Press release

Polyether Polyol Production Plant DPR 2026: Investment Cost, Market Growth & ROI

Market Overview and Growth Potential:

The global polyether polyol market size was valued at USD 18.53 Billion in 2025. According to IMARC Group estimates, the market is expected to reach USD 29.24 Billion by 2034, exhibiting a CAGR of 5.2% from 2026 to 2034. The polyether polyol market is driven by the growing trend towards sustainable and eco-friendly materials that has led to an increased focus on bio-based polyether polyols.

Request for Sample Report: https://www.imarcgroup.com/polyether-polyol-manufacturing-plant-project-report/requestsample

The polyether polyol market is poised for steady growth driven by its widespread use in the production of flexible and rigid foams, which are essential in industries like automotive, construction, and furniture. Rising demand for polyurethane foams, particularly in the automotive and construction sectors, is a key factor propelling market expansion. Additionally, the need for energy-efficient buildings and the growing demand for insulation materials are further supporting the industry's growth. The residential construction sector, which expanded at 6.8% during FY2024-25, is projected to reach USD 350 Billion by 2030, as per industrial reports. Advancements in production technologies and the increasing shift towards low-emission and low-VOC products are likely to shape the future of the market. The polyether polyol market is expected to experience a robust upward trajectory, with a compound annual growth rate in the forecast period.

Polyether polyol is a versatile organic polymer, primarily used as a key raw material in the production of polyurethane foams, coatings, and elastomers. Produced through the polymerization of cyclic ethers like propylene oxide (PO) or ethylene oxide (EO) with initiators, these compounds contain multiple hydroxyl (-OH) functional groups and ether bonds (C-O-C) in their backbone. They are valued for their excellent hydrolytic stability (resistance to moisture degradation), superior low-temperature flexibility, and low viscosity compared to polyester polyols. Polyether polyols are indispensable in manufacturing flexible cushioning (furniture, automotive seats), rigid insulation for construction, and high-performance CASE (Coatings, Adhesives, Sealants, Elastomers) applications. They are generally preferred for products needing high resilience and moisture resistance.

Plant Capacity and Production Scale:

The proposed polyether polyol production facility is designed with an annual production capacity of 300,000 tons, enabling economies of scale while maintaining operational flexibility across product grades flexible foam polyols (standard and high-resilience grades), rigid foam polyols, CASE polyols, and specialty bio-based polyols for construction, automotive, furnishings, bedding, footwear, industrial coatings, adhesives, sealants, and elastomers end-use applications. This large-scale production capacity supports efficient alkoxylation, purification, and blending operations serving both large-volume flexible foam, rigid foam, and automotive polyurethane customers requiring continuous supply of specification-grade standard polyether polyols, and premium CASE, specialty, and bio-based polyol customers requiring tightly controlled hydroxyl number, functionality, molecular weight, and viscosity specification compliance.

Speak to an Analyst for Customized Report: https://www.imarcgroup.com/request?type=report&id=11574&flag=C

Financial Viability and Profitability Analysis:

The polyether polyol production business demonstrates healthy profitability potential under normal operating conditions. The financial projections reveal:

• Gross Profit: 25-35%

• Net Profit: 12-18%

These margins reflect the specialty petrochemical polymerization nature of polyether polyol production, where propylene oxide, ethylene oxide, and initiators are transformed through precision alkoxylation polymerization, purification, and blending into specification-grade polyether polyols meeting the hydroxyl number, functionality, molecular weight, viscosity, and purity requirements of flexible foam, rigid foam, automotive, CASE, and specialty polyurethane customers. Margins are supported by polyether polyols' fundamental and irreplaceable role as core raw materials across diverse polyurethane applications; rising energy-efficient building and insulation demand driving rigid polyol consumption; automotive lightweight materials adoption and EV interior production driving flexible and structural polyol demand; residential construction sector projected to reach USD 350 Billion by 2030 supporting foam and panel demand; growing trend toward bio-based and low-emission polyols creating premium product development opportunities; and regional supply chain reliability preferences of polyurethane formulators and OEMs. The November 2025 Monument Poly-CO2 launch the first U.S.-based production of polyols from renewable carbon replacing fossil feedstocks with captured CO2 and reducing global warming potential by 20-30% demonstrates the compelling innovation direction and premium pricing potential of sustainable polyol products. Propylene oxide procurement cost management is the primary raw material cost variable impacting margin performance.

Cost of Setting Up a Polyether Polyol Production Plant:

Operating Cost Structure:

The cost structure for a polyether polyol production plant is primarily driven by:

• Raw Materials: 65-75% of total OpEx particularly propylene oxide, which accounts for the largest share of raw material costs, along with ethylene oxide and glycerol/sucrose

• Utilities: 10-15% of OpEx

• Other Expenses: Including transportation, packaging, salaries and wages, depreciation, taxes, and other expenses

Raw materials - particularly propylene oxide (the primary alkylene oxide monomer accounting for the majority of polyether polyol chain carbon atoms and the dominant raw material cost for most commercial polyether polyol grades), along with ethylene oxide (for EO-tipped or high-EO content polyols for flexible foam and CASE applications), and initiators (glycerol, sucrose, sorbitol, propylene glycol, or amine initiators for varying polyol functionality and molecular weight) account for approximately 65-75% of total operating expenses, making propylene oxide procurement strategy, supplier qualification, and long-term supply contract management the central raw material cost management priority. Propylene oxide purity, consistent feed quality, and polymerization reaction control directly determine polyol molecular weight, hydroxyl number, functionality distribution, and product grade compliance. Utilities represent 10-15% of OpEx, driven by the energy requirements of pressurized alkoxylation reactor temperature control, vacuum stripping and purification operations, and catalyst handling systems. In the first year of operations, costs cover raw materials, utilities, depreciation, taxes, packing, transportation, and repairs and maintenance. By the fifth year, the total operational cost is expected to increase substantially due to factors such as inflation, market fluctuations, and potential rises in the cost of key materials.

Capital Investment Requirements:

Setting up a polyether polyol production plant requires significant capital investment across propylene oxide and ethylene oxide monomer storage, alkoxylation reactors, catalyst systems, vacuum stripping columns, filtration units, neutralization tanks, stabilizer blending systems, and packaging infrastructure. The total capital investment depends on plant capacity, technology, and location, covering land acquisition, site preparation, and necessary infrastructure. Machinery costs account for the largest portion of the total capital expenditure, while the cost of land and site development forms a substantial part of the overall investment.

Land and Site Development: The location must offer easy access to key raw materials such as propylene oxide, ethylene oxide, and glycerol/sucrose. Proximity to propylene oxide supply ideally through pipeline connection to a propylene oxide production complex offers significant feedstock cost and logistics advantage. The site must have robust infrastructure, including reliable transportation, utilities, and waste management systems. Compliance with local zoning laws and environmental regulations governing flammable alkylene oxide handling and storage must also be ensured.

Machinery and Equipment: High-quality, corrosion-resistant machinery tailored for polyether polyol production must be selected. Essential equipment includes:

• Reactors - pressure-rated stainless steel batch or continuous alkoxylation reactors for controlled ring-opening polymerization of propylene oxide and/or ethylene oxide onto initiator molecules in the presence of alkali metal hydroxide (KOH or DMC catalyst) at specification temperature and pressure, with precise alkylene oxide feed rate control, temperature management through jacket cooling, and inert nitrogen atmosphere management for specification polyol molecular weight, hydroxyl number, and functionality distribution production

• Vacuum dryers - vacuum thin-film or flash evaporation stripping systems for removing residual unreacted propylene oxide, ethylene oxide, water, and volatile impurities from crude polyol product under controlled vacuum and temperature conditions, achieving specification residual monomer content and moisture level in the finished polyether polyol product

• Filtration units - depth filtration or membrane filtration systems for removing catalyst residues (potassium hydroxide neutralization salts, DMC catalyst particles), color bodies, and suspended impurities from the stripped polyol stream, achieving specification color (APHA/Hazen), filtrate clarity, and residual catalyst content in the finished food-contact-compatible or CASE-grade polyether polyol

• Alkoxylation vessels - initiator charging, mixing, and pre-reaction vessels for preparing and conditioning initiator solutions (glycerol, sucrose, propylene glycol, or amine initiator dissolved in small-molecule starter polyol) before charging to the main alkoxylation reactor, with catalyst addition and activation management for consistent polymerization initiation and molecular weight control in each polyol production batch

• Neutralization tanks - controlled acid addition and mixing systems for neutralizing residual alkaline catalyst (KOH) in the crude polyol after alkoxylation, using phosphoric acid, lactic acid, or other specification neutralizing agents to precipitate or deactivate catalyst, with pH control management for specification catalyst-neutralized product before filtration and stripping operations

• Stripping columns - vacuum distillation or steam stripping columns for continuous or batch removal of residual cyclic oligomers, volatile impurities, and residual alkylene oxide from the polyol product stream, with reflux and bottoms composition monitoring for specification residual monomer, volatile organic compound, and oligomer content compliance in finished polyether polyol grades

• Stabilizer blending systems - controlled addition and mixing systems for incorporating specification antioxidant stabilizer packages (hindered phenolic or phosphite antioxidants), anti-yellowing agents, and processing additives into the finished purified polyether polyol to achieve specification storage stability, color retention, and performance consistency in packaged and distributed product

• Packaging machines - automated filling systems for specification-grade polyether polyol into bulk isotank containers, flexi-tanks, HDPE drums, or IBC totes with accurate gravimetric fill control, nitrogen blanket atmosphere for oxidation protection, hermetic sealing, and full product grade identification, specification, lot traceability labeling, safety data sheet, and technical data sheet documentation for polyurethane foam producer and CASE formulator customer dispatch

All equipment must comply with applicable pressure vessel codes and standards for alkylene oxide service (ASME, PED), flammable liquid and gas handling safety regulations for propylene oxide and ethylene oxide, and applicable environmental regulations for alkylene oxide emissions management. Polyether polyol manufacturing requires controlled polymerization processes, specialized reactors, catalyst handling, quality consistency, and strict safety standards.

Civil Works: Building construction and plant layout with separate designated areas for propylene oxide and ethylene oxide bulk storage (explosion-proof classified zone), initiator and catalyst preparation, alkoxylation reactor building, vacuum stripping and purification, filtration and neutralization, stabilizer blending, quality control laboratory, bulk storage tanks, and packaging and dispatch. Comprehensive alkylene oxide leak detection, explosion-proof electrical classification throughout PO and EO handling zones, emergency depressurization and flare systems, and alkylene oxide emergency scrubber systems must be incorporated.

Other Capital Costs: Costs associated with land acquisition, construction, and utilities including electricity, cooling water, steam, and nitrogen must be considered in the financial plan. Pre-operative expenses include chemical plant operating permits for alkylene oxide handling, environmental regulatory approvals for PO and EO emissions management, PSM program development and HAZOP study for alkylene oxide hazard management, quality control laboratory instrument procurement (hydroxyl number titration, viscometer, GPC molecular weight, GC residual monomer), and operator alkoxylation process safety and polyol quality training programs.

Buy Now: https://www.imarcgroup.com/checkout?id=11574&method=2175

Major Applications and Market Segments:

Polyether polyol production outputs serve critical cushioning, insulation, structural bonding, sealing, and coating functions across global construction, automotive, furnishings, refrigeration, and industrial sectors:

Flexible Polyurethane Foams: Polyether polyols are used in mattresses, furniture cushioning, automotive seating, and carpet underlay. The residential construction sector projected to reach USD 350 Billion by 2030 alongside growing consumer spending on premium furniture, bedding, and automotive comfort products provides sustained and expanding demand for flexible polyether polyols in high-resilience and viscoelastic foam applications across furniture, bedding, and automotive seating markets.

Rigid Polyurethane Foams: Polyether polyols are applied in thermal insulation for buildings, refrigerators, and cold storage systems. Growing demand for energy-efficient buildings and the need for insulation materials are key drivers supporting rigid polyol consumption, with increasingly stringent building energy efficiency regulations in major construction markets mandating higher insulation R-values that drive expanding rigid polyurethane spray foam and panel insulation adoption across residential, commercial, and industrial construction.

Coatings, Adhesives, Sealants, and Elastomers (CASE): Polyether polyols are used in protective coatings, industrial adhesives, sealants, and durable elastomeric products. The CASE segment provides premium-margin specialty polyol applications with stringent performance requirements in industrial protective coatings, structural adhesives, building sealants, and elastomeric molded parts, with the shift toward low-VOC and waterborne formulations driving increased adoption of polyether-based CASE chemistry.

Automotive Components: Polyether polyols are utilized in interior parts, insulation materials, and lightweight structural components. Growing automotive lightweighting requirements for fuel efficiency and EV range extension, combined with interior NVH (noise, vibration, harshness) performance requirements, drive consistent demand for automotive-grade flexible, semi-rigid, and rigid polyether polyols in seat cushioning, headliners, dashboards, and structural foam components.

Why Invest in Polyether Polyol Production?

Several compelling strategic and commercial factors make polyether polyol production an attractive investment:

Crucial Chemical Building Block: Polyether polyols are fundamental raw materials used in the production of polyurethane foams, coatings, adhesives, sealants, and elastomers across construction, automotive, furniture, refrigeration, and packaging positioning them as a core input for modern manufacturing and insulation technologies with non-discretionary demand across multiple critical industrial sectors.

Moderate but Justifiable Entry Barriers: Polyether polyol manufacturing requires controlled polymerization processes, specialized reactors, catalyst handling, quality consistency, and strict safety standards. Long-term approvals from polyurethane formulators and OEM-linked industries create barriers that favor technically capable, reliable producers rewarding investment in process safety, product quality consistency, and customer qualification programs with defensible market positions.

Megatrend Alignment: Rising demand for energy-efficient buildings, lightweight automotive materials, electric vehicles, cold-chain logistics, and consumer comfort products is driving sustained growth in polyurethane consumption where polyether polyols play a central role. The residential construction sector projected to reach USD 350 Billion by 2030 and the automotive sector's EV transition both represent large structural demand growth drivers for polyether polyols over the long term.

Policy and Infrastructure Push: Government initiatives supporting energy-efficient construction, refrigeration infrastructure, housing development, automotive manufacturing, and domestic chemical production indirectly boost demand for polyether polyols used in insulation foams, panels, and industrial materials. The November 2025 Monument Poly-CO2 launch using Econic Technologies' process replacing fossil feedstocks with captured CO2 and reducing global warming potential by 20-30% demonstrates the policy-aligned innovation direction driving premium product development in sustainable polyol technology.

Localization and Supply Chain Reliability: Polyurethane foam manufacturers increasingly prefer dependable regional suppliers of polyether polyols to reduce import dependence, manage feedstock price volatility, shorten lead times, and ensure consistent quality creating strong commercial incentives for EPC contractors, foam producers, and OEMs to source from proximate, quality-certified regional polyether polyol producers.

Manufacturing Process Excellence:

The polyether polyol production process involves alkoxylation, purification, and blending. The main production steps include:

• Raw material receiving and quality inspection - receipt, storage, and quality verification of propylene oxide, ethylene oxide, and initiators (glycerol, sucrose, sorbitol, propylene glycol, or amine initiators) for purity, water content, inhibitor levels, and specification compliance, with full material lot traceability and alkylene oxide pressure system safety management including leak detection, emergency pressure relief, and explosion-proof electrical classification in PO and EO storage and feed areas

• Initiator and catalyst preparation - preparation of specification initiator starter polyol through initial propoxylation of initiator molecule to target starter molecular weight in alkoxylation vessels, and preparation of alkali metal hydroxide catalyst solution (KOH in water or propylene glycol) or DMC catalyst slurry at specification concentration for addition to the main alkoxylation reactor

• Alkoxylation polymerization - controlled batch or semi-continuous ring-opening polymerization of propylene oxide and/or ethylene oxide onto initiator molecules in pressurized reactors at specification temperature (80-130°C), pressure, and alkylene oxide feed rate, with catalyst management and continuous reaction progress monitoring for specification polyol hydroxyl number, molecular weight, and EO/PO composition distribution targeting

• Vacuum stripping and devolatilization - controlled vacuum or steam stripping of finished alkoxylation reactor product in stripping columns to remove residual unreacted propylene oxide, ethylene oxide, water, and volatile cyclic oligomers to specification residual content levels, protecting downstream catalyst neutralization and product quality

• Catalyst neutralization - controlled addition of specification acid neutralizing agent to stripped polyol in neutralization tanks to deactivate and precipitate residual KOH catalyst as insoluble salt, with pH monitoring and neutralization end-point control for specification catalyst-neutral product before filtration

• Filtration and purification - pressure or vacuum filtration of neutralized polyol through specification filter media in filtration units to remove precipitated catalyst salts, color bodies, and suspended impurities, achieving specification color (APHA), clarity, and catalyst residue content for foam-grade and CASE-grade polyether polyol products

• Stabilizer blending - controlled incorporation of specification antioxidant and anti-yellowing stabilizer package into the filtered polyether polyol in stabilizer blending systems, achieving specification storage stability and color retention performance in finished packaged polyol product during distribution and customer storage

• Quality testing - comprehensive analytical testing of finished polyether polyol for hydroxyl number (mg KOH/g), acid number, water content (Karl Fischer), viscosity (Brookfield), color (APHA/Hazen), residual alkylene oxide (GC headspace), and molecular weight distribution (GPC) against specification grade requirements, with full batch documentation for certificate of analysis and customer technical data sheet compliance

• Packaging and dispatch - automated filling of specification-grade polyether polyol into bulk isotanks, flexi-tanks, IBC totes, or HDPE drums using packaging machines under nitrogen blanket atmosphere for oxidation protection, with accurate gravimetric fill control, full product grade identification, hydroxyl number specification, viscosity, lot traceability labeling, safety data sheet, and technical data sheet documentation for polyurethane foam producer and CASE formulator customer dispatch

Advanced process control systems, alkylene oxide safety management, and quality management systems are implemented throughout all production stages. PSM documentation, environmental monitoring records for alkylene oxide emissions, and full product traceability are maintained throughout all manufacturing stages for chemical plant regulatory compliance.

Industry Leadership:

Leading producers in the global polyether polyol industry include several multinational companies with extensive production capacities and diverse application portfolios. Key players include:

• Dow

• Covestro AG

• BASF SE

• Shell Chemicals

• Wanhua Chemical Group

These companies serve end-use sectors such as construction, automotive, furnishings, bedding, footwear, industrial coatings, adhesives, sealants, and elastomers, with leading producers investing continuously in alkoxylation catalyst technology (DMC catalyst for narrow molecular weight distribution), bio-based polyol development, low-VOC CASE polyol innovation, and regional production capacity expansion to meet the evolving performance, sustainability, and supply reliability requirements of global polyurethane customers.

Recent Industry Developments:

November 2025: Monument launched Poly-CO2, the first US-based production of polyols from renewable carbon at its manufacturing facility in Brandenburg, KY. The new product line of polycarbonate ether (PCE) polyols is based on a process from Econic Technologies that replaces fossil-based feedstocks with captured CO2 and reduces global warming potential by 20-30%.

Browse Full Report: https://www.imarcgroup.com/polyether-polyol-manufacturing-plant-project-report

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company excels in understanding its client's business priorities and delivering tailored solutions that drive meaningful outcomes. We provide a comprehensive suite of market entry and expansion services. Our offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape, and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: (+1-201-971-6302)

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Polyether Polyol Production Plant DPR 2026: Investment Cost, Market Growth & ROI here

News-ID: 4512446 • Views: …

More Releases from IMARC Group

Water Tank Manufacturing Plant DPR & Unit Setup - 2026: Machinery Cost, CapEx/Op …

Setting up a water tank manufacturing plant positions investors in one of the most essential and structurally growing segments of the global water storage infrastructure and construction materials industry a market driven by increasing demand for reliable water storage infrastructure, rapid urbanization, rising construction activities, and government initiatives for water conservation and supply management. The large and continuously expanding global base of residential homebuilders, commercial property developers, agricultural operators, municipal…

Hydrochloric Acid Production Plant DPR & Unit Setup - 2026: Demand Analysis and …

Setting up a hydrochloric acid production plant positions investors at a critical junction of the global inorganic acids and industrial chemicals supply chain one of the most broadly applied and consistently demanded foundational chemical sectors driven by the foundational role of hydrochloric acid as an irreplaceable strong mineral acid across steel and metal pickling, pH adjustment and neutralization, chemical synthesis, water treatment, food processing, and pharmaceutical manufacturing applications, sustained demand…

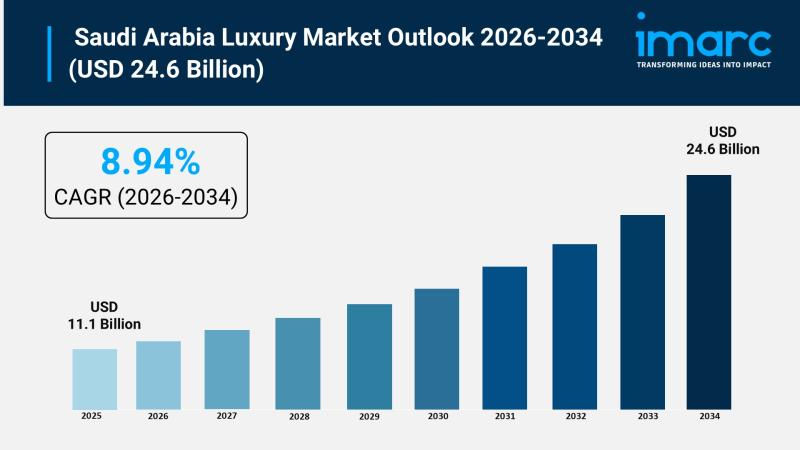

Saudi Arabia Luxury Market Size to Surpass USD 24.6 Billion by 2034, at a CAGR o …

Saudi Arabia Luxury Market Overview

Market Size in 2025: USD 11.1 Billion

Market Size in 2034: USD 24.6 Billion

Market Growth Rate 2026-2034: 8.94%

According to IMARC Group's latest research publication, "Saudi Arabia Luxury Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2026-2034", The Saudi Arabia luxury market size was valued at USD 11.1 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 24.6 Billion by 2034, exhibiting a…

Agrochemicals Production Plant Cost DPR 2026: Capital Investment, Process Flow, …

Setting up an agrochemicals production plant offers investors a strategic opportunity in the agricultural and specialty chemicals sector, as agrochemicals-including fertilizers, pesticides, herbicides, fungicides, insecticides, plant growth regulators, and micronutrients-play a vital role in improving crop productivity and protecting agricultural output from pests, diseases, and nutrient deficiencies; driven by rising global food demand, shrinking arable land availability, and the need for higher farming efficiency, agrochemical products remain essential for modern…

More Releases for Polyether

Global Polyether Polyamine Market Outlook Report 2025

On Nov 5, 2025, Global Info Research released a research report titled "Global Polyether Polyamine Market 2025 by Manufacturers, Regions, Type and Application, Forecast to 2031". This report provides detailed data analysis of the Polyether Polyamine market from 2020 to 2031. Including the market size and development trends of Polyether Polyamine Market, it analyzes market size indicators such as sales, sales volume, average price and CAGR, it also…

Polyether Polyols Market Trends, Demand, and Forecast 2034

The polyether polyols market is projected to reach $12 billion in 2024 and grow to $25 billion by 2034, with a CAGR of 7.5% from 2025-2034.

On March 7, 2025, Exactitude Consultancy., Ltd. released a research report titled "Polyether Polyols Market "evaluation provides information on the major business trends that will impact the market's growth between 2025 and 2034. It provides information on the fundamental business strategies used in this market.…

Global Polyether Polyamine Market Forecast 2023-2028 Under Inflation

Polyether Polyamine is a kind of polyepoxy alkane compounds terminated by primary amidogen or secondary amidogen; and the molecular framework is polyether and the reactive group is terminal amidogen.

Different market evaluation and appropriate data techniques are often used to compile and evaluate the data which is offered in this Polyether Polyamine market report. In addition, we have an in-house information prediction model that forecasts product demand until 2028. This market…

Polyether Acrylate Market 2022 | Detailed Report

The Polyether Acrylate research report combines vital data incorporating the competitive landscape, global, regional, and country-specific market size, market growth analysis, market share, recent developments, and market growth in segmentation. Furthermore, the Polyether Acrylate research report offers information and thoughtful facts like share, revenue, historical data, and global market share. It also highlights vital aspects like opportunities, driving, product scope, market overview, and driving force.

Download FREE Sample Report @ https://www.reportsnreports.com/contacts/requestsample.aspx?name=5390073…

Amino Terminated Polyether Market Size, Share, Development by 2024

Global Info Research offers a latest published report on Amino Terminated Polyether Market Analysis and Forecast 2019-2025 delivering key insights and providing a competitive advantage to clients through a detailed report. This report focuses on the key global Amino Terminated Polyether players, to define, describe and analyze the value, market share, market competition landscape, SWOT analysis and development plans in next few years.

To analyze the Amino Terminated Polyether with respect…

Polyether Polyols Market Size, Share, Development by 2024

Global Info Research offers a latest published report on Polyether Polyols Market Analysis and Forecast 2019-2025 delivering key insights and providing a competitive advantage to clients through a detailed report. This report focuses on the key global Polyether Polyols players, to define, describe and analyze the value, market share, market competition landscape, SWOT analysis and development plans in next few years.

To analyze the Polyether Polyols with respect to individual growth…