value waste into higher-value fibers and polymers, especially when process yields enable textile-grade outputs and stable offtake agreements are secured. The fundamental economics of fabric waste recycling - converting zero or near-zero-cost textile waste feedstock into specification-grade recycled fibers, yarns, and polymer outputs that command positive market prices - create inherently favorable value creation economics that support competitive margins when production yields and output quality are optimized.

Supply-Chain Resilience and Localization: Local recycling reduces dependency on virgin raw materials, improves lead times, and supports compliance documentation across apparel and industrial supply chains. The growing requirements for supply chain traceability, recycled content certification, and Scope 3 emissions reporting across apparel, industrial, and construction customer procurement frameworks are creating growing demand for locally produced, certified recycled fiber from documented, audited sources - favoring domestic fabric waste recycling operators with verifiable chain-of-custody documentation.

Technology Maturation: New facilities and technology hubs are moving from pilot to industrial scale, improving confidence in sorting, purification, and regeneration technologies for complex textile waste streams. The rapid advancement and commercial scale-up of NIR-based automated textile sorting, chemical depolymerization of polyester, and lyocell-process regeneration of cotton cellulose is progressively expanding the range of textile waste streams that can be economically recycled into textile-grade outputs - increasing the total addressable market and commercial opportunity for fabric waste recycling investors.

Manufacturing Process Excellence:

The fabric waste recycling process involves collection, sorting and grading, removal of trims and contaminants, shredding and opening, fiber cleaning and blending, carding, spinning and nonwoven forming, and finishing and packaging as the primary unit operations. The main production steps include:

• Collection and receiving - intake of pre-consumer textile waste (cutting scraps, off-spec fabric rolls, and yarn waste from garment and textile manufacturers) and post-consumer textiles (discarded clothing and household textiles from retail take-back programs, EPR collection points, and municipal separate collection schemes), with incoming bale weighing, lot recording, and initial visual quality assessment for gross contamination and material type identification

• Sorting and grading - manual and automated sorting of received textile waste by fiber type (polyester, cotton, wool, nylon, and blended), color group, and contamination level using combination of experienced manual sorting operators and NIR spectroscopy-based automated fiber identification systems, producing sorted feedstock streams of defined composition for targeted downstream recycling processing routes

• Removal of trims and contaminants - manual and mechanical removal of zippers, buttons, buckles, elastic, labels, and other non-fiber components from sorted garments and textile waste, with metal detection for hardware removal, and separation of heavily contaminated or non-recyclable material fractions for alternative disposal, to produce clean fiber-rich feedstock suitable for shredding and opening

• Shredding and opening - progressive size reduction of de-trimmed sorted textile waste through industrial rotary shredders and multi-stage willowing, tearing, and fiber opening machinery to convert fabric and garment pieces into individual fibers or fiber bundles while maximizing fiber length retention for downstream processing, with dust extraction and collection systems for textile fiber dust management

• Fiber washing and cleaning - industrial washing and rinsing of opened fiber mass for removal of surface dirt, dyes, finishes, and processing aids, with chemical pre-treatment dosing for color reduction or decoating where required for production of higher-grade cleaned fiber meeting apparel or industrial customer specifications, followed by mechanical dewatering and controlled drying to target moisture content

• Blending and carding - precision gravimetric blending of cleaned recycled fibers from different sorted feedstock lots at defined composition ratios for consistent product quality and fiber content, followed by industrial carding for fiber alignment, further opening, nep and short fiber removal, and production of uniform fiber web or sliver for spinning or nonwoven forming

• Spinning or nonwoven forming - open-end or ring spinning of carded fiber sliver into recycled fiber yarns at defined counts and twist for textile and industrial yarn applications; or airlaid, needlepunch, or thermobond nonwoven web bonding for production of recycled fiber nonwoven felts, insulation batts, and industrial nonwoven products from carded fiber web

• Chemical recycling processing (where applicable) - glycolysis, hydrolysis, or solvent dissolution pre-treatment of sorted polyester or cellulosic fiber fractions for chemical depolymerization or dissolution to produce recycled monomer or polymer solution intermediates, followed by purification, repolymerization or regeneration spinning to produce recycled polymer chip or regenerated fiber at textile-grade purity specifications

• Finishing and quality inspection - heat-setting, cutting, baling, coiling, or winding of finished recycled fiber, yarn, or nonwoven products to customer specification, with fiber length, tenacity, color, and contamination quality testing for finished product batch release, and GRS or equivalent recycled content certification documentation preparation for supply chain traceability compliance

• Packaging and dispatch - baling, bagging, or roll-packing of finished recycled fiber and product outputs with recycled content certification labels, lot traceability documentation, and chain-of-custody records for supply to apparel brand, industrial, and construction customer distribution chains

The complete process flow encompasses unit operations involved, mass balance and raw material requirements, quality assurance criteria, and technical tests throughout the recycling operation. A comprehensive quality management system and recycled content traceability program must be implemented across all stages of operations to ensure consistent recycled fiber and product quality, GRS or equivalent certification compliance, and supply chain documentation supporting apparel, industrial, and construction customer sustainability reporting requirements. Standard operating procedures (SOPs), batch processing records, and feedstock lot traceability from incoming textile waste collection through sorting, processing, and finished product dispatch must be maintained throughout all production stages.

Industry Leadership:

The global fabric waste recycling industry is served by a combination of specialist textile recycling companies, large fiber and materials groups investing in circular feedstock capabilities, and technology developers scaling advanced chemical recycling and regeneration processes. Key industry players include:

• Worn Again Technologies

• Lenzing Group

• Birla Cellulose

• BLS Ecotech

• The Woolmark Company

• Ecotex Group

These companies serve diverse end-use sectors including apparel and fashion, home textiles, nonwovens and hygiene, construction and insulation, automotive interiors, industrial wiping and packaging, and fiber and yarn manufacturing, with leading players investing continuously in advanced sorting technology, chemical recycling process development, brand partnership and offtake agreement expansion, and recycled content certification programs to maintain competitive positions across the rapidly growing global fabric waste recycling market.

Recent Industry Developments:

December 2025: Indore Municipal Corporation (IMC) in India began building a waste cloth processing plant at the Devguradia trenching ground, aimed at handling large volumes of discarded garments at the city's zone-wise Three-R Collection Centers and 'Neki ki Deewar'. The INR 2 crore plant, developed under a public-private partnership model, will convert unusable clothing into yarn for reuse, supporting the city's Reduce, Reuse, Recycle initiative - demonstrating growing municipal investment in organized textile waste recycling infrastructure in India.

January 2025: Pune Municipal Corporation announced plans to set up the city's first dedicated textile waste processing facility to handle the roughly 100-125 tons of textile waste generated daily. The plant officials estimated the project cost to be about INR 3-4 crore, with the facility designed to process materials such as clothes, mattresses, cushions, leather goods, and footwear - helping prevent pollution and improving waste management efficiency while creating a model for urban textile waste recycling infrastructure across Indian cities.

Browse Full Report: https://www.imarcgroup.com/fabric-waste-recycling-plant-project-report

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company excels in understanding its client's business priorities and delivering tailored solutions that drive meaningful outcomes. We provide a comprehensive suite of market entry and expansion services. Our offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape, and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: (+1-201-971-6302)

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Fabric Waste Recycling Plant DPR & Unit Setup - 2026: Demand Analysis and Project Cost here

News-ID: 4420418 • Views: …

More Releases from IMARC Group

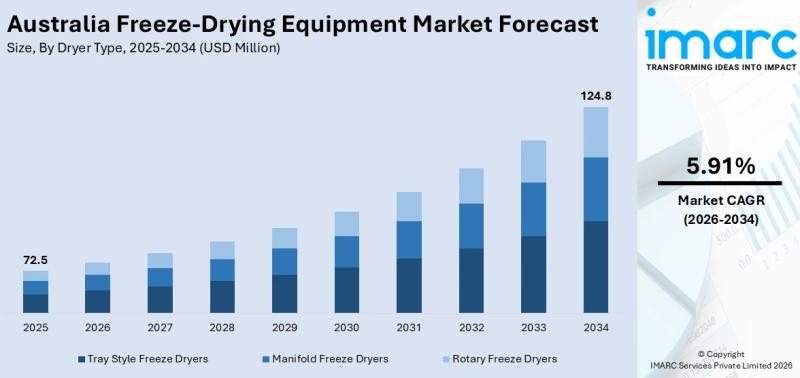

Australia Freeze-Drying Equipment Market Projected to Reach USD 124.8 Million by …

Australia Freeze-Drying Equipment Market Overview:

Australia's freeze-drying equipment market is experiencing robust growth, propelled by expanding pharmaceutical manufacturing investments, surging demand for freeze-dried food products, growing biotechnology research activity, and the country's strategic push to build sovereign capability in vaccine and biologic production. The Australia freeze-drying equipment market size reached USD 72.5 Million in 2025. Looking forward, the market is projected to reach USD 124.8 Million by 2034, exhibiting a growth…

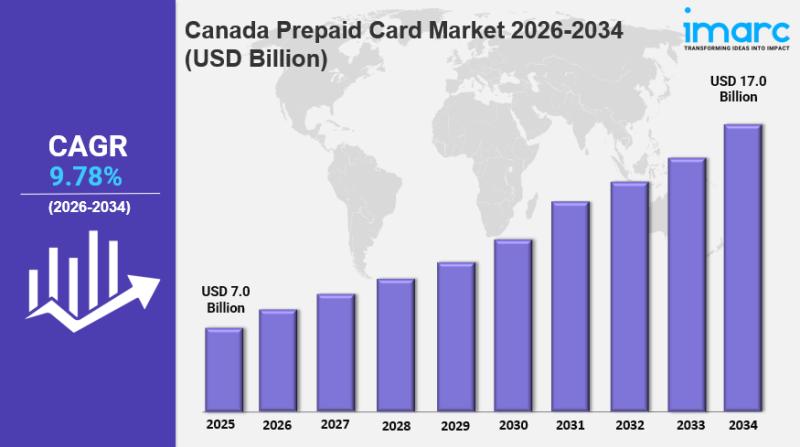

Canada Prepaid Card Market Size Projected to Reach USD 17.0 Billion | Growing at …

IMARC Group has recently released a new research study titled "Canada Prepaid Card Market Size, Share, Trends and Forecast by Card Type, Purpose, Vertical, and Region, 2026-2034", offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends and competitive landscape to understand the current and future market scenarios.

Canada Prepaid Card Market Size, Share, and Growth Forecast (2026-2034)

Prepaid cards in Canada are moving from a niche payment option to…

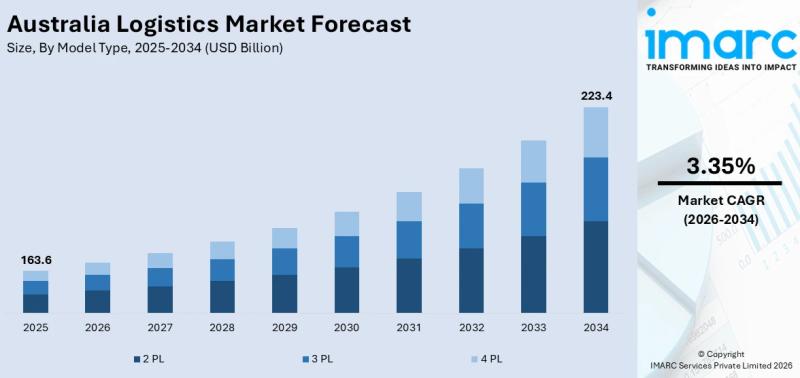

Australia Logistics Market Projected to Reach USD 223.4 Billion by 2034

Australia Logistics Market Overview:

Australia's logistics market is undergoing a significant transformation, driven by the country's position as the 12th-largest e-commerce market globally, a USD 14.5 billion Inland Rail infrastructure program, rapid warehouse automation adoption, and the shift toward electric trucks and sustainable supply chain operations. The Australia logistics market size reached USD 163.6 Billion in 2025. Looking forward, the market is projected to reach USD 223.4 Billion by 2034, exhibiting…

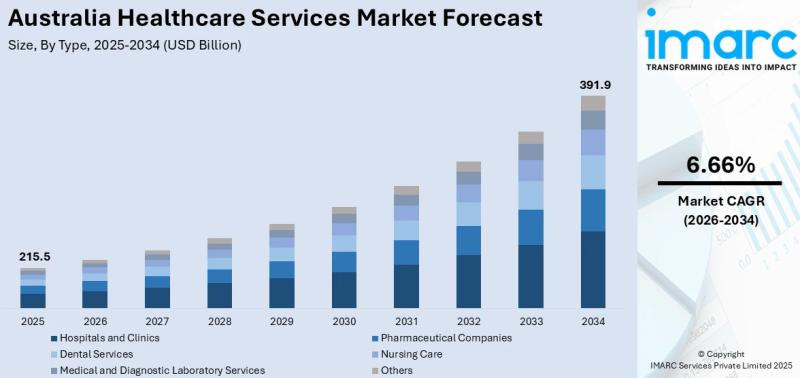

Australia Healthcare Services Market Projected to Reach USD 391.9 Billion by 203 …

Australia Healthcare Services Market Overview:

Australia's healthcare services market is one of the largest and most sophisticated in the Asia-Pacific region, driven by an aging population, rising chronic disease prevalence, record government hospital funding, the rapid expansion of telehealth and digital health technologies, and landmark reforms across the NDIS and aged care sectors. The Australia healthcare services market size reached USD 215.5 Billion in 2025. Looking forward, the market is expected…

More Releases for Fabric

The Difference Between Rib fabric and Jersey fabric

When it comes to choosing fabrics for clothing, the options can be overwhelming. Two popular choices are rib fabric and jersey fabric, each with its own unique characteristics and uses.

Jersey fabric is a type of weft knitted fabric known for its elasticity in both the warp and weft directions. This fabric has a smooth surface, a naturally clean texture, and a soft, fine feel. It is comfortable to wear and…

Fabric Testing and Fabric Testers

CHINA, HEFEI (February 27, 2024)-Based on the material classification, the textile testing laboratory's testing items are separated into three categories: fiber, yarn, and fabric testing. We will present pertinent fabric testing information based on the various fabric qualities in the content that follows.https://fyitester.com/textile-testing-equipments/fabric-garment/

The fabric solid degrees

The most common mechanical damage to textiles during usage is tensile fracture, tearing, bursting, and abrasion.

Tensile performance testing

The fabric's mechanical deformation law when it is…

Coated Fabric Market Global Coated Fabric Market, Coated Fabric Market, Coated F …

Global Coated Fabric Market Research report is an in-depth study of the market Analysis. Along with the most recent patterns and figures that uncovers a wide examination of the market offer. This report provides exhaustive coverage on geographical segmentation, latest demand scope, growth rate analysis with industry revenue and CAGR status. While emphasizing the key driving and restraining forces for this market, the report also offers a complete study of…

Fabric detergents

Market Overview

With the global economic recovery, more people look at the increasing environmental factors, especially underdeveloped regions that have a wide range of people, and fast economic growth, the need will increase. The industry is a high-technology and high-profit-based industry, the research team maintains a very positive outlook. New teams are welcomed to enter the market world. The fabric detergents industry is influenced by the economic guidelines, so…

Global Textile and Fabric Finishing and Fabric Coating Mills Market | Textile an …

The textile and fabric finishing and fabric coatings market consists of sales of textile and fabric finishings and fabric coatings by entities (organizations, sole traders and partnerships) that operate mills that produce textile and fabric finishings or fabric coatings.

According to the report analysis, ‘Textile and Fabric Finishing and Fabric Coating Mills Global Market Report 2020-30: Covid 19 Impact and Recovery’ states that the worldwide textile and fabric finishing and fabric…

Global Denim Fabric Market: Analysis, Technologies, Forecasts and Types: Light D …

Denim Fabric Market Report:

Summary: Excellence consistency maintains by Garner Insights in Research Report in which studies the global Denim Fabric market status and forecast, categorizes and Equipment market value by manufacturers, type, application, and region.

The report on Global Denim Fabric Market studies the historical data and evaluates the current market scenario so as to project the flight of the market during the next couple of years. This study has been…