Press release

Australia Plasterboard Market 2026 | Worth USD 1,833.9 Million by 2034 | CAGR of 7.82%

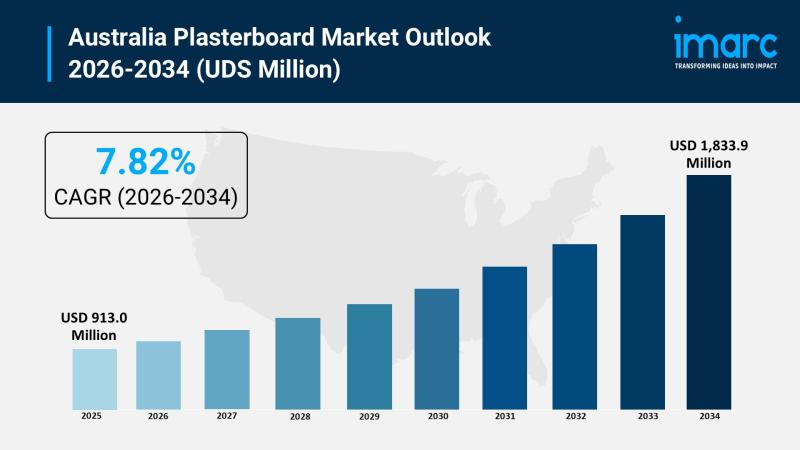

The Australia plasterboard market size reached USD 913.0 Million in 2025. Looking forward, the market is expected to reach USD 1,833.9 Million by 2034, exhibiting a growth rate (CAGR) of 7.82% during 2026-2034. Australia represents one of the most dynamic plasterboard markets in the Asia-Pacific region, driven by strong residential and commercial building activity, tightening safety and energy-efficiency regulatory standards, and an accelerating industry-wide focus on sustainable construction materials. The convergence of urbanization-led housing demand, government stimulus programs, natural disaster resilience requirements, and technological innovation in fire-resistant, moisture-resistant, and smart plasterboard products is shaping a rapidly expanding market landscape that continues to attract investment and product development across all board types, forms, and end-use sectors throughout the country.

Request for a sample report PDF: https://www.imarcgroup.com/australia-plasterboard-market/requestsample

Australia Plasterboard Market Summary:

• Australia's residential housing sector is performing robustly, with dwelling commencements rising 4.6% to 43,247 (seasonally adjusted) as of September 2024 and private sector house building approvals continuing to signal a strong pipeline of new residential projects - both of which directly drive plasterboard consumption as the foundational material for interior wall and ceiling applications across the country's growing housing stock.

• The growing commercial construction industry in major cities including Brisbane, Perth, and Melbourne is generating sustained demand for plasterboards with enhanced fire rating and acoustic performance, as developers and building owners invest in office buildings, retail centers, healthcare facilities, and educational institutions that must meet increasingly stringent occupant safety and comfort requirements under Australia's national and state building codes.

• Australia's exposure to natural disasters including bushfires, cyclones, and floods has resulted in stricter building codes and a measurable shift in material specification toward fire-resistant, moisture-resistant, and impact-resistant plasterboard products - with disaster rebuilding activity also generating steady incremental demand that complements new construction volumes across affected regions.

• Technological innovation is advancing plasterboard product performance well beyond traditional applications, with manufacturers developing boards incorporating enhanced fire protection, acoustic insulation, moisture regulation, and thermal efficiency - as well as emerging smart technologies such as embedded sensors for temperature and humidity monitoring that increase plasterboard's functionality in intelligent building environments.

• The focus on green building materials is reshaping product development and procurement decisions across the Australian construction industry, with manufacturers producing plasterboards made from recycled content and low embodied carbon materials to address growing environmental consciousness among consumers, developers, and government procurement bodies committed to reducing the construction sector's greenhouse gas emissions.

• The retrofit and renovation segment is expanding across Australia's established urban centers - particularly in cities where high new-build costs are making refurbishment of existing buildings the more commercially viable path - creating sustained demand for specialized plasterboard solutions offering acoustic performance, thermal insulation, and compliance with modernized building codes.

• Market segmentation covers two forms (square-edge, tapered), six product types (standard, fire-resistant, thermal insulated, moisture-resistant, sound-resistant, impact-resistant), two end-use sectors (residential, non-residential), and five regional markets across Australia.

Key Trends Shaping the Australia Plasterboard Market:

• Focus on green building materials: Environmental regulation, green building rating systems such as Green Star, and growing consumer demand for climate-responsible construction are compelling plasterboard manufacturers to reformulate products using recycled gypsum content, low embodied carbon inputs, and production processes designed to minimize resource consumption and waste. This shift aligns with the broader decarbonization agenda in Australia's construction industry and positions eco-certified plasterboard products as increasingly preferred specifications for commercial and residential developments seeking sustainability credentials - a trend expected to intensify as environmental consciousness grows among both industry stakeholders and end consumers throughout the forecast period.

• Technological developments in plasterboard products: Manufacturers are investing significantly in research and development to produce plasterboards that deliver superior performance across fire resistance, sound insulation, moisture management, and thermal regulation - capabilities that are becoming standard specification requirements rather than premium options across both residential and commercial construction projects. Beyond passive performance, the integration of smart technologies including embedded sensors capable of measuring temperature, humidity, and environmental conditions within building cavities represents an emerging frontier in plasterboard innovation, expanding the product's functional value from a passive interior lining to an active component of intelligent, connected building systems.

• Impact of regulatory standards on plasterboard market: Australia's national and state-level building codes - including requirements under the National Construction Code governing fire resistance levels, acoustic performance between tenancies, and energy efficiency ratings for building envelopes - are directly shaping product development priorities and market demand patterns for plasterboard manufacturers. Companies that achieve compliance with and exceed these regulatory benchmarks are gaining meaningful competitive advantages in a construction industry where building certifiers, developers, and insurers increasingly specify advanced plasterboard products as a condition of project approval and operational safety compliance, creating a positive feedback loop between regulatory tightening and premium product adoption.

Market Growth Drivers:

Residential Housing Sector Expansion

Australia's residential housing market is generating robust and sustained demand for plasterboard as the country's most widely specified interior wall and ceiling material, with dwelling commencements rising 4.6% to 43,247 (seasonally adjusted) as of September 2024 and a growing pipeline of private sector house approvals signaling continued construction activity through the forecast period. Government programs including the HomeBuilder scheme have directly stimulated residential construction activity, translating into higher gypsum board consumption volumes across new-build projects in metropolitan and regional markets alike. Rapid urbanization in Sydney, Melbourne, and other major cities is simultaneously driving housing demand as population growth and internal migration concentrate residents in urban centers where plasterboard-intensive multi-unit residential and apartment development is the primary supply response. The expanding renovation and remodeling market is adding a parallel demand stream, as homeowners invest in interior upgrades that rely on plasterboard for wall reconfiguration, improved thermal performance, and contemporary interior finishes - reinforcing the material's versatile and enduring role across Australia's entire residential construction ecosystem.

Growing Commercial Infrastructure Development

The booming commercial construction sector across Australia's major cities is a significant and expanding demand driver for the plasterboard industry, as developers and institutional investors commit capital to office buildings, retail centers, healthcare facilities, education campuses, and hospitality venues that require plasterboard products delivering flexibility, durability, acoustic performance, and strict compliance with building safety codes. Brisbane, Perth, and Melbourne are experiencing particularly elevated commercial construction investment driven by economic growth, urban renewal activity, and infrastructure programs that are generating consistent demand for specialist plasterboard grades across large-scale commercial fitout and base build applications. The sector's emphasis on sustainable and green-rated buildings is simultaneously driving adoption of eco-certified plasterboard solutions, while commercial construction's inherent focus on streamlined project delivery timelines favors plasterboard due to its rapid installation capability - enabling projects to meet schedule and budget commitments more reliably than slower alternative interior systems, reinforcing plasterboard's structural position as the default specification in Australian commercial construction.

Impact of Natural Disasters on Building Codes and Material Demand

Australia's geographic exposure to a wide range of natural hazards - including devastating bushfires, tropical cyclones, severe flooding, and coastal storm events - has translated directly into stricter national and state building codes that mandate the use of fire-resistant, moisture-resistant, and structurally resilient construction materials across high-risk areas. These regulatory changes have created durable structural demand for specialized plasterboard products incorporating fire retardant chemistry, water-resistant core formulations, and enhanced impact resistance, as builders, developers, and homeowners in at-risk regions specify products that satisfy both updated code requirements and increasingly demanding insurance standards. Post-disaster rebuilding programs following major events generate discrete periods of concentrated demand growth, adding volume above the baseline new construction and renovation activity that sustains the broader market. This convergence of regulatory tightening, insurance-driven specification changes, and rebuilding demand is embedding a long-term structural preference for performance-grade plasterboard products throughout the Australian market, where safety, resilience, and durability are now evaluated alongside cost and aesthetic considerations in material selection decisions.

Browse the full report with TOC and list of figures: https://www.imarcgroup.com/australia-plasterboard-market

Porter's Five Forces Analysis - Australia Plasterboard Market

The Australia plasterboard market, valued at USD 913.0 Million in 2025 and projected to reach USD 1,833.9 Million by 2034 (CAGR 7.82%), reflects a structurally attractive and innovation-driven industry environment shaped by strong construction demand, escalating regulatory requirements, and growing sustainability imperatives.

Bargaining Power of Suppliers - Moderate

• Gypsum and paper - the two primary raw material inputs for plasterboard manufacturing - are subject to supply volatility, with Australia's partial dependence on imported gypsum exposing domestic manufacturers to international supply chain disruptions, shipping delays, and geopolitical uncertainties that have created periods of material scarcity and elevated input costs in recent years.

• Currency fluctuations directly affect the landed cost of imported gypsum and related raw materials, adding a layer of financial complexity to procurement planning for Australian plasterboard manufacturers who must balance input cost management with competitive product pricing in a construction industry sensitive to materials cost movements.

• Domestic suppliers of specialty additives used in fire-resistant, moisture-resistant, and acoustic plasterboard formulations hold moderate leverage given the technical specificity of these inputs, though the global availability of alternative chemical suppliers and the ongoing development of recycled material sources - including reclaimed gypsum from demolition waste - is gradually reducing dependence on any single supply channel.

Bargaining Power of Buyers - Moderate

• Large commercial builders, residential developers, and national fitout contractors hold meaningful bargaining leverage through the volume of plasterboard they procure across project pipelines, enabling them to negotiate pricing, delivery scheduling, and product specification commitments with manufacturers - particularly in a market where two dominant suppliers, CSR Gyprock and BGC/Etex, have historically concentrated competitive dynamics.

• Building product distributors and hardware retail chains serve as important intermediary buyers, and their ability to stock and promote competing plasterboard brands gives them leverage over manufacturers in terms of shelf placement, promotional support, and volume rebate negotiations - particularly as the renovation and DIY retail segment expands alongside the professional trade channel.

• End consumers - individual homeowners undertaking renovations - have comparatively lower individual bargaining power, though growing access to product specification information and sustainability labeling is enabling more informed purchasing decisions that reward manufacturers with strong eco-certification and performance credentials over purely price-competitive alternatives.

Threat of New Entrants - Low to Moderate

• The capital intensity of plasterboard manufacturing - requiring specialized board-forming lines, continuous drying kilns, and high-volume raw material supply chains - creates significant barriers to greenfield entry, with the investment required to establish a competitive-scale Australian manufacturing facility acting as a deterrent to all but well-capitalized international building materials groups.

• Etex's March 2024 acquisition of BGC's plasterboard and fiber cement divisions - including the gypsum wallboard manufacturing facility in Perth and nine warehouses across Australia and New Zealand - illustrates how the most commercially viable entry strategy for international manufacturers is acquisition of established domestic operations rather than greenfield construction, reflecting the strategic value embedded in existing manufacturing assets, distribution infrastructure, and customer relationships.

• Regulatory compliance requirements covering fire resistance testing, acoustic performance certification, and National Construction Code conformance add procedural entry barriers that require new market entrants to invest in product testing, accreditation, and relationship-building with building certifiers and specifiers before achieving meaningful market penetration.

Threat of Substitutes - Moderate

• Fiber cement boards, timber panels, and advanced composite panels represent the most commercially established substitutes for plasterboard in Australian construction, with these materials often preferred in applications demanding superior moisture resistance, termite protection, or structural load-bearing capability - particularly in coastal, tropical, and high-humidity environments where standard plasterboard performance may be insufficient.

• Modular and prefabricated construction systems, which are gaining traction in Australia's residential sector as a response to construction labor shortages and housing affordability pressure, can reduce per-project plasterboard consumption by pre-integrating interior finishing elements into factory-built modules - representing an indirect but structurally significant substitution risk as prefab's market share grows.

• Plasterboard manufacturers are actively mitigating substitution risk through product innovation, developing moisture-resistant, impact-resistant, and thermally enhanced board variants that match or exceed the performance of competing materials in previously challenging applications, while maintaining the installation speed, workability, and cost efficiency advantages that underpin plasterboard's dominant position across mainstream Australian construction.

Competitive Rivalry - Moderate to High

• The Australian plasterboard market is characterized by a concentrated competitive structure dominated by a small number of large manufacturers - principally CSR Gyprock and Etex (following its acquisition of BGC's plasterboard operations) - who compete across product range breadth, technical performance, distribution network reach, sustainability credentials, and builder loyalty programs rather than through destructive price competition.

• Etex's October 2023 agreement and March 2024 completion of its acquisition of BGC's gypsum and fiber cement divisions - encompassing manufacturing facilities and an extensive nine-warehouse distribution network across Australia and New Zealand - represents a significant competitive rebalancing that has intensified rivalry between the two primary market participants and raised the competitive bar for product innovation, supply reliability, and customer service.

• The growing emphasis on eco-certified, performance-grade, and technically advanced plasterboard products is driving healthy innovation-focused competition, with manufacturers investing in new product development, sustainability certification, and technical sales support as the primary strategic differentiators - a dynamic that benefits the construction industry through continuous product improvement while maintaining constructive competitive equilibrium.

Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Australia plasterboard market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on form, type, end-use sector, and region.

By Form:

• Square-Edge

• Tapered

By Type:

• Standard Plasterboard

• Fire-Resistant Plasterboard

• Thermal Insulated Plasterboard

• Moisture-Resistant Plasterboard

• Sound-Resistant Plasterboard

• Impact-Resistant Plasterboard

By End-Use Sector:

• Residential

• Non-Residential

By Region:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Key Players:

The Australia plasterboard market features a competitive landscape comprising large integrated building materials manufacturers, international groups with domestic manufacturing operations, and specialist plasterboard product companies. The market research report provides a comprehensive analysis of the competitive landscape including key player positioning, market structure, top winning strategies, competitive dashboards, and detailed company profiles. Some of the major participants include CSR Gyprock, Etex Group (including acquired BGC plasterboard and fiber cement operations), and other domestic and international operators competing across standard, specialty, and performance plasterboard segments throughout Australia.

Key Aspects Required for the Australia Plasterboard Market:

• Compliance with Australia's National Construction Code and relevant Australian Standards - including AS 1530.4 for fire resistance testing and AS/NZS 2588 for gypsum plasterboard specifications - is a non-negotiable market access requirement for plasterboard manufacturers, with product performance certification and third-party testing documentation essential for specification approval by building certifiers, developers, and government construction programs across all states and territories.

• Fire resistance performance is a foundational product requirement that is intensifying as Australia's building codes are progressively tightened in response to catastrophic fire events, with manufacturers required to invest in advanced fire-retardant core formulations, comprehensive testing programs, and clear product labeling that communicates fire resistance level (FRL) ratings to specifiers and builders working across residential, commercial, and public building categories.

• Moisture resistance capability across the full range of Australia's climatic zones - from the tropical humidity of northern Queensland and the Northern Territory to the salt-laden coastal environments of Sydney and Perth - is a growing specification requirement that demands manufacturers maintain dedicated moisture-resistant product lines capable of satisfying both building code minimums and the practical durability expectations of builders, owners, and building insurers operating in high-humidity or flood-prone locations.

• Supply chain reliability and national distribution infrastructure are critical operational requirements in Australia's geographically dispersed construction market, where builders working across metropolitan hubs and regional project sites require predictable product availability, consistent lead times, and technical support - making distribution network investment and warehouse coverage across all five regional markets a decisive competitive factor alongside product performance and pricing.

• Sustainability credentials - including recycled content percentages, embodied carbon declarations, Green Star compatibility, and responsible sourcing certification - are becoming increasingly important procurement considerations for commercial developers, government building programs, and large-scale residential developers pursuing green building ratings, creating a growing market requirement for manufacturers to invest in eco-friendly product reformulation, lifecycle assessment documentation, and transparent environmental product declarations.

• Technical sales capability and builder education programs are essential market requirements given the expanding range of specialist plasterboard types - fire-resistant, acoustic, moisture-resistant, thermal insulated, and impact-resistant - that require trained specifiers and installers to select and apply correctly, with manufacturers whose technical field teams can support builders through specification, application, and compliance verification gaining meaningful competitive advantage over competitors relying solely on product distribution.

Recent News and Developments:

Q1 2026: Altus Group's Australian construction material price outlook flagged plasterboard as a particular cost pressure point for the June quarter, driven by geopolitical disruption in the Middle East. As a high-volume, bulky, freight-sensitive product where logistics costs represent a meaningful share of landed price, the Hormuz-driven diesel surge is expected to flow into plasterboard delivery costs before appearing in spot pricing data, with further upward pressure anticipated in the June quarter as fuel surcharges already active in the market work through the supply chain. The price outlook adds to a challenging materials environment for builders operating under fixed-price contracts, particularly on large residential and commercial projects aligned with the government's housing delivery pipeline.

March 2026: The Building Products Industry Council publicly called for stricter anti-dumping measures targeting imported construction materials, with plasterboard among the product categories cited. The construction sector accounts for approximately 17.2% of all imports into Australia, and the industry body's intervention reflects growing concern among domestic manufacturers - led by CSR Gyprock (Saint-Gobain), Knauf, and Etex (Siniat) - that subsidised imported wallboard could undercut local production capacity at a moment when the housing accord is driving record near-term demand, creating a strategic tension between supply sufficiency and trade remedy enforcement.

March 2026: A public installation titled Shattered Topography: A Monument to Waste - developed by a UNSW Architecture team in collaboration with ScaleRule and Prevalent - was presented as part of Climate Action Week Sydney, drawing direct attention to plasterboard waste as a critical environmental challenge for the Australian construction industry. The installation invited architects, construction workers and policymakers to consider how legislative reform could combat the one million tonnes of waste generated each year by the local construction industry, accelerating a policy conversation around mandatory plasterboard recycling requirements and circular economy obligations for gypsum products that manufacturers and specifiers are increasingly being asked to respond to.

October 2025: Knauf Australia launched four new plasterboard products designed to simplify on-site installation and address updated Australian building compliance requirements, meeting the building compliance requirements for Australian construction projects and reinforcing the company's product development momentum following its rebranding from USG Boral to Knauf Gypsum Pty Ltd. The release aligns with rising builder demand for specification-ready systems as residential commencements recover and the National Housing Accord's 1.2 million homes target intensifies pressure on the construction supply chain.

Note: If you need specific information that is not currently within the scope of the report, we will provide it to you as a part of the customization.

Speak to an analyst for a customized sample report PDF: https://www.imarcgroup.com/request?type=report&id=37342&flag=C

Contact Us:

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No.: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Australia Plasterboard Market 2026 | Worth USD 1,833.9 Million by 2034 | CAGR of 7.82% here

News-ID: 4537775 • Views: …

More Releases from IMARC Group

Australia Off-Grid Solar Power Market 2026 | Expected to Grow to USD 143.7 Milli …

Australia Off-Grid Solar Power Market Overview:

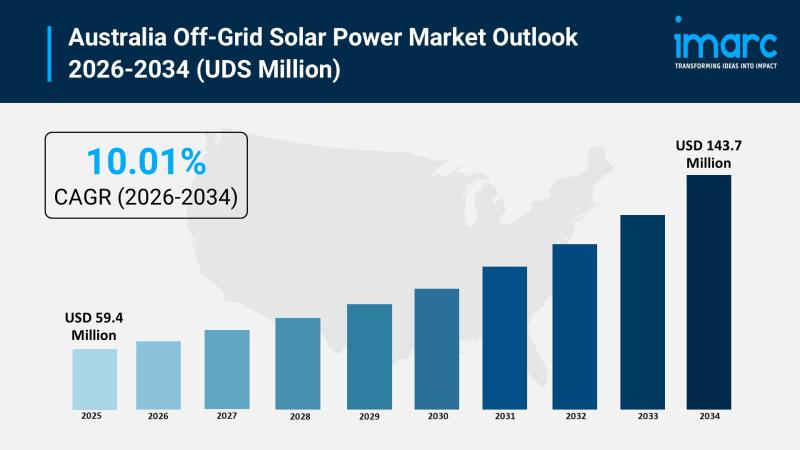

The Australia off-grid solar power market size reached USD 59.4 Million in 2025. Looking forward, the market is projected to reach USD 143.7 Million by 2034, exhibiting a growth rate (CAGR) of 10.01% during 2026-2034. Australia represents one of the most compelling off-grid solar power markets globally, driven by rising energy demands in remote mining and industrial operations, the country's vast geography that renders traditional…

Australia Fisheries and Aquaculture Market 2026 | Projected to Reach 453.0 Thous …

Australia Fisheries and Aquaculture Market Overview:

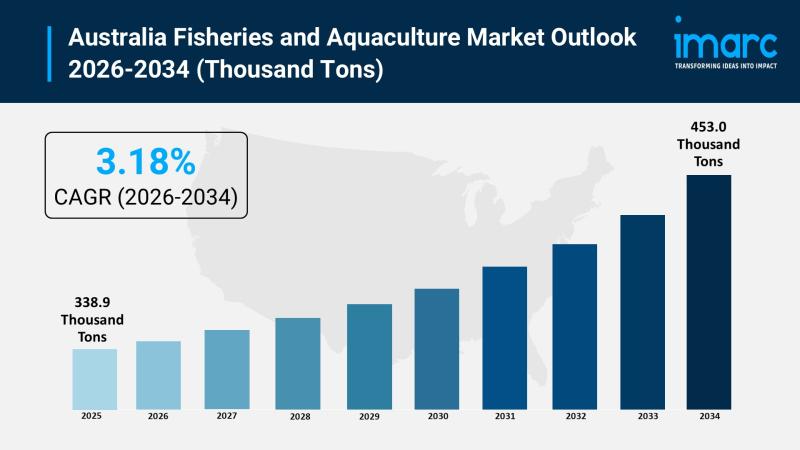

The Australia fisheries and aquaculture market size reached 338.9 Thousand Tons in 2025. Looking forward, the market is projected to reach 453.0 Thousand Tons by 2034, exhibiting a growth rate (CAGR) of 3.18% during 2026-2034. Australia represents one of the most significant fisheries and aquaculture markets in the Asia-Pacific region, driven by rising domestic and international demand for sustainable, high-quality seafood, expanding export opportunities, and…

Australia Black Cumin Seed Oil Market is Set for Strong Growth, To Reach USD 1,0 …

Market Overview

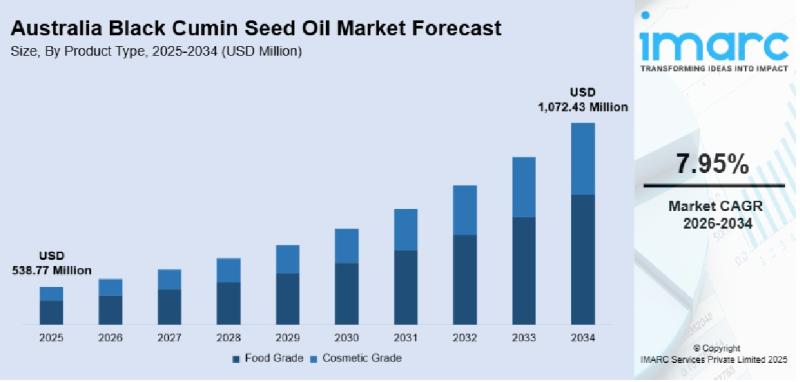

The Australia black cumin seed oil market is experiencing robust expansion, driven by escalating consumer preference for natural and plant-based wellness products. According to IMARC Group, the market size reached USD 538.77 Million in 2025 and is projected to reach USD 1,072.43 Million by 2034, exhibiting a compound annual growth rate (CAGR) of 7.95% from 2026 to 2034. Rising awareness about the therapeutic and cosmeceutical properties of Nigella sativa…

Australia Air Freight Market 2026 | Surge to USD 3.7 Billion by 2034 | CAGR 17.1 …

Australia Air Freight Market Overview:

The Australia air freight market size was valued at USD 2.0 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 3.7 Billion by 2034, exhibiting a growth rate (CAGR) of 7.12% during 2026-2034. Australia represents a strategically vital air freight market in the Asia-Pacific region, driven by booming e-commerce demand, robust international trade linkages, geographic isolation that elevates reliance on air transport,…

More Releases for Australia

Derila Memory foam pillow Australia: Honest Reviews About Derila Australia

Derila is one of the best memory foam pillows sold in Australia today.

Priced at around 30 dollars (USD), derila is currently the most reviewed and the cheapest memory pillow available in Australia.

What is Derila? Is Derila Pillow the best in Australia? Keep reading to discover everything worth knowing about Derila Australia.

OVERVIEW

Recently, Memory foam pillow has been trending and there is a lot of brands to choose from. Which one is…

CeraCare Australia - Where to Buy Legit CeraCare Supplement in Australia?

CeraCare Australia - Ceracare is a glucose support supplement that proposes to augment cardiovascular prosperity and to stay aware of perfect glucose assimilation in Australia. CeraCare supplement is conceptualized and executed by a threesome – Christine, Dr. Jihn and Michael. It is a natural supplement that helps one stay aware of ideal glucose levels, cardiovascular prosperity, and glucose assimilation.

Take Advantage of 80% Discount Offer in Australia >> https://boostsxproaustralia.com/ceracare-new

The indications…

Glucofort Australia - Where to Buy Legit Glucofort Supplement in Australia?

Glucofort Australia - Glucofort is an efficient, all-natural progressive glucose support supplement in Australia. This formula is made out of 12 key ingredients, 7 nutrients, and minerals, and a little of Vanadium. This supplement upholds regulated glucose levels and glucose digestion. Glucofort prides itself as the most inventive supplements available in Oceania, accentuating its solidarity, wellbeing, and quality.

Take Advantage of 75% Discount Offer in Australia >> https://boostsxproaustralia.com/glucofort-new

Rather than simply…

Australia Agriculture Market, Australia Agriculture Industry, Australia Agricult …

Australia Agriculture has been as vital within the development of Australia, because it was within the United States. Australia's ancient dominance in wheat and sheep continues into the 21st century. Recently Australian agriculture has become more and more diversified. The considerable expanses of productive land have helped Australia to become a number one world exporter of grains, meats, and wool. Each grains (predominantly wheat and barley) and wool markets round…

Australia Conveyor Maintenance Analysis by Top Companies Habasit Australia Pty l …

Global Australia Conveyor Maintenance Market and Competitive Analysis

Know your current market situation! Not only a vital element for brand new products but also for current products given the ever-changing market dynamics. The study allows marketers to remain involved with current consumer trends and segments where they'll face a rapid market share drop. Discover who you actually compete against within the marketplace, with Market Share Analysis know market position, to push…

Australia Conveyor Maintenance Market Analysis By Manufacturers Rema Tip Top Aus …

A conveyor system is a common piece of mechanical handling device that moves materials/objects from one location. A conveyor is often lifeline to a company’s ability to effectively move its products in a timely manner. While it is used constantly in a manufacturing plant, proper maintenance from trained technicians can extend the lifespan of conveyor. Furthermore, conveyor maintenance is essential as it may be subjected to different types of failures…