Press release

AI Data Center AEC Modules Market to Reach US$3.58 Billion by 2032 as GPU Clusters Drive High-Speed Interconnect Demand

QY Research can provide sample pages, the full table of contents, supplier coverage, pricing logic, market size, CAGR, etc

AI data centers are no longer constrained only by GPU availability. As clusters scale from thousands to tens of thousands of accelerators, short-reach interconnects are becoming a practical bottleneck in AI infrastructure design. Active Electrical Cable (AEC) modules address this bottleneck by combining copper cable assemblies with embedded signal-conditioning electronics such as retimers, redrivers and equalizers.

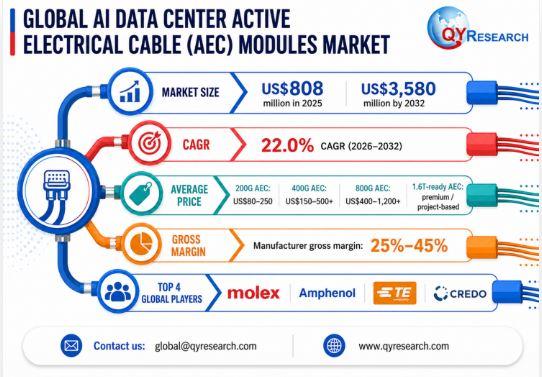

According to QY Research public-indexed information, the global AI Data Center Active Electrical Cable (AEC) Modules market was valued at approximately US$808 million in 2025 and is forecast to reach around US$3,580 million by 2032, implying an estimated CAGR of about 23.7% during 2026-2032. This growth profile places AEC modules among the faster-growing physical-layer markets inside the AI data center ecosystem.

The investment thesis is not that AEC modules will replace optics everywhere. It is that AI clusters create a large zone of short-reach, high-bandwidth links where passive copper may be insufficient and active optical cables may be more expensive or power-intensive than necessary. In that zone, AEC can offer a compelling mix of bandwidth, latency, power efficiency and cost per link.

Why This Market Deserves Attention Now

AEC modules sit at the intersection of three powerful themes: AI infrastructure growth, high-speed Ethernet migration and data center energy efficiency. The market is not driven by a single consumer cycle; it is tied to long-term cloud capex, GPU cluster architecture and the physical reality that every AI accelerator must move data quickly and reliably.

The market also benefits from a "middle-path" value proposition. Passive direct-attach copper cables are low-cost but lose signal integrity as data rates and reach increase. Optical links provide distance and bandwidth but add cost, power, thermal complexity and procurement exposure to optical module supply. AEC modules fill the gap between passive copper and optics, particularly in rack-level, row-level and short-reach AI fabric deployments.

For exporters and suppliers in Asia, the opportunity is attractive but increasingly selective. Buyers are not looking only for cheap cables. They need platform-qualified, thermally reliable, electrically stable and documentation-ready interconnect products that can pass validation with switches, network adapters, GPU servers and hyperscale operating requirements.

A. Consumption Market: AI Fabrics Are Creating a New Cable Value Layer

Consumption is driven by cloud service providers, AI infrastructure operators, GPU cluster builders, high-performance computing centers and colocation facilities supporting AI workloads. These buyers evaluate AEC modules not as commodity accessories, but as part of the AI data path. When a link fails or becomes unstable, the issue can affect GPU utilization, job completion and cluster availability.

Core Demand Drivers

• AI training clusters require low-latency, high-bandwidth connections between GPUs, switches, storage and accelerator trays.

• Inference data centers need scalable and cost-efficient interconnects as AI services move from model development into production.

• 400G and 800G adoption is expanding the market for signal-conditioned copper links, while early 1.6T planning supports longer-term value.

• Hyperscale operators are optimizing cost per bit and watt per bit across the full data center fabric, not only compute hardware.

• Cable congestion and thermal density make mechanical design, flexibility and airflow compatibility more important.

• Multi-source qualification is becoming a procurement priority as tariffs, chip supply constraints and regional sourcing requirements affect delivery risk.

Regional Consumption Dynamics

North America remains the most visible demand center because hyperscale cloud providers, AI model developers and GPU infrastructure companies are aggressively expanding AI clusters. China is also a major demand base as domestic AI infrastructure investment accelerates under export-control pressure. Taiwan and mainland China play important roles in server, cable and connector assembly, while Southeast Asia may gain from data center construction and electronics supply-chain diversification. Europe is a smaller but rising opportunity as sovereign AI infrastructure and energy-efficient cloud capacity expand.

B. Production and Supply Chain: Value Moves from Cable Assembly to Signal Integrity

The AEC value chain is more complex than traditional cable assembly. AEC modules combine high-speed copper twinax, precision connectors, active electronics, firmware, thermal design, validation testing and customer-specific qualification. The market therefore rewards suppliers that can move from low-cost assembly toward signal-integrity engineering and platform-level reliability.

Where Value Is Captured

• Signal-conditioning ICs: retimers, redrivers and equalizers determine reach, power consumption and link stability.

• Connector and cage quality: OSFP, QSFP and related form factors must support high-density deployment without mechanical or thermal failure.

• Copper cable and shielding: twinax quality, shielding design and insulation materials directly influence insertion loss and electromagnetic performance.

• Thermal and mechanical design: AI racks are hot, dense and difficult to service; cables must avoid airflow disruption and excessive heat load.

• Testing and qualification: bit-error-rate testing, interoperability validation, firmware traceability and failure analysis are increasingly purchase gates.

• Regional manufacturing options: customers increasingly value dual sourcing, local assembly and predictable logistics under tariff uncertainty.

For Asian suppliers, the production advantage is real: cable assembly ecosystems, connectors, PCB supply chains and electronics manufacturing capabilities are concentrated in Asia. The challenge is market access. Hyperscale customers require proof of compatibility, quality control, revision stability and long-term supply support. The commercial gap is often not factory capability, but qualification credibility.

Product Breakdown and Technical Structure

AEC Modules by Data Rate

• 100G/200G AEC Modules: used in legacy and transitional data center interconnects. Estimated B2B price range: US$40-150 per assembly, depending on length and connector format.

• 400G AEC Modules: mainstream for cloud and high-density server connectivity. Estimated price range: US$120-350 per assembly.

• 800G AEC Modules: key growth segment for next-generation AI fabrics and GPU scale-out. Estimated price range: US$250-700 per assembly, with premiums for longer reach and advanced retiming.

• 1.6T AEC Modules: emerging ultra-high-speed segment tied to future high-radix AI switches and accelerator interconnects. Estimated early-stage price range: US$600-1,500+ per assembly.

AEC Modules by Deployment Zone

• Short-reach below 2 meters: within-rack or adjacent equipment links; competes with passive DAC when signal integrity is marginal.

• Medium-reach 2-5 meters: rack row and GPU tray applications; a practical high-volume zone for AI data centers.

• Extended short-reach above 5 meters: selected deployments where optics are possible but copper economics, latency or power still favor AEC.

• Hyperscale AI AEC: strict validation, high reliability and customer-specific configurations; pricing reflects qualification depth and volume commitments.

Costs, Pricing and Manufacturer Gross Margin

Pricing is highly sensitive to data rate, reach, connector format, retimer/DSP content, thermal design, customer qualification, order volume and warranty/service requirements. AEC modules are usually purchased as part of broader data center networking procurement, so unit pricing must be interpreted alongside switch generation, server architecture, link length and total cost per port.

• By speed class: 400G modules typically sit in the US$120-350 range, while 800G products can reach US$250-700. Early 1.6T modules may command US$600-1,500+ until volumes scale.

• By cable length: short-reach products below 2 meters are lower priced; 2-5 meter and above-5-meter high-speed products carry premiums because signal conditioning and validation become harder.

• By supplier model: assembly-only OEM suppliers compete on cost, while vendors with signal-integrity design, active electronics, telemetry or platform qualification can defend higher pricing.

• By project structure: hyperscale AI deployments may negotiate aggressive volume pricing but still pay for guaranteed compatibility, stable revisions and fast replacement logistics.

Manufacturer gross margin varies by supplier positioning. Basic high-volume AEC assemblies may operate around 18%-30% gross margin, while higher-speed 800G/1.6T assemblies, proprietary DSP/retimer designs and hyperscale-qualified products can reach approximately 30%-50% depending on chip content, qualification cost, customer concentration and channel structure. The most attractive profit pool is not simple copper assembly; it is qualified high-speed interconnect engineering bundled with diagnostics, documentation and service reliability.

Top Producers and Market Participants

The competitive landscape includes high-speed cable specialists, connector companies, semiconductor interconnect suppliers, server ecosystem vendors and ODM/EMS partners.

Major participants commonly associated with AI data center AEC modules and high-speed interconnect ecosystems include:

• Credo Technology Group Holding Ltd (NASDAQ: CRDO, USA)

• Amphenol Corporation (NYSE: APH, USA)

• Molex LLC (Private, USA)

• TE Connectivity Ltd. (NYSE: TEL, Switzerland)

• Samtec, Inc. (Private, USA)

• Luxshare Precision Industry Co., Ltd. (SZSE: 002475, China)

• BizLink Holding Inc. (TWSE: 3665, Taiwan, China)

• Foxconn Industrial Internet Co., Ltd. (SSE: 601138, China)

• Broadcom Inc. (NASDAQ: AVGO, USA)

• Marvell Technology, Inc. (NASDAQ: MRVL, USA)

• NVIDIA Corporation (NASDAQ: NVDA, USA)

• Arista Networks, Inc. (NYSE: ANET, USA)

• Cisco Systems, Inc. (NASDAQ: CSCO, USA)

• Juniper Networks, Inc. (NYSE: JNPR, USA)

• Accton Technology Corporation (TWSE: 2345, Taiwan, China)

• Delta Electronics, Inc. (TWSE: 2308, Taiwan, China)

• Lumentum Holdings Inc. (NASDAQ: LITE, USA)

• Coherent Corp. (NYSE: COHR, USA)

• Leoni AG (Private, Germany)

• GigaLight (Private, China)

This is not only a cable-assembly race. Companies with signal-integrity expertise, high-speed silicon relationships, connector reliability and hyperscale qualification experience are better positioned than low-cost cable assemblers. The presence of semiconductor and networking companies shows that AEC modules are part of a broader AI networking platform competition.

Technology Roadmap and Innovation Vectors

Technology development is focused on higher data rates, lower power per bit, stronger diagnostics and closer integration with switch ASICs, NICs, DPUs and GPU platforms. AEC modules are gradually becoming smarter interconnect devices, not passive accessories.

• Migration from 400G to 800G and 1.6T: higher speeds require better signal conditioning, tighter materials control and more advanced testing.

• Lower-power retimers and DSPs: power efficiency is becoming a purchase criterion as data center electricity demand rises.

• Telemetry-enabled cables: link-health monitoring can support predictive maintenance and faster failure isolation.

• Improved shielding and mechanical design: dense AI racks need cables that are flexible, reliable and airflow-friendly.

• Co-design with switch and GPU ecosystems: platform validation will matter more as architectures fragment across Ethernet, InfiniBand and proprietary AI fabrics.

• Regional supply-chain qualification: customers may increasingly ask for alternative manufacturing sites and documented component traceability.

A wider data center energy context reinforces this trend. The International Energy Agency expects global data center electricity consumption to roughly double to around 945 TWh by 2030, while recent industry commentary indicates AI chip and infrastructure design are being forced to prioritize energy efficiency. For AEC suppliers, this means watt per link and cost per bit will become more important selling metrics.

Geopolitical Risks and Opportunities

AEC modules are small compared with GPUs and switches, but they are exposed to the same macro forces: semiconductor controls, U.S.-China technology competition, tariff uncertainty, regional sourcing requirements and data center power constraints.

• U.S.-China export controls: advanced chips, networking equipment and semiconductor-related components remain policy-sensitive. This can indirectly affect AEC demand, qualification and regional sourcing.

• Tariff risk: tariffs on electronics, cable assemblies, connectors or semiconductor components can change landed cost and encourage customers to diversify suppliers.

• Hyperscaler capex cycles: a small group of large buyers can drive large orders, but demand can fluctuate if AI cluster projects are delayed.

• Optics competition: active optical cables and optical transceivers may capture more links where reach requirements increase or optics pricing falls.

• Energy and grid constraints: data centers are under pressure to reduce power use. AEC suppliers must prove power efficiency versus optical alternatives in short-reach use cases.

• Southeast Asia localization: Malaysia, Thailand, Vietnam and Indonesia may benefit from data center expansion and supply-chain diversification, creating opportunities for assembly, testing and regional support.

For Asian exporters, the strongest opportunity is not to sell generic cables into the lowest-margin channel. It is to build export-ready, qualification-ready and platform-compatible AEC portfolios supported by English documentation, test reports, revision control, failure-analysis process and regional service partnerships.

Opportunities for Manufacturers, Exporters and Investors

• Move up from assembly to engineering: invest in signal-integrity design, simulation, high-speed testing and retimer/DSP integration capability.

• Target the 800G value window: 800G AEC is the most commercially attractive near-term segment because AI clusters are scaling now while 1.6T remains early.

• Prepare for 1.6T qualification: early supplier relationships, connector knowledge and thermal validation can create future pricing power.

• Build documentation as a product: datasheets, BER reports, thermal data, compatibility matrices and traceability reduce buyer risk.

• Use regional manufacturing as a hedge: ASEAN assembly or warehousing can support customers seeking lower tariff exposure and shorter lead times.

• Bundle with broader interconnect ecosystems: connectors, cable management, AEC modules, DAC, AOC and optics partnerships can improve account value.

• Monitor optics pricing: investors should track the copper-versus-optics boundary because it will define the long-term addressable market for AEC.

Key Market Risks

• Customer concentration: hyperscalers can create large opportunities but also strong pricing pressure and qualification dependency.

• Technology substitution: optical links, co-packaged optics and new fabric architectures may reduce AEC share in some deployment zones.

• Component constraints: retimer, connector and testing-equipment availability can affect capacity and delivery.

• Quality liability: unstable links can affect AI cluster performance, making failure costs much higher than the cable price.

• Margin compression: standard products may commoditize quickly if many assemblers enter without differentiation.

• Policy uncertainty: tariffs and export controls can alter sourcing decisions with limited notice.

Investment Implications and Strategic Outlook

The AI Data Center AEC Modules market offers a high-growth but selective opportunity. With QY Research public-indexed data indicating growth from US$808 million in 2025 to US$3,580 million by 2032, the category deserves monitoring by investors, exporters and suppliers across the AI infrastructure chain.

The strongest opportunities are likely to concentrate in 800G/1.6T AEC modules, telemetry-enabled active cables, hyperscale-qualified product lines and suppliers that combine active electronics with cable manufacturing discipline. Basic assembly will remain competitive, but the higher-margin market will favor companies that can demonstrate signal integrity, thermal reliability, platform compatibility and delivery resilience.

Strategically, AEC modules should be viewed as part of the physical operating system of AI data centers. GPUs create compute, switches create network fabric, but interconnects decide how efficiently data can move between expensive compute assets. Suppliers that help operators reduce link cost, power consumption and deployment risk can capture durable value even in a market where optics remain essential for longer reach.

The market's next phase will be defined by a practical question: how much of the AI cluster fabric can remain copper-based before optics become unavoidable? The answer will vary by link length, switch generation, power budget and data center architecture. That uncertainty does not weaken the market case; it makes AEC a category that investors and suppliers should actively monitor as AI data center networks evolve.

Report Coverage

This analysis is designed for manufacturers, suppliers, distributors, investors, data center operators, semiconductor companies, cloud service providers, procurement teams and strategy departments evaluating the global AI Data Center Active Electrical Cable (AEC) Modules market.

The full QY Research report covers market definition, market size, CAGR, gross margin indicators, product segmentation, key companies, regional outlook, application analysis, technology trends, pricing logic, procurement dynamics, risk factors and commercial considerations.

Related QY Research Reports

• Global AI Data Center Active Electrical Cable (AEC) Modules Market Research Report 2026

https://www.qyresearch.com/reports/5553058/ai-data-center-active-electrical-cable--aec--modules

• Global AI Data Center Active Electrical Cable (AEC) Modules Market Outlook, In-Depth Analysis & Forecast to 2032

https://www.qyresearch.com/reports/6229611/ai-data-center-active-electrical-cable--aec--modules

• Global AI Data Center Active Electrical Cable (AEC) Modules Sales Market Report, Competitive Analysis 2026-2032

https://www.qyresearch.com/reports/5553054/ai-data-center-active-electrical-cable--aec--modules

• Global AI Data Center 800G Active Electrical Cable (AEC) Market Research Report 2026

https://www.qyresearch.com/reports/5553064/ai-data-center-800g-active-electrical-cable--aec

Contact Information:

Tel: +1 626 2952 442 (US); +86-1082945717 (China); +84 865 216594 (Vietnam)

Email: global@qyresearch.com; tranlethanhhang@qyresearch.com

Website: www.qyresearch.com

Address: Room 2905, Vili International, 167 Linhe West Road, Tianhe District, Guangzhou, Guangdong Province, China

About QY Research

QY Research has established close partnerships with over 71,000 global leading players. With more than 20,000 industry experts worldwide, we maintain a strong global network to efficiently gather insights and raw data. Our 36-step verification system ensures the reliability and quality of our data. With over 2 million reports, we have become the world's largest market report vendor. Our global database spans more than 2,000 sources and covers data from most countries, including import and export details. We have partners in over 160 countries, providing comprehensive coverage of both sales and research networks. A 90% client return rate and long-term cooperation with key partners demonstrate the high level of service and quality QY Research delivery. More than 30 IPOs and over 5,000 global media outlets and major corporations have used our data, solidifying QY Research as a global leader in data supply. We are committed to delivering services that exceed both client and societal expectations.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release AI Data Center AEC Modules Market to Reach US$3.58 Billion by 2032 as GPU Clusters Drive High-Speed Interconnect Demand here

News-ID: 4531168 • Views: …

More Releases from QY Research

Global Clay Ventilation Block Market: Opportunities for Manufacturers, Exporters …

Executive Investment Snapshot

Clay ventilation blocks are not a new invention. They are one of the oldest ways to make walls breathe. What is changing is the commercial logic around them. As cities face hotter summers, higher cooling loads, tighter carbon expectations and stronger demand for distinctive architectural facades, the product is moving from a low-cost decorative masonry item toward a passive design component that can support shading, airflow, thermal comfort…

Green Building Materials Market Surges as Construction Shifts from ESG to Cost a …

Executive Summary: The Construction Industry's New Pressure Point

Construction is under pressure from several directions at once. Developers are facing higher material costs, rising energy expenses, stricter building codes, investor ESG requirements and growing concern about climate resilience. At the same time, building owners want healthier indoor environments, lower operating costs and more efficient envelopes that can reduce cooling and heating demand.

This is why green building materials are moving from a…

Indonesia Wrinkle Release Spray Market (2024 Onward): Economic and Regulatory Op …

Indonesia presents an attractive growth opportunity for wrinkle release spray manufacturers as the country's textile care, convenience household products, premium home care, and travel-friendly consumer goods markets continue to expand. Although wrinkle release spray remains a niche category compared with traditional fabric softeners or ironing aids, several structural trends including rising urbanization, growth of middle-income consumers, expansion of e-commerce, increasing business travel, and premiumization of household products to create favorable…

Premium Kitchen Appliances Drive the Next Expansion Cycle for Stainless Steel El …

The global Stainless Steel Automatic Electric Can Opener market is entering a non-linear value inflection where future value creation depends less on shipment expansion and increasingly on premium hardware integration, higher-quality stainless steel construction, ergonomic engineering, food-safe certifications, and automated manufacturing efficiency. Historically, manufacturers competed primarily through low-cost production and retail distribution. That competitive model is gradually giving way to capital-intensive manufacturing requiring precision motor assembly, long-life gearbox systems, improved…

More Releases for AEC

Cresire Provides BIM Solutions for the AEC Industry

Jaipur, India - The Architecture, Engineering, and Construction industry is under increasing pressure to deliver projects faster, more accurately, and with better coordination across all disciplines. Clients today expect reduced construction risks, predictable project timelines, improved collaboration, and minimal on-site surprises. However, many firms continue to struggle with design clashes, rework, fragmented communication, outdated workflows, delayed approvals, and inconsistent project documentation.

This is where CRESIRE is helping AEC professionals bridge the…

The AEC Associates Harnesses Autodesk AEC Collection to Enhance Innovation and E …

The AEC Associates, a leading provider of design documentation and BIM solutions, utilizes the Autodesk AEC Collection to enhance efficiency, accuracy, and collaboration across the Architecture, Engineering, and Construction (AEC) industry.

Noida, Uttar Pradesh Mar 4, 2025 - The AEC Associates, a leading provider of design documentation and BIM solutions, has been utilizing the Autodesk AEC Collection to enhance efficiency, accuracy, and project collaboration across the Architecture, Engineering, and Construction (AEC)…

Top BIM Software Tools for AEC Professionals: A Complete Guide

The architectural, engineering, and construction (AEC) industry has long struggled with high prices, sluggish delivery, and a lack of communication. This is mostly due to a lack of effective coordination among project stakeholders, who include architects, contractors, engineers, owners, designers, and facilities managers. The software market is saturated with many sorts of software. AEC professionals may struggle to choose the best BIM solution for their building projects. I've put together…

Architectural 3D Visualization: Revolutionizing the AEC Industry

One of the most inventive technologies in the contemporary world is Architectural 3D visualization and it is gaining popularity rapidly among professionals in the architecture, engineering and construction (AEC) industry. It helps create a comprehensive representation of the building design, internal spaces or a scheme of urban development through numerous graphic images. Such images present the major attributes of the object and serve as a good conception of the development…

Architecture, Engineering, and Construction (AEC) Market Overview - 2031

Market Dynamics:

Growing Urbanization Globally

Rapid urbanization worldwide necessitates significant infrastructure development to support expanding urban populations. Investments in railroads, airports, bridges, highways, and utilities drive the demand for AEC services, enabling planning, designing, and construction of essential infrastructure projects. With urban areas projected to accommodate over 5 billion people by 2031, sustainable growth initiatives become imperative.

Technological Advancements

Advancements in Building Information Modeling (BIM), Virtual Design and Construction (VDC), Augmented Reality (AR), Virtual…

Revolutionizing AEC Industry with Custom Engineering Application Development

Introduction

In the rapidly evolving Architecture, Engineering, and Construction (AEC) industry, technological advancements play a pivotal role in enhancing efficiency, collaboration, and innovation. One such transformative force is the development of custom engineering applications tailored to the unique needs of AEC professionals. This blog post explores the profound impact of custom engineering application development and delves into the exemplary contributions of ProtoTech Solutions in this domain.

The AEC industry has undergone a…