Press release

Europe Pet Food Market Size to Worth USD 63.29 Billion by 2034 | With a 5.90% CAGR

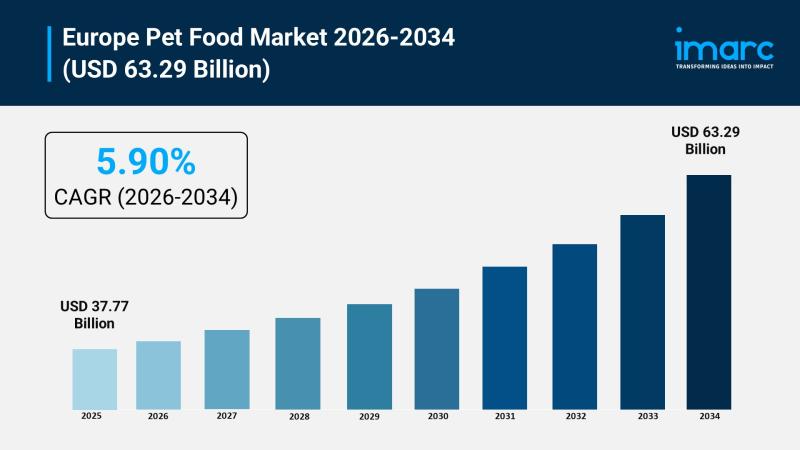

Europe Pet Food Market Graph 2026

Download a sample copy of the report: https://www.imarcgroup.com/europe-pet-food-market/requestsample

For pet food manufacturers, ingredient suppliers, and retailers assessing where to commit capital across Europe, the Europe pet food market keyword now represents a category where novel protein innovation, sustainability compliance, and digital subscription commerce are becoming just as important to competitive position as traditional brand equity.

Market Size and Current Valuation

At USD 37.77 Billion in 2025, Europe's pet food sector reflects an exceptionally deep and recurring demand base: 299 million pets live across 139 million pet-owning households, representing 49 percent of all European households. The climb toward USD 63.29 Billion by 2034 reflects a stable, mature Western European base growing steadily, augmented by faster-growing Central and Eastern European sub-regions, an accelerating online channel, and a novel protein segment expanding well ahead of the broader market.

Post-pandemic lifestyle transformations deepened human-animal bonds across the continent and drove an increase in single-person households, a structural shift that continues to generate recurring annual nutrition expenditure well beyond its original catalyst.

Segment-Wise Performance: Where the Market Concentrates

The Europe pet food market breaks down clearly across pet type, product type, pricing type, ingredient type, and distribution channel, each with a defined leader in 2025.

• Dog Food commands 42.09% share of the pet type segment, reflecting Europe's approximately 104 million dogs and the higher per-unit revenue premium of breed-specific, life-stage, and functional nutrition formulations.

• Cat Food follows closely at 40.31% share, tied to Europe's 127 million domestic cats, with wet and canned formats performing significantly above regional averages given the continent's strong preference for high-moisture, high-palatability feline nutrition.

• Dry Pet Food leads the product type segment at 57.18% share, followed by wet and canned pet food at 26.13% and snacks and treats at 16.69%.

• Mass Products dominate pricing type at 70.04% share, while Animal Derived ingredients lead ingredient type at 65.05% share.

• Supermarkets and Hypermarkets command distribution channel leadership at 62.76% share, the primary purchase point for the majority of European pet food transactions.

Pet Type Segment in Focus: Why Dog Food Holds Its Ground

Dog food's near-half share of the entire market reflects more than population scale. Per-unit revenue for dog food consistently exceeds cat food owing to larger portion sizes, a wider range of breed-specific formulations, and a premium positioning landscape featuring functional health claims spanning joint, digestive, dental, and cognitive wellness sub-categories, giving manufacturers meaningfully higher average transaction values per dog-owning household.

Product Type Segment: Dry Food's Shelf-Stability Advantage

Dry pet food's leadership, while notably lower than in other global markets given Europe's strong wet food culture, is being reinforced by advanced extrusion and high-pressure processing technologies that have narrowed the historical nutritional gap versus wet alternatives. Dry food's competitive advantage in shelf stability of eighteen to twenty-four months without refrigeration, cost-per-serving economics, and easy portioning continues to sustain its market position through 2034.

Country Analysis: Germany's Structural Advantage

Germany leads the Europe pet food market with a 26.0% share in 2025, representing approximately EUR 8.5 Billion in annual pet food sales. German consumers demonstrate Europe's highest per-pet annual expenditure, at approximately EUR 520, with premium dry kibble and veterinary prescription diets performing particularly well alongside the country's advanced e-commerce infrastructure.

Beyond Germany, the country picture spans several distinct markets:

• United Kingdom holds 20.1% share, Europe's second-largest and most innovation-receptive market, distinguished by direct-to-consumer subscription leadership and its position at the forefront of insect protein and cultivated meat commercialization.

• France commands 17.7% share, characterized by cat-heavy ownership patterns, strong organic and grain-free demand, and a high wet food culture.

• Italy accounts for 12.9% share, driven by rising pet humanization, wet food dominance among cat owners, and a consumer preference for natural ingredients.

• Spain holds 11.2% share, supported by growing middle-class pet spending, an outdoor lifestyle culture, and rising functional snacks demand.

• Others, spanning Eastern Europe, the Nordics, and Benelux, together represent 12.1% share, reflecting rapid income growth, sustainability-premium demand, and premium urban markets outside the five largest economies.

Customize the Europe Pet Food Market Report: https://www.imarcgroup.com/request?type=report&id=9491&flag=E

Regulatory Momentum: Packaging Mandates and Novel Protein Approval

Regulation is directly shaping product formulation and packaging investment across the Europe pet food market. The EU Packaging and Packaging Waste Regulation, mandating 70 percent recyclable packaging by 2030, is driving comprehensive material innovation, with paper-based wet food pouches, mono-material flexible films, and compostable treat packaging transitioning from pilot programs into mainstream rollout across premium and mid-tier brands.

Novel protein approval has reached a genuine commercial milestone. As of February 2025, eight insect protein species have received EU Novel Food approval for pet food use, opening commercial-scale production pathways that deliver a meaningfully lower carbon footprint versus beef, alongside substantially reduced water and feed requirements per kilogram of protein produced, aligning directly with European Green Deal mandates.

Company Moves and Product Innovation

Leading players are actively investing in novel protein, digital retail, and loyalty infrastructure to capture demand across the Europe pet food market:

• Meatly became the first company globally to commercialize cultivated meat for pet food in February 2025, launching 'Chick Bites' in partnership with THE PACK at Pets at Home in London, a lab-grown meat offering a resource-efficient, ethically compelling protein source with no antibiotic contamination risk.

• Zooplus SE relaunched its loyalty program across all 26 of its shops in November 2025, reinforcing its position as Europe's largest online pet supplies retailer serving customers across 30 European countries.

• Nestlé Purina PetCare introduced its 'Beyond' organic and plant-enriched pet food line across 12 European markets, driving its online channel to represent more than 25 percent of European revenue through subscription growth.

Among the market's leading key players, Mars Petcare and Nestlé Purina PetCare stand as the two dominant leaders, together commanding an estimated 38 to 44 percent of total European pet food revenue, with Mars Petcare's dual ownership of Royal Canin at the ultra-premium tier and Pedigree and Whiskas at the mainstream tier creating formidable cross-segment competitive coverage. Hill's Pet Nutrition leads the veterinary therapeutic segment through its Science Diet and Prescription Diet lines and Hill's to Home subscription model. Affinity Petcare holds strong Spain and Southern Europe leadership, while Zooplus AG dominates online retail. Other notable participants include Versele-Laga, Animonda, Brit (VAFO Group), Edgard & Cooper, Butternut Box, and Josera, spanning small animal nutrition, direct-to-consumer fresh food subscriptions, and German mid-market grain-free innovation.

Demand Drivers Beyond Pet Ownership

E-commerce and AI-personalized nutrition are scaling rapidly across the Europe pet food market, with online channels growing at approximately 11.4 percent annually, nearly double the broader market average, as subscription delivery models achieve mass-market adoption. Direct-to-consumer platforms including Butternut Box, Tails.com, and Edgard & Cooper deploy machine learning algorithms that analyze pet profile data to generate customized meal plans, reporting three to four times higher customer lifetime values compared to traditional retail channel equivalents.

Additional demand drivers extend beyond premiumization:

• Snacks and treats are evolving from impulse purchases into deliberate functional nutrition investments, with dental chew products clinically proven to reduce plaque by up to 70 percent and probiotic treats enriched with Lactobacillus strains for digestive support commanding two to three times the price of commodity alternatives.

• Insect-based protein represents the highest-growth innovation theme in the market, expanding at approximately 22.8 percent annually as EU regulatory approval enables commercial-scale ingredient supply.

• Functional and therapeutic nutrition, including veterinary-recommended, condition-specific formulas targeting digestive health, joint support, and weight management, continues to reinforce the premiumization trend across both dog and cat categories.

Cost Pressures Companies Must Navigate

Growth is not without friction. Private-label pet food is expanding volume share as major European retailers, including Lidl, Aldi, Tesco, Carrefour, and Rewe, aggressively build out their own pet food ranges, compressing branded player revenues and forcing pricing strategy reassessments across the industry. The transition to mono-material flexible films, paper-based pouches, and compostable treat packaging also requires substantial industry-wide capital investment ahead of the 2030 EU recyclability deadline, an obligation weighing more heavily on smaller and mid-sized manufacturers than on scaled multinational leaders. Post-Brexit regulatory divergence between the UK and EU on packaging regulations, labelling standards, and novel ingredient approval timelines further complicates compliance for manufacturers serving both markets simultaneously.

Opportunities and Growth Potential

The path to USD 63.29 Billion by 2034 rests on several converging opportunities for companies positioned early. Insect-based and novel protein ingredients represent the single highest-growth investment theme in the market, and manufacturers that move quickly to integrate EU-approved insect species into mainstream formulations stand to capture share ahead of competitors still reliant on conventional animal proteins.

Central and Eastern European markets, including Poland, the Czech Republic, Romania, Hungary, and the Baltic states, represent Europe's highest-growth geographic opportunity, expanding at 8 to 10 percent annually as per-pet spending, currently 15 to 20 percentage points below Western European benchmarks, converges with Western norms. First-mover distribution advantages in CEE pet specialty retail remain achievable for brands willing to establish presence ahead of market saturation.

Snacks and treats premiumization offers a third durable growth channel, given the category's evolution into a genuine functional nutrition segment commanding premium pricing well above commodity alternatives. Cultivated meat, following Meatly's commercial breakthrough, points toward a longer-term structural shift in protein sourcing that could reshape supply chains well before 2030. Companies that combine early novel protein investment with sustainable packaging leadership and digital subscription capability, following the models already being built by Zooplus, Nestlé Purina, and the DTC challenger cohort, are best positioned to capture the next phase of growth across the Europe pet food market.

Contact Us:

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201-971-6302

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Europe Pet Food Market Size to Worth USD 63.29 Billion by 2034 | With a 5.90% CAGR here

News-ID: 4578762 • Views: …

More Releases from IMARC Group

United States Weight Management Market Size Projected to Reach USD 132.87 Billio …

IMARC Group has recently released a new research study titled "United States Weight Management Market Size, Share, Trends and Forecast by Diet, Equipment, Service, and Region, 2026-2034," offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends and competitive landscape to understand the current and future market scenarios.

United States Weight Management Market Size, Growth, and Forecast (2026-2034)

The United States weight management market size was valued at USD 87.00…

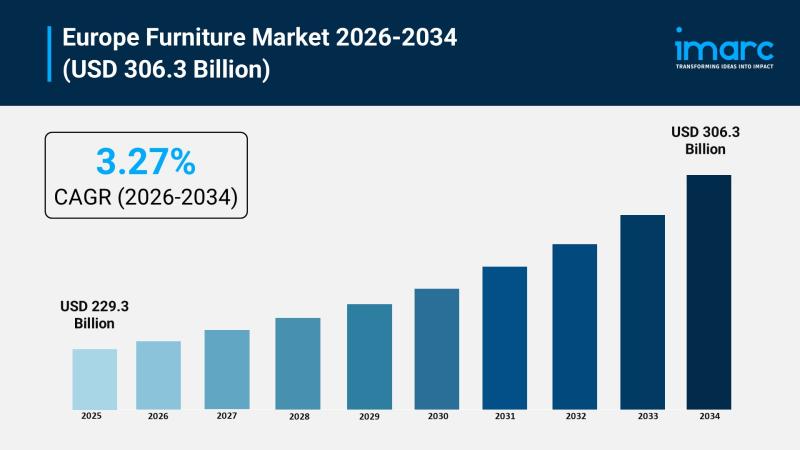

Europe Furniture Market to Witness Outstanding Growth of USD 306.3 Billion by 20 …

Europe's furniture industry is maturing into a market defined less by raw volume growth and more by premiumization, sustainability-led replacement cycles, and a decisive shift toward digital retail. The Europe furniture market, valued at USD 229.3 Billion in 2025, is projected to reach USD 306.3 Billion by 2034, growing at a compound annual rate of 3.27% between 2026 and 2034. That trajectory reflects a steady, innovation-driven expansion rather than a…

India Battery Swapping Market 2026-2034: Government Regulatory Policies, Industr …

India Battery Swapping Market 2026-2034

The report titled "India Battery Swapping Market Size, Share, Trends and Forecast by Operation Type, Service Type, Region, 2026-2034" comprises the overall market analysis of India, size, growth trends, key drivers, and regional insights of the battery swapping market in India and other important aspects related to the report.

How Big is the India Battery Swapping Market?

The India battery swapping market size reached USD 48.13 Million in…

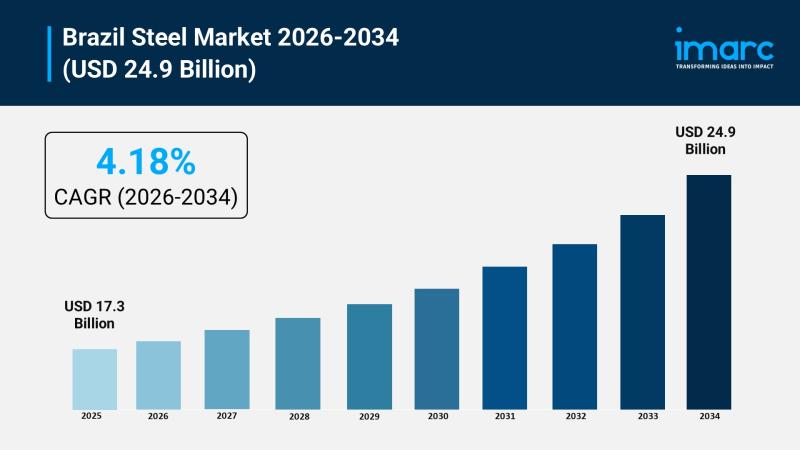

Brazil Steel Market Forecast: Revenue, Production & Demand Outlook Through 2034

Brazil's steel industry sits at the intersection of two powerful forces: a construction and infrastructure boom that shows no signs of slowing, and a global decarbonization push that is reshaping how steel itself gets made. The Brazil steel market, valued at USD 17.3 Billion in 2025, is projected to reach USD 24.9 Billion by 2034, growing at a compound annual rate of 4.18% between 2026 and 2034. That trajectory reflects…

More Releases for Europe

2019 Strategy Consulting Market Analysis | McKinsey, The Boston Consulting Group …

Strategy Consulting Market reports also offer important insights which help the industry experts, product managers, CEOs, and business executives to draft their policies on various parameters including expansion, acquisition, and new product launch as well as analyzing and understanding the market trends

Need for strategic planning in highly competitive environment and to develop business capabilities to meet & exceed the emerging requirements are the major drivers which help in surging…

Strategy Consulting Market 2025 | Analysis By Top Key Players: Booz & Co. , Rola …

Global Strategy Consulting Market 2019-2025, has been prepared based on an in-depth market analysis with inputs from industry experts. This report covers the market landscape and its growth prospects over the coming years. The report also includes a discussion of the key vendors operating in this market.

The key players covered in this study

McKinsey , The Boston Consulting Group , Bain & Company , Booz & Co. , Roland Berger Europe…

Digital Strategy Consulting Market is Thriving Worldwide with Deloitte, McKinsey …

A Digital Strategy is a form of strategic management and a business answer or response to a digital question, often best addressed as part of an overall business strategy. A digital strategy is often characterized by the application of new technologies to existing business activity and focus on the enablement of new digital capabilities to their business.

A new report as a Digital Strategy Consulting market that includes a comprehensive analysis…

Strategy Consulting Market 2019: By McKinsey, The Boston Consulting Group, Bain …

This report studies the global Strategy Consulting market, analyzes and researches the Strategy Consulting development status and forecast in United States, EU, Japan, China, India and Southeast Asia. This report focuses on the top players in global market, like

• McKinsey

• The Boston Consulting Group

• Bain & Company

• Booz & Co.

• Roland Berger Europe

• Oliver Wyman Europe

• A.T. Kearney Europe

• Deloitte

• Accenture Europe

Get Sample Report@ https://www.reporthive.com/enquiry.php?id=1247388&req_type=smpl&utm_source=AB

Market segment by Type, the product can be split into

• Operations Consultants

• Business Strategy Consultants

• Investment Consultants

• Sales and…

Strategy Consulting Market Analysis 2018: McKinsey, The Boston Consulting Group, …

Orbis Research Present’s “Global Strategy Consulting Market” magnify the decision making potentiality and helps to create an effective counter strategies to gain competitive advantage.

The global Strategy Consulting status, future forecast, growth opportunity, key market and key players. The study objectives are to present the Strategy Consulting development in United States, Europe and China.

In 2017, the global Strategy Consulting market size was million US$ and it is expected to reach million…

Influenza Vaccination Market Global Forecast 2018-25 Estimated with Top Key Play …

UpMarketResearch published an exclusive report on “Influenza Vaccination market” delivering key insights and providing a competitive advantage to clients through a detailed report. The report contains 115 pages which highly exhibits on current market analysis scenario, upcoming as well as future opportunities, revenue growth, pricing and profitability. This report focuses on the Influenza Vaccination market, especially in North America, Europe and Asia-Pacific, South America, Middle East and Africa. This…