Press release

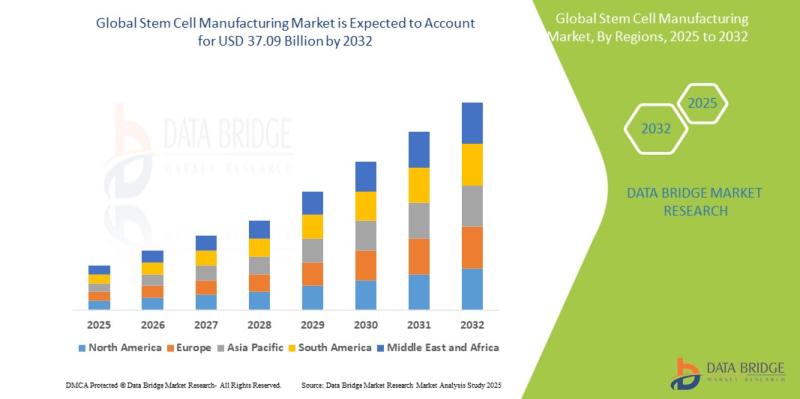

Stem Cell Manufacturing Market Growth Surges from USD 16.56 Billion to USD 37.09 Billion by 2032

Stem Cell Manufacturing Market

As per Data Bridge Market Research analysis, the Stem Cell Manufacturing Market was estimated at USD 18.02 billion in 2025. The market is expected to grow from USD 19.93 billion in 2026 to USD 37.09 billion in 2032, at a CAGR of 10.6% during the forecast period with driven by the rising demand for regenerative medicine, increasing investments in stem cell therapy manufacturing facilities, expanding clinical applications of stem cell-based treatments, and technological advancements in automated cell processing systems.

Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs) : https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-stem-cell-manufacturing-market

Market Size & Forecast

2025 Market Size: USD 18.02 Billion

2026 Projected Market Size: USD 19.93 Billion

2032 Projected Market Size: USD 37.09 Billion

CAGR (2026-2032): 10.6%

Largest Region: North America

Fastest Growing Region: Asia-Pacific

Key Market Report Takeaways

North America held the largest market share of approximately 42.3% in 2025, supported by advanced biotechnology infrastructure, high R&D expenditure, and strong clinical trial activity.

Asia-Pacific is projected to register the fastest growth rate during the forecast period due to expanding healthcare infrastructure and increasing government support for regenerative medicine.

Adult stem cells represented the leading product segment owing to extensive therapeutic applications and lower ethical concerns compared to embryonic stem cells.

Cell and tissue banking emerged as the dominant application segment due to growing demand for long-term preservation of stem cells for research and therapeutic use.

Pharmaceutical and biotechnology companies accounted for the largest end-user segment because of rising investments in cell therapy development and commercialization activities.

Automated bioprocessing and closed-system manufacturing technologies are increasingly improving scalability, product consistency, and regulatory compliance in stem cell production.

Key Market Trends & Highlights

North America continues to dominate the global market due to the presence of major biotechnology firms, established regulatory frameworks, and increasing investments in regenerative medicine research.

Asia-Pacific is the fastest-growing regional market, driven by rising stem cell therapy approvals, expanding healthcare expenditure, and growing clinical research activities in China, India, Japan, and South Korea.

Cell therapy manufacturing remains the dominant application segment owing to increasing demand for personalized medicine and regenerative treatment solutions for chronic diseases.

Key growth drivers include increasing prevalence of chronic disorders, rising demand for regenerative medicine, and growing public-private investments in advanced biologics manufacturing infrastructure.

Automation, AI-driven bioprocess monitoring, 3D cell culture systems, and scalable bioreactor technologies are reshaping manufacturing efficiency and product quality standards.

Regulatory agencies across North America and Europe are strengthening GMP compliance frameworks, while strategic collaborations between biotechnology companies and research institutes are accelerating commercialization activities.

Details about the report and current availability can be viewed : https://www.databridgemarketresearch.com/reports/global-stem-cell-manufacturing-market

Market Dynamics

Market Drivers

Rising Demand for Regenerative Medicine

The increasing adoption of regenerative medicine for treating chronic diseases, orthopedic disorders, cardiovascular conditions, and neurological diseases is significantly driving market growth. Stem cell therapies are gaining traction due to their ability to repair damaged tissues and improve clinical outcomes. North America and Europe continue to lead clinical adoption owing to strong reimbursement frameworks and advanced healthcare systems. Growing patient preference for minimally invasive and personalized treatment approaches further supports demand expansion.

Advancements in Automated Cell Manufacturing Technologies

Technological innovations in automated bioprocessing systems, closed manufacturing platforms, and single-use bioreactors are improving scalability and reducing contamination risks in stem cell production. Automation enhances manufacturing consistency and reduces labor-intensive procedures, making commercial-scale production more viable. Companies across the U.S., Germany, and Japan are increasingly investing in smart manufacturing technologies to streamline production workflows. These advancements are accelerating the transition from laboratory-scale research to commercial therapeutic production.

Increasing Investments in Cell Therapy Research

Government agencies, venture capital firms, and pharmaceutical companies are substantially increasing investments in stem cell research and advanced therapy medicinal products. Funding support for clinical trials and manufacturing infrastructure is accelerating product development pipelines. The U.S. National Institutes of Health (NIH), European Commission, and Asian healthcare authorities continue to allocate significant budgets toward regenerative medicine innovation. Increased collaboration between academic institutes and biotechnology firms is also contributing to market expansion.

Expansion of Clinical Trials and Therapeutic Applications

The growing number of stem cell-based clinical trials targeting oncology, autoimmune diseases, diabetes, and rare genetic disorders is creating strong demand for manufacturing capabilities. Pharmaceutical and biotechnology companies are expanding production facilities to support increasing clinical-stage therapies. Regulatory agencies are providing accelerated approval pathways for advanced therapies in major markets. Asia-Pacific countries are witnessing rapid growth in clinical research activities due to supportive regulatory reforms and lower operational costs.

Growing Focus on Personalized Medicine

The rising adoption of personalized and precision medicine is increasing demand for patient-specific stem cell therapies. Autologous stem cell treatments are gaining popularity because of reduced immune rejection risks and improved therapeutic compatibility. Healthcare providers are increasingly integrating regenerative therapies into treatment protocols for chronic and degenerative diseases. This trend is particularly strong in developed healthcare markets such as the U.S., Canada, Germany, and the U.K.

Market Restraints

High Manufacturing and Operational Costs

Stem cell manufacturing requires sophisticated laboratory infrastructure, GMP-certified facilities, advanced bioreactors, and skilled professionals, resulting in high production costs. Commercial-scale manufacturing remains capital-intensive, limiting accessibility for small and mid-sized biotechnology firms. High treatment costs also restrict patient adoption in price-sensitive regions. Developing economies in Latin America and Africa face significant affordability challenges due to limited healthcare funding.

Stringent Regulatory Compliance Requirements

The market is highly regulated due to safety concerns associated with stem cell therapies and biologics manufacturing. Companies must comply with strict GMP guidelines, product validation standards, and quality assurance protocols imposed by regulatory authorities. Regulatory approval processes are often lengthy and costly, delaying commercialization timelines. Differences in international regulatory standards further complicate global market expansion strategies.

Ethical and Legal Concerns

Ethical debates surrounding embryonic stem cell research continue to create regulatory uncertainties in several countries. Restrictions on stem cell sourcing and clinical applications limit research activities in specific regions. Public concerns regarding genetic manipulation and long-term treatment safety also impact market acceptance. Regulatory inconsistencies across global markets continue to create barriers for multinational companies.

Limited Skilled Workforce Availability

Stem cell manufacturing requires highly specialized expertise in cell biology, bioprocess engineering, and quality control management. The shortage of trained professionals capable of handling advanced manufacturing systems remains a key challenge, particularly in emerging economies. Limited workforce availability increases operational complexity and training costs. Rapid technological evolution further intensifies the need for continuous workforce upskilling.

Complex Supply Chain and Storage Requirements

Stem cell products require highly controlled transportation, cryopreservation systems, and cold-chain logistics to maintain viability and product quality. Supply chain disruptions can significantly affect manufacturing timelines and therapeutic efficacy. Maintaining ultra-low temperature storage infrastructure increases operational costs for manufacturers and healthcare providers. Emerging markets often face logistical limitations due to inadequate cold-chain infrastructure.

Market Opportunities

Expansion of Regenerative Medicine Applications

The increasing use of stem cell therapies across oncology, orthopedics, cardiology, and neurology presents substantial revenue opportunities for manufacturers. Emerging therapeutic areas such as tissue engineering and organ regeneration are expected to create new commercial pathways. Expanding clinical indications will increase demand for scalable manufacturing solutions globally. Asia-Pacific and Middle Eastern healthcare systems are increasingly investing in regenerative treatment capabilities.

Growing Adoption of AI and Automation Technologies

Integration of artificial intelligence, robotics, and digital bioprocess monitoring systems is creating opportunities for improving manufacturing efficiency and reducing production errors. Automated quality control systems enhance scalability and compliance management. Companies investing in digital manufacturing ecosystems are expected to gain competitive advantages through reduced operational costs and faster production cycles. Advanced analytics also improve batch consistency and product traceability.

Emerging Markets Offering Untapped Potential

Developing countries across Asia-Pacific, Latin America, and the Middle East are witnessing increasing investments in biotechnology infrastructure and healthcare modernization. Governments are introducing favorable policies to attract regenerative medicine companies and clinical research activities. Rising healthcare expenditure and expanding patient populations provide strong long-term growth opportunities. China and India are becoming key manufacturing hubs due to lower operational costs and skilled workforce availability.

Strategic Collaborations and Partnerships

Partnerships between biotechnology firms, academic institutions, and contract manufacturing organizations are accelerating innovation and commercialization. Collaborative research initiatives are enabling faster development of advanced cell therapies and scalable production technologies. Companies are increasingly pursuing joint ventures to strengthen regional presence and technology capabilities. Strategic alliances are also improving access to regulatory expertise and distribution networks.

Increasing Demand for Off-the-Shelf Cell Therapies

The development of allogeneic stem cell therapies is creating opportunities for large-scale commercial manufacturing and broader patient accessibility. Off-the-shelf products reduce production timelines and improve treatment availability compared to autologous therapies. Pharmaceutical companies are increasingly investing in universal donor cell platforms to achieve scalable commercialization. Advances in gene editing technologies are further supporting this transition.

Market Challenges

Maintaining Product Consistency and Quality

Achieving standardized manufacturing outcomes remains challenging due to variability in stem cell sources, donor characteristics, and production processes. Maintaining batch-to-batch consistency is critical for regulatory approval and clinical effectiveness. Variability can increase production failures and impact therapeutic reliability. Manufacturers must invest heavily in advanced quality control and monitoring systems to address these issues.

Scalability Limitations in Commercial Production

Transitioning from laboratory-scale production to commercial-scale manufacturing remains technically complex. Many stem cell manufacturing systems face scalability constraints related to cell viability, contamination risks, and process optimization. Large-scale bioreactor integration and automation require substantial capital investments. Smaller companies often struggle to achieve economically sustainable production volumes.

Regulatory Uncertainty Across Global Markets

Variations in international regulatory frameworks create challenges for companies seeking multi-regional commercialization. Different approval standards, clinical trial requirements, and manufacturing guidelines increase compliance complexity. Regulatory uncertainty can delay product launches and increase operational expenses. Emerging markets continue to face inconsistent regulatory enforcement and infrastructure limitations.

Supply Chain Vulnerabilities

The market depends heavily on specialized raw materials, cryogenic storage systems, and temperature-sensitive transportation networks. Disruptions in global supply chains can delay production schedules and increase operational costs. Geopolitical tensions, trade restrictions, and raw material shortages further intensify supply chain risks. Maintaining uninterrupted logistics remains particularly difficult in developing regions.

Intense Competitive Pressure and Pricing Constraints

The increasing number of biotechnology firms entering the regenerative medicine sector is intensifying competition. Companies face pricing pressure due to high R&D expenditures and reimbursement limitations. Larger organizations with advanced infrastructure and broader distribution capabilities often dominate market positioning. Smaller firms may struggle to sustain profitability amid rising commercialization costs.

Market Segmentation & Analysis

By Product

Consumables

Consumables include culture media, reagents, buffers, and cryopreservation materials used during stem cell processing and storage. This segment accounted for the largest revenue share in 2025 due to recurring demand across research laboratories and commercial manufacturing facilities. Continuous clinical trial expansion and increasing production volumes are supporting strong growth. The segment is projected to maintain steady CAGR growth throughout the forecast period.

Instruments

Instruments include bioreactors, cell sorters, incubators, and automated processing systems used in stem cell manufacturing workflows. The segment is experiencing rapid growth due to increasing adoption of automation and scalable manufacturing technologies. Advanced instrumentation improves process efficiency, contamination control, and regulatory compliance. Demand is particularly strong in North America, Europe, and Japan.

By Stem Cell Type

Adult Stem Cells

Adult stem cells dominated the market due to broader clinical acceptance, lower ethical concerns, and extensive applications in regenerative medicine. These cells are widely used in hematopoietic stem cell transplantation and tissue repair therapies. Increasing research investments and favorable regulatory acceptance continue to strengthen segment growth. The segment accounted for the highest market share in 2025.

Pluripotent Stem Cells

Pluripotent stem cells, including induced pluripotent stem cells (iPSCs), are expected to witness the fastest CAGR during the forecast period. Their ability to differentiate into multiple cell types makes them highly valuable for disease modeling and advanced therapeutics. Technological advancements in reprogramming techniques are accelerating commercial adoption. Pharmaceutical companies are increasingly investing in iPSC-based drug discovery programs.

By Application

Cell and Tissue Banking

Cell and tissue banking represented the dominant application segment due to rising demand for long-term storage of stem cells for therapeutic and research purposes. Growing awareness regarding regenerative medicine and increasing transplantation procedures support segment growth. Biobanking facilities are expanding globally to address increasing clinical demand. North America and Europe remain key regional contributors.

Drug Discovery and Development

Stem cells are increasingly used in pharmaceutical drug screening, toxicity testing, and disease modeling applications. The segment is projected to register significant growth due to rising investments in personalized medicine and biologics research. Pharmaceutical companies are adopting stem cell platforms to reduce drug development timelines and improve predictive accuracy. Asia-Pacific is emerging as a major research hub for this segment.

By End User

Pharmaceutical & Biotechnology Companies

This segment accounted for the largest market share due to rising investments in stem cell therapy commercialization and biologics development. Companies are heavily investing in manufacturing infrastructure and clinical research programs. Strategic partnerships and acquisitions continue to strengthen production capabilities globally. The segment is expected to maintain strong revenue contribution throughout the forecast period.

Research Institutes and Academic Centers

Academic institutions and research organizations play a critical role in stem cell innovation and early-stage therapeutic development. Increasing government funding and collaborative research programs are driving segment growth. Universities across the U.S., Europe, China, and Japan are actively engaged in advanced stem cell studies. The segment continues to support pipeline expansion and technology development.

Regional Analysis

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America dominated the global stem cell manufacturing market in 2025, accounting for approximately 42.3% of total revenue. The region benefits from strong biotechnology infrastructure, high healthcare expenditure, and advanced clinical research capabilities. The U.S. remains the key contributor due to significant investments in regenerative medicine and the presence of major biotechnology companies. Favorable FDA regulatory pathways and increasing commercialization of cell therapies continue to support regional market expansion.

Europe

Europe represents a mature and steadily growing market supported by extensive R&D investments and strong regulatory oversight for advanced therapy medicinal products. Germany, the U.K., and France remain leading contributors due to expanding biotechnology research and clinical trial activities. The region benefits from increasing collaboration between academic institutes and pharmaceutical companies. Government funding for regenerative medicine innovation continues to strengthen manufacturing capabilities across Europe.

Asia Pacific

Asia-Pacific is projected to register the fastest CAGR during the forecast period due to rapid healthcare infrastructure development and increasing biotechnology investments. China, India, Japan, and South Korea are witnessing growing stem cell therapy research activities and manufacturing expansion projects. Government initiatives supporting regenerative medicine and favorable clinical trial environments are accelerating market growth. Lower operational costs and expanding patient populations further attract global biotechnology companies to the region.

Latin America

Latin America is emerging as a developing market with gradual adoption of stem cell manufacturing technologies. Brazil and Mexico remain key regional markets due to improving healthcare infrastructure and increasing clinical research activities. Economic limitations and uneven regulatory frameworks continue to restrain rapid commercialization. However, growing investments in biotechnology research and regenerative medicine awareness are supporting long-term market potential.

Middle East & Africa

The Middle East & Africa market is experiencing steady but relatively slower growth due to limited advanced manufacturing infrastructure and regulatory complexities. Governments in the UAE and Saudi Arabia are increasing investments in biotechnology and healthcare modernization programs. Private sector participation in regenerative medicine research is gradually expanding across the region. Infrastructure gaps and limited skilled workforce availability continue to affect large-scale market development.

Key Insights:

Largest Region: North America

Fastest Growing Region: Asia-Pacific

Competitive Landscape

Market Structure Overview

The stem cell manufacturing market is moderately consolidated, with the presence of established biotechnology leaders, specialized regenerative medicine companies, and emerging cell therapy startups. Competition is primarily driven by technological innovation, manufacturing scalability, regulatory compliance capabilities, and strategic partnerships. Major companies focus on strengthening global production capacity and expanding advanced therapy portfolios. Competitive landscape analysis helps stakeholders understand company positioning, technological strengths, and long-term strategic direction.

Key Industry Players

Leading companies are focusing on automation technologies, bioprocess optimization, and expansion of GMP-certified manufacturing facilities to strengthen competitive positioning. Global players maintain strong market presence through diversified product portfolios and strategic collaborations with research institutions and pharmaceutical companies. Several firms are also investing in AI-driven manufacturing systems and next-generation stem cell platforms to improve scalability and efficiency.

List of Key Industry Players

Thermo Fisher Scientific Inc.

Merck KGaA

Lonza Group AG

Fujifilm Holdings Corporation

Sartorius AG

STEMCELL Technologies Inc.

Takara Bio Inc.

Danaher Corporation

Bio-Techne Corporation

Catalent, Inc.

Competitive Strategies

Companies are increasingly focusing on product innovation, automated manufacturing systems, and expansion of biologics production capabilities. Strategic partnerships between biotechnology companies and contract development organizations are accelerating commercialization timelines. Mergers and acquisitions are enabling firms to strengthen regional presence and technological expertise. Organizations are also investing in advanced analytics and digital manufacturing systems to enhance operational efficiency and product differentiation.

Emerging Players & Market Dynamics

Emerging biotechnology startups are introducing specialized stem cell platforms and cost-efficient manufacturing solutions, increasing competitive intensity across the market. Venture capital investments and government funding are supporting innovation in regenerative medicine technologies. New entrants are focusing on niche therapeutic applications and scalable production models to compete with established companies. Increasing adoption of digital transformation and automation technologies continues to reshape competitive market dynamics.

Latest Developments

January 2025 - Thermo Fisher Scientific Inc.: Expanded its advanced cell therapy manufacturing services in North America to support rising demand for commercial-scale regenerative medicine production. The expansion strengthens the company's position in biologics manufacturing and enhances supply chain capabilities.

October 2024 - Lonza Group AG: Announced new automated bioprocessing solutions for stem cell therapy production aimed at improving scalability and reducing contamination risks. The development supports increasing adoption of closed-system manufacturing technologies.

July 2024 - Sartorius AG: Launched advanced single-use bioreactor systems designed for large-scale stem cell cultivation and biopharmaceutical manufacturing. The launch enhances manufacturing efficiency and supports commercial therapy production.

March 2024 - Fujifilm Holdings Corporation: Expanded regenerative medicine manufacturing operations in Asia-Pacific through additional investments in cell culture and therapy production infrastructure. The initiative strengthens regional manufacturing ecosystems.

November 2023 - Merck KGaA: Introduced new GMP-compliant cell culture media solutions for stem cell manufacturing applications. The launch supports improved production consistency and regulatory compliance for advanced therapies.

August 2023 - Catalent, Inc.: Expanded its cell and gene therapy manufacturing facility in Europe to support increasing clinical and commercial demand. The expansion improves regional production capacity and supply chain resilience.

May 2023 - STEMCELL Technologies Inc.: Announced strategic collaboration agreements with research institutes to accelerate stem cell research and advanced therapeutic development. The partnership strengthens innovation capabilities and clinical application expansion.

February 2023 - Takara Bio Inc.: Increased investments in induced pluripotent stem cell (iPSC) manufacturing technologies to support next-generation regenerative medicine applications. The investment highlights growing commercial interest in scalable pluripotent stem cell production.

Check out more related studies published by Data Bridge Market Research:

https://www.databridgemarketresearch.com/reports/global-augmented-bone-graft-market

https://www.databridgemarketresearch.com/reports/global-balantidiasis-market

https://www.databridgemarketresearch.com/reports/global-bone-growth-stimulator-market

About Data Bridge Market Research:

Data Bridge Market Research is dedicated to deliver market intelligence with highest quality and accuracy. Through meticulous analysis and research, we strive to provide our clients with reliable and precise insights into various industries and markets. Over 500 full-time analysts at Data Bridge Market Research follow a wide array of models that allow proactive collaboration with clients, categorize new sources of incremental revenues, deliver revenue planning, and first-mover advantage about innovations and disruptions through early market research.

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Stem Cell Manufacturing Market Growth Surges from USD 16.56 Billion to USD 37.09 Billion by 2032 here

News-ID: 4509384 • Views: …

More Releases from Data Bridge Market Research

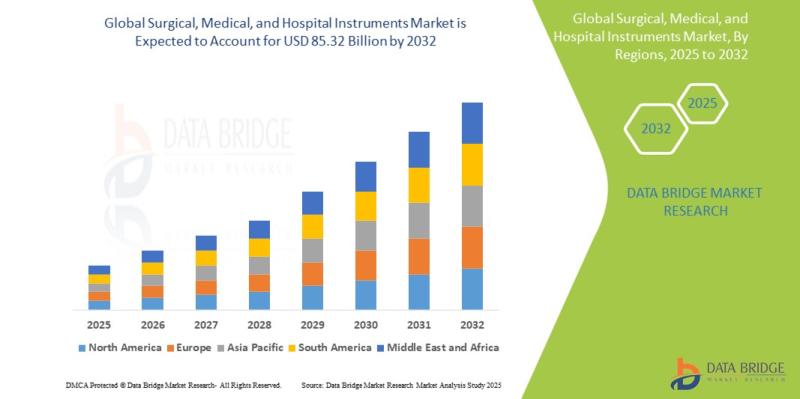

Surgical, Medical, and Hospital Instruments Market Growth Surges from USD 48.20 …

Market Summary

As per Data Bridge Market Research analysis, the Surgical, Medical, and Hospital Instruments Market was estimated at USD 48.20 billion in 2024. The market is expected to grow from USD 51.48 billion in 2025 to USD 85.32 billion in 2032, at a CAGR of 6.80% during the forecast period with driven by the rising demand for minimally invasive surgeries, growing healthcare infrastructure investments, increasing prevalence of chronic diseases, and…

Frequency Synthesizer Market Size, Share & Industry Analysis, Forecast to 2032 - …

As per Data Bridge Market Research analysis, the Frequency Synthesizer Market was estimated at USD 2.61 billion in 2025. The market is expected to grow from USD 2.81 billion in 2026 to USD 4.05 billion in 2032, at a CAGR of 7.6% during the forecast period with driven by the rising demand for high-frequency communication systems, increasing deployment of 5G infrastructure, growing aerospace & defense investments, and rapid adoption of…

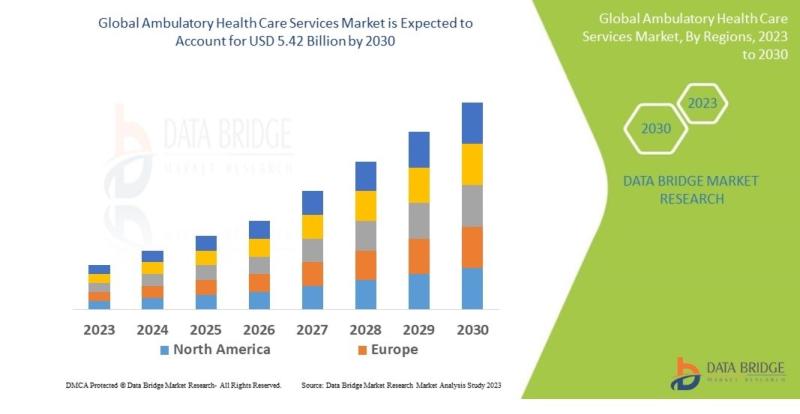

Ambulatory Health Care Services Market Projected to Expand at 6.00% CAGR Through …

Market Summary

As per Data Bridge Market Research analysis, the Ambulatory Health Care Services Market was estimated at USD 4.05 billion in 2025. The market is expected to grow from USD 4.29 billion in 2026 to USD 5.42 billion in 2030, at a CAGR of 6.00% during the forecast period with driven by the rising demand for cost-effective outpatient care services, increasing adoption of digital healthcare technologies, growing prevalence of chronic…

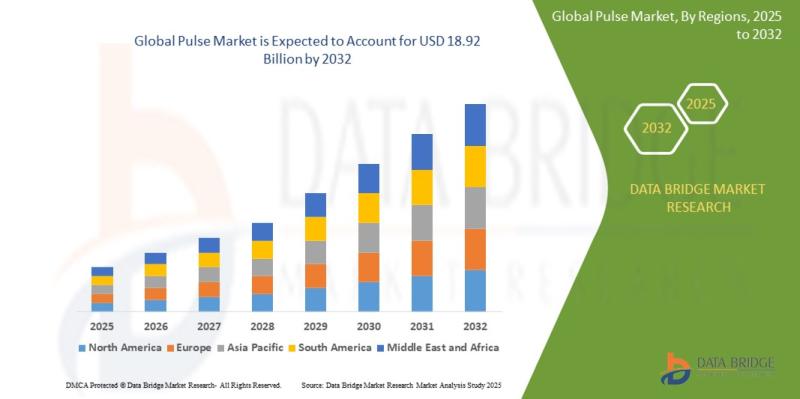

Pulse Market Forecast 2026-2032 | CAGR 6.00%

As per Data Bridge Market Research analysis, the Pulse Market was estimated at USD 12.58 billion in 2025. The market is expected to grow from USD 13.34 billion in 2026 to USD 18.92 billion in 2032, at a CAGR of 6.00% during the forecast period, driven by the rising demand for plant-based protein, increasing health-conscious consumer preferences, expanding vegan and flexitarian diets, and growing government support for sustainable agriculture and…

More Releases for America

Stabilit America Highlights Applications of Fiberglass Roof Panels with Stabilit …

Roofing materials are very important in the realm of modern construction, as they should be long lasting, economical and attractive. Fiberglass roof panels are a few of the numerous choices among several alternatives that have received a reputation of being versatile, long life, and adaptable in various sectors. They are favored by the architects, contractors, and property developers due to their lightweight construction, resistance to weather factors, and the ease…

Deodorants Market Report by Region (North America, EMEA, Latin America, Asia)

2025 - Pristine Market Insights, a leading market research firm, announced the release of its latest and comprehensive market research report on Deodorants market. The report spans over 500 pages and delivers 10-year market forecast in US dollars (or custom currencies upon request). It provides in-depth analysis of market dynamics (drivers, opportunities, restraints), PESTLE insights, latest industry trends, and demand factors. The report includes segmented market value, share (%), compound…

Sequestrant Market Report by Region (North America, EMEA, Latin America, Asia)

2025 - Pristine Market Insights, a leading market research firm, announced the release of its latest and comprehensive market research report on Sequestrant market. The report spans over 500 pages and delivers 10-year market forecast in US dollars (or custom currencies upon request). It provides in-depth analysis of market dynamics (drivers, opportunities, restraints), PESTLE insights, latest industry trends, and demand factors. The report includes segmented market value, share (%), compound…

Buttermilk Market Study by Region (North America, Latin America, Europe, Asia, M …

2025 - Pristine Market Insights, a leading market research firm, announced the release of its latest and comprehensive market research report on Buttermilk market. The report spans over 500 pages and delivers 10-year market forecast in US dollars (or custom currencies upon request). It provides in-depth analysis of market dynamics (drivers, opportunities, restraints), PESTLE insights, latest industry trends, and demand factors. The report includes segmented market value, share (%),…

Textiles Market Analysis Report, Regional Outlook - Europe, North America, South …

Adroit Market Research has announced the addition of the “Global Textiles Market Size Status and Forecast 2025”, The report classifies the global Textiles in a precise manner to offer detailed insights about the aspects responsible for augmenting as well as restraining market growth.

This report studies the global Textiles Speaker market, analyzes and researches the Textiles Speaker development status and forecast in Europe, North America, Central America, South America, Asia Pacific…

Global Gaucher Disease Market 2018 Covering North America, South America, Europe

Gaucher Disease Market

Summary

The Global Gaucher Disease Market is defined by the presence of some of the leading competitors operating in the market, including the well-established players and new entrants, and the suppliers, vendors, and distributors. The key players are continuously focusing on expanding their geographic reach and broadening their customer base, in order to expand their product portfolio and come up with new advancements.

Gaucher Disease market size to maintain the average annual growth…