Press release

United States Flexible Packaging Market Poised to Reach USD 50.7 Billion by 2033, Driven by E-Commerce Surge, Sustainability Shift, and Advanced Barrier Technology

Once viewed primarily as a low-cost commodity sector, the United States Flexible Packaging Market has evolved into one of the most strategically dynamic segments of the broader packaging industry. Rising consumer demand for on-the-go convenience, accelerating e-commerce penetration, and mounting pressure to deliver sustainable packaging solutions are collectively rewriting the sector's competitive story. After reaching USD 33.6 Billion in 2024, the market is on a firm trajectory toward USD 50.7 Billion by 2033, reflecting a steady CAGR of 4.7% from 2025 through 2033.

Industry professionals, capital allocators, and market entrants are increasingly searching for clarity on topics like "U.S. flexible packaging industry outlook," "sustainable packaging growth trends," and "e-commerce packaging demand" signals of robust commercial activity across all segments. This press release delivers verified data and actionable insights for those making high-stakes decisions in today's fast-evolving flexible packaging landscape.

Analyze the United States Flexible Packaging Download the IMARC Sample Report for Insights: https://www.imarcgroup.com/united-states-flexible-packaging-market/requestsample

United States Flexible Packaging Market at a Glance

• Current Market Revenue (2024): USD 33.6 Billion

• Projected Market Revenue (2033): USD 50.7 Billion

• Growth Rate (2025-2033 CAGR): 4.7%

• Base Year for Analysis: 2024

• Forecast Window: 2025 to 2033

• Historical Reference Period: 2019-2024

Where the Market Is Headed in 2025

Sustained revenue growth through 2033 is not a matter of speculation it is backed by converging forces on both the demand and supply sides. Consumer preference for lightweight, portable, and shelf-life-extending packaging, combined with surging e-commerce volumes and escalating sustainability mandates, is propelling a market that is continuously raising its own performance bar.

• Total market revenue is expected to grow by more than USD 17 Billion over the forecast period, representing consistent year-over-year expansion underpinned by diverse end-use demand.

• Sustainability-driven material innovation from biodegradable films to recyclable barrier laminates is emerging as the primary competitive differentiator for flexible packaging manufacturers and converters.

• E-commerce channels are rapidly becoming essential demand drivers, with online grocery sales alone reaching USD 95.8 Billion in the U.S. as of 2023, fueling robust need for flexible, transit-safe packaging formats.

2026: A Turning Point the Industry Cannot Ignore

Market participants who move strategically in 2026 stand to capture disproportionate gains. Several structural forces are converging this year to reshape the competitive hierarchy and unlock fresh revenue pools.

• Approximately 60% of consumers today choose ready-to-eat or snack-style meals, making convenient, single-serve, and on-the-go flexible packaging solutions a baseline requirement rather than a premium feature for food and beverage brands.

• Consumer sustainability consciousness has surged dramatically - 80% of consumers now report being very or somewhat concerned about the environmental impact of packaging, up from 68% in 2023 and 66% in 2022 - intensifying pressure on brands to adopt eco-friendly flexible materials.

• The U.S. green packaging market is projected to grow at 4.3% annually, with flexible packaging recognized as a key contributor given that flexible pouches require approximately 60% less plastic than equivalent rigid bottles.

• U.S. packaging machinery investment is set to surge by 2.5% yearly as businesses upgrade to high-performance equipment for advanced flexible packaging production, signaling deep capital commitment to format modernization across the supply chain.

Speak to An Analyst: : https://www.imarcgroup.com/request?type=report&id=20042&flag=C

Forces Driving Market Expansion in 2026

Advances in Packaging Technology and Barrier Materials

Continuous material science innovation is dramatically expanding the performance envelope of flexible packaging. Advanced barrier films now protect contents from oxygen, moisture, and light far more effectively than previous-generation materials, extending shelf life without reliance on preservatives. High-performance laminates, active packaging systems, and intelligent packaging incorporating freshness indicators are becoming commercially viable at scale. These technological advancements not only improve product protection but also enable manufacturers to reduce material usage without sacrificing performance delivering simultaneous cost and sustainability benefits that resonate across the supply chain.

E-Commerce Boom and Online Grocery Expansion

The explosive growth of online shopping is one of the most powerful structural demand drivers in the flexible packaging market. As consumers order food, beverages, personal care, and pharmaceutical products online in growing volumes, brands require packaging that is lightweight, durable, tamper-evident, and optimized for transit. Flexible packaging excels across all these criteria it is cheaper to ship and store than rigid alternatives, adapts to a wide range of product geometries, and delivers superior damage protection during last-mile delivery. With U.S. e-commerce grocery sales already at USD 95.8 Billion, this channel's demand pull on flexible packaging is set to intensify throughout the forecast period.

Cost Efficiency and Manufacturing Flexibility

Flexible packaging consistently outperforms rigid alternatives on manufacturing and logistics economics. Lower material input requirements, reduced warehousing footprint due to flat-pack storage, and lighter shipping weights translate directly into margin advantages for brands and converters. The ability to produce a broad range of package sizes and formats without major retooling investments makes flexible packaging particularly attractive to small and medium enterprises seeking production agility. As raw material optimization and production automation continue to advance, cost-per-unit economics for flexible packaging are improving further reinforcing the format's dominant position in high-volume consumer goods categories.

Breaking Down the United States Flexible Packaging Market: Segment-by-Segment Opportunity

By Product Type

• Printed Rollstock: Printed rollstock is a pre-printed packaging substrate that manufacturers convert into finished bags, pouches, wraps, and labels. Offering exceptional branding flexibility and suitability for large-scale production runs, printed rollstock is the format of choice for high-volume consumer goods categories. Its compatibility with advanced printing technologies enables vibrant, detailed designs that deliver powerful shelf impact.

• Preformed Bags and Pouches: Pre-shaped and ready-to-fill, preformed bags and pouches represent one of the most dynamic growth segments in flexible packaging. Available in a wide range of configurations including stand-up pouches, spouted pouches, and resealable zipper formats these solutions are dominant in snack foods, beverages, prepared meals, and personal care products. Their consumer convenience credentials and superior shelf presence are driving accelerating adoption across food and non-food applications.

• Others: Specialty flexible packaging formats including wraps, shrink sleeves, flow packs, and lidding films serve highly specific application requirements across pharmaceutical, agricultural, and industrial sectors. Innovation in this sub-segment is driven by performance requirements such as tamper evidence, sterile barrier maintenance, and high-clarity visual inspection windows.

By Raw Material

• Plastic: Plastics remain the dominant raw material in flexible packaging, valued for their versatility, lightweight properties, and exceptional barrier performance. Polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET) are the most widely used variants, offering moisture resistance, strength, and compatibility with high-speed converting processes. Innovation in mono-material plastic structures and enhanced recyclability is addressing sustainability concerns while preserving performance.

• Paper: Paper-based flexible packaging is gaining significant momentum driven by consumer preference for renewable, biodegradable, and recyclable materials. Its positive environmental profile makes it highly attractive for brands with ambitious sustainability commitments, particularly in dry food, snack, and bakery applications. Advances in paper-barrier coating technology are expanding paper packaging's functional performance into categories previously dominated by plastic laminates.

• Aluminium Foil: Aluminium foil delivers unmatched barrier properties against oxygen, light, and moisture, making it the material of choice for applications demanding maximum product integrity - including pharmaceuticals, dairy, snacks, and cosmetics. Typically used in combination with plastic or paper layers, aluminium foil-based laminates command premium pricing and are central to the high-value end of the flexible packaging market.

• Cellulose: Cellulose-based flexible packaging is emerging as a compelling biodegradable and compostable alternative to conventional plastics. Derived from plant fibers, cellulosic packaging materials align with growing consumer and regulatory demand for packaging that returns safely to the biosphere. While still a smaller share of the overall market, cellulose packaging is gaining rapid traction in fresh produce, confectionery, and baked goods applications.

By Printing Technology

• Flexography: Flexography is the workhorse printing technology of the flexible packaging industry, capable of printing on virtually all substrate types - plastic films, paper, and aluminium foil - at high speed and low cost per unit. Its economic advantages for large production runs and ability to deliver consistent, high-quality output make it the dominant process for mainstream flexible packaging applications including bags, labels, and wrappers.

• Rotogravure: Rotogravure printing delivers the highest level of print quality and color consistency available in flexible packaging, utilizing engraved cylinders to transfer ink with exceptional precision. Preferred for premium, high-volume packaging applications in food, cosmetics, and pharmaceuticals where sharp imagery and exact color reproduction are non-negotiable, rotogravure remains the benchmark for luxury and brand-sensitive flexible packaging production.

• Digital: Digital printing is the fastest-growing printing technology segment in flexible packaging, driven by its low setup costs, rapid turnaround times, and ability to economically produce short runs, variable data, and fully customized designs. As brand owners increasingly pursue personalized packaging campaigns, limited editions, and market-specific labeling, digital printing is becoming a strategic competitive tool - particularly for emerging brands and fast-moving consumer goods companies seeking packaging agility.

• Others: Screen printing, offset lithography, and hybrid printing technologies serve specialized segments of the flexible packaging market where unique substrate requirements or specific aesthetic outcomes demand departure from conventional high-speed methods.

By Application

• Food and Beverages: Food and beverages represent the largest and fastest-growing application segment for flexible packaging in the United States. Driven by consumer demand for convenience, extended shelf life, and portion control, flexible pouches, bags, wraps, and films are integral to the packaging of snack foods, frozen meals, beverages, dairy products, condiments, and pet food. The continued growth of ready-to-eat meal formats and e-commerce grocery is sustaining robust demand growth across this category.

• Pharmaceuticals: Flexible packaging plays a critical role in pharmaceutical product protection, with aluminium foil-based blister packs, sachets, and pouches providing sterile barrier performance for tablets, capsules, powders, and medical devices. Regulatory requirements for tamper evidence, child resistance, and moisture protection are driving ongoing material and format innovation in this high-value, high-compliance application segment.

• Cosmetics: The cosmetics and personal care sector is an expanding end-use market for flexible packaging, with brands adopting pouches, tubes, and sachets to deliver premium product experiences at lower packaging cost. The growing popularity of single-use sample sachets, refillable pouches, and sustainable cosmetic packaging formats is creating new opportunities for flexible packaging converters serving beauty and personal care brands.

• Others: Agricultural inputs, industrial chemicals, household products, and pet care goods represent diverse additional application markets for flexible packaging, each with specific performance requirements around chemical resistance, UV protection, moisture control, and format-specific handling.

By Region

• Northeast: The Northeast's dense urban population, high consumer spending power, and concentration of major food and pharmaceutical manufacturing create strong baseline demand for flexible packaging. Premium and sustainability-oriented packaging formats are gaining disproportionate traction here, driven by an environmentally aware consumer base and proximity to major brand owner headquarters.

• Midwest: The Midwest is home to major food processing and agricultural production hubs, creating substantial demand for flexible packaging across grain, dairy, meat, and snack food applications. The region's large manufacturing base and cost-conscious buyer culture favor the economic advantages of flexible over rigid packaging formats.

• South: The South's rapidly growing population, expanding food and beverage manufacturing sector, and strong retail distribution infrastructure make it a high-growth market for flexible packaging. The region's favorable business environment and logistics cost advantages are attracting new packaging converter investments that will expand regional supply capacity.

• West: The West leads the nation in sustainable packaging adoption and innovation. California's stringent extended producer responsibility (EPR) regulations and highly eco-conscious consumer culture are driving accelerated transition to recyclable, compostable, and mono-material flexible packaging formats. The region is the primary testing ground for next-generation sustainable packaging solutions that will subsequently roll out nationally.

Competitive Dynamics and Strategic Moves

The competitive landscape in the U.S. flexible packaging market is more dynamic than it has been in years. Established converters and material manufacturers are no longer simply optimizing existing formats - they are actively reinventing their portfolios around sustainable materials, digital printing capabilities, and application-specific performance innovations. From billion-dollar investments in recyclable film technology to strategic acquisitions of specialty converter businesses, the industry's most powerful players are placing bold bets on the future of flexible packaging.

Simultaneously, innovative mid-size converters and material science startups are carving out high-value positions through bio-based film development, compostable laminate commercialization, and digital-first short-run production capabilities. The competitive frontier is shifting decisively from pure price competition toward value-added performance differentiation and sustainability credentials.

Where Smart Money Is Looking in 2026

For investors and operators sizing up the U.S. flexible packaging sector, the opportunity set is wider than it appears on the surface:

• Sustainable flexible packaging material developers bio-based films, mono-material recyclable laminates, and compostable cellulose solutions serving CPG brands under mounting EPR and sustainability reporting pressure

• Flexible packaging converters with advanced digital printing capability serving the growing demand for short-run, customized, and personalized packaging across food, beauty, and pharmaceutical categories

• E-commerce-optimized flexible packaging manufacturers developing transit-safe, lightweight, and brand-expressive formats for direct-to-consumer and third-party marketplace fulfillment

• Barrier film and advanced coating technology providers extending shelf life and reducing preservative dependency for food and pharmaceutical brand owners

• Packaging machinery and automation technology suppliers enabling flexible packaging converters to upgrade production speed, precision, and format changeover efficiency

• Recyclability and end-of-life infrastructure developers including chemical recycling operators and PCR (post-consumer recycled) content suppliers enabling circular economy packaging solutions

Who's Leading the U.S. Flexible Packaging Market

• Amcor plc: A global leader in flexible packaging, Amcor is at the forefront of sustainable packaging innovation with its AmLite recyclable flexible packaging platform and commitment to making all packaging recyclable or reusable by 2025. Its broad U.S. manufacturing footprint spans food, pharmaceutical, and personal care flexible packaging.

• Sealed Air Corporation: Sealed Air's Cryovac brand is synonymous with high-performance food flexible packaging, delivering advanced barrier solutions for meat, poultry, dairy, and ready-meal applications. The company's focus on automation-compatible packaging formats positions it well for growth in high-speed food processing environments.

• Berry Global Group: Berry Global is a major U.S. flexible packaging converter with extensive capabilities across film extrusion, lamination, and pouch converting. The company's investment in recyclable and PCR-content flexible packaging materials reflects its strategic commitment to circular economy leadership.

• Sonoco Products Company: Sonoco's flexible packaging division delivers printed rollstock, pouches, and specialty films for food, industrial, and consumer products applications. Its focus on sustainable flexible packaging innovation and integrated converting capabilities differentiates it in value-sensitive market segments.

• Other Key Players: Bemis Company (now part of Amcor), Printpack Inc., ProAmpac, Transcontinental Inc., Huhtamaki, Mondi Group, Winpak Ltd., Hood Packaging Corporation, Novolex, and Constantia Flexibles.

What the Full IMARC Report Delivers

IMARC Group's United States Flexible Packaging Market Report 2025 is built for professionals who need more than surface-level data. Here's what you'll gain access to:

• Comprehensive revenue forecasts (2025-2033) with segment-level granularity across product types, raw materials, printing technologies, applications, and U.S. regions

• In-depth analysis of sustainable packaging trends, including recyclable film innovation, bio-based material adoption, and EPR regulatory impact on market dynamics

• Category deep-dives into Printed Rollstock, Preformed Bags and Pouches, Plastic, Paper, Aluminium Foil, and Cellulose segments with comparative growth rate analysis

• Regional breakdown across Northeast, Midwest, South, and West with state-specific demand intelligence, converter capacity data, and sustainability regulatory landscape

• Competitive profiling of all major players with analysis of product innovation strategy, M&A activity, capacity expansion, and sustainability positioning

• End-use demand analysis across Food and Beverages, Pharmaceuticals, Cosmetics, and Other application sectors with brand owner purchasing trend data

• Investment feasibility frameworks with risk-adjusted return modeling for converter capacity investment, material innovation development, and geographic market entry scenarios

Questions Decision-Makers Are Asking

1. What is the projected size of the U.S. flexible packaging market through 2033, and which product formats and raw materials will grow fastest?

2. How are sustainability regulations particularly California's EPR legislation and national recyclability mandates - reshaping material selection and investment priorities across the flexible packaging supply chain?

3. Which U.S. regions offer the strongest near-term growth opportunities for flexible packaging converters, material suppliers, and equipment manufacturers?

4. What role is e-commerce playing in driving demand for new flexible packaging formats, and which end-use categories are generating the most incremental volume growth?

5. How are leading flexible packaging companies positioning their portfolios for the sustainable packaging transition, and what M&A and capital investment activity signals the most significant strategic shifts?

About IMARC Group

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA,

Email: sales@imarcgroup.com,

United States: +1-201971-6302

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release United States Flexible Packaging Market Poised to Reach USD 50.7 Billion by 2033, Driven by E-Commerce Surge, Sustainability Shift, and Advanced Barrier Technology here

News-ID: 4517003 • Views: …

More Releases from IMARC Group

Brazil Electricity Market Outlook 2026: Record Capacity Growth, Clean Energy Mix …

That means that in less than a decade‚ Brazil will have doubled its entire infrastructure base. This is not an optimistic scenario. The country plans to increase installed capacity from 180.67 GW in 2020 to 253.50 GW by 2025‚ and 505.40 GW by 2034‚ at a growth rate of 7.01% CAGR.

For energy investors‚ independent power producers‚ equipment manufacturers and infrastructure developers‚ the Brazil power market has become one of the…

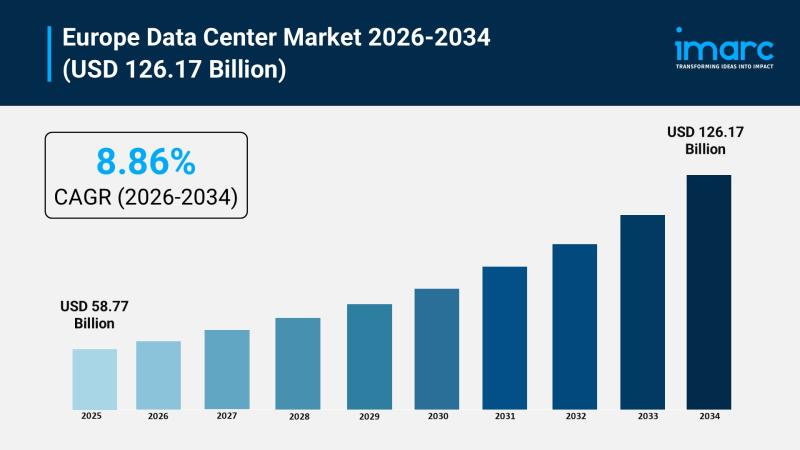

Europe Data Center Market 2026: $126.17 Billion Revenue, 8.86% CAGR and AI-Drive …

The Europe data center market reached USD 58.77 Billion in 2025. According to IMARC Group, this market is projected to reach USD 126.17 Billion by 2034, growing at a compound annual growth rate of 8.86% during 2026-2034. That is more than a doubling of revenue in under a decade, driven by forces that are structural, not cyclical: AI workload proliferation, digital sovereignty mandates, cloud-first enterprise strategies, and an edge computing…

Hydroxycitric Acid (HCA) Production Plant DPR 2026: Setup Cost, Machinery & Prof …

Setting up a hydroxycitric acid (HCA) production plant offers investors a promising opportunity in the nutraceutical and wellness industry, as HCA-primarily extracted from the rind of Garcinia cambogia-is widely used in natural weight management and nutraceutical product formulations due to its potential role in supporting fat metabolism and appetite control; driven by increasing consumer preference for plant-based health products, growing awareness of fitness and obesity management, and the expanding global…

Ice Maker Manufacturing Plant Cost DPR 2026: Complete Setup, Machinery & ROI Ana …

Setting up an ice maker manufacturing plant offers investors a strong opportunity in the commercial appliance industry, as ice makers are essential equipment for foodservice, hospitality, healthcare, supermarkets, and cold chain operations where reliable and hygienic ice production is critical for daily operations and food safety compliance; increasing demand from restaurants, quick-service chains, cafés, hotels, beverage outlets, and food processing facilities is driving market growth, while the expansion of organized…

More Releases for Flexible

Flexible Super Capacitor Market

Flexible Super Capacitor Market Overview

Flexible super capacitor usually consists of flexible electrode with superior electrochemical properties, compatible electrolyte and separator in a flexible assembly.

This report provides a deep insight into the global Flexible Super Capacitor market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis,…

The Future is Flexible: Opportunities and Challenges in the Flexible Substrate I …

The global Flexible Substrate market is estimated to attain a valuation of US$ 28.7 Bn by the end of 2031, states a study by Transparency Market Research (TMR). Besides, the report notes that the market is prognosticated to expand at a CAGR of 18.9% during the forecast period, 2022-2031.

The key objective of the TMR report is to offer a complete assessment of the global market including major leading stakeholders of…

Global Flexible Honeycomb Market, Global Flexible Honeycomb Industry, Covid-19 I …

The Flexible Honeycomb market is expected to grow from USD X.X million in 2020 to USD X.X million by 2026, at a CAGR of X.X% during the forecast period. The Global Flexible Honeycomb Market report is a comprehensive research that focuses on the overall consumption structure, development trends, sales models and sales of top countries in the global Flexible Honeycomb market. The report focuses on well-known providers in the global…

ASEAN Flexible Packaging Market: Rising Urban Population to Fuel Demand for Flex …

Already making up almost half of the retail packaging industry, the flexible packaging market is set to rise exponentially. In the Association of Southeast Asian Nations (ASEAN) in particular, the market is scaling new highs, thus connoting the presence of several large players. In a recent study, Transparency Market Research (TMR) finds that the vendor landscape of the ASEAN flexible packaging market exhibits the presence of numerous players. While none…

Flexible Glass for Flexible Electronics Market Trends and Segments 2016-2026

Glass is a non-crystalline solid which is mostly transparent and has technological, practical and decorative usage in things like window panes, electronic devices, tableware, Containers & so many. The oldest type of glass is based on the chemical compound silica which is the primary constituent of sand as well. Moving on to Flexible glass for flexible electronics, which is an ultra-thin glass with flexible and stretching feature along with all…

Flexible Glass for Flexible Electronics Market Growth, Forecast and Value Chain …

Glass is a non-crystalline solid which is mostly transparent and has technological, practical and decorative usage in things like window panes, electronic devices, tableware, Containers & so many. The oldest type of glass is based on the chemical compound silica which is the primary constituent of sand as well. Moving on to Flexible glass for flexible electronics, which is an ultra-thin glass with flexible and stretching feature along with all…