Press release

Aerospace Materials Market Research Report 2026-2032: Opportunities, Trends, and Growth Projections at 8.7% CAGR

Aerospace Materials

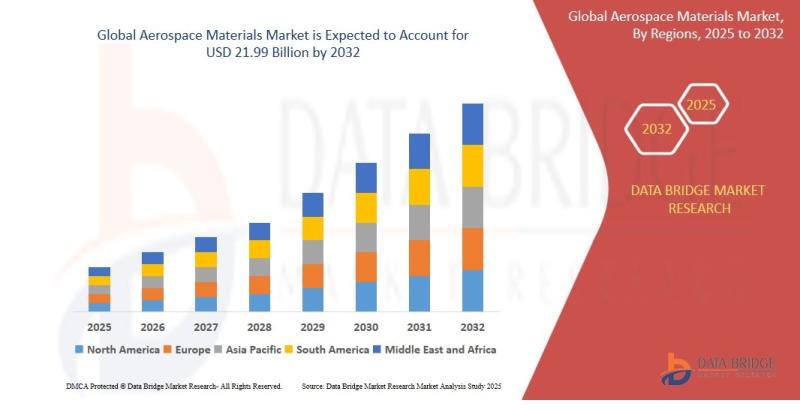

As per Data Bridge Market Research analysis, the Aerospace Materials Market was estimated at USD 13.65 billion in 2025. The market is expected to grow from USD 14.84 billion in 2026 to USD 21.99 billion in 2032, at a CAGR of 8.7% during the forecast period, driven by the rising demand for lightweight aircraft materials, increasing commercial aircraft production, expanding defense modernization programs, and growing investments in advanced composites and sustainable aerospace manufacturing technologies.

Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs) https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-aerospace-materials-market

Market Size & Forecast

2025 Market Size: USD 13.65 Billion

2026 Projected Market Size: USD 14.84 Billion

2032 Projected Market Size: USD 21.99 Billion

CAGR (2026-2032): 8.7%

Largest Region: North America

Fastest Growing Region: Asia Pacific

Key Market Report Takeaways

North America accounts for approximately 38%-40% of global market revenue, supported by the presence of major aircraft manufacturers, advanced aerospace infrastructure, and substantial defense spending.

Asia Pacific represents the fastest-growing regional market due to rapid aircraft fleet expansion, indigenous aircraft manufacturing programs, and increasing aerospace investments in China and India.

Composite materials hold the highest market share among material types owing to superior strength-to-weight ratio, corrosion resistance, and fuel-efficiency benefits.

Airframe structures/aerostructures constitute the dominant application segment, accounting for the largest proportion of aerospace material consumption.

OEM (Original Equipment Manufacturer) demand represents the leading end-use segment, driven by commercial aircraft production and defense procurement programs.

Details about the report and current availability can be viewed: https://www.databridgemarketresearch.com/reports/global-aerospace-materials-market

Market Trends

Key Market Trends & Highlights

North America continues to lead the global market due to the strong presence of aircraft OEMs, extensive aerospace supply chains, and sustained investments in defense and space programs.

Asia Pacific is emerging as the fastest-growing region, supported by expanding airline fleets, rising passenger traffic, localization of aerospace supply chains, and government-backed aerospace manufacturing initiatives.

Airframe structures remain the dominant application segment as manufacturers increasingly deploy lightweight materials across fuselage, wing, and structural assemblies.

Growth is being driven by aircraft weight reduction requirements, fuel-efficiency targets, rising commercial aviation demand, and increased defense procurement worldwide.

Advanced composites, carbon-fiber-reinforced polymers (CFRPs), titanium alloys, and additive manufacturing technologies are reshaping material selection and production processes.

Sustainability regulations, aerospace decarbonization goals, strategic partnerships, and investments in next-generation aircraft platforms continue to influence market expansion and innovation.

Market Dynamics

Market Drivers

Growing Commercial Aircraft Production and Fleet Expansion

Rising global air passenger traffic and airline fleet modernization programs are significantly increasing demand for aerospace materials. Aircraft manufacturers are expanding production rates for narrow-body and wide-body aircraft to meet growing travel demand. Emerging economies in Asia Pacific and the Middle East are witnessing substantial airline investments, further strengthening material consumption. Commercial aviation remains the largest aircraft segment globally.

Increasing Adoption of Lightweight Composite Materials

Aircraft manufacturers are prioritizing lightweight materials to improve fuel efficiency and reduce emissions. Carbon-fiber-reinforced polymers, thermoplastic composites, and advanced aluminum-lithium alloys are increasingly replacing conventional materials. These materials offer superior strength-to-weight ratios, durability, and corrosion resistance, supporting next-generation aircraft development.

Rising Defense Modernization Programs

Governments worldwide are increasing defense budgets and investing in advanced fighter aircraft, unmanned aerial vehicles (UAVs), and military transport fleets. Defense modernization initiatives in North America, Europe, and Asia Pacific are generating sustained demand for high-performance aerospace materials. Military platforms require specialized composites, titanium alloys, and heat-resistant materials for enhanced operational performance.

Expansion of Space Exploration Activities

Growing investments in satellite deployment, reusable launch vehicles, and commercial space missions are creating new opportunities for aerospace materials manufacturers. Spacecraft require lightweight and high-temperature-resistant materials capable of withstanding extreme operational environments. The increasing participation of private aerospace companies further accelerates material innovation.

Technological Advancements in Material Science

Continuous innovation in aerospace-grade composites, ceramic matrix composites, additive manufacturing, and nanomaterials is enhancing aircraft performance and lifecycle efficiency. Advanced manufacturing techniques enable improved structural integrity, lower maintenance costs, and reduced production waste. Ongoing R&D investments by major aerospace manufacturers continue to drive material innovation globally.

Market Restraints

High Cost of Advanced Aerospace Materials

Advanced composites, titanium alloys, and specialty aerospace materials involve substantial manufacturing and processing costs. Raw material procurement, certification, and fabrication expenses remain significantly higher than traditional metals. High costs can limit adoption among smaller manufacturers and suppliers, particularly in developing regions.

Stringent Certification and Regulatory Requirements

Aerospace materials must undergo extensive qualification, testing, and certification processes before commercial deployment. Compliance with aviation safety standards increases development timelines and costs. Regulatory complexity often delays product commercialization and limits the pace of material innovation.

Raw Material Supply Constraints

The aerospace industry depends on a limited number of suppliers for critical materials such as titanium, carbon fiber, and specialty alloys. Supply disruptions, geopolitical tensions, and trade restrictions can impact production schedules and increase procurement costs. Material shortages continue to present operational risks across global aerospace supply chains.

Complex Manufacturing Processes

Advanced aerospace materials often require specialized production technologies, skilled labor, and precision manufacturing capabilities. Integration challenges and capital-intensive production infrastructure increase operational costs. These factors can create barriers for new entrants and limit scalability.

Price Volatility of Metals and Composites

Fluctuations in aluminum, titanium, nickel, and carbon fiber prices directly impact manufacturing costs. Market volatility can affect profitability, procurement planning, and long-term supply agreements. Aerospace manufacturers face increasing pressure to manage material costs while maintaining product quality standards.

Get Detailed Table of Contents (TOC) - Request Now for Complete Market Insights: https://www.databridgemarketresearch.com/toc/?dbmr=global-aerospace-materials-market

Market Opportunities

Growth of Sustainable Aviation Programs

Global efforts to reduce aviation emissions are encouraging the adoption of lightweight and sustainable aerospace materials. Manufacturers are investing in recyclable composites, bio-based resins, and low-carbon production processes. These developments create long-term opportunities for material suppliers aligned with sustainability objectives.

Expansion of Aerospace Manufacturing in Asia Pacific

China, India, Japan, and Southeast Asian countries are investing heavily in aerospace production capabilities and supply chain localization. Government incentives, rising aircraft demand, and indigenous aircraft programs are creating attractive growth opportunities for material manufacturers.

Adoption of Additive Manufacturing Technologies

The increasing use of additive manufacturing in aerospace production enables lightweight component fabrication, material optimization, and cost reduction. Aerospace companies are integrating 3D printing technologies to accelerate product development and improve manufacturing efficiency.

Increasing Demand from Space and Satellite Industries

The commercialization of space exploration and satellite deployment programs is generating new demand for advanced aerospace materials. Reusable launch systems, satellite constellations, and deep-space missions require high-performance materials capable of operating under extreme conditions.

Strategic Partnerships and Supply Chain Expansion

Collaborations between aerospace OEMs, material suppliers, and research institutions are accelerating innovation and market penetration. Joint development programs and long-term supply agreements create opportunities for technology transfer, product differentiation, and market expansion.

Market Challenges

Lengthy Product Qualification Cycles

Aerospace materials require extensive validation and testing before deployment. Qualification programs often take several years, delaying revenue realization and increasing development costs. The lengthy approval process presents a significant challenge for emerging material technologies.

Supply Chain Vulnerability

Global aerospace supply chains remain susceptible to geopolitical tensions, transportation disruptions, and raw material shortages. Dependence on specialized suppliers can create bottlenecks affecting aircraft production and delivery schedules.

Skilled Workforce Shortages

The production of advanced aerospace materials requires highly specialized engineering and manufacturing expertise. Talent shortages in materials science, aerospace engineering, and advanced manufacturing continue to affect industry productivity and innovation.

Intense Competitive Pressure

Leading suppliers compete aggressively through innovation, pricing strategies, and long-term contracts with aerospace OEMs. New entrants face substantial barriers due to certification requirements, established supplier relationships, and capital-intensive operations.

Economic and Aviation Industry Cyclicality

The aerospace sector is sensitive to economic conditions, airline profitability, and government defense budgets. Economic slowdowns, reduced air travel demand, or delayed aircraft procurement programs can negatively impact material demand and market growth.

Market Segmentation & Analysis

By Material Type

Composites

Composites represent the largest material segment, accounting for approximately 40%-45% of market revenue. Their superior strength-to-weight ratio, corrosion resistance, and fuel-efficiency benefits make them indispensable in modern aircraft structures. The segment is expected to record the fastest growth, supported by increasing use in commercial and military aircraft.

Aluminum Alloys

Aluminum alloys remain widely utilized due to cost-effectiveness, machinability, and structural performance. They continue to dominate several aircraft structural applications despite increasing composite adoption. Demand remains strong in commercial aviation programs.

Titanium Alloys

Titanium alloys are increasingly adopted in engines and high-stress structural components due to exceptional strength and heat resistance. Growing use in next-generation aircraft platforms is supporting above-average growth rates.

Steel Alloys and Superalloys

These materials are primarily used in landing gear systems, engine components, and high-temperature applications. Their durability and fatigue resistance remain critical for aerospace performance requirements.

By Application

Airframe Structures

Airframe structures constitute the largest application segment, representing more than one-third of market demand. Fuselages, wings, empennage structures, and primary load-bearing components require significant quantities of advanced materials.

Engine Components

Engine applications are witnessing strong growth due to increasing use of high-temperature alloys and ceramic matrix composites. Demand is driven by fuel-efficiency improvements and next-generation propulsion systems.

Interior Components

Cabin interiors increasingly utilize lightweight composites and polymers to reduce aircraft weight and improve passenger comfort. Airlines continue to invest in cabin modernization programs.

MRO Applications

Maintenance, Repair, and Overhaul (MRO) activities create recurring demand for aerospace materials throughout aircraft lifecycles. Growing global aircraft fleets support steady segment growth.

By End User

OEMs

OEMs represent the largest end-user segment, accounting for over 60% of total market demand. Aircraft manufacturers consume substantial quantities of aerospace materials during production activities.

MRO Providers

MRO providers represent a growing segment due to increasing fleet age and maintenance requirements. Airlines are investing in lifecycle extension programs, supporting aftermarket material demand.

Defense Organizations

Military aviation programs require specialized aerospace materials for combat aircraft, helicopters, and defense platforms. Defense procurement continues to drive material innovation.

Analytical Insights

Largest Segment: Composites

Fastest-Growing Segment: Composites

Largest Application Segment: Airframe Structures

Largest End-User Segment: OEMs

Dominance is supported by aircraft lightweighting initiatives, fuel-efficiency requirements, and expanding aircraft production programs.

Regional Analysis

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America - Dominant Region

North America remains the largest regional market, accounting for approximately 38%-40% of global revenue. The region benefits from the presence of major aerospace manufacturers, advanced R&D capabilities, and robust defense spending. The United States serves as the primary contributor due to its extensive aerospace ecosystem, aircraft production facilities, and space exploration programs. Strong certification infrastructure further supports regional leadership.

Europe - Mature Market

Europe represents a well-established aerospace materials market supported by strong aerospace manufacturing activity and technological innovation. Germany, the United Kingdom, and France remain major contributors. Significant investments in sustainable aviation technologies and advanced material research continue to support steady market growth. The region also benefits from a strong aerospace supplier network.

Asia Pacific - Fastest Growing Region

Asia Pacific is projected to record the highest CAGR throughout the forecast period. Rapid industrialization, expanding airline fleets, increasing aircraft production, and government-backed aerospace programs in China, India, and Japan are driving demand. Regional supply chain localization initiatives further enhance growth prospects.

Latin America - Emerging Region

Latin America remains a developing market characterized by gradual aerospace infrastructure improvements and increasing aircraft maintenance activities. Brazil and Mexico serve as key contributors due to growing aerospace manufacturing capabilities and regional aviation demand. Economic constraints continue to limit rapid expansion.

Middle East & Africa - Gradual Growth

The Middle East & Africa market is experiencing moderate growth supported by airline expansion, defense investments, and government-led aviation development programs. Gulf countries continue to invest in aerospace infrastructure and maintenance facilities, while broader regional growth remains constrained by industrial and supply chain limitations.

Key Insights

Largest Region: North America

Fastest Growing Region: Asia Pacific

Mature Markets: North America, Europe

High-Growth Markets: Asia Pacific

Emerging Markets: Latin America, Middle East & Africa

Key regional differences are driven by aerospace manufacturing concentration, technology adoption rates, supply chain maturity, defense spending, and government industrial policies.

Competitive Landscape

Market Structure Overview

The aerospace materials market is moderately consolidated, characterized by the presence of global material manufacturers, aerospace-focused suppliers, and specialized technology providers. Competition is driven by material innovation, certification capabilities, manufacturing expertise, and long-term supply agreements with aerospace OEMs. Market participants focus heavily on R&D investments to strengthen competitive positioning and expand product portfolios.

Key Industry Players

Leading companies compete through advanced material technologies, global production networks, and strategic collaborations with aerospace manufacturers. Market leaders emphasize lightweight composites, specialty alloys, and next-generation aerospace materials to address evolving aircraft performance requirements.

List of Key Industry Players

Hexcel Corporation

Toray Industries, Inc.

Solvay S.A.

Teijin Limited

SGL Carbon

Arconic Corporation

Constellium SE

VSMPO-AVISMA Corporation

Kobe Steel, Ltd.

Mitsubishi Chemical Group

Competitive Strategies

Companies are pursuing product innovation, aerospace certification programs, strategic partnerships, and capacity expansion initiatives. Mergers and acquisitions remain important for technology acquisition and geographic expansion. Market participants increasingly focus on sustainable materials, additive manufacturing, and advanced composite technologies to differentiate offerings and strengthen customer value propositions.

Emerging Players & Market Dynamics

Emerging material innovators and specialty composite manufacturers are introducing niche aerospace solutions focused on lightweighting and sustainability. Increased venture funding, advanced manufacturing adoption, and digital transformation initiatives are intensifying competition. New entrants primarily compete through technological specialization and cost-efficient production approaches.

Latest Developments

January 2025 - Toray Industries

Expanded advanced carbon fiber production capabilities to support increasing aerospace composite demand. The expansion strengthens global supply availability and supports next-generation aircraft manufacturing requirements.

October 2024 - Hexcel Corporation

Introduced advanced aerospace composite solutions designed to improve structural performance and manufacturing efficiency. The development supports increasing adoption of lightweight aircraft structures.

July 2024 - Solvay

Expanded its aerospace materials portfolio through advanced thermoplastic composite technologies aimed at reducing aircraft weight and improving sustainability performance.

March 2024 - Airbus and Material Suppliers Consortium

Strengthened collaborative programs focused on sustainable aviation materials and recyclable composite technologies. The initiative supports industry decarbonization objectives and long-term material innovation.

November 2023 - Boeing Supply Chain Partners

Increased investments in lightweight aerospace materials and digital manufacturing technologies to enhance aircraft production efficiency and supply chain resilience.

August 2023 - Teijin Limited

Expanded aerospace composite manufacturing capabilities in response to growing global demand from commercial and defense aviation programs.

May 2023 - Global Aerospace Manufacturers

Accelerated adoption of additive manufacturing technologies for aerospace-grade components, supporting material optimization, reduced waste generation, and improved production flexibility.

February 2023 - Aerospace Industry Regulatory Bodies

Advanced sustainability-focused aerospace material standards and certification frameworks, encouraging broader adoption of lightweight and environmentally responsible materials across aircraft platforms.

Check out more related studies published by Data Bridge Market Research:

https://www.databridgemarketresearch.com/reports/global-calcium-tartrate-market

https://www.databridgemarketresearch.com/reports/global-caprylic-acid-market

https://www.databridgemarketresearch.com/reports/global-carbon-black-market

https://www.databridgemarketresearch.com/reports/global-cross-linked-polyethylene-market

https://www.databridgemarketresearch.com/reports/global-cutting-fluid-lubricants-market

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com

Data Bridge Market Research is a market research and consulting company that educates its clients about the market and encourages growth and expansion. We offer customized reports, syndicated research, consulting services, cloud-connected intelligence, and a holistic suite of offerings including competitive intelligence, epidemiology analyses, trade analytics, country analysis, and pharma insights.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Aerospace Materials Market Research Report 2026-2032: Opportunities, Trends, and Growth Projections at 8.7% CAGR here

News-ID: 4541838 • Views: …

More Releases from Data Bridge Market Research

Europe Epigenetics Diagnostic Market Size Projected to Hit USD 5.43 billion by 2 …

Market Summary

As per Data Bridge Market Research analysis, the Europe Epigenetics Diagnostic Market was estimated at USD 2.34 billion in 2025. The market is expected to grow from USD 2.08 billion in 2024 to USD 5.43 billion by 2032, at a CAGR of 12.70% during the forecast period driven by the rising demand for early-stage precision oncology, expanding utilization of non-invasive liquid biopsy platforms, increasing research investments in histone modification…

Age-Related Macular Degeneration (AMD) Anti-VEGF Therapeutics Market: Industry A …

Market Summary

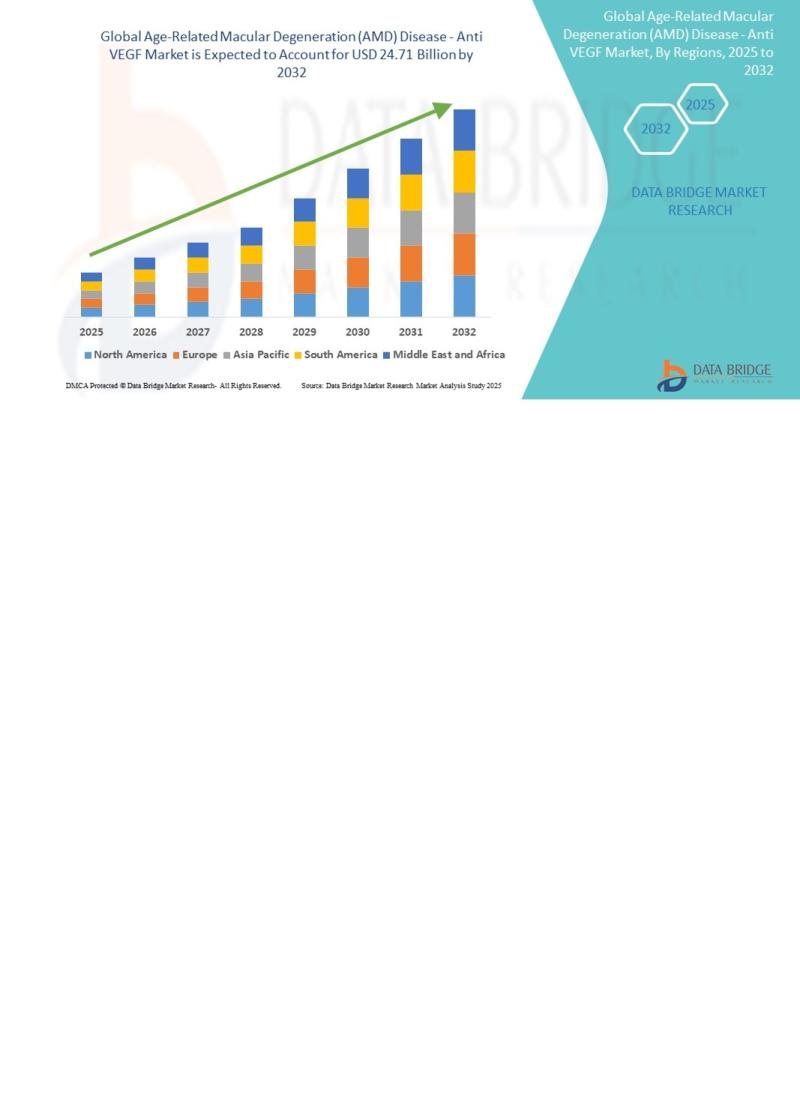

As per Data Bridge Market Research analysis, the Age-Related Macular Degeneration (AMD) Disease - Anti-VEF Market was estimated at USD 15.59 billion in 2025. The market is expected to grow from USD 16.65 billion in 2026 to USD 24.71 billion in 2032, at a CAGR of 6.80% during the forecast period with driven by the rising demand for effective retinal disease therapies, increasing prevalence of age-related vision disorders, advancements…

Yogurt Powder Market Size Expected to Reach USD 1.41 Billion by 2032 at a CAGR o …

Market Summary

As per Data Bridge Market Research analysis, the Yogurt Powder Market was estimated at USD 0.28 billion in 2025. The market is expected to grow from USD 0.30 billion in 2026 to USD 1.41 billion in 2032, at a CAGR of 8.10% during the forecast period with driven by the rising demand for shelf-stable dairy ingredients, growing consumption of functional and protein-enriched foods, expansion of the food processing industry,…

Pressure Transmitter Market Size, Share & Industry Trends Analysis Report - Glob …

As per Data Bridge Market Research analysis, the Pressure Transmitter Market was estimated at USD 3.41 billion in 2025. The market is expected to grow from USD 3.54 billion in 2026 to USD 4.44 billion in 2032, at a CAGR of 3.86% during the forecast period (2026-2032), driven by the rising demand for industrial automation, increasing adoption of Industry 4.0 technologies, expansion of oil & gas and process industries, and…

More Releases for Aerospace

Aerospace Wiring Harness Market will reach $4.1 billion by 2032: Amphenol Aerosp …

The Latest published market study on Global Aerospace Wiring Harness Market provides an overview of the current market dynamics in the Aerospace Wiring Harness space, as well as what our survey respondents- all outsourcing decision-makers- predict the market will look like in 2032. The study breaks the market by revenue and volume (wherever applicable) and price history to estimate the size and trend analysis and identify gaps and opportunities. Some…

Aerospace Composites Market Future Growth Insight And Competitive Outlook 2025 | …

The Global Aerospace Composites Market is expected to reach USD 57.04 billion by 2025, from USD 26.90 billion in 2017, growing at a CAGR of 9.4% during the forecast period of 2018 to 2025. The upcoming market report contains data for historic years 2015 & 2016, the base year of calculation is 2017 and the forecast period is 2018 to 2025.Global Aerospace Composites Market, By Fibre Type (Carbon, Glass, Ceramic),…

Aerospace Evacuation Market 2025 By Top Key Players UTC Aerospace Systems, Zodia …

Asia Pacific will witness a significant growth rate in the aerospace evacuation market place over the forecast timeframe. This is attributed to the increasing air travel coupled with investments in aviation industry across the region. International Air Transport Association (IATA) estimates that the region will have around 3.5 billion passengers by 2036.

Europe aircraft evacuation market holds substantial share with the expansion of airlines. In August 2018, Wizz Air announced expansion…

Aircraft Evacuation Market 2025 | UTC Aerospace Systems, GKN Aerospace, Zodiac A …

Asia Pacific aircraft evacuation market share will witness a significant growth owing to increasing demand for air travel. Further, as per IATA, the region is witnessing an annual increase of around 5.5% passenger traffic. Continuous investments by industry players for setting up of manufacturing facilities are further supporting the regional growth till 2025.

Europe aircraft evacuation market holds substantial share with the expansion of airlines. In August 2018, Wizz Air announced…

Aerospace Lavatory System Market Outlook to 2027 - Percival Aviation, Zodiac Aer …

The Aerospace Lavatory System Market research report analyzes factors affecting market from both demand and supply side and further evaluates market dynamics affecting the market during the forecast period i.e., drivers, restraints, opportunities, and future trend. The report also provides exhaustive Poter's five forces analysis.

Factors responsible to drive the growth of aerospace lavatory system is increase in the number of passengers has raised the demand for more commercial aircraft equipped…

Aerospace Control Surface Market - Spirit AeroSystems, Aernnova Aerospace, GKN A …

North America aerospace control surface market size is expected to lead owing to presence of key manufacturers in the region. Europe led by Germany, France, UK and Russia is estimated to witness significant growth in aerospace control surface market during the forecast timeframe. Advancement in technology with implementation of light weight composites allowing improved efficiency of aircraft will support the overall industry demand.

Aerospace control surface market can be segmented based…