Press release

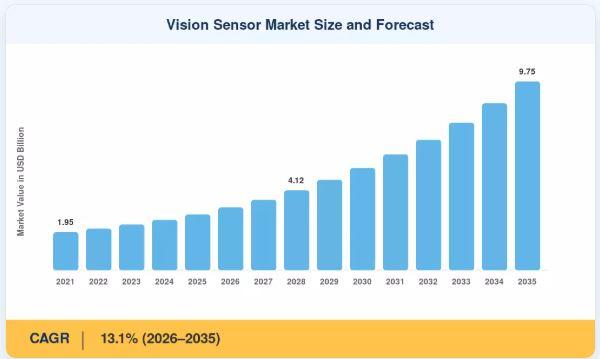

USD 2.85 Billion Vision Sensor Market Expected to Hit USD 9.75 Billion by 2035

Legacy pass/fail photoelectric sensors and human visual inspection stations are increasingly being replaced by smart, edge-processing vision sensors that incorporate imagery, in-built algorithms, and communication protocols in a single housing. Investment in smart-factory retrofits in discrete production is increasingly focused on sensor-level intelligence over centralized vision PCs, reducing integration cycles and total cost of ownership. North America dominates the market with an estimated 36% share, driven by dense automotive and semiconductor production capacity. Asia-Pacific is the fastest-expanding area as electronics contract manufacturers in China, Vietnam, and India develop automated quality control. Not far behind is Europe, with Industry 4.0 retrofit schemes in Germany and the Nordic countries. Vision sensors are becoming a fundamental manufacturing need rather than a competitive differentiator as production lines increase throughput and tolerances become tighter.

Get Full PDF Sample Copy of Report: (Including Full TOC, List of Tables & Figures, Chart) @

https://www.marketresearchfuture.com/sample_request/7771

➤ How Significant Is the Vision Sensor Market's Growth?

The vision sensor market's trajectory from USD 2.85 billion in 2025 to a projected USD 9.75 billion by 2035 represents more than a three-fold expansion over the forecast decade, reflecting the structural shift across discrete manufacturing from statistical sampling and human visual inspection toward 100% inline automated optical verification as a baseline production quality standard. The market's 13.1% CAGR is anchored in a manufacturing investment supercycle where EV component lines, semiconductor packaging facilities, and consumer electronics contract manufacturers are all specifying vision sensor arrays as a non-negotiable infrastructure element.

2D vision sensors account for an estimated 64% of 2025 revenue, remaining the default choice for code reading and presence detection, while 3D vision sensors are forecast to grow at a CAGR above the category average through 2035 as bin-picking and robotic guidance applications scale. Inspection applications represent roughly 48% of total demand the largest single application segment followed by Gauging at 27% and Code Reading at 25%. The automotive end-user segment is valued at USD 0.97 billion in 2025, the largest end-user category, driven by EV component lines specifying inline vision inspection from initial design rather than retrofit. Consumer Electronics is the second-largest at USD 0.63 billion, followed by Electrical & Electronics at USD 0.54 billion, Food & Beverages at USD 0.40 billion, and Pharmaceuticals at USD 0.31 billion.

➤ What Does the Future Hold for the Vision Sensor Market?

Factory automation capex growth contributes approximately 22% to the vision sensor market's CAGR the single highest driver impact. Global industrial automation spending exceeding USD 265 billion in 2024 is generating sustained sensor procurement volumes as manufacturers install vision-dense automated lines requiring image-based verification at every robotic pick station, conveyor transfer, and end-of-line quality gate. The International Federation of Robotics projects robot density per 10,000 manufacturing employees rising from 151 units in 2023 toward 220+ by 2028, and each collaborative and industrial robot installation increasingly interfaces with vision sensors for workspace safety monitoring and pick-and-place position confirmation.

Automotive part-defect tolerance tightening contributes approximately 18% to the CAGR, establishing tier-1 automotive suppliers as a primary, regulation-anchored demand source. Tier-1 suppliers are tightening acceptable defect rates on stamped and machined parts, pushing vision-based gauging onto lines that previously relied on sampling-based manual checks. This shift is most pronounced in regions with dense EV component manufacturing, where new battery and motor assembly lines are being specified with inline vision inspection by default. The EU's 2035 combustion engine phase-out and China's NEV penetration mandate are legislative backstops that make automotive vision sensor demand structurally non-cyclical, while bar code and traceability mandates in retail and pharmaceutical packaging contribute a further 12% to the CAGR.

The next product generation is shifting from rule-based image processing to onboard deep-learning inference, allowing sensors to classify novel defect types without manual threshold reprogramming. Vendors are increasingly competing on software ecosystem breadth fleet management dashboards, defect-trend analytics, and remote configuration rather than hardware specifications alone. Manufacturers are standardizing on edge-to-cloud architectures that keep inference at the sensor edge while streaming aggregated quality metrics to centralized manufacturing execution systems, reducing bandwidth needs versus full-frame video transmission. Vendors that successfully compress deep-learning defect classification models for low-power edge sensor hardware can differentiate on accuracy without requiring customers to add external compute a capability still unevenly distributed across the competitive set and representing one of the market's most powerful near-term performance differentiation opportunities.

Get access to the full description of the report @

https://www.marketresearchfuture.com/reports/vision-sensor-market-7771

➤ Who Are the Key Players in the Vision Sensor Market?

The vision sensor market is moderately fragmented, with the combined share of the top five estimated at 35-42% and no single vendor dominating outright a structure consistent with a market still defined by differentiated technology approaches (2D versus 3D, smart-camera versus PC-based) rather than commoditized hardware. MRFR identifies the following key participants with estimated revenue share ranges:

✿ Cognex Corporation (~9-12% share) - the innovation-led, software-ecosystem leader providing smart cameras and 3D vision systems, with the broadest deployed base of machine vision installations globally and an In-Sight series that anchors inspection applications across automotive, electronics, and pharmaceutical end markets.

✿ Keyence Corporation (~8-11% share) - a direct-sales, application-breadth specialist providing vision sensors and image sensors across the widest product range in the market, with the July 2018 IV-H series enabling multi-part all-in-one detection and an aggressive Asia-Pacific expansion strategy targeting emerging electronics contract manufacturing customers.

✿ OMRON Corporation (~6-9% share) - an integrated automation portfolio provider offering smart sensors and industrial automation systems, leveraging its broader control and robotics ecosystem to offer vision sensors pre-integrated with PLC and robot controller architectures favored by Japan and Asia-Pacific OEM customers.

✿ SICK AG (~6-8% share) - an industrial safety and automation heritage specialist providing 2D and 3D vision sensors with particular strength in logistics conveyor and automotive body-shop applications, with the September 2018 Visionary-T DT single-snapshot 3D time-of-flight sensor enabling collision warning on AGVs at sensing ranges up to 50 meters.

✿ Basler AG (~4-6% share) - a component-level specialization leader providing vision components and embedded vision cameras, with particular strength in OEM camera supply to system integrators building custom machine vision solutions for semiconductor inspection and medical imaging applications.

✿ Baumer Group (~3-5% share) - a precision manufacturing focus specialist providing smart cameras and sensors, with an October 2018 CMOS-based GigE and USB 3.0 CX series of polarization cameras enabling quality control of glass, carbon fiber fabric, and reflective surfaces previously difficult for conventional imaging.

✿ ifm electronic (~3-5% share) - a process industry strength provider of vision and condition-monitoring sensors, with established distribution relationships across European industrial automation system integrators and strong positioning in food and beverage and chemical processing environments.

✿ Panasonic Corporation (~3-5% share) - an electronics manufacturing synergy specialist providing industrial vision systems with deep integration into its broader factory automation ecosystem, leveraging electronics manufacturing heritage to serve consumer electronics contract manufacturers in Asia-Pacific with vision sensor packages optimized for high-speed PCB and connector inspection.

✿ Sony Corporation (~3-4% share) - an upstream sensor technology leader providing image sensor components that underpin a significant share of third-party machine vision and smart camera designs globally, establishing Sony as an indirect but strategically significant participant in the vision sensor market through its IMX sensor series.

✿ Datalogic S.p.A. (~3-5% share) - a retail and logistics specialization leader providing code-reading vision sensors with established deployment across barcode scanning conveyor lines, supermarket self-checkout, and e-commerce parcel distribution center applications where traceability mandates drive sustained code-reader sensor procurement.

Strategic competition in the vision sensor market is increasingly defined by SDK and deep-learning model compression capability with the absence of a dominant AI programming framework cited as the top adoption barrier for edge inference features alongside Ethernet/IP and PROFINET communication protocol breadth, washdown-rated housing availability for food and pharma environments, and the depth of vision-data analytics subscription platforms that convert one-time hardware sales into recurring software revenue.

➤ What Are the Emerging Trends in the Vision Sensor Market?

Several transformational trends are redefining the vision sensor market's evolution through 2035:

AI-Native Vision Sensors with Onboard Deep-Learning Inference: The next product generation is shifting from rule-based image processing to embedded deep-learning classification, allowing sensors to identify novel defect morphologies without manual threshold reprogramming or offline model retraining. Vendors compressing neural network inference to run within sensor-class power and memory budgets are establishing AI-native performance as the new competitive baseline for premium inspection applications.

3D Vision Sensor Scaling for Bin-Picking and Robotic Guidance: 3D vision sensors growing at above-category-average CAGR are penetrating bin-picking and volumetric gauging applications that 2D systems cannot address. Automotive body-shop line introduction and logistics automated storage and retrieval systems are the two highest-volume near-term application ramps, with SICK's Visionary-T DT and Cognex 3D-A5000 series establishing competing platform standards for mid-range 3D deployment.

Platform and Ecosystem Economics Displacing Specification Competition: Vendors are building recurring-revenue moats through fleet management dashboards, remote sensor configuration, defect-trend analytics subscriptions, and centralized model-update pipelines that reduce customer switching costs after initial installation. Cognex's VisionPro Deep Learning and Keyence's XG-X Series AI platforms exemplify the ecosystem depth that is reshaping vendor selection from hardware specification comparisons to software capability evaluations.

Emerging-Market Contract Manufacturing Build-Out as Greenfield Opportunity: Southeast Asian and Indian electronics contract manufacturing capacity additions represent a substantial untapped opportunity for vision sensor vendors, as new greenfield facilities in Vietnam, India, and Malaysia are increasingly specified with automated inspection from day one rather than retrofitted later with India posting the fastest country-level CAGR within Asia-Pacific as automotive component export capacity expands.

Food and Pharmaceutical Traceability Mandates Creating Secondary Demand Channels: Tightening traceability and tamper-evidence requirements in food and pharmaceutical packaging are opening secondary growth channels for code-reading vision sensors beyond their traditional industrial base, with washdown-rated IP69K housing variants enabling direct installation on high-pressure cleaning lines that previously precluded sensor deployment.

ESG and Sustainability Reporting Extending Vision Sensor Use Cases: Expanding ESG disclosure requirements are creating secondary demand for vision-based material and component traceability data, beyond the original quality-control use case. Vision sensors deployed for inline inspection are being repurposed as traceability data nodes that log component provenance, material composition, and batch genealogy for scope-3 emissions reporting and circular-economy compliance programs.

Buy Full Research Report:

https://www.marketresearchfuture.com/checkout?currency=one_user-USD&report_id=7771

➤ How Is the Vision Sensor Market Segmented?

The vision sensor market report provides a comprehensive segmentation framework:

By Type: Contour Sensor, Pixel Counter Sensor, 3D Sensor, Monochrome Sensor, Color Sensor, Code Reader

By Technology: 2D Vision Sensors (64% share, 2025), 3D Vision Sensors (36% share, 2025; fastest CAGR)

By Application: Inspection (48% share), Gauging (27%), Code Reading (25%), Object Recognition, Localization

By End-User Industry: Automotive (USD 0.97B), Consumer Electronics (USD 0.63B), Electrical & Electronics (USD 0.54B), Food & Beverages (USD 0.40B), Pharmaceuticals (USD 0.31B)

By Region: North America (36%), Asia-Pacific (28%), Europe (24%), South America (6%), Middle East & Africa (6%)

➤ What Are the Regional Insights from the Vision Sensor Market?

North America leads the vision sensor market with a 36% share in 2025, with the United States commanding 78% of regional revenue through automotive and semiconductor capex. US reshoring of semiconductor and EV battery manufacturing capacity under CHIPS Act and Inflation Reduction Act incentives is the single largest regional growth contributor, with new fabrication and assembly facilities specifying inline vision inspection as a baseline requirement rather than an add-on. Canada contributes 14% of regional share through food processing automation, and Mexico adds 8% through nearshored electronics assembly lines where vision sensors are increasingly specified as a standard quality infrastructure element.

Asia-Pacific holds 28% of global vision sensor market revenue in 2025 and represents the fastest-growing region, anchored by China's 42% regional share through electronics contract manufacturers that are the world's largest single demand pool for 2D inspection and code-reading vision sensors. Japan contributes 18% of regional share through precision electronics manufacturing, South Korea 14% through semiconductor packaging, and India 16% through rapidly expanding automotive component export capacity that is driving the country's position as the fastest-growing national market within the region. ASEAN contributes 7% of regional share as manufacturing relocation from China accelerates across Vietnam, Thailand, and Malaysia.

Europe accounts for 24% of global vision sensor market share, with Germany commanding 31% of regional revenue through the world's highest robot density among large economies and Industry 4.0 retrofit incentive programs that have made automated optical inspection a commonly cited line item in manufacturing modernization grant applications. The UK contributes 14% of European share through pharmaceutical traceability compliance requirements, France 12% through aerospace component inspection, Italy 11% through packaging machinery OEM applications, and the Nordic countries 9% through industrial robotics integration programs. Germany's automotive and machine-building base continues to anchor European demand, reinforced by retrofit incentive programs targeting brownfield manufacturing sites that represent the continent's primary vision sensor replacement cycle.

South America and the Middle East & Africa each represent 6% of global vision sensor market revenue, with distinct demand profiles. Brazil commands 58% of South American revenue through food and beverage processing compliance requirements that favor automated inspection over manual sampling, with Argentina's agro-industrial automation adding 22% of regional share. Saudi Arabia holds 28% of MEA revenue through Vision 2030 industrial diversification programs gradually introducing automated quality control into sectors historically reliant on manual inspection, the UAE 24% through logistics automation in Dubai's free zone distribution infrastructure, and South Africa 20% through automotive assembly operations serving the continent's largest vehicle manufacturing base. Gulf state programs remain at an earlier adoption stage than other regions but represent a structurally growing long-term frontier for vision sensor market expansion through 2035.

➤➤➤ Regional & Country-Level Reports by Market Research Future:

US Vision Sensor Market -

https://www.marketresearchfuture.com/reports/us-vision-sensor-market-18116

➤➤➤ Industry Analysis Reports by Market Research Future:

Smart Home Automation Market-

https://www.marketresearchfuture.com/reports/smart-home-automation-market-12426

Logic Semiconductors Market-

https://www.marketresearchfuture.com/reports/logic-semiconductors-market-12486

Semiconductor Wafer Transfer Robots Market-

https://www.marketresearchfuture.com/reports/semiconductor-wafer-transfer-robots-market-12488

Us Warehouse Robotics Market-

https://www.marketresearchfuture.com/reports/us-warehouse-robotics-market-12533

Capacitors And Resistors Wholesale Market-

https://www.marketresearchfuture.com/reports/capacitors-resistors-wholesale-market-12579

Assembly Line Solutions Market-

https://www.marketresearchfuture.com/reports/assembly-line-solutions-market-12707

High Voltage Capacitor Market-

https://www.marketresearchfuture.com/reports/high-voltage-capacitor-market-13906

Mobile Dram Market-

https://www.marketresearchfuture.com/reports/mobile-dram-market-17756

Photonics Market-

https://www.marketresearchfuture.com/reports/photonics-market-17757

Probe Card Market-

https://www.marketresearchfuture.com/reports/probe-card-market-17763

About Market Research Future:

At Market Research Future (MRFR), we enable our customers to unravel the complexity of various industries through our Cooked Research Report (CRR), Half-Cooked Research Reports (HCRR), Raw Research Reports (3R), Continuous-Feed Research (CFR), and Market Research & Consulting Services.

MRFR team have supreme objective to provide the optimum quality market research and intelligence services to our clients. Our market research studies by products, services, technologies, applications, end users, and market players for global, regional, and country level market segments, enable our clients to see more, know more, and do more, which help to answer all their most important questions.

Contact:

Market Research Future

(Part of Wantstats Research and Media Private Limited)

99 Hudson Street, 5Th Floor

New York, NY 10013

United States of America

+1 628 258 0071 (US)

+44 2035 002 764 (UK)

Email: sales@marketresearchfuture.com

Website: https://www.marketresearchfuture.com

Website: https://www.wiseguyreports.com/

Website: https://www.wantstats.com/

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release USD 2.85 Billion Vision Sensor Market Expected to Hit USD 9.75 Billion by 2035 here

News-ID: 4575370 • Views: …

More Releases from Market Reseach Future (MRFR)

Neuromorphic Chip Market Set for 46.8% CAGR, Rising from USD 0.37 Billion to USD …

The Global Neuromorphic Chip market stood at USD 0.37 billion in 2025 and is projected to reach USD 0.55 billion in 2026 before surging to USD 17.41 billion by 2035, reflecting a compound annual growth rate of 46.8% across the 2026-2035 forecast window one of the highest growth rates of any semiconductor category globally. Neuromorphic chips brain-inspired processors that implement spiking neural networks, in-memory analog compute arrays, and event-driven sensing…

Interactive Whiteboard Market Valued at USD 5.32 Billion in 2025 Forecast to Rea …

The Global interactive whiteboard market stood at USD 5.32 billion in 2025 and is projected to climb from USD 5.73 billion in 2026 to USD 11.13 billion by 2035, registering a CAGR of 7.65% over the forecast window. Two primary catalysts are converting latent interest into purchase orders at scale: government-backed classroom digitization mandates the U.S. E-Rate program disburses over USD 2.5 billion annually to schools for connectivity and classroom…

Mobile Accessories Market to Reach USD 240.00 Billion by 2035 from USD 106.20 Bi …

The Global mobile accessories market was valued at USD 106.20 billion in 2025 and is projected to grow from USD 115.20 billion in 2026 to USD 240.00 billion by 2035, registering a CAGR of 8.5% during the forecast period. Two major catalysts are accelerating this extraordinary trajectory: the global smartphone installed base reaching approximately 6.8 billion users in 2024 making every device a recurring procurement trigger for cases, chargers, cables,…

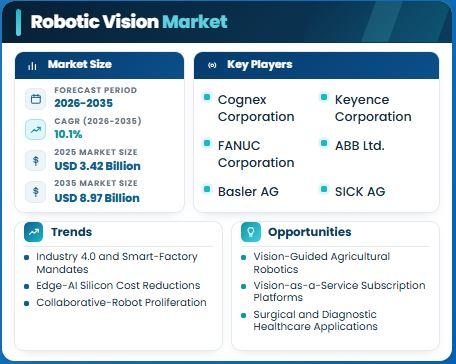

Global Robotic Vision Market registering a CAGR of 10.1% & Opportunities Toward …

The Global robotic vision market reached an estimated USD 3.42 billion in 2025 and is projected to grow to USD 8.97 billion by 2035, registering a CAGR of 10.1% during the forecast period. Two major catalysts are accelerating this trajectory: the accelerating deployment of collaborative robots (cobots) and autonomous mobile robots (AMRs) across manufacturing, logistics, and healthcare sectors, and the rapid maturation of deep learning-based machine vision algorithms that now…

More Releases for USD

Bone Cement Market Outlook USD 1,871.10M-USD 3,512.31M

How Is the Bone Cement Market Supporting the Rise of Modern Orthopedic Surgery?

The Bone Cement Market plays a critical role in modern orthopedic and spinal procedures, acting as a foundational material for joint replacement, fracture fixation, and vertebral stabilization. Bone cement is widely used to anchor implants, restore bone structure, and improve patient mobility-making it an essential component of musculoskeletal care.

In 2025, the global bone cement market was valued at…

Autologous Cell Therapy Market Outlook USD 9.31B-USD 54.83B

How Is the Autologous Cell Therapy Market Redefining the Future of Precision Medicine?

The Autologous Cell Therapy Market is rapidly emerging as one of the most transformative areas in modern healthcare, offering highly personalized treatment options for complex and chronic diseases. By using a patient's own cells to repair, replace, or regenerate damaged tissues, autologous cell therapy minimizes immune rejection risks while maximizing therapeutic effectiveness.

In 2025, the global autologous cell therapy…

US Ostomy Care and Accessories Market USD 4.03B-USD 6.75B

How Is the United States Ostomy Care and Accessories Market Evolving to Meet the Needs of a Growing Patient Population?

The United States Ostomy Care and Accessories Market plays a critical role in improving the quality of life for millions of patients who undergo life-altering surgical procedures involving the digestive or urinary systems. Ostomy care products are essential medical devices designed to manage bodily waste safely and discreetly following surgeries such…

PACS Market USD 5.59B in 2025, USD 9.73B by 2035

Picture Archiving and Communication System (PACS) Market Expands as Digital Imaging Transforms Global Healthcare

Introduction: PACS at the Core of Modern Medical Imaging

The healthcare industry is undergoing a rapid digital transformation, with medical imaging playing a critical role in diagnosis, treatment planning, and patient monitoring. At the heart of this transformation lies the Picture Archiving and Communication System (PACS)-a technology that enables the storage, retrieval, management, and sharing of medical images…

Global HEOR Market USD 1.70B-USD 6.03B

Health Economics and Outcomes Research (HEOR) Market Accelerates as Value-Based Healthcare Redefines Global Decision-Making

Introduction: The Growing Importance of HEOR in Modern Healthcare

The global healthcare industry is undergoing a profound transformation, shifting from volume-driven care models to value-based healthcare systems that prioritize patient outcomes, cost efficiency, and real-world effectiveness. At the center of this transformation lies Health Economics and Outcomes Research (HEOR)-a discipline that evaluates the economic value, clinical outcomes, and…

Foam Tape Market Outlook 2035: Industry Growth from USD USD 4.89 Billion (2025) …

The Foam Tape Market plays a vital role in modern industrial and manufacturing ecosystems. Foam tapes are pressure-sensitive adhesive products manufactured using materials such as polyurethane, polyethylene, PVC, and acrylic foam. These tapes are widely used for bonding, sealing, insulation, cushioning, vibration damping, and noise reduction across multiple industries. Their ability to replace traditional mechanical fasteners like screws, bolts, and rivets has positioned foam tapes as a preferred solution in…