Press release

United States Agrochemicals Market Size Projected to Reach USD 53.2 Billion by 2034 with a CAGR of 4.21%

United States Agrochemicals Market Size, Growth, and Forecast (2026-2034)

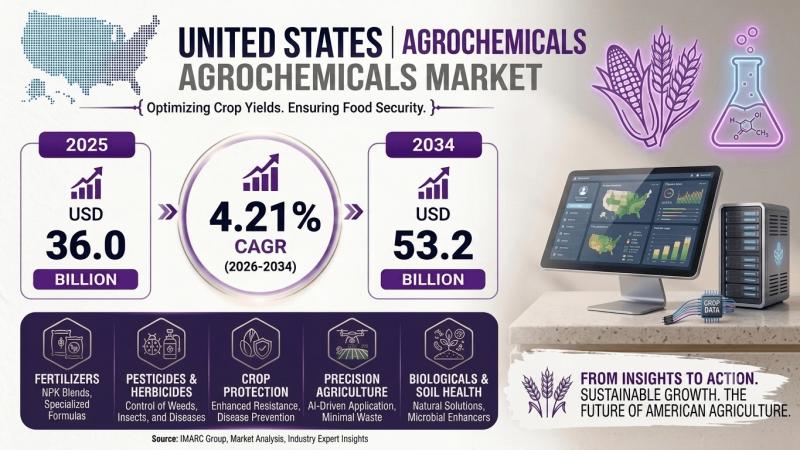

The United States agrochemicals market size reached USD 36.0 Billion in 2025 and is projected to reach USD 53.2 Billion by 2034, growing at a CAGR of 4.21% during 2026-2034. Growing population and food demand, increasing awareness about environmental sustainability, climate variability, ongoing research and development, favorable government support, and advancements in agrochemical technology represent some of the key factors driving the market.

Agrochemicals refer to a broad category of chemical substances used to enhance crop production and protect plants from pests, diseases, and weeds. These chemicals play a vital role in modern agriculture by improving crop yields and ensuring food security for a growing global population. Agrochemicals encompass several key categories including fertilizers, pesticides, herbicides, and plant growth regulators.

Fertilizers provide essential nutrients such as nitrogen, phosphorus, and potassium to plants, promoting healthy growth and increased crop yields. Pesticides are designed to control and manage pests that can damage crops, reducing yield loss and ensuring food quality. Herbicides target unwanted weeds that compete with crops for resources, helping to maintain the overall health of cultivated plants across U.S. agricultural systems.

Precision agriculture techniques including the use of drones, GPS technology, and data analytics are enabling farmers to apply agrochemicals more precisely, reducing waste and environmental impact. This integration of digital tools with agrochemical programs is improving input efficiency and supporting more sustainable intensification of crop production across the United States.

Get Insights on the United States Agrochemicals Market Access the IMARC Sample Report: https://www.imarcgroup.com/united-states-agrochemicals-market/requestsample

Key Trends Driving the United States Agrochemicals Market

• Growing population and rising global food demand: The continuous increase in the U.S. and global population is driving the need for higher agricultural productivity. Agrochemicals such as fertilizers and pesticides are essential for maximizing crop yields to meet this expanding demand. The U.S. remains a critical global food supplier, and sustained agricultural output requires reliable access to effective crop protection and nutrition products.

• Climate change adaptation and weather variability challenges: Climate change and unpredictable weather patterns are posing escalating challenges to agriculture across the United States. Agrochemicals, particularly those that enhance drought resistance, address new pest and disease pressures, and protect crops under extreme temperature conditions, are becoming increasingly critical for adapting to changing environmental conditions across diverse U.S. growing regions.

• Shift toward environmentally sustainable and bio-based agrochemicals: Growing consumer demand for organically and sustainably produced food is compelling a market-wide shift toward more environmentally friendly agrochemicals. Biological pesticides, bio-stimulants, and reduced-risk chemical formulations are gaining traction as farmers respond to retailer sustainability requirements and consumer preferences for lower pesticide residue food products.

• Precision agriculture integration improving agrochemical efficiency: The adoption of precision agriculture technologies including GPS-guided variable rate applicators, drone-based crop scouting, and AI-powered decision support tools is enabling farmers to apply agrochemicals more precisely and efficiently. Targeted application reduces input waste, lowers environmental impact, and improves return on agrochemical investment across high-value crop production systems.

• Government support and regulatory frameworks shaping market dynamics: Government subsidies, crop insurance programs, and research investment support agrochemical adoption by reducing farmer risk and encouraging the uptake of innovative products. EPA regulatory frameworks governing pesticide registration and label requirements shape product availability and application practices, while USDA programs promote sustainable agricultural input programs across U.S. farming operations.

• Ongoing research and development driving product innovation: Continuous R&D investment by leading agrochemical companies is generating new and improved products with enhanced efficacy, reduced environmental footprints, and broader crop safety profiles. Innovations in active ingredient discovery, formulation chemistry, and delivery systems are expanding the agrochemical toolkit available to U.S. farmers for managing crop nutrition and protection challenges.

United States Agrochemicals Market Report Segmentation:

The United States Agrochemicals Market report provides a detailed segmentation analysis to help businesses identify key growth segments and evolving industry trends. The market is categorized based on fertilizer type, pesticide type, and crop type, offering insights into demand patterns across the U.S. agricultural input ecosystem.

Fertilizer Type Insights:

• Nitrogen Fertilizer: Nitrogen fertilizer is the largest and most widely used fertilizer category in the United States, essential for supporting protein synthesis, vegetative growth, and yield potential across corn, wheat, cotton, and other major row crops. Urea, anhydrous ammonia, and liquid nitrogen solutions are the primary nitrogen fertilizer forms, with application timing and rate precision becoming increasingly important for both yield optimization and nitrogen loss reduction.

• Phosphatic Fertilizer: Phosphatic fertilizers supply phosphorus, a critical macronutrient for root development, energy transfer, and crop maturation. Diammonium phosphate (DAP) and monoammonium phosphate (MAP) are the most widely used phosphatic fertilizer products in the U.S. market, with application driven by soil phosphorus status and the phosphorus removal rate of high-yielding crop varieties.

• Potassic Fertilizer: Potassic fertilizers provide potassium, which is essential for water regulation, enzyme activation, and disease resistance in crops. Potassium chloride (muriate of potash) is the dominant potassic fertilizer product. U.S. potash demand is closely tied to corn and soybean production area and yield expectations, with high-productivity farming systems requiring consistent potassium replenishment to maintain soil fertility.

• Others: Includes secondary and micronutrient fertilizers such as sulfur, calcium, magnesium, boron, zinc, and manganese, as well as specialty fertilizers including slow-release and controlled-release formulations, liquid fertigation products, and foliar nutrition programs designed to address specific crop nutrition gaps and optimize nutrient use efficiency.

Pesticide Type Insights:

• Herbicides: Herbicides represent the largest pesticide category by volume in the United States, reflecting the scale of row crop production where weed control is a foundational agronomic practice. Glyphosate-based and selective grass and broadleaf herbicides are widely used across corn, soybean, cotton, and cereal production systems, with herbicide resistance management driving adoption of diverse mode-of-action programs.

• Fungicides: Fungicide demand is driven by disease pressure management in high-value crops including soybeans, corn, specialty fruits and vegetables, and turfgrass. Rising adoption of fungicide programs in row crops, particularly for soybean sudden death syndrome and corn southern corn leaf blight management, and the expansion of specialty crop acreage are supporting consistent fungicide market growth.

• Insecticides: Insecticides protect crops from pest damage across multiple application timings, including seed treatments, in-furrow applications, and foliar sprays throughout the growing season. The integration of insecticide seed treatments with fungicide and biological seed treatment packages has become standard practice in major U.S. row crop systems, driving consistent insecticide demand.

• Others: Includes nematicides, rodenticides, molluscicides, and plant growth regulators that address specific pest and regulatory challenges in specialty and high-value crop production systems. Biologically derived crop protection products including microbial pesticides and pheromone-based pest management systems are a growing sub-category within this segment.

Crop Type Insights:

• Cereals and Grains: Cereals and grains represent the largest crop type segment by agrochemical consumption volume, encompassing corn, wheat, sorghum, and rice production across the Midwest and Great Plains. The vast scale of U.S. cereal production, combined with the high agrochemical intensity of modern corn and wheat farming systems, makes this segment the foundational driver of national agrochemical demand.

• Oilseeds and Pulses: Oilseeds and pulses, led by soybeans, represent a large and growing agrochemical consumption segment. U.S. soybean production requires extensive herbicide, fungicide, and insecticide programs, with growing adoption of biological seed treatments and foliar nutrition products further expanding per-acre input intensity in this critical export crop category.

• Fruits and Vegetables: Fruits and vegetables represent the highest per-acre agrochemical intensity segment, given the high crop value and the stringent pest, disease, and weed management requirements of specialty crop production. California, Florida, and Pacific Northwest specialty crop production regions are primary drivers of high-value agrochemical demand across this segment.

• Others: Includes cotton, peanuts, sugar crops, turf and ornamental, and emerging agrochemical application areas such as hemp and controlled environment agriculture, collectively representing a diverse set of crop production systems with distinct and growing agrochemical requirements across U.S. agricultural markets.

Regional Insights:

• Midwest: The Midwest is the dominant regional market, anchored by the Corn Belt states of Iowa, Illinois, Indiana, and Ohio along with broader coverage across Minnesota, Wisconsin, and Missouri. The region's massive corn and soybean production base generates the highest agrochemical consumption volumes of any U.S. region, driving sustained demand for nitrogen, phosphatic, and potassic fertilizers alongside herbicide, fungicide, and insecticide programs.

• South: The South is a major regional market supported by cotton, soybean, peanut, and specialty crop production across Texas, Mississippi, Arkansas, and Georgia. The region's diverse crop mix, combined with high pest and disease pressure under warm and humid growing conditions, supports significant pesticide consumption and growing specialty fertilizer demand.

• West: The West, particularly California, is the highest per-acre intensity agrochemical market, driven by the concentration of high-value specialty crop production including fruits, vegetables, nuts, and wine grapes. The region's premium crop values justify intensive agrochemical programs, and its large organic and sustainable farming sector is driving growth in bio-based and reduced-risk agrochemical products.

• Northeast: The Northeast supports a growing specialty crop and organic farming sector, with agrochemical demand concentrated in vegetable, fruit, and dairy-associated forage crop production. The region's relatively small scale compared to Midwest row crop production is offset by high per-acre input intensity and growing demand for specialty and organic-approved agrochemical products.

Speak to An Analyst: https://www.imarcgroup.com/request?type=report&id=19921&flag=C

United States Agrochemicals Market Recent News and Developments:

Biological and bio-based product expansion: Leading agrochemical companies are accelerating their biological product portfolios through acquisitions and new product launches. Major players including BASF, Bayer, Corteva, and Syngenta are all expanding into biological crop protection and bio-stimulant categories, driven by grower demand for sustainable input programs and the growing regulatory and market environment supporting bio-based solutions.

Herbicide resistance management driving new product development: The growing challenge of herbicide-resistant weed populations across U.S. corn and soybean production regions is driving demand for new modes of action and multi-site herbicide programs. Companies are investing in new herbicide active ingredients, innovative formulation technologies, and integrated weed management programs to address resistance-driven efficacy gaps.

Precision agriculture and digital tools integration:

Agrochemical companies are increasingly integrating their product recommendations with precision agriculture platforms and digital farm management tools. Data-driven variable rate application recommendations, field-level risk mapping, and AI-powered agronomic advisory services are becoming key competitive differentiators for major agrochemical suppliers serving U.S. commercial farming operations.

Challenges Impacting the United States Agrochemicals Market

Herbicide and insecticide resistance development in target pest populations is an ongoing challenge that reduces the efficacy of established active ingredients and increases the cost and complexity of crop protection programs. Managing resistance across millions of acres of U.S. row crop production requires continuous innovation in new active ingredients, formulation strategies, and integrated pest management approaches.

Stringent and evolving EPA regulatory requirements for pesticide registration, re-registration, and label amendments add cost and time to new product development and can restrict the use of established active ingredients. Compliance with EPA, state-level, and international maximum residue limit requirements demands sustained regulatory investment from agrochemical manufacturers and creates market access uncertainty.

Commodity price volatility directly impacts farmer purchasing decisions for agrochemical inputs. When crop prices decline, farmers reduce input spending to manage costs, which can create meaningful volume swings in fertilizer and pesticide demand that challenge agrochemical manufacturers and distributors in maintaining stable revenue and inventory management across market cycles.

Raw material price volatility, particularly for nitrogen fertilizer precursors including natural gas and for phosphate and potash mining inputs, creates significant input cost fluctuations for agrochemical manufacturers. These cost pressures can compress margins and are sometimes passed through to farmers as retail price increases that influence purchasing behavior and product mix decisions.

Investment Opportunities in the United States Agrochemicals Market

The U.S. agrochemicals market offers compelling investment opportunities across its projected growth from USD 36.0 Billion in 2025 to USD 53.2 Billion by 2034. Biological and bio-based agrochemical products represent the highest-growth investment category, driven by strong regulatory tailwinds, growing farmer adoption, and increasing retailer and food company requirements for sustainable input programs.

Specialty fertilizer and precision nutrition products present strong margin-accretive investment opportunities, as farmers increasingly adopt variable rate fertility management and enhanced efficiency fertilizer technologies that reduce nutrient loss and improve crop response. Products that demonstrably improve nitrogen use efficiency or provide foliar micronutrient solutions are well-positioned for premium market positioning.

Digital agriculture platforms that integrate agrochemical recommendations with field-level data and precision application technology represent a forward-looking investment category. Companies that can deliver actionable, data-driven agrochemical prescriptions connected to precision application equipment are creating differentiated value propositions that build customer loyalty and support premium product adoption.

Outlook of the United States Agrochemicals Market (2026-2034)

The outlook for the United States agrochemicals market is positive, supported by growing food demand, advancing precision agriculture adoption, ongoing R&D investment, and the expanding role of biological and sustainable products. The market is projected to grow from USD 36.0 Billion in 2025 to USD 53.2 Billion by 2034 at a CAGR of 4.21%.

As U.S. agriculture continues to evolve toward greater precision, sustainability, and data integration, the agrochemical industry will adapt its product mix toward higher-efficacy, lower-environmental-footprint solutions. Companies that successfully balance agronomic performance with sustainability credentials will be best positioned to serve the next generation of commercially oriented and environmentally conscious U.S. farmers through 2034.

Frequently Asked Questions (FAQs): United States Agrochemicals Market

1. What is the current size of the United States agrochemicals market?

The United States agrochemicals market reached USD 36.0 Billion in 2025 and is projected to reach USD 53.2 Billion by 2034, growing at a CAGR of 4.21% during 2026-2034.

2. What are agrochemicals?

Agrochemicals are chemical substances used to enhance crop production and protect plants from pests, diseases, and weeds. Key categories include fertilizers that supply essential plant nutrients, pesticides that manage harmful insects and pathogens, herbicides that control weeds, and plant growth regulators that modify crop development to optimize yield and quality.

3. What are the key drivers of the United States agrochemicals market?

Key drivers include growing population and rising global food demand, climate change adaptation requirements, increasing environmental sustainability awareness driving demand for bio-based products, precision agriculture adoption improving agrochemical efficiency, favorable government support programs, and continuous R&D investment generating innovative new agrochemical products with improved efficacy and safety profiles.

4. Which fertilizer type leads the U.S. agrochemicals market?

Nitrogen fertilizer is the largest fertilizer category, essential for supporting protein synthesis and yield potential across the vast corn and wheat production systems that dominate U.S. row crop agriculture. Phosphatic and potassic fertilizers represent significant complementary segments, with consumption closely tied to cropping system intensity and soil fertility management programs.

5. Which pesticide type drives the most demand in the U.S.?

Herbicides represent the largest pesticide category by volume in the United States, reflecting the scale of row crop production where weed control is foundational to crop management. Herbicide resistance management is a growing driver of new product demand. Fungicides are the fastest-growing pesticide segment, supported by expanding adoption in soybean and corn systems and growth in specialty crop acreage.

6. Which crop type generates the most agrochemical demand?

Cereals and grains, led by corn and wheat, generate the largest volume of agrochemical demand due to the vast scale of U.S. row crop production. Oilseeds and pulses, primarily soybeans, represent a large and growing segment. Fruits and vegetables generate the highest per-acre agrochemical intensity, making specialty crop production regions disproportionately important to high-value agrochemical product demand.

7. Which region leads the United States agrochemicals market?

The Midwest is the dominant regional market, driven by the massive scale of Corn Belt corn and soybean production generating the highest national agrochemical consumption volumes. The South is a significant secondary market supported by cotton, soybean, and specialty crop production. The West, particularly California, is the highest per-acre intensity market for specialty agrochemical products.

8. What are the main challenges facing the U.S. agrochemicals market?

Key challenges include herbicide and insecticide resistance development reducing active ingredient efficacy, stringent and evolving EPA regulatory requirements for pesticide registration and use, commodity price volatility directly impacting farmer input spending decisions, and raw material price fluctuations affecting agrochemical manufacturer margins and retail pricing stability.

9. What investment opportunities exist in the U.S. agrochemicals market?

Compelling investment opportunities include biological and bio-based agrochemical products aligned with sustainability megatrends, specialty and enhanced efficiency fertilizer products offering precision nutrition solutions, and digital agriculture platforms that integrate data-driven agrochemical recommendations with precision application technology to create differentiated value for commercial farmers.

10. Who are the key players in the United States agrochemicals market?

Key players include Corteva Agriscience, Bayer CropScience, Syngenta (a ChemChina company), BASF Agricultural Solutions, Nutrien, Mosaic Company, CF Industries, Winfield United, FMC Corporation, and UPL, alongside regional distributors and specialty agrochemical companies serving niche crop protection and nutrition market segments across U.S. agriculture.

Author IMARC Group

IMARC Group is a leading global management consulting firm providing in-depth market research, strategic advisory services, and feasibility studies. The firm empowers organizations worldwide with actionable insights and data-driven strategies to support sustainable growth and informed decision-making.

Contact Us

IMARC Group

Email: sales@imarcgroup.com

United States: +1-201-971-6302

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release United States Agrochemicals Market Size Projected to Reach USD 53.2 Billion by 2034 with a CAGR of 4.21% here

News-ID: 4570693 • Views: …

More Releases from IMARC Group

Europe Crane Market Report 2026-2034: Business Insights for Crane Makers, Constr …

Europe Crane Market Summary:

• The Europe Crane Market reached USD 14.1 Billion in 2025.

• The market is projected to reach USD 17.1 Billion by 2034.

• Germany dominates the Europe crane market with a significant market share.

• Growth is driven by rising infrastructure investments, expanding manufacturing activities, and increasing adoption of advanced lifting technologies.

IMARC Group, a leading market research company, has released its latest report titled "Europe Crane Market Report by Type, Mobility, Capacity, End…

European Frozen Seafood Market Analysis for Seafood Importers, Exporters and Pro …

European Frozen Seafood Market Summary:

• The European Frozen Seafood Market reached USD 26.37 Billion in 2025.

• The market is projected to reach USD 32.97 Billion by 2034.

• Spain, Germany, the United Kingdom, Italy, France, Poland, and Portugal account for a significant share of the regional market.

• Growth is driven by rising demand for convenient protein-rich foods, expanding cold chain infrastructure, and increasing consumer preference for sustainably sourced seafood.

IMARC Group, a leading market research company,…

Latin America IT in Real Estate Market to USD 1,964.7 Million by 2034 with a Rob …

Latin America IT in Real Estate Market Summary

• The Latin America IT in Real Estate Market was valued at USD 761.8 Million in 2025.

• The market is projected to reach USD 1,964.7 Million by 2034.

• The market is expected to grow at a CAGR of 11.10% during 2026-2034.

• Rising digital transformation across commercial and residential real estate is driving market expansion.

• Cloud computing and software-as-a-service (SaaS) platforms are streamlining property management…

Latin America Logistics Market to Hit USD 580.1 Billion by 2034 with a Robust CA …

Latin America Logistics Market Summary

• The Latin America Logistics Market was valued at USD 366.1 Billion in 2025.

• The market is projected to reach USD 580.1 Billion by 2034.

• The market is expected to expand at a CAGR of 5.25% during 2026-2034.

• Rapid expansion of e-commerce is increasing demand for efficient warehousing and last-mile delivery services.

• Governments across the region are investing in transportation infrastructure to improve trade connectivity.

• Rising cross-border trade is encouraging logistics providers…

More Releases for United

AI Image Recognition Market Will Hit Big Revenues In Future | Google (United Sta …

According to HTF Market Intelligence, the Global AI Image Recognition market to witness a CAGR of 13.42% during the forecast period (2024-2030). The Latest Released AI Image Recognition Market Research assesses the future growth potential of the AI Image Recognition market and provides information and useful statistics on market structure and size.

This report aims to provide market intelligence and strategic insights to help decision-makers make sound investment decisions and identify…

Movable Walls Market By Top Key Players- Hufcor (United States), Dormakaba (Swit …

Global Movable Walls Market Report from Advance Market Analytics (AMA) covers market characteristics, size and growth, segmentation, regional breakdowns, competitive landscape, market shares, trends and strategies for this market. The market characteristics section of the report defines and explains the market. The market size section gives the electronic equipment market revenues, covering both the historic growth of the market and forecasting the future. Drivers and restraints looks at the external…

Military Personal Protective Equipment Market 2024 | 3M Ceradyne (United States) …

Military personal protective equipment has become a crucial and standard element of soldier equipment. One of the major factor driving the market is the increasing role of ground troops in different parts of the world such as Iraq, Afghanistan and India among others. The demand for military personal protective equipment is anticipated to be driven by modernization initiatives undertaken by several large defense spenders globally and various internal security threats,…

Infrared Sensor Market 2024 | Honeywell International, Inc. (United States), Tex …

Infrared sensors are devices emitting, detecting, receiving infrared waves as heat and infrared radiation. However, there are only a few among these sensors which are capable of only receiving the waves. Most of the infrared detectors are coated with either Fresnel lenses or parabolic mirrors for receiving infrared waves from an entire area. As these waves reach the sensor, it generates a voltage in different waves that is used for…

Internet of Things Market 2021 | Google Inc. (United States), Cisco Systems Inc. …

The Internet of Things refers to the network of physical objects that attribute an IP address for Internet connectivity. Internet of Things is defined as an invisible and intelligent network of things that communicate indirectly or directly with each other. Internets of Things enable communication between the physical objects and other internet-enabled systems and devices. In addition, Internet of Things also makes the life of consumers much more comfortable and…

Logistics Market | Global Growing Industry Key Players - J.B. Hunt Transport Ser …

Market Research Reports Search Engine (MRRSE) has recently updated its massive research catalog by adding a new study, titled “Logistics Market”. The study offers a clear insight about the prevailing trends and innovations happening in the Logistics Market. Readers can further access details about research highlights and executive summary to gain a better idea about this assessment. The market overview covers key industry developments and market opportunity map during the…