Press release

Deep Learning Chips Market to Reach US$ 63.2 Billion by 2033 as AI Inference, Edge Devices and Data Centers Demand New Compute Architectures

Deep Learning Chips Market

Request Executive Sample | Market Intelligence: https://www.datamintelligence.com/download-sample/deep-learning-chips-market?kailas

Deep Learning Chips Become a Core Compute Architecture

The market is scaling because AI workloads are changing from isolated model experiments to production systems that must operate continuously across data centers and devices. Deloitte's Tech Trends 2026 notes that AI inference is reshaping enterprise compute strategies as production-scale deployment creates cost, scalability and latency challenges that existing infrastructure cannot always support.

This is why AI chips, neural processor architectures, GPU accelerators, ASICs and edge AI chips are becoming strategic building blocks. Training remains important, but inference at scale is creating a wider demand base across cloud services, smartphones, PCs, industrial machines, connected vehicles, medical systems, retail analytics and security platforms.

Growth Drivers: Inference Scale, Edge AI and Autonomous Workloads

The strongest driver for the deep learning chips market is inference scale. As generative AI, computer vision, speech recognition, recommendation engines and agentic AI move closer to users and machines, chips must process models faster, locally and with lower energy consumption. Capgemini reports that AI agents are moving into enterprise operations, while only a small share of organizations have deployed them at scale, indicating significant room for infrastructure-led adoption.

Data center expansion is another major driver. The International Energy Agency states that there is "no AI without energy," because training and deploying AI models take place in large, power-hungry data centers. It also notes that data center electricity consumption is set to more than double to around 945 TWh by 2030, with AI as the most important driver of that growth.

Demand is also rising from robotics and autonomous workloads. AI-enabled machines need real-time perception, decision-making and control. In factories, deep learning accelerators support inspection, predictive maintenance, digital twins and automation. In vehicles, AI inference chips support driver assistance, cockpit intelligence and future autonomous functions. In devices, NPUs and low-power AI accelerators allow workloads to run locally, improving latency, privacy and reliability.

Disruption: Memory, Energy, Supply and Software Lock-In

The market is also being reshaped by bottlenecks. Memory bandwidth has become a key constraint as larger models require faster movement of data between compute, memory and interconnect. Intel Foundry highlights that advanced packaging enables larger chiplet systems, high-density 2.5D interconnects and logic-to-HBM integration for demanding AI and HPC applications.

Energy use is another disruption point. AI data centers are becoming highly power-intensive, while edge AI systems must deliver useful performance within strict battery, heat and size limits. Chip shortages, dependence on advanced manufacturing capacity and software ecosystem lock-in further complicate buying decisions. Once an organization standardizes on a hardware and software stack, switching costs can rise because model optimization, libraries, developer tools and deployment pipelines become tightly connected to the selected AI accelerator.

Request a Customized Report According to Your Business Strategy: https://www.datamintelligence.com/customize/deep-learning-chips-market?kailas

Opportunities: NPUs, ASICs, Chiplets and Low-Power AI Chips

The opportunity landscape is expanding beyond high-end GPUs. NPUs are becoming essential in smartphones, PCs and embedded devices. ASICs are gaining attention where buyers need domain-specific performance and predictable cost. FPGAs remain relevant where reconfigurability matters, especially in telecom, defense, industrial systems and low-latency applications. Chiplets and advanced packaging are opening new design paths by combining compute, memory and interconnect more efficiently.

The most attractive opportunities include:

AI inference chips for cloud platforms and enterprise workloads.

Edge AI chips for devices, robotics, automotive and IoT systems.

Low-power NPUs for on-device generative AI.

Chiplet-based AI accelerators that improve scalability and memory access.

DataM Segmentation: Chip Type, Processing, Deployment and End Use

DataM Intelligence segments the market by Chip Type into graphics processing units, application-specific integrated circuits, central processing units, field-programmable gate arrays and others. By Processing Type, the market covers training and inference. By Deployment Mode, it includes cloud/data center and edge. By End-Use, the market covers datacenters and telecommunication, BFSI, healthcare and life sciences, automotive and transportation, retail and e-commerce, industrial manufacturing, consumer electronics and others.

The cloud/data center segment is estimated to hold 68.9% market share, according to DataM Intelligence, reflecting the concentration of AI workloads in large-scale computing environments. Edge deployment is becoming increasingly important as real-time applications move closer to users, machines and sensors.

Regional Analysis: USA, Japan, Germany and South Korea

The USA remains central to cloud and semiconductor design, supported by hyperscale platforms, AI software ecosystems and accelerator suppliers. DataM Intelligence identifies North America as the largest regional market, while the IEA notes that the United States accounted for the largest share of global data center electricity consumption in 2024.

Japan is positioned around robotics, automotive electronics, edge AI and semiconductor revival. METI's AI and semiconductor framework targets more than JPY 10 trillion in public support through fiscal 2030 to stimulate more than JPY 50 trillion in public-private investment, strengthening the country's foundation for AI chips and physical AI applications.

Germany is driven by Industry 4.0, automotive engineering, industrial AI and high-performance simulation. Deutsche Telekom and NVIDIA's Industrial AI Cloud initiative is positioned as sovereign AI infrastructure for Germany and Europe, supporting industrial transformation through AI and digital twin platforms.

South Korea remains important because of its memory, foundry and device AI ecosystem. Korea's science and ICT ministry has highlighted the country's semiconductor memory and manufacturing capabilities as part of its broader AI competitiveness base.

Purchase Corporate License | Market Intelligence: https://www.datamintelligence.com/buy-now-page?report=deep-learning-chips-market?kailas

Key Players and Company Profiles

DataM Intelligence lists major players in the global deep learning chips market including NVIDIA Corporation, Intel Corporation, Advanced Micro Devices Inc., Qualcomm Incorporated, Apple Inc., Alphabet Inc., Amazon Web Services, Microsoft Corporation, Alibaba Group and Cerebras Systems.

NVIDIA Corporation remains one of the most important suppliers in the AI accelerator and GPU market. Its Blackwell architecture includes the GB200 NVL72, which connects 36 Grace CPUs and 72 Blackwell GPUs in a rack-scale, liquid-cooled design for real-time trillion-parameter AI workloads.

Advanced Micro Devices Inc. is expanding its AI accelerator position through AMD Instinct GPUs. The AMD Instinct MI350 Series is built on 4th Gen AMD CDNA architecture and targets generative AI, training, inference and HPC workloads, with HBM3E memory and an open software stack designed to reduce deployment barriers.

Intel Corporation is competing through Gaudi AI accelerators and foundry packaging capabilities. Intel describes Gaudi as an AI acceleration platform built for training, fine-tuning and inference, while its advanced packaging work supports chiplet scaling, HBM integration and energy-efficient AI/HPC systems.

Qualcomm Incorporated is positioned strongly in edge AI chips and NPUs. The Qualcomm AI Engine supports on-device AI across PCs, smartphones, IoT, robotics, XR and automotive systems, with the Hexagon NPU enabling real-time processing and power-efficient AI experiences across device categories.

The deep learning chips market is entering a scale-up phase where procurement decisions are no longer limited to peak chip performance. Buyers are evaluating AI chips based on memory bandwidth, power efficiency, software maturity, deployment flexibility, supply assurance, edge readiness, and total operating cost. As AI inference, robotics, autonomous systems, and data center workloads expand, deep learning chips will define how efficiently organizations convert AI ambition into scalable compute capacity.

Read Exclusive Report Description: https://www.datamintelligence.com/research-report/deep-learning-chips-market

Contact:

Fabian Mathew

DataM Intelligence 4market Research LLP

6th Floor, M2 Tech Hub, DataM Intelligence 4market Research LLP, Lalitha Nagar, Habsiguda, Secunderabad, Hyderabad, Telangana 500039

USA: +1 877-441-4866

Email: fabian@datamintelligence.com

About DataM Intelligence

DataM Intelligence is a global market research and business intelligence firm delivering actionable insights across healthcare, pharmaceuticals, chemicals, energy, technology, food, and industrial sectors. Through syndicated reports, custom research, consulting, and competitive intelligence services, the company helps organizations identify growth opportunities, navigate market challenges, and make informed strategic decisions in over 50+ countries worldwide.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Deep Learning Chips Market to Reach US$ 63.2 Billion by 2033 as AI Inference, Edge Devices and Data Centers Demand New Compute Architectures here

News-ID: 4571760 • Views: …

More Releases from DataM intelligence 4 Market Research LLP

Edge AI Processor Market to Reach US$ 16.51 Billion by 2035 as Enterprises Move …

The global edge AI processor market was valued at US$ 3.05 billion in 2025 and is projected to reach US$ 16.51 billion by 2035, growing at a CAGR of 18.4% during 2026-2035, according to DataM Intelligence. The market is expanding as organizations shift from centralized AI architectures toward distributed intelligence, where latency, privacy, bandwidth cost, energy efficiency and uptime decide how AI is deployed across devices, machines, vehicles, cameras, factories…

AI Training Chip Market to Reach US$ 29.4 Billion by 2033 as Hyperscalers, Semic …

The global AI training chip market was valued at US$ 8.44 billion in 2025 and is projected to reach US$ 29.4 billion by 2033, expanding at a CAGR of 16.9% during 2026-2033, according to DataM Intelligence. The market is moving beyond a conventional technology procurement cycle as AI training chips become a compute-security, cost, capacity and sovereignty decision for enterprises, cloud platforms and governments building long-term AI infrastructure.

Request Executive Sample…

AI Data Centers Market Becomes the New Infrastructure Battleground as Compute, P …

The global AI data centers market reached US$ 17.02 billion in 2025 and is estimated to reach US$ 21.19 billion in 2026, before expanding to US$ 98.24 billion by 2033, growing at a CAGR of 24.50% during 2026-2033, according to DataM Intelligence. This growth reflects a major shift from traditional cloud capacity planning to AI factory infrastructure, where power availability, land access, high-speed interconnect, data center cooling, hardware density and…

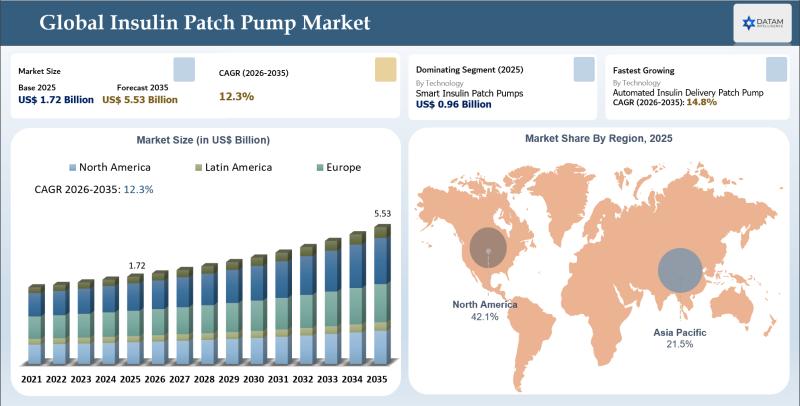

United States Insulin Patch Pump Market 2035 | Growth Drivers, Trends & Market F …

Market Size and Growth 2026

The global Insulin Patch Pump market stood at US$ 1.72 billion in 2025 and is expected to reach US$ 5.53 billion by 2035, growing with a CAGR of 12.3% during the forecast period 2026-2035.

DataM Intelligence has released a new research report titled Insulin Patch Pump Market Size 2026 The report delivers in-depth insights into key market dynamics, including regional growth trends, market segmentation, CAGR projections,…

More Releases for Intel

Vision Processing Unit Market Is Booming Rapidly with Strong Demand By 2033 | In …

Coherent Market Insights has added a new research study on the Global "Vision Processing Unit Market" 2026 by Size, Growth, Trends, and Dynamics, Forecast to 2033 which is a result of an extensive examination of the market patterns. This report covers a comprehensive investigation of the information that influences the market regarding fabricates, business providers, market players, and clients. The report provides data about the aspects which drive the expansion…

Global Slim Laptop Market By Type (Intel I3, Intel I5 Low Power Version, Sharp D …

The Global Slim Laptop Market 2020 report implement in-depth research of the industry with a focus on the current market trends future prospects. The Global Slim Laptop Market report aims to provide an overview of Slim Laptop Market players with detailed market segmentation by product, application and geographical region. It also provides market share and size, revenue forecast, growth opportunity. The most recent trending report Worldwide Slim Laptop Market Economy…

Wearable Computer Market Global Forecast 2018| Studied By LG, ,Honeywell, Epson, …

UpMarketResearch published an exclusive report on “Wearable Computer market” delivering key insights and providing a competitive advantage to clients through a detailed report. The report contains 115 pages which highly exhibits on current market analysis scenario, upcoming as well as future opportunities, revenue growth, pricing and profitability. This report focuses on the Wearable Computer market, especially in North America, Europe and Asia-Pacific, South America, Middle East and Africa.…

Smart Grid Security Market - Competitive Analysis | Cisco Systems, Inc., Intel C …

The global market for smart grid security is highly influenced by the rise in the population and the rapid pace of urbanization in emerging economies. The main factor behind this is increasing shift of energy resources companies to smart meters and smart appliances by leveraging Internet of Things (IoT) and cloud, owing to the augmenting pressure on them to meet the ever-increasing energy requirements of the urban population. With this,…

Intel Labs launches the Intel Collaborative Research Institute for Computational …

22 May, 2012

—While computer performance exceeds human performance in many respects, there are still many tasks that humans perform easily and computers have a hard time with. Intel, in collaboration with the Technion–Israel Institute of Technology and the Hebrew University of Jerusalem, hopes to change this situation by exploring technologies that mimic the human brain's mode of action—

Intel today announced it is establishing the Intel Collaborative Research institute for…

Intel Distributes ESET Security Software With Intel® Desktop Boards

ESET Validates Market Strength as Industry-Leading AV Solution

Dubai, United Arab Emirates, September 23, 2009 – ESET, the leader in proactive threat protection, announced today that Intel will distribute ESET security software products with Intel-branded desktop motherboards starting in Q1 2010. As a result of the distribution agreement, Intel Desktop Boards will include either a 45-day or one-year product license for ESET Smart Security.

ESET will ship exclusively with new Intel®…