Press release

Small Modular Reactor Market to Add US$5.82 Billion by 2033 as AI Data Centers, Energy Security and Firm Low-Carbon Power Pull Utilities, EPCs and Reactor Vendors Into Commercial Deployment

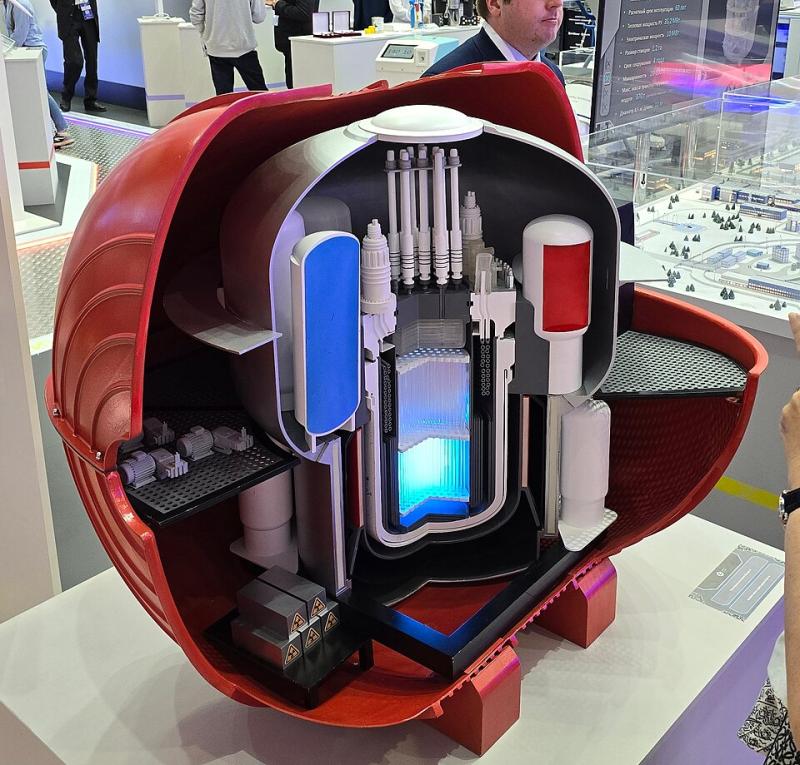

Small Modular Reactor Market

Request Executive Sample | Market Intelligence: https://www.datamintelligence.com/download-sample/small-modular-reactor-market?kailas

The most important shift in the market is that SMRs are no longer being discussed only as future nuclear technology. They are increasingly being framed as infrastructure for power-hungry digital economies, industrial decarbonization, grid reliability, remote energy access, desalination, process heat, and hydrogen production. The commercial ecosystem is also becoming clearer: utilities, reactor vendors, EPC contractors, data-center developers, public agencies, fuel suppliers, national labs, and industrial off-takers are beginning to move from memorandums of understanding toward site selection, licensing, early works, and supply-chain formation.

The timing matters. The International Energy Agency projects global electricity generation required for data centers to rise from 460 TWh in 2024 to more than 1,000 TWh by 2030 in its base case, while EPRI estimates that U.S. data centers could consume 4.6% to 9.1% of U.S. electricity generation annually by 2030, compared with roughly 4% today. This is creating a new buyer class for SMRs: companies and utilities that need around-the-clock clean electricity, not intermittent power alone.

Recent Developments Reshaping the SMR Market

1. U.S. federal support moved from broad policy to project-specific deployment funding. In December 2025, the U.S. Department of Energy selected Tennessee Valley Authority and Holtec Government Services to support early deployments of advanced light-water SMRs, with project teams eligible for up to US$800 million in federal cost-shared funding for projects in Tennessee and Michigan. TVA is also the first U.S. utility applying to build GE Vernova Hitachi's BWRX-300 at the Clinch River site, after securing an early site permit for SMR development.

2. Canada turned the BWRX-300 into the Western world's most advanced commercial SMR construction case. The Canadian Nuclear Safety Commission issued Ontario Power Generation a construction licence in April 2025 to build one GE Hitachi BWRX-300 reactor at the Darlington New Nuclear Project, with the licence valid until March 31, 2035. Ontario later approved construction on the first of four planned SMRs at Darlington, positioning the project as a critical reference case for utilities and regulators watching whether factory-style nuclear deployment can move from planning into construction discipline.

3. AI infrastructure buyers are becoming direct SMR market shapers. Amazon and X-energy announced a partnership supporting the first phase of the Cascade Advanced Energy Facility with Energy Northwest in Washington, using four Xe-100 reactor units for an initial 320 MW and the option to expand to 12 units and 960 MW. X-energy states that each Xe-100 unit is engineered to provide 80 MW of electricity and that multi-unit plants can scale from 320 MW to 960 MW, a format that fits hyperscale data-center growth better than one-off power procurement.

4. The United Kingdom created one of Europe's strongest SMR commercialization signals. Rolls-Royce SMR signed a contract with Great British Energy - Nuclear in April 2026, paving the way for the design and delivery of the first SMRs in the UK. The company also stated that three SMRs will be sited at Wylfa in North Wales and that Czech utility CEZ Group had signed an early works agreement linked to up to 3 GW of low-carbon energy in Czechia.

5. NuScale strengthened its regulatory-first positioning. NuScale reported that it remains the first and only SMR technology to have received U.S. Nuclear Regulatory Commission design approval, including its uprated 77 MWe NuScale Power Module. The company also said ENTRA1 and TVA continue to advance discussions around deployment of up to 6 GW of NuScale SMR capacity across TVA's seven-state service region.

6. Westinghouse linked SMRs to a larger U.S. nuclear industrial-base strategy. Westinghouse, Brookfield and Cameco entered into a strategic partnership with the U.S. Government to accelerate nuclear deployment, with at least US$80 billion of new reactors planned across the United States using AP1000 and AP300 nuclear reactor technology. This is important for SMRs because it connects deployment to supply-chain rebuilding, AI power demand, and large-scale financing rather than technology promotion alone.

Market Segmentation:

By reactor type, light-water reactors are expected to remain the largest commercial segment through the first half of the forecast period. Internal analyst allocation places light-water SMRs at approximately 65% of 2025 revenue, or about US$4.17 billion, with the segment potentially reaching US$7.10 billion by 2033 even as its share moderates as advanced reactors mature. The reason is practical: utilities, regulators, EPC firms, component suppliers, and fuel providers already understand light-water technology, making it the near-term bankable route for grid-connected SMRs. The U.S. DOE also notes that light-water SMRs can leverage existing service and supply-chain sectors supporting the current reactor fleet, which could speed deployment.

High-temperature reactors are the segment to watch for upside. Analyst allocation places the segment at around US$0.96 billion in 2025, with potential to reach US$2.82 billion by 2033 as industrial steam, process heat, refining, chemicals, hydrogen, and data-center campuses become more important. X-energy's Xe-100 strategy is a clear example: the reactor is being positioned for electricity and industrial steam, not only grid power.

By connectivity, grid-connected SMRs dominate current demand, estimated at about US$5.01 billion in 2025 and projected to approach US$9.18 billion by 2033. Utilities are the natural first buyers because they already manage licensing, transmission, long-term power planning, and rate-base economics. Off-grid SMRs will grow selectively in mining, defense, remote communities, islands, and industrial sites, but those markets will depend heavily on siting, licensing model, operator capability, and local acceptance.

By application, power generation remains the anchor segment, estimated at US$4.49 billion in 2025 and potentially reaching US$7.71 billion by 2033. However, the more lead-generating opportunity is in hybrid applications: power plus heat, power plus desalination, power plus hydrogen, or power plus data-center reliability. Buyers are increasingly asking whether SMRs can solve a full energy problem rather than simply add megawatts.

Regional Analysis: North America, Europe and Asia-Pacific

North America is the strongest near-term commercialization region. The United States has policy momentum, advanced reactor developers, national laboratory support, growing data-center electricity demand, and utilities exploring first-of-a-kind deployment. Canada has the most advanced commercial construction reference through Darlington. Together, these markets give North America a clear advantage in licensing depth, public-private funding, and early deployment visibility.

The United States is especially important because the market is moving from pilot language to deployment architecture. The NRC's new Part 53 framework establishes a risk-informed, performance-based, technology-inclusive licensing pathway for commercial nuclear plants, while the DOE has identified federal sites that may support AI infrastructure and new energy generation such as nuclear. These moves are aligning SMRs with the urgent U.S. debate over data-center load growth, grid reliability, and energy security.

Canada's advantage is execution visibility. OPG's Darlington project gives reactor vendors, EPCs, suppliers, public agencies, and utilities a live case to study. If Darlington keeps schedule discipline, it could become the most powerful sales reference in the global SMR market because buyers need proof that modular nuclear construction can be repeated, financed, licensed, and delivered.

Europe is moving through a different pathway: government-backed procurement, energy-security pressure, and industrial policy. The UK's Rolls-Royce SMR decision is not only a reactor award; it is a supply-chain and national capability decision. Czechia's early works agreement with Rolls-Royce SMR also shows that European demand is being shaped by coal replacement, industrial competitiveness, and long-term sovereign energy planning.

Asia-Pacific is emerging as a strategic supply-chain and export region. GE Vernova and Hitachi signed an MoU in March 2026 to explore deployment of the BWRX-300 in Southeast Asia and to incorporate qualified Japanese suppliers into the SMR supply chain. South Korea also remains important through KEPCO Engineering & Construction, which states it is focusing on SMRs such as BANDI, its original model for offshore floating SMRs.

Detailed Company Profiles

Westinghouse Electric Company

Westinghouse is positioning the AP300 SMR as a lower-risk route into modular nuclear because it is based on licensed and operating AP1000 technology. The company says the AP300 leverages AP1000 operating experience, tens of millions of engineering hours, and more than 70 years of nuclear technology experience. This is a powerful commercial message for utilities and public agencies that want modular deployment without taking unnecessary first-of-a-kind technology risk.

Westinghouse's strategic relevance also increased after its partnership with Brookfield, Cameco, and the U.S. Government, under which at least US$80 billion of new reactors are expected to be constructed across the United States using AP1000 and AP300 technology. For SMR buyers, this matters because it ties AP300 deployment to a broader U.S. nuclear industrial-base rebuild, not a standalone reactor marketing campaign.

GE Vernova Hitachi Nuclear Energy

GE Vernova Hitachi is the leading commercial reference case through the BWRX-300. GE Vernova states that construction began in May 2025 at Ontario's Darlington New Nuclear Project and that the first unit is scheduled to be operational in 2030, delivering 300 MW of low-carbon baseload power. The company also says the BWRX-300 can reduce plant site size by about 90% and use about 50% less concrete per unit of energy produced compared with conventional designs.

GE Vernova's 2025 annual report highlights US$38 billion in revenue, US$59 billion in orders, and US$150 billion in backlog, giving the company a strong industrial base behind its nuclear ambitions. This matters in SMRs because buyers will favor vendors that can combine reactor technology, project delivery discipline, services, and supply-chain scale.

Rolls-Royce SMR / Rolls-Royce Holdings plc

Rolls-Royce SMR is becoming one of Europe's clearest SMR commercialization stories. Rolls-Royce confirmed in April 2026 that Rolls-Royce SMR signed a contract with Great British Energy - Nuclear to support the design and delivery of the first SMRs in the UK. The company also noted that the UK program provides certainty for site-specific design activity, site-build preparation at Wylfa, and long lead-time equipment orders.

The parent company's 2025 full-year results show a stronger financial platform behind the SMR effort. Rolls-Royce reported £3.5 billion in underlying operating profit, £3.3 billion in free cash flow, and upgraded mid-term guidance. For SMR customers, this strengthens confidence that Rolls-Royce can support a long-cycle nuclear deployment program requiring engineering depth, manufacturing discipline, and sustained balance-sheet capacity.

NuScale Power Corporation

NuScale's main advantage is regulatory positioning. The company states that it remains the first and only SMR technology to have received U.S. NRC design approval, including its uprated 77 MWe NuScale Power Module. NuScale is targeting use cases including electricity generation, data centers, district heating, desalination, commercial-scale hydrogen production, and process heat.

NuScale reported US$31.5 million in 2025 revenue and ended the year with US$1.3 billion in cash, cash equivalents, and short- and long-term investments. It also highlighted commercialization activity with ENTRA1 and TVA, including a nonbinding collaborative agreement to deploy up to 6 GW of NuScale SMR capacity across TVA's seven-state service region.

Purchase Corporate License | Market Intelligence: https://www.datamintelligence.com/buy-now-page?report=small-modular-reactor-market?kailas

Analyst Views

The SMR market is entering a more commercial and less speculative phase. The strongest lead-generation message is not that SMRs are compact; it is that they can provide firm, low-carbon, site-flexible power for utilities, AI data centers, industrial clusters, desalination facilities, hydrogen projects, and remote energy users.

The most bankable near-term opportunities are grid-connected light-water SMRs backed by utilities and public funding. The highest-upside opportunities are multi-module plants for data centers and industrial heat. The hardest challenge will be execution: licensing timelines, first-of-a-kind construction cost, fuel availability, community acceptance, EPC capacity, and long-term power purchase structures.

Key players shaping the market include Westinghouse Electric, NuScale Power, Rolls-Royce plc, GE Vernova, Hitachi Nuclear Energy, Terrestrial Energy, Holtec International, X-energy, Moltex Energy, Framatome, and KEPCO Engineering & Construction Company, Inc.

The projected rise from US$6.42 billion in 2025 to US$12.24 billion by 2033 should be read as a signal that SMRs are moving into the center of energy-security planning. The winners will be companies that can convert reactor design into a complete commercial ecosystem: licensed technology, credible EPC partners, fuel access, utility or data-center off-take, public-agency support, and repeatable construction.

Contact:

Fabian

DataM Intelligence 4market Research LLP

6th Floor, M2 Tech Hub, DataM Intelligence 4market Research LLP, Lalitha Nagar, Habsiguda, Secunderabad, Hyderabad, Telangana 500039

USA: +1 877-441-4866

UK: +44 161-870-5507

Email: fabian@datamintelligence.com

About DataM Intelligence

DataM Intelligence is a renowned provider of market research, delivering deep insights through pricing analysis, market share breakdowns, and competitive intelligence. The company specializes in strategic reports that guide businesses in high-growth sectors such as nutraceuticals and AI-driven health innovations.

To find out more, visit https://www.datamintelligence.com/ or follow us on Twitter, LinkedIn and Facebook.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Small Modular Reactor Market to Add US$5.82 Billion by 2033 as AI Data Centers, Energy Security and Firm Low-Carbon Power Pull Utilities, EPCs and Reactor Vendors Into Commercial Deployment here

News-ID: 4512449 • Views: …

More Releases from DataM intelligence 4 Market Research LLP

VR/AR Technology for Healthcare Market to Add US$11.31 Billion by 2033 as Surgic …

NEW YORK, May 13, 2026 - The global VR/AR Technology for Healthcare Market reached US$5.03 billion in 2025 and is expected to reach US$16.34 billion by 2033, growing at a CAGR of 15.8% during 2026-2033, according to the supplied market model. The forecast represents an additional US$11.31 billion in annual market value by 2033, supported by clinical demand for surgical visualization, provider training, rehabilitation, pain management, remote care, diagnostics support,…

3D Printed Organ Market to Add US$4.84 Billion by 2033 as Organ Shortage, Biofab …

NEW YORK, May 13, 2026 - The global 3D Printed Organ Market reached US$3.06 billion in 2025 and is expected to reach US$7.90 billion by 2033, growing at a CAGR of 12.6% during 2026-2033, according to the supplied market model. The forecast represents an additional US$4.84 billion in annual market value by 2033, supported by organ-shortage pressure, personalized medicine, tissue engineering, organ-on-chip spillovers, biofabrication advances, drug-discovery demand, and rising investment…

Open Radio Access Networks Market to Expand 15.7x from US$2.92 Billion in 2024 t …

NEW YORK, May 13, 2026 - The global O-RAN (Open Radio Access Networks) market reached US$2.92 billion in 2024 and is expected to reach US$45.70 billion by 2032, growing at a CAGR of 41.03% during 2025-2032, according to DataM Intelligence research. The forecast implies an additional US$42.78 billion in annual market value by 2032, driven by telecom operators' move away from closed radio access systems toward open interfaces, multivendor radio…

Smart Glasses Market to Rise from US$1,047.44 Million in 2025 to US$2,826.15 Mil …

NEW YORK, May 13, 2026 - The global smart glasses market reached US$1,047.44 million in 2025 and is expected to reach US$2,826.15 million by 2033, expanding at a CAGR of 13.21% during 2026-2033, according to the supplied market model. The forecast implies an additional US$1.78 billion in annual market value by 2033, driven by a new buying cycle around hands-free AI, live captions, real-time translation, private messaging, contextual displays, prescription-ready…

More Releases for SMR

https://www.epressrelease.org/roofing-market-size-growth-trends-2021-by-smr/

The report covers forecast and analysis for the Roofing market on a global and regional level. The study provides historic data of 2015 along with a forecast from 2016 to 2021 based on volume and revenue (USD Million). The study includes drivers and restraints for the market along with the impact they have on the demand over the forecast period. Additionally, the report includes study of opportunities available in the…

Lymphoma Treatment Market size, Growth, Trends 2020 by SMR

Lymphoma is a type of cancer that starts from lymphametic cells which are part of immune system. The lymph system helps body to fight infection and disease. There are two main types of lymphoma such as hodgkin lymphoma and non-hodgkin lymphoma (NHL). These cells are present in the spleen, lymph nodes, bone marrow, thymus, and among other parts of the body. Lymphoma can occur in both children and adults. Lymphoma…

SMR : Global Ethoxylates Market Analysis,share, size, trends 2020

Ethoxylates is a compound obtained from a conduct in which ethylene oxide added to alcohols and phenols. Production of detergents, surface cleaners, cosmetics, and paints mainly involve ethoxylates compound as intermediate. Major end application of ethoxylates includes textile processing, paints & coatings, agriculture, pulp & paper, and personal care industries.

Growing textile processing, personal care, and paints & coatings industries is major driving factor of ethoxylates market. Cosmetic & personal…

Global Barrier Materials Market share, size, trends 2020 by SMR

Barrier material is an enclosure material designed to stop means of access of gases, liquids, or radiation. Barrier materials market has witnessed a significant growth in the recent years, which is projected to continue in the years to come. Barrier materials market exhibit enormous opportunities for industry participants. Supply-demand gap in raw materials and protection against counterfeit products are the major challenges in the barrier materials market.

The report provides a…

SMR Automotive Services Selects IQS for Global Quality Standardization

July 15, 2011 | Cleveland, OH – IQS, a leader of enterprise compliance and quality management software announced today that customer SMR Automotive Services, a member of Samvardhana Motherson Group, one of the world’s largest manufacturers of external rearview mirrors for passenger cars, will deploy IQS’ web-based solution throughout all of its manufacturing sites worldwide to centralize quality operations and improve efficiency.

SMR manufactures exterior and interior mirrors and blind…

SMR Bathrooms Offer Next Day Delivery On Colosseum Radiators

Portsmouth, United Kingdom (10 December, 2010) – SMR Bathrooms, a leading UK supplier of bathrooms and bathroom accessories, can give next day delivery on Ultra Colosseum radiators to any UK address.

SMR Bathrooms stock Colosseum column radiators in a variety of styles and sizes to suit different locations, such as a smaller one for a downstairs bathroom or a larger one for a main bathroom. Produced by Ultra, all of…