Press release

Automotive Axle and Propeller Shaft Market - Industry Outlook and Forecast with CAGR 3.52% (2026-2032)

Automotive Axle and Propeller Shaft Market

Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs): https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-automotive-axle-propeller-shaft-market

Market Size & Forecast

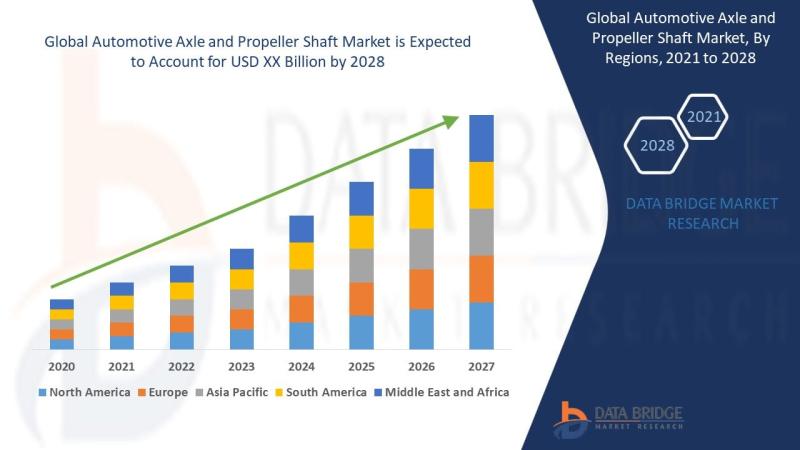

2025 Market Size: USD 25.80 Billion

2026 Projected Market Size: USD 26.71 Billion

2032 Projected Market Size: USD 32.87 Billion

CAGR (2026-2032): 3.52%

Largest Region: Asia-Pacific

Fastest Growing Region: Asia-Pacific

Key Market Report Takeaways

Asia-Pacific accounted for the largest market share of approximately 43% in 2025 due to strong automotive manufacturing capacity in China, India, Japan, and South Korea.

Asia-Pacific is projected to remain the fastest-growing region owing to increasing passenger vehicle production and rising investments in EV manufacturing infrastructure.

Front axle systems represented the largest product segment due to their extensive integration across passenger and commercial vehicles.

Passenger vehicles remained the dominant application segment, supported by high global production volumes and increasing consumer vehicle ownership.

OEMs accounted for the leading end-use segment driven by long-term supply contracts and continuous demand from automotive assembly lines.

Lightweight and high-strength steel propeller shafts are witnessing increased adoption to improve fuel efficiency and reduce drivetrain weight.

Growing electrification of vehicles is accelerating innovation in e-axles and integrated drivetrain systems globally.

Market Trends & Highlights

Asia-Pacific dominates the global market due to large-scale automobile production, cost-efficient manufacturing ecosystems, and strong supply chain networks across China, Japan, and India.

Europe is witnessing steady growth supported by stringent emission regulations and increasing adoption of lightweight automotive components.

Passenger vehicle applications continue to dominate market demand because of rising urbanization, increasing disposable income, and higher global vehicle sales volumes.

Key market growth drivers include rising commercial vehicle demand, expansion of electric mobility, and continuous advancements in drivetrain efficiency technologies.

Emerging technologies such as e-axles, carbon-fiber reinforced shafts, and smart drivetrain monitoring systems are reshaping product innovation.

Strategic partnerships between OEMs and component manufacturers, along with investments in EV drivetrain technologies, are intensifying global competition.

View Full Report: https://www.databridgemarketresearch.com/reports/global-automotive-axle-propeller-shaft-market

Market Dynamics

Market Drivers

Rising Global Vehicle Production

Increasing production of passenger and commercial vehicles across Asia-Pacific and North America continues to drive demand for axle and propeller shaft systems. Countries such as China, India, and the U.S. are witnessing sustained vehicle manufacturing expansion supported by urbanization and industrial development. Growing automotive exports and rising domestic vehicle ownership are strengthening OEM procurement activities. Commercial fleet modernization further contributes to demand for durable drivetrain components.

Growing Adoption of Electric and Hybrid Vehicles

The transition toward electric mobility is accelerating demand for advanced e-axles and lightweight propeller shaft systems. EV manufacturers are focusing on integrated drivetrain technologies to improve energy efficiency and vehicle performance. Europe and China remain major contributors due to aggressive emission reduction policies and EV incentives. Automotive suppliers are increasing investments in next-generation axle architectures specifically designed for battery-electric platforms.

Technological Advancements in Lightweight Materials

Manufacturers are increasingly adopting aluminum alloys, composite materials, and high-strength steel to reduce drivetrain weight and improve fuel economy. Lightweight axle and shaft systems enhance vehicle efficiency and help automakers comply with global emission regulations. Advanced manufacturing technologies such as precision forging and robotic assembly are improving product durability and performance. Demand is particularly strong in premium passenger vehicles and electric SUVs.

Expansion of Commercial Vehicle Fleets

Global logistics expansion, infrastructure projects, and e-commerce growth are increasing demand for medium and heavy-duty commercial vehicles. This trend directly supports higher adoption of robust axle assemblies and propeller shafts capable of handling greater torque loads. Emerging economies in Asia-Pacific and Latin America are witnessing significant freight transportation expansion. Fleet operators are prioritizing reliable drivetrain systems to reduce operational downtime and maintenance costs.

Increasing OEM Investments in Drivetrain Innovation

Automotive OEMs are investing heavily in drivetrain optimization to improve vehicle efficiency, durability, and driving performance. Collaborations between OEMs and component suppliers are accelerating development of integrated axle systems and modular driveline solutions. North America and Europe are leading innovation in electronically controlled axle technologies. Continuous R&D spending supports product differentiation and long-term supplier contracts.

Market Restraints

Volatility in Raw Material Prices

Fluctuations in steel, aluminum, and composite material prices significantly impact manufacturing costs for axle and propeller shaft producers. Global supply chain disruptions and geopolitical uncertainties contribute to procurement instability. Manufacturers operating in cost-sensitive regions face pressure on profit margins due to inconsistent raw material pricing. Long-term pricing volatility also complicates strategic sourcing and production planning.

High Development and Manufacturing Costs

Advanced axle systems designed for EVs and high-performance vehicles require substantial investments in R&D, precision engineering, and automated manufacturing infrastructure. Smaller manufacturers often face financial constraints in adopting advanced production technologies. High tooling and testing expenses limit market entry for regional suppliers. Cost pressures are particularly significant in emerging markets with price-sensitive automotive sectors.

Complex Regulatory Compliance Requirements

Stringent emission regulations and automotive safety standards increase product development complexity. Manufacturers must continuously redesign components to comply with evolving efficiency and durability requirements across multiple regions. Europe and North America maintain highly regulated automotive compliance frameworks. Frequent regulatory changes increase testing, certification, and operational costs for global suppliers.

Supply Chain Disruptions and Component Shortages

Global automotive supply chains remain vulnerable to transportation bottlenecks, semiconductor shortages, and geopolitical tensions. Delays in sourcing critical raw materials and drivetrain components affect production timelines and OEM deliveries. Asia-Pacific manufacturing hubs are particularly exposed to export restrictions and logistics disruptions. Supply chain instability impacts inventory management and operational efficiency.

Intense Pricing Competition Among Suppliers

The market remains highly competitive with significant pricing pressure from global and regional component manufacturers. OEMs continuously negotiate lower procurement costs to maintain vehicle affordability and profitability. Smaller suppliers often face margin compression due to aggressive bidding practices. Price-based competition limits profitability despite growing demand volumes.

Market Opportunities

Expansion of Electric Drivetrain Technologies

Rapid EV adoption creates substantial opportunities for manufacturers developing e-axles and integrated propulsion systems. Electrified drivetrains require specialized lightweight components optimized for battery-powered vehicles. Government incentives supporting EV manufacturing in China, Europe, and North America are accelerating investment opportunities. Companies focusing on high-efficiency drivetrain systems are expected to gain long-term revenue advantages.

Growth in Emerging Automotive Markets

Developing economies such as India, Brazil, Indonesia, and Vietnam present significant growth potential due to rising vehicle ownership and expanding industrialization. Government infrastructure development and increasing middle-class populations are driving automotive demand. Local manufacturing initiatives are encouraging international suppliers to establish regional production facilities. These markets offer substantial opportunities for cost-effective drivetrain component suppliers.

Increasing Adoption of Advanced Materials

The growing shift toward lightweight and corrosion-resistant materials opens new opportunities for innovation in propeller shaft and axle manufacturing. Carbon-fiber composites and aluminum alloys are gaining traction in premium and electric vehicles. Manufacturers investing in advanced material technologies can enhance fuel efficiency and vehicle performance. This trend is expected to support premium product pricing and technological differentiation.

Aftermarket Expansion and Replacement Demand

The global vehicle parc continues to grow, creating strong opportunities in the automotive aftermarket segment. Aging commercial fleets and rising maintenance requirements increase replacement demand for axle and shaft assemblies. Developing regions with poor road infrastructure generate higher component wear rates. Aftermarket suppliers can benefit from expanding service networks and product customization strategies.

Strategic Collaborations and Localization Initiatives

Automotive suppliers are increasingly entering joint ventures and regional manufacturing partnerships to strengthen supply chain resilience. Localization strategies reduce dependency on imports and improve operational efficiency. Governments in Asia-Pacific and the Middle East are encouraging domestic automotive component manufacturing through incentives and industrial policies. Strategic collaborations support technology transfer and regional market expansion.

Market Challenges

Rapid Technological Transition Toward Electrification

The automotive industry's transition from internal combustion engines to electric drivetrains creates significant adaptation challenges for traditional axle and propeller shaft manufacturers. Companies must redesign existing product portfolios to align with EV architectures. Legacy production infrastructure may become obsolete without significant modernization investments. Transition-related uncertainty impacts long-term capital allocation strategies.

Managing Global Supply Chain Complexity

Manufacturers face operational challenges related to multi-regional sourcing, logistics management, and inventory optimization. Dependence on international suppliers increases vulnerability to geopolitical tensions and transportation disruptions. Semiconductor shortages and shipping delays continue to impact automotive production schedules globally. Maintaining supply chain continuity remains a critical operational concern.

Balancing Cost Efficiency with Product Innovation

OEMs demand advanced lightweight and high-performance drivetrain components while simultaneously pressuring suppliers to reduce costs. Achieving profitability while investing in R&D and manufacturing modernization remains challenging for mid-sized suppliers. Innovation-driven competition increases operational expenditure across the industry. Manufacturers must optimize production efficiency without compromising quality standards.

Compliance with Evolving Environmental Standards

Governments worldwide are implementing stricter carbon emission and fuel efficiency regulations, requiring continuous product redesign and compliance testing. Manufacturers operating across multiple regions face complex regulatory harmonization challenges. Compliance-related investments increase operational costs and extend product development cycles. Europe represents one of the most demanding regulatory markets globally.

Market Fragmentation and Competitive Intensity

The presence of numerous global and regional manufacturers intensifies market competition and pricing pressure. Established players compete aggressively through product differentiation, geographic expansion, and strategic partnerships. Smaller companies often struggle to maintain market share against technologically advanced multinational suppliers. Market fragmentation limits pricing flexibility and profitability across the value chain.

Market Segmentation & Analysis

By Product Type

Front Axle

Front axles represent the largest segment due to their widespread integration across passenger cars, SUVs, and light commercial vehicles. These components support steering functionality and vehicle load distribution, making them critical for drivetrain performance. The segment accounted for the highest revenue share in 2025 owing to increasing vehicle production volumes globally. Growth is driven by rising demand for durable and lightweight axle systems in modern automotive platforms. CAGR for the segment is estimated at approximately 3.4% through 2032.

Rear Axle

Rear axles are extensively used in commercial vehicles and performance-oriented passenger vehicles requiring enhanced torque handling capabilities. Demand is increasing due to expanding logistics and transportation industries worldwide. Heavy-duty trucks and buses continue to generate strong revenue contribution for this segment. Manufacturers are investing in high-strength rear axle systems to improve durability and fuel efficiency. The segment is expected to witness steady growth during the forecast period.

Propeller Shaft

Propeller shafts are critical drivetrain components that transmit torque from transmission systems to vehicle axles. This segment is witnessing increasing adoption of lightweight materials including aluminum and composites. Growing EV integration and drivetrain optimization trends are accelerating innovation within the segment. Commercial vehicles remain major end-users due to higher torque transmission requirements. The segment is projected to register a CAGR above the overall market average.

By Vehicle Type

Passenger Vehicles

Passenger vehicles accounted for the dominant market share in 2025 due to high global production and increasing urban mobility demand. Rising disposable income, consumer preference for personal transportation, and SUV popularity continue to support segment expansion. OEMs are integrating advanced lightweight axle systems to improve fuel efficiency and vehicle handling. Asia-Pacific remains the primary production hub for passenger vehicles globally. The segment is expected to maintain leadership throughout the forecast period.

Commercial Vehicles

Commercial vehicles represent a significant market segment driven by rapid growth in logistics, e-commerce, and infrastructure development activities. Heavy-duty trucks require high-performance axle systems capable of handling large payload capacities and long-distance operations. Fleet modernization initiatives in North America and Europe are contributing to replacement demand. Increasing freight transportation activity in emerging economies is supporting long-term segment growth. CAGR for the segment is projected to exceed 3.8% through 2032.

By Material Type

Steel

Steel remains the dominant material segment due to its durability, strength, and cost-effectiveness. High-strength steel axle and shaft systems are widely used across commercial and passenger vehicles. Manufacturers continue to adopt advanced steel processing technologies to improve performance and reduce component weight. The segment maintains strong demand due to extensive compatibility with existing automotive manufacturing processes.

Aluminum and Composite Materials

Aluminum and composite materials are emerging as the fastest-growing material segment due to increasing demand for lightweight drivetrain systems. These materials improve fuel efficiency and vehicle performance while supporting emission reduction goals. Adoption is particularly strong in EVs and premium automotive segments. Continuous advancements in composite manufacturing technologies are expected to accelerate market penetration during the forecast period.

By Sales Channel

OEM

OEMs account for the largest market share due to long-term supply agreements and continuous automotive production demand. Component suppliers prioritize strategic partnerships with major automakers to ensure stable revenue generation. OEM demand is particularly strong in Asia-Pacific and Europe where automotive manufacturing capacity remains high. Technological collaboration between suppliers and OEMs continues to accelerate innovation.

Aftermarket

The aftermarket segment is growing steadily due to rising vehicle parc and increasing replacement requirements. Aging commercial vehicles and harsh operating environments contribute to higher maintenance demand. Independent repair networks and regional distributors are expanding aftermarket accessibility globally. The segment offers significant growth opportunities in emerging markets with expanding transportation sectors.

Regional Analysis

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America represents a significant share of the global automotive axle and propeller shaft market due to advanced automotive manufacturing infrastructure and strong commercial vehicle demand. The U.S. remains the primary contributor supported by major OEM presence and increasing investments in EV production. Technological innovation in lightweight drivetrain systems continues to drive regional competitiveness. Strong regulatory frameworks promoting fuel efficiency are encouraging adoption of advanced axle technologies. Mexico also contributes through expanding automotive manufacturing operations and export activities.

Europe

Europe is a mature and steadily growing market supported by strong automotive engineering capabilities and stringent environmental regulations. Germany leads regional demand due to its extensive premium vehicle manufacturing ecosystem. The U.K. and France continue to invest in EV drivetrain technologies and sustainable automotive solutions. Regulatory pressure regarding emission reduction is accelerating lightweight component adoption. Continuous R&D investment and collaboration between OEMs and suppliers support long-term market stability.

Asia Pacific

Asia Pacific dominates the global market and is projected to remain the fastest-growing region during the forecast period. China, India, Japan, and South Korea collectively account for substantial automotive production capacity and component manufacturing activity. Rapid industrialization, rising disposable income, and expanding vehicle ownership continue to drive demand growth. Government incentives supporting EV adoption and domestic automotive manufacturing are strengthening regional expansion. The region also benefits from cost-efficient labor availability and extensive supplier networks.

Latin America

Latin America is an emerging market characterized by gradual industrial development and expanding automotive production activities. Brazil and Mexico remain the key contributors due to their established automotive assembly industries. Infrastructure improvements and increasing freight transportation demand are supporting commercial vehicle sales. Economic volatility and limited technological penetration continue to restrict faster market expansion. However, growing localization initiatives are expected to improve long-term supply chain resilience.

Middle East & Africa

The Middle East & Africa market is witnessing gradual growth driven by infrastructure investments and expanding transportation sectors. Gulf countries are increasing investments in logistics and industrial diversification projects, supporting commercial vehicle demand. South Africa remains a major automotive manufacturing hub within the region. Limited local manufacturing capabilities and infrastructure gaps continue to challenge market growth. However, government-backed industrial initiatives and increasing private sector participation are creating new opportunities for component suppliers.

Key Insights

Largest Region: Asia-Pacific

Fastest Growing Region: Asia-Pacific

Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs): https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-automotive-axle-propeller-shaft-market

Competitive Landscape

Market Structure Overview

The global automotive axle and propeller shaft market is moderately consolidated with the presence of established multinational manufacturers, regional suppliers, and emerging drivetrain technology providers. Competition is heavily influenced by product innovation, manufacturing efficiency, and long-term OEM relationships. Leading companies focus on lightweight materials, electrified drivetrain systems, and advanced axle technologies to strengthen competitive positioning. Competitive landscape analysis helps assess market positioning, operational strengths, technological capabilities, and strategic direction of key participants.

Key Industry Players

Major market participants maintain strong global manufacturing networks and diversified drivetrain product portfolios. Leading companies compete through technological innovation, strategic partnerships, and investments in EV-focused drivetrain solutions. Global players continue to expand regional production capabilities to improve supply chain efficiency and customer responsiveness. Several manufacturers are prioritizing lightweight and high-performance axle technologies to align with evolving automotive industry requirements.

List of Key Industry Players

American Axle & Manufacturing Holdings, Inc.

Dana Incorporated

GKN Automotive Limited

Meritor, Inc.

Hyundai Wia Corporation

Nexteer Automotive Group Limited

NTN Corporation

Showa Corporation

JTEKT Corporation

ZF Friedrichshafen AG

Competitive Strategies

Companies are actively investing in lightweight material technologies, integrated e-axle systems, and automated manufacturing solutions to strengthen market differentiation. Strategic partnerships between automotive OEMs and component suppliers are increasing to accelerate EV drivetrain development. Mergers and acquisitions remain a key strategy for expanding product portfolios and geographic presence. Manufacturers are also strengthening regional distribution networks and localized production facilities to improve operational resilience and reduce supply chain risks. Innovation-driven competition continues to shape long-term market positioning.

Emerging Players & Market Dynamics

Emerging manufacturers and niche technology providers are increasing competition by offering cost-effective and specialized drivetrain solutions. Startups focusing on electric mobility and smart drivetrain systems are disrupting traditional market structures. Increased venture capital investments and government support for EV ecosystems are encouraging market entry by innovative companies. Growing digitalization and advanced manufacturing adoption are expected to reshape competitive dynamics over the forecast period.

Latest Developments

January 2025 - Dana Incorporated: Announced expansion of its electrified drivetrain manufacturing capabilities in North America to support growing EV demand. The investment strengthens the company's position in integrated e-axle technologies and enhances regional supply chain efficiency.

October 2024 - ZF Friedrichshafen AG: Introduced next-generation lightweight commercial vehicle axle systems designed to improve fuel efficiency and reduce carbon emissions. The launch supports increasing regulatory compliance requirements in Europe and North America.

July 2024 - American Axle & Manufacturing Holdings, Inc.: Expanded its electric drive unit portfolio through strategic collaboration with EV manufacturers. The initiative aims to accelerate innovation in integrated propulsion technologies.

March 2024 - GKN Automotive: Announced increased investments in advanced eDrive systems and sustainable manufacturing processes across Europe and Asia-Pacific. The expansion strengthens the company's EV drivetrain production capacity.

November 2023 - Meritor, Inc.: Enhanced heavy-duty axle manufacturing capabilities following rising global demand for commercial vehicle components. The development supports logistics and freight transportation growth worldwide.

August 2023 - Hyundai Wia Corporation: Launched advanced rear-drive axle systems optimized for electric SUVs and premium vehicles. The product innovation improves vehicle efficiency and driving performance.

May 2023 - NTN Corporation: Expanded R&D investments focused on lightweight automotive drivetrain technologies and precision engineering solutions. The initiative aims to improve product durability and operational efficiency.

February 2023 - JTEKT Corporation: Strengthened strategic partnerships with global OEMs to accelerate development of high-performance axle systems for next-generation electric vehicles. The collaboration enhances technological competitiveness in the global market.

Check out more related studies published by Data Bridge Market Research:

https://www.databridgemarketresearch.com/reports/asia-pacific-electric-vehicle-charging-stations-market

https://www.databridgemarketresearch.com/reports/india-ev-charging-stations-market

https://www.databridgemarketresearch.com/reports/north-america-electric-vehicle-charging-stations-market

https://www.databridgemarketresearch.com/reports/global-golf-cart-market

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com

Data Bridge Market Research is dedicated to deliver market intelligence with highest quality and accuracy. Through meticulous analysis and research, we strive to provide our clients with reliable and precise insights into various industries and markets.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Automotive Axle and Propeller Shaft Market - Industry Outlook and Forecast with CAGR 3.52% (2026-2032) here

News-ID: 4530382 • Views: …

More Releases from Data Bridge Market Research

Artificial Grass Market Size, Share & Industry Trends Analysis Report - Growth F …

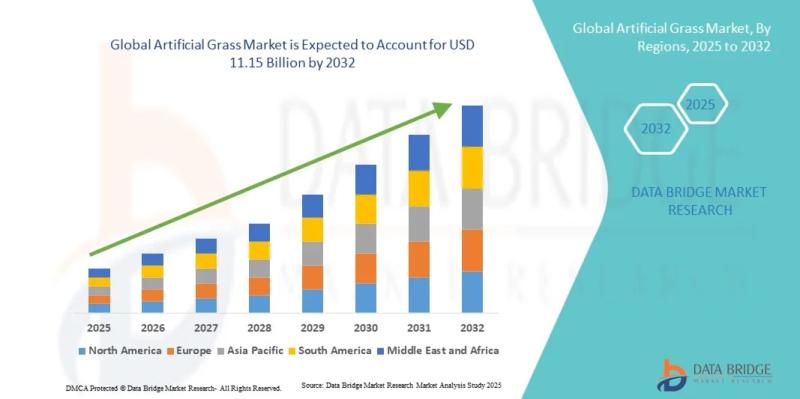

As per Data Bridge Market Research analysis, the Artificial Grass Market was estimated at USD 6.66 billion in 2025. The market is expected to grow from USD 7.17 billion in 2026 to USD 11.15 billion in 2032, at a CAGR of 7.62% during the forecast period with driven by the rising demand for low-maintenance landscaping solutions, increasing adoption in sports infrastructure, growing urbanization, and advancements in recyclable synthetic turf technologies.

Get…

Melamine-Based Products Market Trends, Share, and Forecast Report with 3.49% CAG …

As per Data Bridge Market Research analysis, the Melamine Market was estimated at USD 9.24 billion in 2025. The market is expected to grow from USD 9.56 billion in 2026 to USD 11.75 billion in 2032, at a CAGR of 3.49% during the forecast period with driven by the rising demand for laminates, wood adhesives, construction materials, and flame-retardant applications across residential, commercial, and industrial sectors.

Get the full PDF sample…

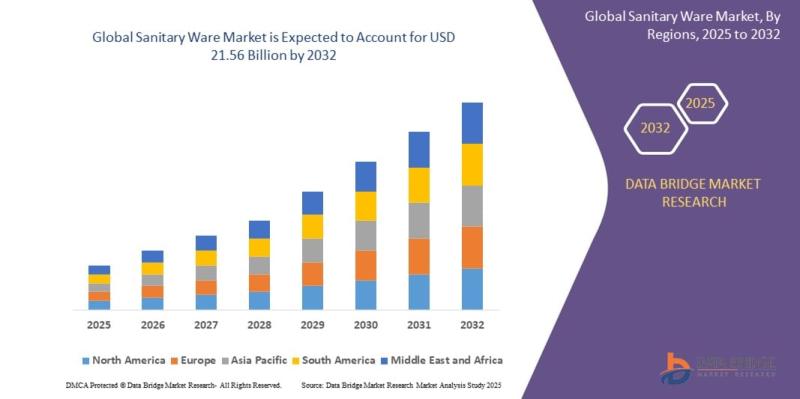

Sanitary Ware Industry Outlook 2026-2032 Driven by 5.85% CAGR Growth

As per Data Bridge Market Research analysis, the Sanitary Ware Market was estimated at USD 14.48 billion in 2025. The market is expected to grow from USD 15.32 billion in 2026 to USD 21.56 billion in 2032, at a CAGR of 5.85% during the forecast period with driven by the rising demand for modern bathroom infrastructure, smart sanitation solutions, rapid urbanization, and increasing investments in residential and commercial construction activities.

Get…

Lubricants Market to Reach USD 215.19 Billion by 2032 Growing at 5.2% CAGR

As per Data Bridge Market Research analysis, the Lubricants Market was estimated at USD 152.56 Billion in 2025. The market is expected to grow from USD 160.49 Billion in 2026 to USD 215.19 Billion in 2032, at a CAGR of 5.2% during the forecast period with driven by the rising demand for automotive lubricants, increasing industrial automation, expanding manufacturing activities, and growing investments in high-performance synthetic lubricant technologies.

Get the full…

More Releases for OEM

OEM Partnership Guide: Working with a Touch-free Automatic Kitchen Garbage Can O …

With increasing global demand for smart home solutions, Sinoware International Ltd, a top provider in household products industry, is pleased to unveil expanded OEM partnership initiatives.

Sinoware has established itself in Jiangmen--China's premier stainless steel industry zone--as an indispensable touch-free automatic kitchen garbage can OEM manufacturer for global brands seeking to incorporate high-tech sanitation solutions into their portfolios.

By combining their decades-old tradition of metal craftsmanship with cutting-edge infrared and…

Revolutionizing OEM Coatings With Sustainable Solutions Trend: A Crucial Influen …

Which drivers are expected to have the greatest impact on the over the oem coatings market's growth?

The surge in requirements from final consumer industries is forecasted to boost the expansion of the OEM coatings market. These coatings, referred to as OEM, are utilized during the integration of other firms' products into the substrate process or application. They prove to be beneficial for a variety of end-user sectors, including automotive and…

OEM Technology Partnerships Launches Brokerage Specializing in 100+ OEM Technolo …

San Francisco, California, USA - February 13, 2025 - OEM Technology Partnerships is thrilled to announce the launch of its specialized brokerage focused on connecting businesses with a comprehensive portfolio of over 100 Original Equipment Manufacturer (OEM) technologies. This new venture is poised to revolutionize how companies access and implement cutting-edge solutions across diverse industries.

Leveraging deep industry expertise and a vast network of OEM partners, OEM Technology Partnerships offers a…

OEM or ODM Watches? What's the Difference?

When searching for a watch manufacturer for your store or watch brand, you may come across the terms OEM and ODM. But do you truly understand the difference between them? In this article, we will delve into the distinctions between OEM and ODM watches to help you better grasp and choose the manufacturing service that suits your needs.

Image: https://www.naviforce.com/uploads/15a6ba3911.png

What's OEM / ODM Watches [https://www.naviforce.com/products/]

OEM (Original Equipment Manufacturer) watches are produced…

OEM Partnership with Extreme Networks

ComputerVault announces an OEM partnership with Extreme Networks and has certified its switches for use with ComputerVault enterprise software to deliver virtual desktop infrastructure (VDI).

Extreme Networks industry leading switches deliver ComputerVault Virtual Desktops at faster than PC speeds in the LAN and WAN.

“ComputerVault is very excited to work with Extreme Networks. Not only are their switches very reliable, but their exceptional performance guarantees a great user experience”, said Marc…

Humidity Measurement Module for OEM Applications

The EE1900 humidity module from E+E Elektronik is optimised for the measurement of relative humidity (RH) or dew point temperature (Td) in climate and test chambers. With outstanding temperature compensation across the working range from -70 °C to 180 °C (-94 °F to 356 °F) and the choice of stainless steel and plastic probes, the module is suitable for a wide range of applications.

High Accuracy in Harsh Environment

The excellent…