Press release

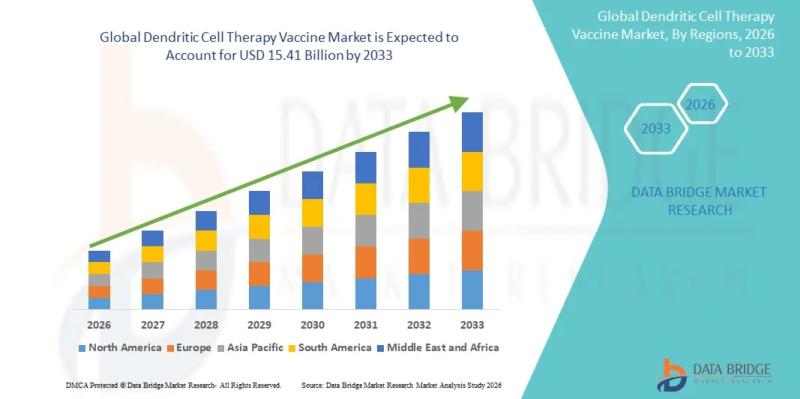

Dendritic Cell Therapy Vaccine Market to Hit USD 15.41 billion by 2033 at a 5.25% CAGR

Dendritic Cell Therapy Vaccine Market

As per Data Bridge Market Research analysis, the Dendritic Cell Therapy Vaccine Market was estimated at USD 10.24 billion in 2025. The market is expected to grow from USD 10.24 billion in 2025 to USD 15.41 billion by 2033, at a CAGR of 5.25% during the forecast period driven by the rising demand for targeted oncological immunotherapies, accelerating clinical pipeline investments, expanding clinical trial approvals for solid tumors, and technological innovations in automated ex vivo cell processing and scaling.

Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs): https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-dendritic-cell-therapy-vaccine-market

Market Size & Forecast

2025 Market Size: USD 10.24 Billion

2026 Projected Market Size: USD 10.24 Billion

2033 Projected Market Size: USD 15.41 Billion

CAGR (2026-2033): 5.25%

Largest Region: North America

Fastest Growing Region: Asia-Pacific

Key Market Report Takeaways

Regional Leadership: North America commands the largest global market share at approximately 41.30% due to an advanced clinical trial ecosystem, substantial healthcare infrastructure, and the presence of prominent industry players.

Fastest-Growing Region: The Asia-Pacific territory exhibits the highest global growth rate, driven by rapidly developing biopharmaceutical infrastructure, rising oncological disease prevalence, and supportive regional regulatory modifications.

Product Segment with Highest Market Share: Autologous Dendritic Cell Vaccines hold the dominant product market share owing to their high biocompatibility profiles, reduced risks of graft-versus-host rejection, and extensive clinical documentation.

Dominant Application Segment: Cancer Immunotherapy represents the leading application segment, relying heavily on dendritic cell platforms to target specific solid tumors, including prostate, melanoma, and glioblastoma pathways.

Leading End-Use Segment: Hospitals and Specialized Oncology Centers lead the procurement sector, functioning as the primary clinical venues for cell extraction, processing coordination, and patient vaccine infusion.

Details about the report and current availability can be viewed: https://www.databridgemarketresearch.com/reports/global-dendritic-cell-therapy-vaccine-market

Key Market Trends & Highlights

North American Regional Infrastructure Consolidation: North America leads the global landscape because extensive clinical trial investments, proactive FDA regenerative medicine advanced therapy designations, and an established network of cell-processing centers facilitate accelerated commercial vaccine production.

Asia-Pacific Structural Acceleration: Asia-Pacific stands as the fastest-growing global region due to rapid modernization of biopharmaceutical manufacturing pipelines, growing healthcare budgets, and updating clinical approval tracks across China, India, and Japan.

Dominance of Oncological Cellular Applications: The oncology segment commands the market as therapeutic developers increasingly prioritize dendritic cell platforms over traditional non-specific chemotherapies to minimize patient systemic toxicity.

Escalating Targeted Immunotherapy Demand: Market expansion is driven by a strong shift toward personalized medicine formats that harness a patient's own immune system, aligning directly with global healthcare initiatives focused on precision oncology.

Emerging Automated Ex Vivo Cell Processing Technologies: Advanced closed-system bioprocessing platforms, automated leukapheresis equipment, and specialized bioreactor systems are transforming production lines by ensuring high cellular purity and minimizing manual handling contamination risks.

Strategic Regulatory and Distribution Alliances: Major cellular therapeutics developers are forming long-term manufacturing agreements and direct cold-chain logistics joint ventures to streamline cryogenic transport and protect cellular viability across global supply networks.

Market Dynamics

Market Drivers

Technological Advancements in Automated Ex Vivo Cell Processing Systems: The implementation of innovative closed-system bioreactors and automated cell selection mechanisms allows therapeutic developers to process cellular materials with high precision. These updated systems optimize cell yield, enhance antigen-loading efficiency, and maintain standard cellular quality controls while shortening overall preparation cycles. This increased processing consistency helps cellular manufacturing facilities scale up production lines, supporting dependable clinical delivery pipelines.

Rising Global Demand for Personalized Oncology Therapeutics: Oncology patient populations and clinical groups are actively seeking highly targeted immunotherapy options that present fewer systemic side effects compared to traditional cytotoxic chemotherapies. Dendritic cell vaccines fulfill this clinical requirement by leveraging patient-specific tumor antigens to train autologous T-cells against specific malignancies. This deep alignment with precision medicine standards drives significant treatment adoption and volume growth across major hospital networks.

Expanding Clinical Pipelines and Increased Regulatory Fast-Track Designations: Global biopharmaceutical enterprises and research universities are steadily expanding their oncology portfolios to include novel dendritic cell formulations targeting glioblastoma, prostate, and lung carcinomas. Regulatory bodies assist this development by granting fast-track status and orphan drug designations to promising cellular therapies, which reduces clinical timeline barriers. This proactive regulatory support builds consistent, multi-year research and commercial investment momentum.

Favorable Government Funding Initiatives and Biopharmaceutical Investment Inflows: Public healthcare authorities and private venture capital funds are refining their investment pipelines to allocate substantial capital toward advanced therapy medicinal products (ATMPs). These financial commitments optimize early-stage clinical trial designs, improve specialized cell processing infrastructure, and reduce baseline technical hurdles for developer companies. This financial support enables manufacturers to expand their research operations while widening their international therapeutic footprints.

Market Restraints

High Initial Setup Expenditures and Intensive Cellular Processing Operational Costs: Establishing specialized Good Manufacturing Practice (GMP) cell-processing laboratories and acquiring precision automated leukapheresis systems require massive upfront capital outlays that challenge mid-tier therapeutic developers. Additionally, executing custom ex vivo cellular modifications requires expensive single-use consumables and specialized cleanroom utilities, which raises operational overhead costs. These combined financial demands limit profitability margins, preventing quick price adjustments in cost-sensitive regional healthcare systems.

Strict Regulatory Compliance Controls and Complex Quality Standardization Frameworks: Global health organizations enforce highly detailed regulatory guidelines regarding product sterility, cellular identity metrics, and potency standards for living cell therapies. Batches that fail to meet these strict cellular quality baselines face immediate rejection, clinical trial delays, or complete batch discard protocols. Managing these differing regional compliance guidelines increases manufacturing quality-control spending and heightens logistical risks for international distributors.

Complex Supply Chain Logistics Cascading from Rigid Cryopreservation Requirements: Moving living cellular therapies requires continuous ultra-low temperature cryogenic logistics to ensure cell viability from initial extraction to final patient re-infusion. Any unexpected transport delay, equipment breakdown, or temperature deviation along the distribution chain immediately ruins the therapeutic batch, creating heavy financial losses. This extreme logistical vulnerability complicates distribution networks, particularly across developing regions with limited cold-chain infrastructure.

Intense Clinical Competition from Alternative Immunotherapy Modalities: The cellular oncology landscape is highly saturated with established immune checkpoint inhibitors, advanced CAR-T cell therapies, and cost-effective monoclonal antibodies that compete directly for clinical usage. Many of these alternative modalities feature faster manufacturing timelines and simpler off-the-shelf logistics, making them attractive options for healthcare networks. This continuous competitive pressure limits the immediate market share potential of custom dendritic cell vaccine rollouts.

Market Opportunities

Deployment of Combined Checkpoint Inhibitor and Adjuvant Therapeutic Lines: Incorporating advanced dendritic cell vaccines in combination with established anti-PD-1 or anti-CTLA-4 checkpoint therapies provides a clear path to generating highly effective treatment regimens. These combination therapies work together to trigger stronger immune responses while preventing tumor cells from escaping detection. These clinical strategy investments allow forward-thinking pharmaceutical brands to capture premium positions in advanced combination oncology markets.

Penetration into Untapped Premium Healthcare Facilities Across High-Growth Corridors: Building dedicated cell-collection partnerships, specialized regional processing centers, and targeted oncological networks across expanding economies creates high-margin revenue streams. Developing urban landscapes allow global biotech firms to introduce premium cellular therapies as local private hospitals upgrade their oncology treatment capabilities. This geographic focus helps pioneering companies secure market share ahead of slower competitors.

Strategic Manufacturing Alliances with Specialized Contract Development and Manufacturing Organizations (CDMOs): Partnering with established cell therapy CDMOs and automated bioprocessing platforms unlocks valuable operational efficiencies by outsourcing complex scaling tasks. Utilizing third-party manufacturing infrastructure reduces initial capital requirements, optimizes asset use, and shortens commercial launch timelines for early-stage developers. These collaborative production arrangements expand market flexibility and strengthen overall supply chain security.

Development of Off-the-Shelf Allogeneic Dendritic Cell Platforms: Using advanced gene-editing methods to create universal, non-patient-specific allogeneic dendritic cell lines offers an opportunity to build a new product category. These innovative platforms eliminate the lengthy wait times of autologous cell collection, allowing physicians to initiate targeted immunotherapy immediately upon patient diagnosis. This product evolution allows cell therapy manufacturers to capture high-volume returns from acute oncology sectors.

Market Challenges

Fragmented Traceability Documentation Criteria Across International Borders: Different national health agencies require separate chain-of-custody tracking certificates and distinct cell-source verification documents for cross-border biological shipments. This regulatory fragmentation forces global therapy providers to continuously re-audit their internal tracking databases to stay compliant with changing regional laws. Managing these overlapping documentation paths slows down distribution velocity and increases corporate administrative spending.

Maintaining High Cellular Viability Across High-Volume Patient Groups: Living cell therapies are naturally sensitive to processing variations, and patient-derived cells can vary significantly in quality and strength depending on a person's health status. In large-scale clinical rollouts, these variations make it difficult to guarantee identical therapeutic potency for every single batch produced. Ensuring stable, high-potency cellular outputs across thousands of individual patients remains a difficult and costly operational challenge.

Rapidly Shifting Reimbursement Policies and Volatile Insurance Coverage Criteria: Unforeseen changes in national insurance coverage models and sudden updates to government drug pricing lists can rapidly destabilize commercial sales plans. A sudden reduction in insurance coverage directly increases out-of-pocket costs for patients, making cellular treatments unaffordable for most demographics overnight. This high level of reimbursement uncertainty challenges corporate planners trying to project reliable long-term sales growth.

Macroeconomic Inflationary Pressures Compressing Public Healthcare Budgets: Ongoing economic slowdowns, rising hospital utility costs, and tighter government budgets can force public health systems to re-evaluate their spending on high-cost medical therapies. When healthcare budgets contract, procurement offices often favor traditional, low-cost generic oncology drugs over premium personalized cell therapies. This shift in healthcare purchasing patterns creates sales volume volatility for specialized biotech firms operating in affected regions.

Get Detailed Insights Before You Buy - Request Complete Market Intelligence Now: https://www.databridgemarketresearch.com/checkout/buy/global-dendritic-cell-therapy-vaccine-market/compare-licence

Market Segmentation & Analysis

Segmentation Structure

The market is structured into separate categories based on product type, application type, and primary end-user to monitor clinical consumption trends.

Segment-Wise Analytical Breakdown

By Product Type

Autologous Vaccines: Commands the highest market revenue share (over 72.00% of global value) due to their minimal risk of immunological rejection, high patient biocompatibility, and widespread clinical trial utilization.

Allogeneic Vaccines: Represents the fastest-growing product segment, expanding at an elevated CAGR due to rising research focus on developing off-the-shelf formulations that bypass customized cell extraction timelines.

By Application Type

Cancer Immunotherapy: Holds the largest operational segment share, driven by extensive global clinical spending to target melanoma, renal cell carcinoma, and colorectal malignancies.

Infectious Disease Management: Represents an expanding technology application, capturing market share as research pipelines explore dendritic cells for targeted antiviral immunotherapies.

By End-User

Hospitals & Specialized Oncology Clinics: Commands the primary market footprint, as these institutions maintain the complex clinical infrastructure and leukapheresis equipment required to administer advanced cell therapies.

Biopharmaceutical Research Institutes: Functions as a key foundational segment, driving volume growth through early-phase clinical trial management and cellular translation studies.

Analytical Insights

The combination of Autologous Vaccines utilized within Cancer Immunotherapy applications remains the largest revenue generator for this market. This configuration dominates because patient-derived cells minimize immune rejection risks, making them the preferred framework for regulatory bodies approving advanced personalized oncology lines. Concurrently, Allogeneic Vaccines managed by Biopharmaceutical Research Institutes represents the fastest-growing sector. Growth in this area is accelerated by the industry-wide push for scalable, off-the-shelf treatments, as allogeneic platforms eliminate patient cell extraction delays and lower production costs, meeting the demand for standardized cellular options.

Regional Analysis

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America - This region holds the largest global market footprint, accounting for approximately 41.30% of global market revenue. Growth is sustained by an advanced oncology research network, extensive federal funding allocations for cell therapy development, and clear regulatory frameworks like the FDA's regenerative medicine designation pathway. The United States serves as the primary regional contributor due to its concentration of leading biopharmaceutical companies and high clinical adoption rates for personalized medicine.

Europe - Functions as a highly established and steadily growing market, supported by strong institutional R&D investments, robust clinical trial frameworks, and consistent demand for advanced oncology therapeutics. Strict cell therapy compliance standards established by regional health authorities ensure high processing quality across the territory. Key national contributors driving procurement volumes through centralized hospital systems include Germany, the United Kingdom, and France.

Asia Pacific - Identified as the fastest-growing geographical market during the forecast period, expanding rapidly due to accelerating biopharmaceutical industrialization, supportive regional clinical regulations, and expanding healthcare budgets. The rapid modernization of cell processing centers and growing investments in precision medicine across China, India, and Japan provide an ideal foundation for cellular therapies. Government initiatives aimed at streamlining biotech approvals further accelerate local market development.

Latin America - Operating as an emerging regional market focused on updating local clinical trial infrastructure and expanding premium oncology specialized clinics. Countries like Brazil and Mexico are showing gradual technology adoption and steady improvements in localized biological storage networks, though broader market growth faces limitations from regional economic fluctuations and varying patient healthcare access across demographics.

Middle East & Africa - Exhibits gradual, steady growth, driven by new private sector clinical investments, focused government health initiatives in affluent regions, and expanding international healthcare partnerships. While advanced medical centers within the Gulf Cooperation Council (GCC) nations drive early adoption of cell therapies, overall regional market acceleration is balanced by infrastructure and specialist availability gaps in less developed sub-Saharan territories.

Key Insights:

Largest Region: North America

Fastest Growing Region: Asia-Pacific

Competitive Landscape

Market Structure Overview

The global dendritic cell therapy vaccine market displays a moderately consolidated structure, led by established global biopharmaceutical leaders, specialized cellular therapy innovators, and collaborative clinical research institutions. The competitive landscape is shaped by ongoing technological innovations, with companies focusing on advanced automated cell manufacturing and strategic regulatory positioning to gain a competitive advantage. Analyzing this competitive framework helps clarify the market positioning, product strengths, and future strategic directions of the sector's key players.

Key Industry Players

Dendreon Pharmaceuticals LLC: Maintains a leading market position through its established autologous cellular immunotherapy platform for advanced prostate cancer management.

Northwest Biotherapeutics, Inc.: A major global participant specializing in personalized immune therapies for solid tumors, leveraging advanced ex vivo antigen loading technologies.

Medigene AG: Concentrates on developing highly tailored dendritic cell vaccine lines, using an innovative automated screening platform to treat specialized myeloid malignancies.

Elios Therapeutics, LLC: Uses its extensive clinical development networks and targeted vaccine portfolio to advance autologous treatments for high-risk melanoma populations.

Agenus Inc.: An innovative cellular therapeutics producer focused on combining dendritic cell platforms with novel adjuvant combinations to maximize anti-tumor immune responses.

Competitive Strategies

Leading companies rely on strategic product launches and targeted technological innovations to expand their portfolios and address unmet clinical needs. Many firms use collaborative partnerships, mergers, and acquisitions to strengthen their global distribution networks and improve their long-term customer value proposition. Additionally, companies are using advanced data analytics and specialized clinical support services to differentiate their products and maintain strong relationships with major regional healthcare networks.

Emerging Players & Market Dynamics

Specialized biotechnology startups and niche innovators are increasingly active, introducing competitive pressure by developing targeted gene therapies and alternative oral delivery systems. These emerging companies often focus on disruptive, cost-effective solutions that challenge the market share of established pharmaceutical leaders. This segment is supported by growing venture capital investments and funding rounds, with an increasing industry-wide emphasis on digital transformation and advanced molecular engineering.

Latest Developments

January 2026 - Northwest Biotherapeutics, Inc.: Secured expanded regulatory approvals across European medical markets for its flagship autologous dendritic cell platform, optimizing therapy deployment options for adult glioblastoma patients.

November 2025 - Dendreon Pharmaceuticals LLC: Completed an automation upgrade across its main US cell-processing facilities, increasing commercial production capacity for its cellular immunotherapy line by 25%.

August 2025 - Medigene AG: Formed a strategic research partnership with an international oncology institute to advance its next-generation dendritic cell vaccine candidates through Phase II clinical testing.

April 2025 - Elios Therapeutics, LLC: Published positive long-term survival data from its multi-center clinical trial investigating personalized dendritic cell treatments for high-risk melanoma patients.

October 2024 - Agenus Inc.: Entered a specialized manufacturing and logistics collaboration with a leading biopharmaceutical CDMO to optimize cold-chain distribution workflows for its cellular vaccine portfolio.

June 2024 - DC Prime BV: Expanded its clinical development pipelines by initiating a multi-center study combining allogeneic dendritic cell formulations with standard checkpoint inhibitors for solid tumor indications.

Check out more related studies published by Data Bridge Market Research:

https://www.databridgemarketresearch.com/reports/global-dried-fruits-market

https://www.databridgemarketresearch.com/reports/global-hot-drinks-market

https://www.databridgemarketresearch.com/reports/global-dendritic-cell-therapy-vaccine-market

https://www.databridgemarketresearch.com/reports/global-drilling-fluids-market

https://www.databridgemarketresearch.com/reports/global-ai-driven-care-navigation-services-market

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com

An absolute way to forecast what the future holds is to comprehend the trend today!

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Dendritic Cell Therapy Vaccine Market to Hit USD 15.41 billion by 2033 at a 5.25% CAGR here

News-ID: 4539533 • Views: …

More Releases from Data Bridge Market Research

Hot Drinks Market Outlook: Driving Toward USD 346.81 billion by 2032

As per Data Bridge Market Research analysis, the Hot Drinks Market was estimated at USD 229.13 billion in 2025. The market is expected to grow from USD 215.96 billion in 2024 to USD 346.81 billion by 2032, at a CAGR of 6.10% during the forecast period driven by the rising demand for premium, organic, and ethically sourced coffee and tea varieties, major engineering innovations in automated smart brewing appliances, rapid…

Mediterranean Fever Treatment Market Outlook (2026-2032): Expected to Reach USD …

"As per Data Bridge Market Research analysis, the Mediterranean Fever Treatment Market was estimated at USD 5.91 billion in 2025. The market is expected to grow from USD 7.09 billion in 2026 to USD 21.31 billion in 2032, at a CAGR of 20.10% during the forecast period with driven by the rising demand for advanced rare disease therapeutics, improved genetic diagnostics, and increasing awareness of autoinflammatory disorders across developed and…

Meningitis Treatment Market to Reach USD 0.270 Billion by 2032, Growing at a CAG …

"As per Data Bridge Market Research analysis, the Meningitis Treatment Market was estimated at USD 0.201 billion in 2025. The market is expected to grow from USD 0.210 billion in 2026 to USD 0.270 billion in 2032, at a CAGR of 4.30% during the forecast period with driven by the rising demand for advanced antimicrobial therapies, improved diagnostic capabilities, and increasing incidence of bacterial and viral meningitis globally.

Get the full…

Pork Extract Market Forecast Report 2026-2032: Growing at a CAGR of 5.40% to Ach …

As per Data Bridge Market Research analysis, the Pork Extract Market was estimated at USD 4.80 billion in 2025. The market is expected to grow from USD 5.05 billion in 2026 to USD 6.94 billion in 2032, at a CAGR of 5.40% during the forecast period (2026-2032), driven by the rising demand for processed and convenience foods, increasing consumption of meat-based flavoring ingredients, expansion of the foodservice industry, and ongoing…

More Releases for Cell

Cell Sorting Market Accelerates as Cell Therapy, Immuno-Oncology & Single-Cell R …

The rising focus on precision medicine, immunotherapy, and advanced cell-based research is driving the global cell sorting market into a high-growth phase. With expanding applications in stem cell therapy, CAR-T manufacturing, cancer immunology, and single-cell genomics, demand for accurate, high-purity cell isolation systems is stronger than ever. This release highlights key market trends, segmentation insights, technological innovations, and the factors shaping the future of cell sorting.

Download Full PDF Sample Copy…

Cell Isolation Cell Separation Market Size Analysis by Application, Type, and Re …

According to Market Research Intellect, the global Cell Isolation Cell Separation market under the Internet, Communication and Technology category is expected to register notable growth from 2025 to 2032. Key drivers such as advancing technologies, changing consumer behavior, and evolving market dynamics are poised to shape the trajectory of this market throughout the forecast period.

The market for cell isolation and separation is expanding rapidly as a result of sophisticated biotechnological…

Cell Free Protein Synthesis Market Beyond the Cell: Revolutionizing Protein Prod …

Cell-Free Protein Synthesis Market to reach over USD 457.13 Mn by the year 2031 - Exclusive Report by InsightAce Analytic

"Cell-Free Protein Synthesis Market" in terms of revenue was estimated to be worth $265.94 Mn in 2023 and is poised to reach $457.13 Mn by 2031, growing at a CAGR of 7.20% from 2024 to 2031 according to a new report by InsightAce Analytic.

Request for free Sample Pages: https://www.insightaceanalytic.com/request-sample/1445

Current…

Cell Expansion Market - Expand the Boundaries of Cell Therapy: Redefine Cell Exp …

Newark, New Castle, USA: The "Cell Expansion Market" provides a value chain analysis of revenue for the anticipated period from 2022 to 2030. The report will include a full and comprehensive analysis of the business operations of all market leaders in this industry, as well as their in-depth market research, historical market development, and information about their market competitors

Cell Expansion Market: https://www.growthplusreports.com/report/cell-expansion-market/7939

This latest report researches the industry structure, sales, revenue,…

Global GMP Cell Banking Market By Type - Mammalian Cell, Microbial Cell, Insect …

Researchmoz added Most up-to-date research on "Global GMP Cell Banking Market By Type - Mammalian Cell, Microbial Cell, Insect Cell and Others" to its huge collection of research reports.

This report researches the worldwide GMP Cell Banking market size (value, capacity, production and consumption) in key regions like North America, Europe, Asia Pacific (China, Japan) and other regions.

This study categorizes the global GMP Cell Banking breakdown data by manufacturers, region, type…

Cell Culture Market Size, Cell Culture Market Share, Cell Culture Market Trends …

According to a new research published by Polaris Market Research the global cell culture market is anticipated to reach more than USD 49 billion by 2026. Cell culture is a rapidly emerging as an implement for analyzing and treating various disease such as Alzheimer’s and cancer.

Request for Sample of This Research Report @ https://bit.ly/2D7pZ5u

Top Key Players: -

Becton,

Dickinson and Company

Biospherix

EMD Millipore

Eppendorf AG

Merck KGaA

Sartorius AG

VWR International

Cell culture is a rapidly emerging…