Press release

Isobutylene Production Plant DPR & Unit Setup - 2026: Machinery Cost, CapEx/OpEx, ROI and Raw Materials

Market Overview and Growth Potential:

The global isobutylene market is driven by the rising demand for high-performance fuels, increasing production of synthetic rubber, expanding petrochemical applications, and growing use in fuel additives such as MTBE and ETBE. The isobutylene market size was valued at USD 17.00 Billion in 2025. According to IMARC Group estimates, the market is expected to reach USD 25.05 Billion by 2034, exhibiting a CAGR of 4.4% from 2026 to 2034. According to IMARC Group data, the global petrochemicals market reached USD 675.7 Billion in 2025, reflecting steady expansion across key end-use industries. This growth continues to support rising demand for isobutylene, as its applications in fuel additives, rubber production, and specialty chemicals align closely with increasing industrial and energy sector requirements. Increasing global vehicle demand and stricter fuel efficiency and emission norms are encouraging the use of high-performance fuel components such as MTBE and ETBE. Additionally, the expansion of industrial manufacturing and infrastructure development is supporting demand for polymers and specialty chemicals derived from isobutylene.

Request for Sample Report: https://www.imarcgroup.com/isobutylene-manufacturing-plant-project-report/requestsample

Isobutylene, also known as isobutene, is a colorless, flammable hydrocarbon belonging to the olefin family with the chemical formula C4H8. It is primarily produced as a byproduct of petroleum refining processes such as steam cracking and fluid catalytic cracking, or through dehydrogenation of isobutane. Isobutylene serves as a key intermediate in the petrochemical industry and is widely used in the production of butyl rubber, polyisobutylene, and fuel additives like methyl tert-butyl ether (MTBE) and ethyl tert-butyl ether (ETBE). It also plays a crucial role in manufacturing antioxidants, plasticizers, and specialty chemicals. Due to its high reactivity and versatility, isobutylene is essential in enhancing fuel efficiency, improving product performance, and supporting various industrial and automotive applications.

The isobutylene market is driven by steady growth in the petrochemical and automotive industries, particularly due to its role in fuel additives and synthetic rubber production. Increasing global vehicle demand and stricter fuel efficiency and emission norms are encouraging the use of high-performance fuel components such as MTBE and ETBE. The expansion of industrial manufacturing and infrastructure development is supporting demand for polymers and specialty chemicals derived from isobutylene. Refinery integration and advancements in catalytic dehydrogenation technologies are improving production efficiency and cost optimization, while the growth of the specialty chemicals sector driven by increasing industrial and consumer applications creates expanding and diversified downstream demand for isobutylene as a versatile and reactive petrochemical building block.

Plant Capacity and Production Scale:

The proposed isobutylene production facility is designed with an annual production capacity ranging between 200,000 to 300,000 tons, enabling economies of scale while maintaining operational flexibility across high-purity polymer-grade isobutylene for butyl rubber and polyisobutylene production, fuel additive-grade isobutylene for MTBE and ETBE synthesis, chemical intermediate-grade isobutylene for antioxidant, plasticizer, and specialty chemical synthesis, and technical-grade isobutylene for industrial and lubricant additive applications across the petrochemical industry, automotive and transportation sector, fuel refining industry, and rubber manufacturing industry end-use sectors. This production range supports supply to both large-scale butyl rubber producers and MTBE and ETBE fuel additive manufacturers requiring high-volume, continuous supply of specification-grade isobutylene with controlled purity and impurity profile, and specialty chemical customers requiring high-purity isobutylene with verified analytical specifications for polyisobutylene and antioxidant synthesis applications.

Speak to an Analyst for Customized Report: https://www.imarcgroup.com/request?type=report&id=10068&flag=C

Financial Viability and Profitability Analysis:

The isobutylene production business demonstrates healthy profitability potential under normal operating conditions. The financial projections reveal:

• Gross Profit: 25-35%

• Net Profit: 12-18%

These margins reflect the catalytic process chemistry and feedstock-intensive nature of isobutylene production, where isobutane feedstock and platinum catalyst are processed through controlled feedstock pre-treatment, catalytic dehydrogenation or fluid catalytic cracking, separation and purification, distillation, and storage operations to produce specification-grade isobutylene meeting stringent purity, moisture, diolefin, and sulfur impurity requirements for butyl rubber polymerization, MTBE and ETBE synthesis, and polyisobutylene manufacturing customer applications. Margins are supported by strong and consistent demand from rubber, fuel additive, and specialty chemical sectors with long-term supply agreements providing revenue visibility; growing automotive production driving butyl rubber and MTBE demand; the ability to command stable pricing supported by chemical purity specifications and consistent product quality; and meaningful refinery or petrochemical complex integration, platinum catalyst management, and large-scale process plant capital barriers to entry. The project demonstrates solid return on investment (ROI) potential with comprehensive financial analysis covering income projections, expenditure projections, break-even points, net present value (NPV), internal rate of return, and detailed profitability and sensitivity analysis. Isobutane feedstock procurement cost management and dehydrogenation catalyst performance and selectivity optimization are the primary operational variables impacting margin performance.

Cost of Setting Up an Isobutylene Production Plant:

Operating Cost Structure:

The cost structure for an isobutylene production plant is primarily driven by:

• Raw Materials: 65-75% of total OpEx

• Utilities: 15-20% of OpEx

• Other Expenses: Including transportation, packaging, salaries and wages, depreciation, taxes, and other expenses

Raw materials - particularly isobutane feedstock and platinum dehydrogenation catalyst account for approximately 65-75% of total operating expenses, making isobutane procurement strategy, feedstock supply pipeline access, supplier qualification, and long-term supply contract management the central raw material cost management priority. Isobutane purity, normal butane and propane impurity content, moisture, and sulfur specification critically impact both dehydrogenation catalyst life and reaction selectivity, and finished isobutylene product purity, diolefin content, and downstream polymerization or alkylation catalyst compatibility, with feedstock quality management directly affecting achievable isobutylene yield, product specification compliance, and catalyst cycle length between regenerations. Utilities represent a notably high 15-20% of OpEx, driven by the high-temperature dehydrogenation reactor heating energy requirements (reaction temperatures typically above 550 to 600 degrees Celsius), recycle gas compression energy, distillation column reboiler energy consumption, and the significant steam and electricity requirements of continuous isobutylene production and purification processes. In the first year of operations, costs cover raw materials, utilities, depreciation, taxes, packing, transportation, and repairs and maintenance. By the fifth year, the total operational cost is expected to increase substantially due to factors such as inflation, market fluctuations, and potential rises in the cost of key materials, with supply chain disruptions, rising consumer demand, and shifts in the global economy also expected to contribute to this increase.

Capital Investment Requirements:

Setting up an isobutylene production plant requires significant capital investment across feedstock pre-treatment, catalytic dehydrogenation or cracking reactors, separation and purification, distillation columns, compressors, heat exchangers, storage tanks, and safety systems infrastructure. The total capital investment depends on plant capacity, production technology selection (catalytic dehydrogenation versus fluid catalytic cracking byproduct recovery), product purity grade requirements, automation level, and location, covering land acquisition, site preparation, and large-scale petrochemical process plant infrastructure meeting all applicable pressure vessel safety, environmental, and process safety management regulatory compliance requirements.

Land and Site Development: The location must offer easy access to key raw materials such as isobutane from petroleum refinery butane streams, natural gas liquids fractionation facilities, or pipeline infrastructure, and platinum dehydrogenation catalyst from specialty catalyst manufacturers, along with proximity to target markets including butyl rubber plants, MTBE and ETBE synthesis units, polyisobutylene manufacturers, specialty chemical producers, and fuel blending terminals to minimize isobutylene transportation distances and logistics costs. The site must have robust infrastructure including reliable high-capacity electrical power and steam for dehydrogenation reactor and separation process operations, isobutane feedstock pipeline or storage and vaporization infrastructure meeting flammable gas handling safety requirements, reliable pipeline or road tanker isobutylene product dispatch infrastructure, and effluent treatment and flare systems for process hydrocarbon waste stream management. Compliance with chemical plant process safety management regulations, flammable hydrocarbon gas handling and containment safety standards, environmental compliance for hydrocarbon emission management and flaring minimization, and all applicable worker safety and health regulations for flammable gas and hydrocarbon exposure management must be ensured.

Machinery and Equipment: Equipment costs for reactors (dehydrogenation units), distillation columns, compressors, heat exchangers, storage tanks, and safety systems represent the largest capital expenditure category. High-quality, pressure-rated, and corrosion-resistant machinery tailored for isobutylene production must be selected. Essential equipment includes:

• Feedstock pre-treatment systems - isobutane feedstock receiving, storage, vaporization, and pre-treatment systems including sulfur removal (hydrodesulfurization or guard bed adsorbents) for removal of sulfur compounds from isobutane feedstock to sub-ppm levels required for protection of downstream platinum dehydrogenation catalyst from sulfur poisoning, together with moisture removal by molecular sieve drying for catalyst protection

• Dehydrogenation reactors - fixed-bed or moving-bed catalytic dehydrogenation reactor systems for selective catalytic dehydrogenation of isobutane to isobutylene over platinum-based or chromia-alumina catalyst at high temperature (550 to 620 degrees Celsius) and low pressure with controlled hydrogen co-feed for catalyst stability, achieving per-pass isobutylene yield at specified conversion and selectivity for continuous isobutylene production

• Catalyst regeneration systems - continuous or cyclic catalyst regeneration systems for removal of carbon deposits (coke) from dehydrogenation catalyst by controlled combustion in air-steam atmosphere at specified temperature conditions, restoring catalyst activity and maintaining sustained per-pass conversion in continuous production operation

• Compressors - multi-stage centrifugal or reciprocating compressors for reactor effluent gas compression and recycle gas pressurization in the dehydrogenation reaction loop, hydrogen recycle and purge compression, and product isobutylene compression for pipeline or storage transfer at specified process pressures throughout the isobutylene production and separation flowsheet

• Distillation columns - multi-stage fractionation column systems for separation of isobutylene product from unconverted isobutane recycle, propylene and lighter hydrocarbon byproducts, and heavier C5+ byproducts in the dehydrogenation reactor effluent, achieving specification isobutylene purity and recovery in distilled product at controlled reflux ratio and column cut points

• Heat exchangers - multi-pass shell-and-tube heat exchangers for process heat recovery between hot reactor effluent and cold feed streams, reaction product cooling, and distillation overhead condenser and reboiler heat duty provision, reducing utility energy consumption through efficient process heat integration across the isobutylene production flowsheet

• Storage tanks - refrigerated or pressurized bullet or sphere storage vessels for isobutylene product inventory management at specified storage pressure and temperature conditions meeting flammable gas storage safety standards, with product quality monitoring during storage and controlled vapor recovery and loading systems for pipeline, road tanker, or rail car isobutylene product dispatch

• Safety systems - distributed control system (DCS) process automation, safety instrumented system (SIS) emergency shutdown and pressure relief management, flammable and toxic gas detection systems throughout isobutylene and isobutane handling areas, flare system for emergency hydrocarbon depressurization and vent stream combustion, and fire detection and suppression systems for process area safety compliance

All machinery must comply with applicable chemical plant pressure vessel safety codes, flammable gas process plant safety standards, and petrochemical product quality requirements. ISO 9001 quality management system certification, process safety management (PSM) documentation and HAZOP study compliance, environmental permit compliance for hydrocarbon emissions and flaring management, and compliance with butyl rubber producer, MTBE synthesis unit, and specialty chemical customer technical specification and isobutylene supplier qualification requirements are standard prerequisites for commercial isobutylene supply to major rubber, fuel additive, and specialty chemical customers.

Civil Works: Building construction and plant layout optimized for efficient workflow, flammable hydrocarbon process safety compliance, and isobutylene production quality and environmental monitoring requirements across isobutane feedstock receiving and storage, pre-treatment, dehydrogenation reactor area, catalyst regeneration, reactor effluent separation and compression, distillation, isobutylene product storage, and dispatch areas. Explosion-proof electrical classification throughout isobutane and isobutylene handling and processing areas, emergency shutdown and pressure relief valve discharge to flare system piping throughout the process plant, hydrocarbon vapor detection and safety interlock systems, isobutylene product storage area with earthing and bonding for static discharge prevention, and continuous emissions monitoring for environmental compliance are essential isobutylene production facility safety and regulatory compliance requirements.

Other Capital Costs: Costs associated with land acquisition, construction, and utilities including high-capacity electrical substation for compressor and reactor heating system power supply, steam generation plant for process steam and heating requirements, isobutane feedstock storage and vaporization infrastructure, flare and vapor recovery system for hydrocarbon emission control, isobutylene product storage and loading infrastructure with metering and quality sampling systems, and process safety management documentation and HAZOP study for plant safety case development must be considered in the financial plan. Pre-operative expenses including process safety management documentation and HAZOP study, environmental impact assessment and air emission permit for hydrocarbon processing operations, chemical plant operating license, ISO 9001 quality system certification, initial isobutane and catalyst inventory for dehydrogenation process commissioning and product grade qualification, and operator dehydrogenation process chemistry, catalyst management, and safety training programs are important components of total project investment planning.

Buy Now: https://www.imarcgroup.com/checkout?id=10068&method=2175

Major Applications and Market Segments:

Isobutylene production outputs serve critical polymer synthesis, fuel blending, lubrication, and specialty chemical intermediate functions across the global petrochemical, automotive, fuel refining, and rubber manufacturing sectors:

Petrochemical Industry: Isobutylene serves as a fundamental building block for producing polymers and intermediates used in various chemical processes. It enables efficient large-scale chemical synthesis with consistent quality. Polyisobutylene (PIB) produced by cationic polymerization of isobutylene serves as the key component in fuel and lubricant additive packages for internal combustion engine deposits control, as a sealant and adhesive base polymer in construction and automotive applications, and as a carrier resin for pharmaceutical tablet coating applications, with molecular weight selection enabling wide-ranging physical property tailoring from highly viscous liquid PIB to solid, high-molecular-weight elastomeric grades.

Automotive and Transportation Sector: Isobutylene is used in the production of fuel additives and synthetic rubber, enhancing fuel performance and vehicle efficiency. Its derivatives improve durability and emission control. Butyl rubber (isobutylene-isoprene copolymer) produced by low-temperature cationic copolymerization of isobutylene with isoprene is the dominant synthetic rubber used for tire inner tubes, tire innerliner in tubeless tires, automotive hoses, and engine mounts due to its exceptional air impermeability and vibration damping properties, with each passenger car and truck tire requiring butyl rubber inner liner for air retention performance, creating a large and structural demand link between global tire production and isobutylene consumption.

Fuel Refining Industry: Isobutylene is widely utilized in manufacturing MTBE and ETBE, which are blended with gasoline to improve octane ratings and combustion efficiency. Methyl tert-butyl ether (MTBE) and ethyl tert-butyl ether (ETBE) produced by acid-catalyzed etherification of isobutylene with methanol and ethanol respectively are high-octane, low-Reid-vapor-pressure fuel blending oxygenates used in reformulated gasoline formulations to improve octane rating, reduce CO and unburned hydrocarbon emissions, and meet specification requirements for oxygen content in regions with oxygenate-mandated fuel standards.

Rubber Manufacturing Industry: Isobutylene plays a critical role in producing butyl rubber, which is used in tire manufacturing due to its excellent air retention and resistance properties. TPC Group's October 2024 expansion of its di-isobutylene unit capacity to strengthen supply amid rising downstream demand illustrates the commercial confidence in continued isobutylene derivative demand growth across specialty rubber and fuel additive applications, with the growing global tire production volume driven by expanding vehicle fleets in emerging markets creating sustained and expanding butyl rubber demand that drives upstream isobutylene consumption.

Why Invest in Isobutylene Production?

Several compelling strategic and commercial factors make isobutylene production an attractive investment:

Growing Demand for Fuel Additives: Increasing fuel efficiency regulations are driving demand for high-octane additives derived from isobutylene, supporting market growth. Stricter automotive emission standards and fuel economy regulations across major vehicle markets are creating regulatory-backed demand for high-performance gasoline formulations incorporating MTBE or ETBE octane enhancers derived from isobutylene, with the global petrochemicals market reaching USD 675.7 Billion in 2025 per IMARC Group data reflecting the scale of downstream chemical demand expansion that encompasses isobutylene-derived fuel additive and polymer applications.

Expansion of Synthetic Rubber Industry: Rising automotive production and tire demand are boosting the consumption of butyl rubber derived from isobutylene. The structural growth of global tire production driven by expanding passenger car and commercial vehicle fleets in Asia-Pacific, the Middle East, and Africa creates expanding and persistent butyl rubber demand, with each new tire produced requiring isobutylene-derived butyl rubber for inner tube or innerliner applications that together constitute a large and stable consumption base for upstream isobutylene supply.

Versatile Chemical Intermediate: Its wide applicability across petrochemicals, plastics, and lubricants enhances its industrial significance and demand stability. The diversity of isobutylene end-use applications across butyl rubber, polyisobutylene, MTBE and ETBE fuel additives, antioxidants, plasticizers, and specialty chemical intermediates provides natural revenue diversification that protects isobutylene producers from single-application demand cyclicality, with the multi-sector demand base providing inherent commercial resilience and volume stability.

Integration with Refinery Operations: Isobutylene production can be integrated with existing refinery units, optimizing resource utilization and reducing operational costs. Integration of isobutylene dehydrogenation capacity adjacent to existing refinery butane processing infrastructure enables feedstock supply chain efficiency and product dispatch cost minimization, with refinery integration enabling production scheduling coordination, shared utilities and infrastructure utilization, and operational synergy that can improve overall production economics relative to standalone greenfield isobutylene plant investments.

Stable and Scalable Production: Established processing technologies enable scalable operations with reliable output and efficient cost management. The catalytic dehydrogenation of isobutane to isobutylene is a commercially mature and well-understood large-scale petrochemical process with established engineering, procurement, and construction contractor capability for plant delivery, enabling confident capital investment in 200,000 to 300,000 ton per year isobutylene production capacity with known technology performance, catalyst management requirements, and operational reliability profiles based on extensive commercial production experience.

Manufacturing Process Excellence:

The isobutylene production process involves feedstock pre-treatment, catalytic dehydrogenation or cracking, separation and purification, distillation, and storage. The main production steps include:

• Feedstock receiving and pre-treatment - isobutane feedstock receiving from pipeline or storage, moisture removal by molecular sieve drying, sulfur compound removal by hydrodesulfurization or guard bed adsorption to below-ppm specification for platinum catalyst protection, and feedstock quality verification by online analysis for isobutane purity and impurity profile

• Catalytic dehydrogenation - controlled high-temperature catalytic dehydrogenation of purified isobutane feed over platinum or modified alumina catalyst at specified reactor temperature (typically 550 to 620 degrees Celsius), pressure, space velocity, and hydrogen co-feed ratio conditions to produce reactor effluent containing isobutylene, unconverted isobutane, hydrogen, and minor byproducts at specified per-pass conversion and isobutylene selectivity

• Reactor effluent cooling and compression - controlled quench cooling of hot reactor effluent from reaction temperature to downstream separation conditions, followed by multi-stage compression of reactor effluent gas for pressure elevation to distillation separation column operating pressure, with inter-stage knockout drums for liquid hydrocarbon condensate separation

• Separation and purification - multi-stage distillation of compressed reactor effluent in deisobutanizer, debutanizer, and isobutylene fractionation column systems for sequential removal of hydrogen and light gases, propylene and propane, n-butane, and heavier C5+ byproducts from isobutylene product stream, and concentration of isobutylene to specification purity by controlled fractionation cut points

• Recycle compression and isobutane recycle - compression and recycle of unconverted isobutane from distillation column overhead streams back to dehydrogenation reactor feed for overall isobutane-to-isobutylene conversion maximization across the production unit, with purge gas management for inert accumulation control and hydrogen recovery or fuel gas disposal

• Catalyst regeneration - periodic or continuous catalyst regeneration by controlled combustion of catalyst coke deposits in air-steam atmosphere at specified temperature profiles, restoring catalyst activity and per-pass conversion performance for sustained production continuity between scheduled turnarounds

• Product quality testing - isobutylene product purity by gas chromatography, diolefin content, water content, sulfur content, and other specification parameter analysis for continuous production quality monitoring and customer shipment certificate preparation

• Storage and dispatch - isobutylene product storage in refrigerated or pressurized storage vessels at specification conditions with continuous quality monitoring, followed by pipeline transfer, road tanker, or rail car loading with full batch traceability and analytical certificate documentation for customer delivery

The complete process flow encompasses unit operations involved, mass balance and raw material requirements, quality assurance criteria, and technical tests throughout production. Dehydrogenation reactor condition logs, catalyst activity monitoring records, isobutane conversion and isobutylene selectivity data, distillation column operating records, product purity gas chromatography test results, and full feedstock-to-product traceability records must be maintained throughout all production and dispatch operations. Regular butyl rubber producer, MTBE synthesis unit, and specialty chemical customer supplier quality audit visits are standard operating requirements for commercial isobutylene supply to major petrochemical, fuel additive, and rubber manufacturing customers.

Industry Leadership:

The global isobutylene industry is served by major integrated petrochemical and refining companies with access to isobutane feedstock and established downstream customer relationships. Key industry players include:

• Exxon Mobil Corporation

• TPC Group

• BASF

• Shell plc

• LyondellBasell Industries Holdings B.V.

These companies serve diverse end-use sectors including the petrochemical industry, automotive and transportation sector, fuel refining industry, and rubber manufacturing industry, with leading players investing continuously in dehydrogenation catalyst performance improvement, refinery integration optimization, specialty isobutylene derivative development, and production capacity expansion to meet the evolving purity, volume, and supply security requirements of global butyl rubber, fuel additive, and specialty chemical customers.

Recent Industry Developments:

October 2024: TPC Group expanded its capacity at its di-isobutylene unit to strengthen supply amid rising downstream demand. The project focuses on improving operational efficiency, supporting fuel and lubricant applications, and reinforcing the company's position in specialty petrochemicals. This strategic expansion move highlights the growing consumption trends across sectors and the strategic importance of isobutylene in the specialty petrochemical value chain.

Browse Full Report: https://www.imarcgroup.com/isobutylene-manufacturing-plant-project-report

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company excels in understanding its client's business priorities and delivering tailored solutions that drive meaningful outcomes. We provide a comprehensive suite of market entry and expansion services. Our offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape, and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: (+1-201-971-6302)

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Isobutylene Production Plant DPR & Unit Setup - 2026: Machinery Cost, CapEx/OpEx, ROI and Raw Materials here

News-ID: 4513198 • Views: …

More Releases from IMARC Group

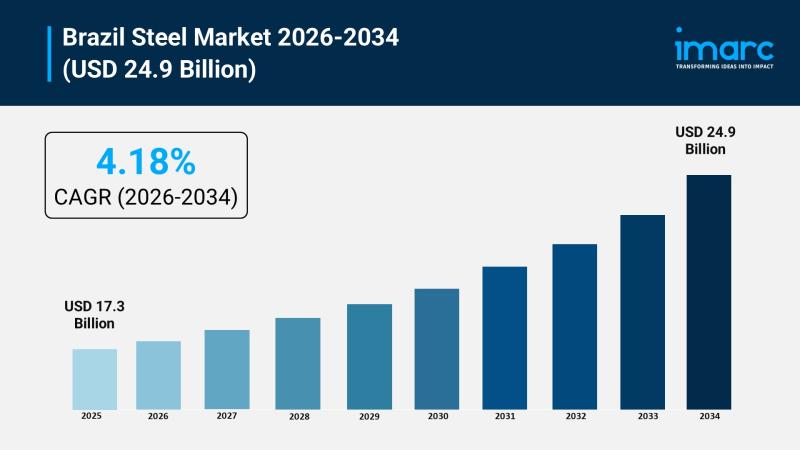

Brazil Steel Market Forecast: Revenue, Production & Demand Outlook Through 2034

Brazil's steel industry sits at the intersection of two powerful forces: a construction and infrastructure boom that shows no signs of slowing, and a global decarbonization push that is reshaping how steel itself gets made. The Brazil steel market, valued at USD 17.3 Billion in 2025, is projected to reach USD 24.9 Billion by 2034, growing at a compound annual rate of 4.18% between 2026 and 2034. That trajectory reflects…

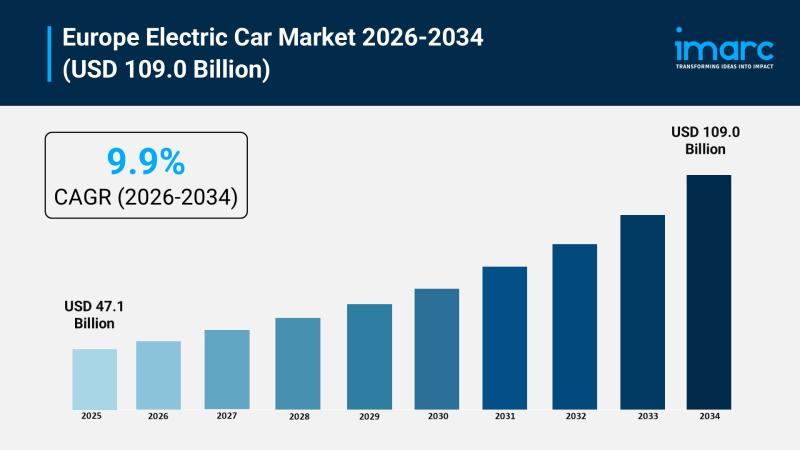

Europe Electric Car Market Report 2026: Revenue, CAGR & Emerging Opportunities B …

Europe's electric car industry is entering a phase where policy, affordability, and infrastructure are finally moving in the same direction at the same time. The Europe electric car market, valued at USD 47.1 Billion in 2025, is projected to reach USD 109.0 Billion by 2034, growing at a compound annual rate of 9.9% between 2026 and 2034. This trajectory reflects more than doubling market value within a decade, driven by…

Mexico Precision Agriculture Market Size Projected to Reach USD 289.5 Million by …

IMARC Group has recently released a new research study titled "Mexico Precision Agriculture Market Report by Technology (GNSS/GPS Systems, GIS, Remote Sensing, Variable Rate Technology (VRT), Others), Type (Automation and Control Systems, Sensing and Monitoring Devices, Farm Management System), Component (Hardware, Software), Application (Mapping, Crop Scouting, Yield Monitoring, Soil Monitoring, Precision Irrigation, Others), and Region 2026-2034," offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends and competitive…

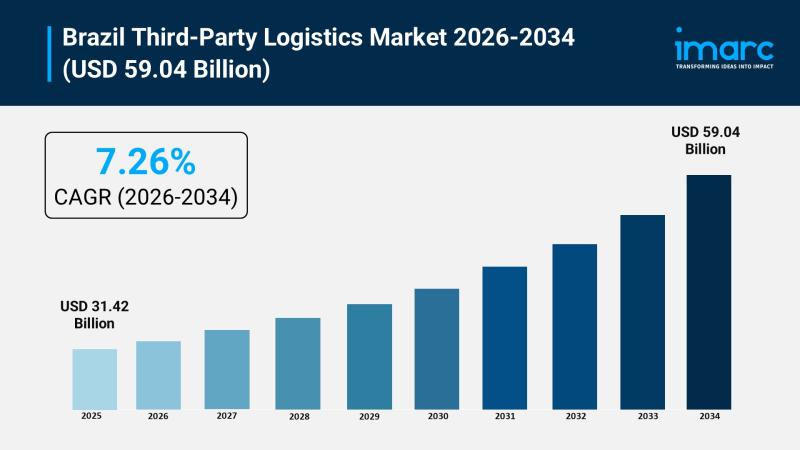

Brazil Third-Party Logistics Market to Reach USD 59.04 Billion by 2034 at 7.26% …

Brazil's outsourced logistics sector is scaling rapidly as e-commerce fulfillment, manufacturing recovery, and government-backed infrastructure investment converge into a single growth narrative. The Brazil third-party logistics market, valued at USD 31.42 Billion in 2025, is projected to reach USD 59.04 Billion by 2034, growing at a compound annual rate of 7.26% between 2026 and 2034, a pace that positions Brazil among Latin America's fastest-expanding logistics economies.

Download a sample copy of…

More Releases for MTBE

Methyl Tert-Butyl Ether (MTBE) Prices, Trend, Index & Analysis October 2025

Northeast Asia Methyl Tert-Butyl Ether (MTBE) Prices Movement Oct 2025

In October 2025, Methyl Tert-Butyl Ether (MTBE) prices in Northeast Asia stood at 0.74 USD/kg, reflecting a slight 0.6% decline. The downturn was mainly due to softened gasoline blending demand and improved regional supply. Stable crude oil prices and steady refinery operations helped maintain market balance despite moderate demand reduction.

Regional Analysis: The price analysis can be expanded to include detailed…

MTBE Production Cost: An In-Depth Analysis 2023-2028 | Syndicated Analytics

The latest report by Syndicated Analytics titled "MTBE Production Cost Analysis 2023-2028: Capital Investment, Manufacturing Process, Raw Materials, Operating Cost, Industry Trends and Revenue Statistics" provides the necessary information needed to enter the MTBE industry. Based on the most recent economic data, the study provides in-depth insights into pricing, margins, utility expenses, operating costs, capital investments, raw material requirements, and basic process flow.

The techno-economic report offers the latest information about the…

High Purity MTBE Market Key Futuristic Trends and Opportunities 2030

High Purity MTBE Market: Introduction

Transparency Market Research delivers key insights on the global high purity MTBE market. In terms of revenue, the global high purity MTBE market is estimated to expand at a CAGR of ~7% during the forecast period, owing to numerous factors, regarding which TMR offers thorough insights and forecasts in its report on the global high purity MTBE market.

Read report Overview:

https://www.transparencymarketresearch.com/high-purity-mtbe-market.html

The global high purity MTBE market is…

Methyl Tertiary Butyl Ether (MTBE) Market 2022 | Detailed Report

Global Methyl Tertiary Butyl Ether (MTBE) Market 2021-2027, has been prepared based on an in-depth market analysis with inputs from industry experts. The report covers the market landscape and its growth prospects in the coming years. The report includes a discussion of the key vendors operating in this market. An exclusive data offered in this report is collected by research and industry experts team.

Download FREE Sample Report @ https://www.reportsnreports.com/contacts/requestsample.aspx?name=5312448

The…

Global MTBE Market Expected to Witness a Sustainable Growth over 2025

LP INFORMATION recently released a research report on the MTBE market analysis, which studies the MTBE's industry coverage, current market competitive status, and market outlook and forecast by 2025.

Global “MTBE Market 2020-2025” Research Report categorizes the global MTBE market by key players, product type, applications and regions,etc. The report also covers the latest industry data, key players analysis, market share, growth rate, opportunities and trends,…

MTBE Market Size, Share, Development by 2023

New report published by Market Research Report Store (MRRS) which offers insights on the global MTBE market.

Methyl Tertiary Butyl Ether(MTBE)is an organic compound with molecular formula (CH3)3COCH3. MTBE is a volatile, flammable, and colorless liquid that is sparingly soluble in water. It has a minty odor vaguely reminiscent of diethyl ether, leading to unpleasant taste and odor in water. It has a minty odor vaguely reminiscent of diethyl ether, leading…