Press release

Australia Consumer Credit Market 2026 | Worth USD 481.6 Million by 2034

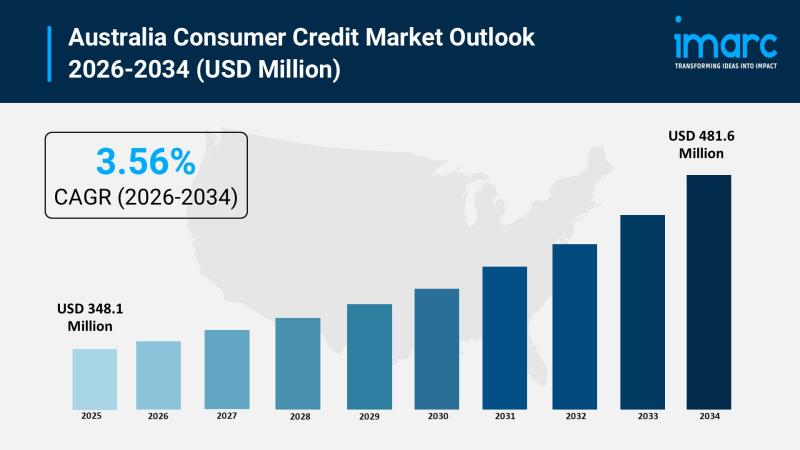

The Australia consumer credit market size reached USD 348.1 Million in 2025. Looking forward, the market is expected to reach USD 481.6 Million by 2034, exhibiting a growth rate (CAGR) of 3.56% during 2026-2034. The market encompasses revolving credits and non-revolving credits delivered through credit services and software and IT support services issued by banks and finance companies, credit unions, and other institutions via direct deposit, debit card, and other payment methods across Australia Capital Territory and New South Wales, Victoria and Tasmania, Queensland, Northern Territory and Southern Australia, and Western Australia. The Reserve Bank of Australia's first interest rate cut in February 2025 reducing the cash rate to 4.1%, BNPL providers including Afterpay and Zip becoming subject to the National Consumer Credit Protection Act from June 2025, the Consumer Data Right (CDR) expansion to non-bank lenders effective mid-2026, Australia's BNPL market reaching USD 19.50 billion in 2025, and rising fintech innovation transforming digital lending across the country are among the key factors shaping the market throughout the forecast period.

Request for a sample report PDF: https://www.imarcgroup.com/australia-consumer-credit-market/requestsample

Australia Consumer Credit Market Summary:

• The Reserve Bank of Australia issued its first interest rate cut in February 2025 after 13 consecutive hikes, reducing the cash rate to 4.1%-signaling a shift in monetary policy that is expected to ease borrowing costs for consumers across mortgages, personal loans, and credit card products, potentially stimulating credit demand as households benefit from reduced repayment burdens and improved confidence in taking on new credit commitments.

• Buy Now Pay Later (BNPL) providers became subject to the National Consumer Credit Protection Act from 10 June 2025, requiring platforms including Afterpay, Zip, and Humm to hold Australian Credit Licences, conduct credit checks, and comply with responsible lending obligations-fundamentally transforming the BNPL sector from an unregulated alternative into a formally supervised credit product, with Australia's BNPL market valued at USD 19.50 billion in 2025 and projected to reach USD 48.66 billion by 2031.

• The Australian government expanded the Consumer Data Right (CDR) to include non-bank lending institutions effective mid-2026, enabling consumers to securely share their financial data across a wider range of credit providers-fostering competition, driving personalized credit offerings, and empowering consumers to compare products more effectively while enabling fintech companies and non-bank lenders to develop innovative credit solutions tailored to diverse borrower profiles.

• ASIC launched a consultation in February 2025 on new regulatory guidance for BNPL providers under the Treasury Laws Amendment Act 2024, establishing modified responsible lending obligations, fee caps to limit excessive charges, electronic disclosure requirements, and unsuitability assessments ensuring credit offerings match consumers' financial situations-creating a regulatory framework that balances consumer protection with continued BNPL innovation and market growth.

• The Reserve Bank of Australia consulted on proposed changes to interchange fee caps in its July 2025 paper, with the preferred option reducing domestic credit card interchange from 0.8% to 0.3%-a potential shift that would reshape credit card economics, reduce merchant costs, and potentially alter consumer credit card reward programs while encouraging greater adoption of lower-cost payment alternatives including debit cards and direct deposit methods.

• Beforepay Group launched its first regulated personal loan under the National Consumer Credit Protection Act in October 2024, offering loans of USD 2,001 to USD 3,000 for up to three months using AI-driven risk models-demonstrating how fintech companies are expanding beyond wage advance products into formal consumer credit, leveraging technology-driven underwriting to serve consumers who may not qualify for traditional bank lending products.

• Market segmentation covers two credit types (revolving credits, non-revolving credits), two service types (credit services, software and IT support services), three issuers (banks and finance companies, credit unions, others), three payment methods (direct deposit, debit card, others), and five regions (Australia Capital Territory and New South Wales, Victoria and Tasmania, Queensland, Northern Territory and Southern Australia, Western Australia).

Key Trends Shaping the Australia Consumer Credit Market:

• BNPL regulation transforming alternative credit into supervised financial products: The formal regulation of BNPL providers under the National Consumer Credit Protection Act from June 2025 represents a watershed moment for Australia's consumer credit landscape, bringing platforms like Afterpay, Zip, and Humm under the same regulatory framework as traditional lenders. With Australia's BNPL market valued at USD 19.50 billion in 2025 and projected to reach USD 48.66 billion by 2031, the new requirements for credit licensing, responsible lending obligations, and credit checks are reshaping business models across the sector. Providers are adjusting by implementing more robust affordability assessments, transparent fee structures, and flexible repayment options that meet regulatory standards. While compliance costs may consolidate the market-favoring larger, well-capitalized providers-the reforms ultimately strengthen consumer trust in BNPL as a legitimate credit product, potentially expanding its addressable market beyond younger, lower-risk consumers to include mainstream borrowers who previously avoided unregulated credit alternatives.

• Open banking and CDR expansion driving personalized credit innovation: The expansion of Australia's Consumer Data Right to include non-bank lending institutions from mid-2026 is creating the foundation for a more competitive, consumer-centric credit market where borrowers can leverage their financial data to access better-tailored products. By enabling consumers to securely share transaction history, income patterns, and spending behavior with a broader range of lenders, the CDR reduces information asymmetry that traditionally favored incumbent banks. Fintech companies and non-bank lenders are using this data to develop AI-powered credit assessment models that evaluate borrowers beyond traditional credit scores-considering factors like rent payment history, utility bills, and digital transaction patterns. This data-driven approach particularly benefits younger Australians, recent migrants, and consumers rebuilding credit histories who may lack conventional credit records but demonstrate responsible financial behavior through alternative data, expanding financial inclusion while enabling lenders to offer competitively priced products matched to individual risk profiles.

• Digital-first lending and fintech disruption accelerating credit accessibility: Australia's tech-savvy population and supportive regulatory environment are driving rapid adoption of digital lending platforms that offer faster approvals, streamlined applications, and personalized credit products through mobile-first interfaces. Fintech companies like Beforepay-which launched its first regulated personal loan using AI-driven risk models-are demonstrating how technology-enabled underwriting can serve consumer segments traditionally underserved by major banks. Digital lenders are leveraging alternative data sources, machine learning algorithms, and automated verification processes to deliver loan decisions in minutes rather than days, reducing friction and expanding the addressable market for consumer credit. The emergence of embedded finance-where credit products are integrated directly into retail, travel, and lifestyle platforms at the point of purchase-is further blurring the boundary between commerce and lending, creating new credit distribution channels that reach consumers where they already shop and spend.

• Green credit products and sustainable finance gaining consumer traction: Australian consumers-particularly in environmentally progressive states like Victoria and the ACT-are increasingly seeking credit products that align with sustainability values, driving demand for green personal loans, energy-efficient home improvement financing, and electric vehicle credit. Lenders are responding by developing dedicated green loan products linked to state government incentives and rebates, making environmentally beneficial purchases more affordable while differentiating their credit offerings in an increasingly competitive market. The integration of Environmental, Social, and Governance (ESG) principles into consumer lending is creating a new product category where borrowers receive preferential rates for verified sustainable purchases-from rooftop solar installations to home battery systems and zero-emission vehicles. This sustainable finance trend aligns with Australia's broader climate targets and positions early-moving lenders to capture an expanding consumer segment that views environmental responsibility as a credit product selection criterion alongside interest rates and fees.

• Interchange fee reform reshaping credit card economics and consumer behavior: The RBA's July 2025 consultation proposing to reduce domestic credit card interchange caps from 0.8% to 0.3% signals a potential structural shift in Australia's credit card market that would significantly reduce the revenue available for card-linked reward programs. If implemented in 2026, lower interchange fees would reduce merchant costs but likely prompt issuers to restructure credit card products-potentially reducing rewards, adjusting annual fees, or introducing new fee structures to maintain profitability. This reform could accelerate the ongoing shift away from credit cards toward debit cards and alternative payment methods, while encouraging consumers to evaluate credit products based on interest rates and lending features rather than reward program generosity. For the broader consumer credit market, interchange reform may redirect consumer credit demand toward personal loans, lines of credit, and BNPL products that offer transparent pricing without the cross-subsidization dynamics inherent in interchange-funded reward systems.

Market Growth Drivers:

Digital Financial Services and Fintech Innovation Expanding Credit Access

Australia's position as one of the world's most digitally connected economies-with high smartphone penetration, widespread internet access, and a tech-savvy consumer population-creates an ideal environment for fintech-driven credit innovation that is expanding the addressable market for consumer lending. Digital lenders are using unconventional data sources, machine learning algorithms, and real-time verification to assess creditworthiness more accurately and efficiently than traditional scoring methods, enabling credit access for consumers who may lack extensive conventional credit histories. Beforepay's launch of its first regulated personal loan using AI-driven risk models demonstrates how technology companies are moving beyond niche products into mainstream consumer credit, while open banking reforms under the Consumer Data Right enable consumers to share financial data securely with competing lenders for better-tailored offers. The emergence of embedded finance-where credit is integrated at the point of purchase across retail, travel, and service platforms-is creating new distribution channels that reach consumers where they naturally transact. Australia's supportive regulatory framework, which balances consumer protection with innovation encouragement, has attracted significant fintech investment and enabled rapid product development that is transforming how Australians access, evaluate, and use consumer credit products.

Regulatory Reform Strengthening Consumer Protection and Market Confidence

Australia's proactive regulatory approach-including the formal regulation of BNPL providers under the National Consumer Credit Protection Act from June 2025, ASIC's enhanced oversight guidance, CDR expansion to non-bank lenders, and proposed interchange fee reforms-is building a more transparent and trustworthy consumer credit market that encourages responsible borrowing and lending. The BNPL reforms requiring credit licensing, responsible lending obligations, and affordability assessments address the consumer debt risks that previously constrained mainstream adoption, while fee caps and electronic disclosure requirements ensure transparent pricing. These regulatory improvements build consumer confidence in using credit products by ensuring that lenders-whether traditional banks, credit unions, or fintech platforms-are held to consistent standards of conduct and disclosure. The Australian Financial Complaints Authority (AFCA) provides an independent dispute resolution mechanism that gives consumers recourse without litigation, while mandatory hardship support obligations ensure borrowers facing financial difficulty receive assistance rather than punitive treatment. This comprehensive regulatory infrastructure positions Australia's consumer credit market for sustainable growth built on trust, transparency, and responsible lending practices.

Evolving Consumer Spending Patterns and Housing Market Dynamics

Shifting Australian lifestyles and spending patterns-driven by rising cost-of-living pressures in major cities, the RBA's February 2025 rate cut to 4.1% easing borrowing costs, and cultural preferences for flexible payment solutions-are creating sustained demand for diverse consumer credit products across income levels and demographics. The strong preference for BNPL among millennials and Gen Z consumers who favor shorter installment plans over traditional credit cards has driven the sector to USD 19.50 billion in 2025, while personal loans and lines of credit serve consumers financing travel, education, home renovations, and lifestyle purchases. Australia's property market continues driving credit demand through mortgage-linked products, home equity loans, and bridging finance-particularly as regional migration trends and remote working expand housing demand beyond traditional metropolitan centers into Brisbane, Perth, Canberra, and regional markets. The interplay between housing affordability challenges, lifestyle aspirations, and flexible credit solutions creates multi-dimensional demand that supports growth across revolving and non-revolving credit categories, with the February 2025 rate cut providing additional stimulus for consumers considering new credit commitments.

Browse the full report with TOC and list of figures: https://www.imarcgroup.com/australia-consumer-credit-market

How AI is Reshaping the Australia Consumer Credit Market:

• AI-powered credit scoring and alternative data assessment expanding financial inclusion: Machine learning models are analyzing transaction patterns, employment data, rental payment history, utility bills, and digital spending behavior to build comprehensive credit profiles that extend beyond traditional credit scores-enabling lenders to accurately assess borrowers who lack conventional credit histories, including young Australians, recent migrants, and consumers rebuilding their financial standing, while maintaining responsible lending obligations under ASIC's regulatory framework.

• AI-driven fraud detection and identity verification securing digital lending: Real-time AI algorithms are monitoring credit applications and transactions for fraudulent patterns, synthetic identity indicators, and anomalous behavior across digital lending platforms-enabling instant verification decisions that balance security with seamless customer experience, reducing approval times from days to minutes while detecting sophisticated fraud attempts that traditional rule-based systems miss in Australia's increasingly digital-first credit environment.

• AI-enhanced affordability assessments supporting responsible lending compliance: Automated AI systems are analyzing consumers' income, expenditure patterns, existing debt obligations, and financial commitments in real-time to conduct the affordability and unsuitability assessments required under the National Consumer Credit Protection Act-enabling BNPL providers and digital lenders to comply with responsible lending obligations at scale while processing thousands of applications simultaneously without manual underwriting delays.

• AI-powered personalized credit product matching and pricing optimization: Machine learning algorithms are analyzing consumer financial profiles, spending patterns, and credit behavior to dynamically match borrowers with optimal credit products and personalized interest rates-leveraging Consumer Data Right information to offer tailored credit solutions that reflect individual risk profiles, reducing information asymmetry between lenders and borrowers while enabling competitive pricing that drives consumer value in Australia's increasingly data-driven credit marketplace.

• AI-based early warning systems and hardship prediction for proactive borrower support: Predictive AI models are analyzing borrower payment patterns, spending changes, and financial stress indicators to identify consumers at risk of financial hardship before they miss payments-enabling lenders to proactively offer repayment modifications, hardship arrangements, and financial counseling referrals that prevent debt spirals and support the consumer protection objectives mandated by ASIC and the Australian Financial Complaints Authority.

Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Australia consumer credit market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on credit type, service type, issuer, and payment method.

By Credit Type:

• Revolving Credits

• Non-revolving Credits

By Service Type:

• Credit Services

• Software and IT Support Services

By Issuer:

• Banks and Finance Companies

• Credit Unions

• Others

By Payment Method:

• Direct Deposit

• Debit Card

• Others

By Region:

• Australia Capital Territory and New South Wales

• Victoria and Tasmania

• Queensland

• Northern Territory and Southern Australia

• Western Australia

Key Players:

The Australia consumer credit market features a competitive landscape comprising major banks, fintech disruptors, BNPL providers, and credit unions. The market research report provides a comprehensive analysis of the competitive landscape including key player positioning, market structure, top winning strategies, competitive dashboards, and detailed company profiles. Some of the major players include Commonwealth Bank of Australia, Westpac Banking Corporation, National Australia Bank, ANZ Group, Macquarie Group, Afterpay (Block Inc.), Zip Co., Humm Group, Latitude Financial Services, Beforepay Group, and other domestic and international participants competing across revolving credit, personal lending, BNPL, and digital credit platforms throughout Australia.

Key Aspects Required for the Australia Consumer Credit Market:

• Demand encompasses consumers seeking revolving credit products including credit cards and lines of credit for everyday spending flexibility, borrowers requiring non-revolving personal loans for major purchases and debt consolidation, BNPL users preferring installment-based payment solutions for retail purchases, homeowners accessing mortgage-linked credit for renovations and property costs, and underbanked regional and remote communities requiring accessible digital lending solutions.

• ACT and New South Wales dominate the market driven by Sydney's concentration of major banks, fintech headquarters, and the country's largest consumer spending base, while Victoria and Tasmania's Melbourne-centric economy and Queensland's growing Brisbane and Gold Coast markets represent significant demand centers-with Western Australia and NT and SA providing growth opportunities where regional and remote communities remain underserved by traditional banking infrastructure.

• The BNPL sector's transformation from unregulated alternative to formally supervised credit product under the National Consumer Credit Protection Act creates both compliance costs and market legitimization-requiring providers to invest in credit licensing, affordability assessment systems, and responsible lending infrastructure while gaining access to mainstream consumer segments that previously avoided unregulated credit alternatives.

• The Consumer Data Right expansion to non-bank lenders from mid-2026 represents a structural market transformation-enabling fintech companies and credit unions to compete with major banks on a more level data footing, requiring investment in secure data infrastructure, API integration, and AI-powered credit assessment capabilities that leverage consumer-permissioned financial data for personalized product development.

• High household debt levels, rising cost-of-living pressures in Sydney and Melbourne, and limited financial literacy among young consumers and culturally diverse communities represent persistent challenges-requiring coordinated investment in financial education, responsible lending practices, and hardship support mechanisms to ensure market growth is sustainable and does not contribute to over-indebtedness among vulnerable consumer segments.

• The competitive landscape features the Big Four banks (CBA, Westpac, NAB, ANZ) competing on scale, brand trust, and comprehensive product ranges against fintech disruptors (Afterpay, Zip, Beforepay) offering technology-driven speed and accessibility-with credit unions serving community-focused segments and specialized lenders targeting niche markets, requiring differentiation through digital experience, pricing transparency, regulatory compliance, and data-driven personalization.

Recent News and Developments:

April 2026: Consumer instalment spending in Australia increased approximately 26% over the past three years, rising from around AUD 469 per month in January 2023 to approximately AUD 589 per month in January 2026. Analysts noted that cost-of-living pressures are driving wider use of BNPL and short-term credit solutions across middle-income households.

March 2026: Australia's unsecured lending market recorded rising financial stress indicators as BNPL late arrears climbed to approximately 2.45%, while early-stage arrears increased to around 4.09%. Despite tighter regulation, BNPL new account volumes increased approximately 25% year-on-year, reflecting continued strong consumer demand for flexible credit products.

February 2026: Australia's personal loan market continued expanding as digital lenders and fintech platforms accelerated online credit approvals and AI-driven loan assessments. Australians borrowed approximately AUD 9.3 billion in fixed-term personal loans during the September 2025 quarter alone, marking one of the highest lending levels on record.

January 2026: Consumer debt levels continued rising across Australia amid persistent inflationary pressures, with average personal debt increasing to approximately AUD 17,634 in 2025, up from AUD 15,179 in 2024. Credit card usage remained widespread, with approximately 33% of Australians actively using credit cards, while nearly 24% used BNPL services.

December 2025: Australia's consumer credit landscape entered a major regulatory transition phase as new BNPL regulations came into effect under the National Consumer Credit Protection framework. Industry estimates showed that Afterpay alone accounted for more than 3.5 million active monthly users, representing roughly half of Australia's BNPL accounts nationwide.

Note: If you require any specific information that is not covered currently within the scope of the report, we will provide the same as a part of the customization.

Speak to an analyst for a customized sample report PDF: https://www.imarcgroup.com/request?type=report&id=32006&flag=C

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel. No.: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Australia Consumer Credit Market 2026 | Worth USD 481.6 Million by 2034 here

News-ID: 4510556 • Views: …

More Releases from IMARC Group

India Edible Oil Market 2026-2034: Emerging Trends, Govt Policy Support & Future …

How is India Edible Oil Market Performing?

India's edible oil industry is navigating a steady and structurally supported growth phase, driven by rising household consumption, increasing health awareness among consumers, and the rapid expansion of packaged and branded cooking oil segments across the country. As India's population grows and urbanization accelerates, demand for refined, fortified, and premium edible oils is expanding across residential, foodservice, and food processing applications.

Behind this consistent market…

Qatar Real Estate Market Size to Surpass USD 17,583.08 Million by 2033 | With a …

Qatar Real Estate Market Overview

Market Size in 2024: USD 14,988.18 Million

Market Size in 2033: USD 17,583.08 Million

Market Growth Rate 2025-2033: 1.79%

According to IMARC Group's latest research publication, "Qatar Real Estate Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2025-2033", the Qatar real estate market size reached USD 14,988.18 Million in 2024. The market is projected to reach USD 17,583.08 Million by 2033, exhibiting a growth rate (CAGR) of 1.79%…

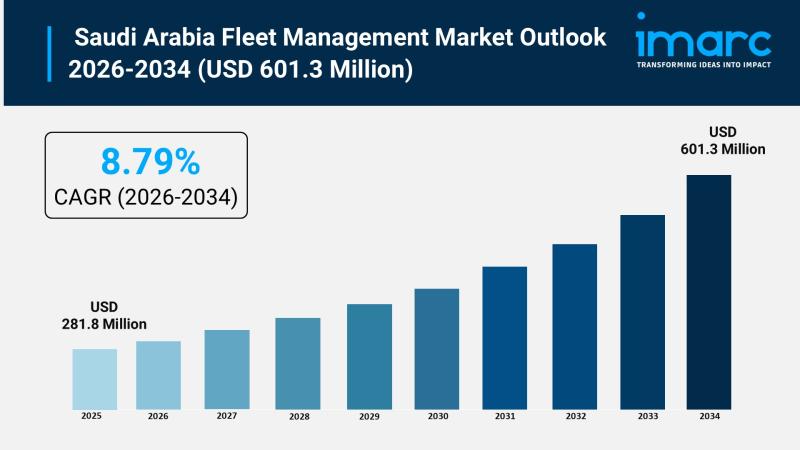

Saudi Arabia Fleet Management Market to Grow at 8.79% CAGR by 2034| IMARC Group

Saudi Arabia Fleet Management Market Overview

Market Size in 2025: USD 281.8 Million

Market Size in 2034: USD 601.3 Million

Market Growth Rate 2026-2034: 8.79%

According to IMARC Group's latest research publication, "Saudi Arabia Fleet Management Market: Industry Trends, Share, Size, Growth, Opportunity and Forecast 2026-2034", The Saudi Arabia fleet management market size was valued at USD 281.8 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 601.3 Million by…

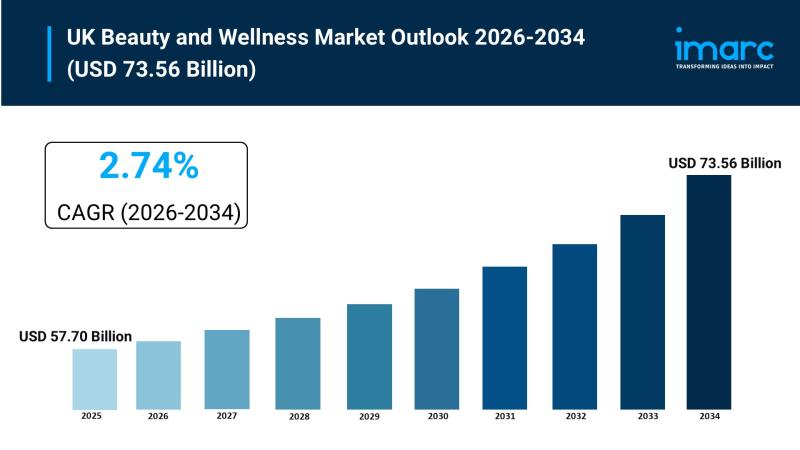

UK Beauty and Wellness Market Size to Worth USD 73.56 Billion by 2034 | With a 2 …

UK Beauty and Wellness Market Overview

Market Size in 2025: USD 57.70 Billion

Market Size in 2034: USD 73.56 Billion

Market Growth Rate 2026-2034: 2.74%

According to IMARC Group's latest research publication, "UK Beauty and Wellness Market Report by Product Type, Distribution Channel, and Region, 2026-2034," the UK beauty and wellness market size was valued at USD 57.70 Billion in 2025 and is projected to reach USD 73.56 Billion by 2034, growing at a…

More Releases for Australia

Derila Memory foam pillow Australia: Honest Reviews About Derila Australia

Derila is one of the best memory foam pillows sold in Australia today.

Priced at around 30 dollars (USD), derila is currently the most reviewed and the cheapest memory pillow available in Australia.

What is Derila? Is Derila Pillow the best in Australia? Keep reading to discover everything worth knowing about Derila Australia.

OVERVIEW

Recently, Memory foam pillow has been trending and there is a lot of brands to choose from. Which one is…

CeraCare Australia - Where to Buy Legit CeraCare Supplement in Australia?

CeraCare Australia - Ceracare is a glucose support supplement that proposes to augment cardiovascular prosperity and to stay aware of perfect glucose assimilation in Australia. CeraCare supplement is conceptualized and executed by a threesome – Christine, Dr. Jihn and Michael. It is a natural supplement that helps one stay aware of ideal glucose levels, cardiovascular prosperity, and glucose assimilation.

Take Advantage of 80% Discount Offer in Australia >> https://boostsxproaustralia.com/ceracare-new

The indications…

Glucofort Australia - Where to Buy Legit Glucofort Supplement in Australia?

Glucofort Australia - Glucofort is an efficient, all-natural progressive glucose support supplement in Australia. This formula is made out of 12 key ingredients, 7 nutrients, and minerals, and a little of Vanadium. This supplement upholds regulated glucose levels and glucose digestion. Glucofort prides itself as the most inventive supplements available in Oceania, accentuating its solidarity, wellbeing, and quality.

Take Advantage of 75% Discount Offer in Australia >> https://boostsxproaustralia.com/glucofort-new

Rather than simply…

Australia Agriculture Market, Australia Agriculture Industry, Australia Agricult …

Australia Agriculture has been as vital within the development of Australia, because it was within the United States. Australia's ancient dominance in wheat and sheep continues into the 21st century. Recently Australian agriculture has become more and more diversified. The considerable expanses of productive land have helped Australia to become a number one world exporter of grains, meats, and wool. Each grains (predominantly wheat and barley) and wool markets round…

Australia Conveyor Maintenance Analysis by Top Companies Habasit Australia Pty l …

Global Australia Conveyor Maintenance Market and Competitive Analysis

Know your current market situation! Not only a vital element for brand new products but also for current products given the ever-changing market dynamics. The study allows marketers to remain involved with current consumer trends and segments where they'll face a rapid market share drop. Discover who you actually compete against within the marketplace, with Market Share Analysis know market position, to push…

Australia Conveyor Maintenance Market Analysis By Manufacturers Rema Tip Top Aus …

A conveyor system is a common piece of mechanical handling device that moves materials/objects from one location. A conveyor is often lifeline to a company’s ability to effectively move its products in a timely manner. While it is used constantly in a manufacturing plant, proper maintenance from trained technicians can extend the lifespan of conveyor. Furthermore, conveyor maintenance is essential as it may be subjected to different types of failures…