Press release

Passive Fire Protection Market to Reach $8.9 Billion by 2034 as Stringent Building Codes and Infrastructure Growth Drive Demand for Fire-Resistant Materials

Passive Fire Protection Market Size, Share, Trends & Outlook Report 2034

Passive fire protection-built-in fire safety measures designed to contain fires or slow their spread without human intervention or external power-has become an essential component of modern construction and industrial safety. According to Dimension Market Research, the U.S. market alone is projected to reach USD 1.2 billion in 2025 and grow to USD 2.0 billion by 2034 at a CAGR of 5.5% , driven by the International Building Code (IBC), National Fire Protection Association (NFPA) standards, and increasing adoption of intumescent coatings and firestop sealants. With Europe dominating at 32.0% market share (USD 1.7 billion in 2025) and Japan maintaining steady demand (USD 290 million), the sector is witnessing consistent global growth as fire safety becomes a non-negotiable priority across building and industrial applications.

📄 Get Your Sample Report Today → https://dimensionmarketresearch.com/request-sample/passive-fire-protection-market/

🔷 The News Angle: From Reactive Response to Built-In Resilience-The Passive Fire Protection Evolution

The dominant narrative reshaping the passive fire protection market is the transition from reactive firefighting to proactive, built-in fire containment-a shift that recognizes that effective fire safety begins with structural design and material selection, not just alarms and sprinklers.

Stringent fire safety regulations are the most powerful catalyst. Governments and local authorities worldwide are mandating the use of passive fire protection systems across commercial, industrial, and residential buildings. The International Building Code (IBC), NFPA standards, EN standards, and national fire codes require certified fire-resistant materials in construction and industrial applications. These regulations are accelerating adoption of fire-rated coatings, sealants, and compartmentation systems during both new construction and renovation activities. Countries including Germany, the UK, and France have led adoption in commercial real estate, transport infrastructure, and public facilities.

Industrial growth in high-risk sectors is equally transformative. Oil & gas, petrochemicals, and manufacturing industries involve high fire hazards due to the presence of flammable substances. Passive fire protection systems are critical for these sectors to ensure equipment integrity and prevent fire escalation. On offshore platforms, refineries, processing units, and storage facilities, cementitious coatings, fireproof enclosures, and fire barriers maintain structural performance of steel frameworks, protect pipelines and control rooms, and contain fires within defined zones. The expansion of these industries, especially in emerging markets, is driving substantial demand for reliable and durable fireproofing solutions.

Urbanization and infrastructure development represent the third pillar. Rapid urbanization across Asia Pacific, Latin America, and the Middle East has accelerated adoption of passive fire protection solutions. Large-scale construction projects-high-rise commercial buildings, airports, hospitals, transport hubs-require comprehensive fire containment strategies. Passive systems including fire-resistant coatings, firestop sealants, and fire-rated barriers help compartmentalize fires, protect evacuation routes, and provide more time for emergency response. The renovation of aging buildings in mature markets further fuels demand.

🔷 Key Insights: Data Points Defining the Passive Fire Protection Market

Europe Leads (32.0% Share in 2025): Well-established fire safety regulations (EN standards), advanced construction practices, strong compliance culture, and ongoing green building investments drive regional dominance.

Coatings Dominate Product Type (38.0% Share): Intumescent and cementitious coatings applied to steel and structural components prevent critical failure temperatures; ease of application and aesthetic flexibility drive preference.

Cementitious Materials Lead Material Type (33.0% Share): Cost-effectiveness, ease of application, excellent fire-resistance properties, and non-combustible nature make cementitious materials preferred for large-scale industrial and commercial projects.

Intumescent Technology Leads Technology (47.0% Share): Versatility, effectiveness, clean aesthetic finish, and expansion upon heat exposure forming insulating char layers make intumescent coatings the gold standard.

Structural Protection Leads Application (36.0% Share): Preserving integrity of load-bearing elements (steel beams, columns, concrete frameworks) during fire incidents is critical for occupant safety and minimizing property damage.

Building & Construction Leads End-User Industry (42.0% Share): Growing urbanization, high-rise and commercial building projects, and rising fire safety awareness drive adoption across residential and public infrastructure.

U.S. Regulatory Environment: IBC, NFPA standards, and International Building Code mandate fire-resistant materials; oil & gas, healthcare, transportation, and data centers are prominent end-users.

EU Fire Workforce: In 2023, 61% of EU firefighters were aged 30-49; Croatia had highest firefighter density at 0.49%, with the Netherlands lowest at 0.05%.

AI Integration Emerging: AI-powered computer vision and drones enable automated inspection of PFP systems, detecting cracks, coating degradation, and material fatigue in real-time.

🔷 Market Dynamics: Drivers, Restraints, and Strategic Opportunities

Drivers: Fire Safety Codes & Industrial Growth

The primary driver is the implementation of stringent fire safety codes globally. The growing focus on life safety and property protection has led to widespread enforcement of fire safety regulations. Governments and local authorities are mandating the use of passive fire protection systems across commercial, industrial, and residential buildings. These regulations are accelerating adoption of fire-rated coatings, sealants, and compartmentation systems during both new construction and renovation activities.

Simultaneously, industrial growth in high-risk sectors is driving demand. Industries including oil & gas, petrochemicals, and manufacturing involve high fire hazards due to flammable substances. Passive fire protection systems are critical for these sectors to ensure equipment integrity and prevent fire escalation. The expansion of these industries, especially in emerging markets, is driving substantial demand for reliable and durable fireproofing solutions.

Restraints: High Costs & Limited Awareness

Despite momentum, significant barriers remain. Passive fire protection systems involve high-grade materials and specialized installation, which can significantly increase construction or retrofitting costs. This acts as a major barrier, particularly in cost-sensitive markets where builders may opt for lower-cost alternatives or delay fire protection integration. High material and installation costs challenge widespread adoption, especially in residential construction and smaller commercial projects.

Additionally, limited awareness in developing economies restrains market growth. In many developing countries, passive fire protection is still viewed as a secondary priority. A lack of awareness among contractors, architects, and regulators regarding long-term benefits and compliance requirements hinders widespread market penetration. Without education and enforcement, the full potential of passive fire protection remains unrealized in high-growth regions.

Opportunities: Green Solutions & Smart Building Integration

There is rising demand for low-emission, environmentally friendly fire protection materials. Manufacturers are innovating with non-toxic, recyclable, and low-VOC fireproofing products, opening new opportunities, especially in the green building segment. Sustainable construction practices and green building certifications (LEED, BREEAM) are driving demand for compliant, eco-friendly passive fire protection solutions.

Integration with smart building systems represents another major opportunity. The growth of digital construction technologies-Building Information Modeling (BIM), digital twins-is paving the way for integrating passive fire protection data with smart building platforms. This allows real-time monitoring, digital compliance tracking, and lifecycle management of fireproofing systems. AI-powered computer vision and drones enable automated inspection, detecting cracks, coating degradation, and material fatigue before failures occur.

📄 Get the Insights You Need to Drive Real Impact → https://dimensionmarketresearch.com/request-sample/passive-fire-protection-market/

🔷 Selective Segmentation: Where the Growth is Concentrated

By Product Type (Coatings-38.0% Share): Coatings dominate due to widespread application of intumescent and cementitious coatings in structural fire protection. These coatings are applied to steel and other structural components to prevent critical failure temperatures during fire. Intumescent coatings expand when exposed to heat, forming an insulating char layer that protects the substrate. Their ease of application, compatibility with various surfaces, and aesthetic flexibility make them preferred in commercial and industrial construction. Sealants and fillers represent another essential segment, used to close gaps, joints, and penetrations in walls, floors, and ceilings to prevent fire and smoke spread.

By Material Type (Cementitious Materials-33.0% Share): Cementitious materials dominate due to cost-effectiveness, ease of application, and excellent fire-resistance properties. Commonly applied as sprays or plasters, cementitious fireproofing forms thick, durable barriers insulating structural components from extreme heat. Their non-combustible nature and strong adhesion to various surfaces make them suitable for large-scale industrial facilities, commercial buildings, and infrastructure projects. Intumescent materials are gaining traction for advanced thermal performance and aesthetic appeal, particularly in architectural applications where maintaining visual appeal of exposed structural elements is important.

By Technology (Intumescent Technology-47.0% Share): Intumescent technology leads due to versatility, effectiveness, and clean aesthetic finish. Intumescent coatings expand significantly when exposed to high temperatures, forming thick, protective char layers that insulate structural elements like steel beams and columns. This expansion delays substrate temperature rise, maintaining structural integrity longer during fire. The technology is favored in commercial buildings, transportation hubs, and infrastructure projects where both performance and appearance matter. Endothermic technology plays a crucial role in specialized applications-data centers, electrical rooms, industrial facilities with sensitive equipment-absorbing heat through chemical or physical reactions.

By Application (Structural Protection-36.0% Share): Structural protection leads, focusing on preserving integrity of load-bearing elements-steel beams, columns, concrete frameworks-during fire incidents. Intumescent and cementitious coatings insulate these structures, preventing temperatures that could cause collapse. This application is critical in high-rise buildings, industrial facilities, and infrastructure projects where maintaining structural stability during fire is essential for occupant safety. Compartmentation is another key application, dividing structures into fire-resisting zones using fire-rated walls, floors, ceilings, doors, and barriers to contain fire to its origin point.

By End-User Industry (Building & Construction-42.0% Share): Building and construction dominates, driven by growing urbanization, rise in high-rise and commercial building projects, and growing awareness of fire safety standards across residential and public infrastructure. Passive fire protection systems-intumescent coatings, fire-rated boards, firestop sealants-are being widely integrated into modern construction practices to meet stringent safety regulations. Oil & gas/petrochemical represents another significant contributor, with cementitious coatings, fireproof enclosures, and fire barriers used extensively on offshore platforms, refineries, processing units, and storage facilities.

🔷 Regional Analysis: Europe Leads, Asia-Pacific Emerges as Fastest-Growing

Europe (32.0% Revenue Share in 2025): Europe is anticipated to lead the global passive fire protection market, driven by well-established fire safety regulations, widespread adoption of advanced construction practices, and strong emphasis on compliance with building codes including EN standards. Germany, the UK, and France have been at the forefront of integrating passive fire protection systems across commercial, residential, and industrial infrastructure. Ongoing investments in green buildings, renovation of aging structures, and development of critical infrastructure-airports, hospitals, transport hubs-continue to fuel demand for high-performance fire-resistant materials and technologies. Europe's leadership in digital construction, including BIM, encourages better integration of fire protection solutions during planning and design stages.

The U.S. Market (USD 1.2 billion in 2025, 5.5% CAGR): The U.S. market is witnessing steady growth, fueled by stringent fire safety regulations, rising infrastructure investments, and modernization of aging buildings. Implementation of building codes including IBC and NFPA standards, along with growing adoption of intumescent coatings, firestop sealants, and fire-rated barriers, are key demand drivers. Surge in commercial and industrial construction, especially in urban areas, has accelerated deployment of compartmentation systems and load-bearing structural fire protection technologies. Industries including oil & gas, healthcare, transportation, and data centers are becoming prominent end-users. Growing trend of sustainable construction is pushing the market toward low-VOC, environmentally friendly, fire-resistant materials.

Asia-Pacific (Fastest-Growing Region): Asia Pacific is expected to witness the most significant growth, driven by rapid urbanization, booming construction industry, and growing industrialization in China, India, Indonesia, and Vietnam. Growing awareness of fire safety, combined with evolving building codes and stricter regulatory frameworks, is encouraging adoption of fire-resistant materials across residential and commercial sectors. Expansion of high-risk industries-oil & gas, manufacturing, transportation infrastructure-further boosts need for reliable passive fire protection systems. Japan's market (USD 290 million in 2025, 4.8% CAGR) reflects a strong regulatory environment where building and fire safety standards are strictly enforced, particularly in urban centers and earthquake-prone regions.

📄 Get the Full Premium Report Now- https://dimensionmarketresearch.com/checkout/passive-fire-protection-market/

🔷 Competitive Landscape: Multinational Leaders and Regional Specialists

The global passive fire protection market features well-established multinational companies alongside growing numbers of regional and specialized players.

Global Industry Leaders: 3M Company, Hilti Group, PPG Industries, BASF SE, AkzoNobel N.V., RPM International Inc., Etex Group, The Sherwin-Williams Company, Promat International, Rockwool International A/S, Sika AG, Hempel A/S, Morgan Advanced Materials, Contego International Inc., Rudolf Hensel GmbH, Nullifire (Tremco Inc.), Carboline Company, ISOLATEK International, Tremco CPG Inc., and Firetherm (Sika Group) dominate through extensive product portfolios, strong R&D capabilities, and strategic partnerships with construction and industrial stakeholders.

Innovation Focus: Companies are focused on developing advanced intumescent and cementitious coatings, eco-friendly firestop solutions, and smart fireproofing technologies to meet evolving safety standards and sustainability goals. Isolatek International introduced FireSolve SB (January 2025), a solvent-based intumescent coating formulated for commercial steel structures offering improved surface aesthetics, low VOC levels, and application efficiency.

Recent Developments Highlighting Market Momentum:

May 2025: Huntsman launched POLYRESYST EV5005, an intumescent polyurethane coating designed for electric vehicle battery modules offering fast-curing spray application.

May 2025: Summit Fire Consulting completed acquisition of Performance Based Fire Protection Engineering (PBFPE), strengthening fire modeling and consulting capabilities.

February 2025: Agellus Capital launched Bluejack Fire Holdings by consolidating FirePro Tech, Chase Fire, and AAA Fire Protection Services.

January 2025: Isolatek International introduced FireSolve SB, a solvent-based intumescent coating for commercial steel structures.

December 2024: NV5 acquired Global Fire Protection Group (Global FPG), expanding footprint in data centers and healthcare sectors.

March 2024: IK Partners invested in Checkmate Fire, a passive fire protection specialist, to support growth across the UK and Europe.

🔷 The Road Ahead: What Decision-Makers Need to Know

For B2B decision-makers-construction project managers, facility owners, architects, industrial safety officers, and technology investors-the strategic imperative is clear: passive fire protection has moved from a regulatory checkbox to an essential component of resilient building design and industrial safety. The 5.9% CAGR reflects sustained demand driven by regulatory intensity, urbanization, and the recognition that built-in fire containment saves lives and property.

Key strategic imperatives include:

Prioritize intumescent coatings for structural steel protection. With 47.0% market share and growing, intumescent technology offers the optimal balance of performance, aesthetics, and compliance.

Address cost barriers through value engineering. While high-grade materials carry premium costs, lifecycle benefits-reduced damage, business continuity, insurance premiums-justify investment.

Expand into Asia-Pacific emerging markets. Rapid urbanization, booming construction, and strengthening regulations across China, India, and Southeast Asia offer significant growth opportunities.

Invest in low-VOC and eco-friendly formulations. Green building certifications (LEED, BREEAM) increasingly require sustainable fire protection materials. Manufacturers with compliant products will capture premium segments.

Leverage AI and BIM for compliance and lifecycle management. AI-powered inspection and digital twin integration enable real-time monitoring, predictive maintenance, and streamlined regulatory reporting.

The full report from Dimension Market Research provides granular segmentation by product type (coatings, sealants and fillers, boards and panels, spray shields and blankets, mortars, others), material type (cementitious materials, intumescent materials, fibrous materials, vermiculite and perlite, others), technology (intumescent, endothermic, ablative), application (structural protection, compartmentation, opening protection, others), end-user industry (building & construction, oil & gas/petrochemical, industrial facilities, transportation-railways, airports, marine, others), and 20+ regional markets, offering actionable intelligence for strategic planning.

📄 Explore the Report with TOC → https://dimensionmarketresearch.com/report/passive-fire-protection-market/

For Sales or Inquiries, Contact

Robert John

957 Route 33, Suite 12 #308 Hamilton Square, NJ-08690 USA

Email: enquiry@dimensionmarketresearch.com

United States: (+1 732 369 9777)

Tel No: +91 88267 74855

Dimension Market Research (DMR) is a market research and consulting firm based in India & US, with its headquarters located in the USA. The company believes in providing the best and most valuable data to its customers using the best resources and analysts to work on, to create unmatchable insights into the industries and markets while offering in-depth results of over 30 industries, and all major regions across the world. We also believe that our clients don't always want what they see, so we provide customized reports as well, as per their specific requirements, to create the best possible outcomes for them and enhance their business through our data and insights in every possible way.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Passive Fire Protection Market to Reach $8.9 Billion by 2034 as Stringent Building Codes and Infrastructure Growth Drive Demand for Fire-Resistant Materials here

News-ID: 4508663 • Views: …

More Releases from Dimension Market Research

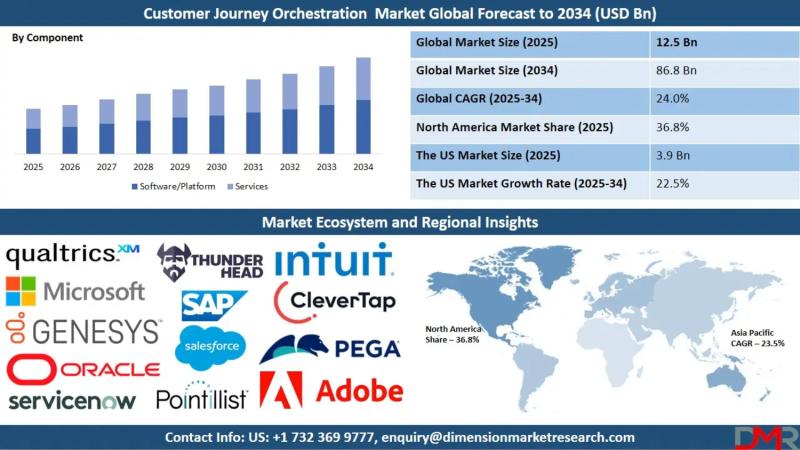

Customer Journey Orchestration Market to Skyrocket from 12.5 billion in 2025 to …

The global Customer Journey Orchestration Market is poised for explosive growth, with market valuation projected to surge from an estimated USD 12.5 billion in 2025 to USD 86.8 billion by 2034, registering a remarkable compound annual growth rate (CAGR) of 24.0%. According to Dimension Market Research, this extraordinary expansion is being driven by three converging forces: the widening gap between customer expectations for personalization and actual brand experiences, the rapid…

Zero Trust Security Market to Reach $179.5 Billion by 2034 as Cyber Threats and …

According to Dimension Market Research, the market is set to expand at a 17.2% CAGR from 2025 to 2034, with multi-factor authentication capturing 81.8% of authentication revenue as identity-based attacks surge 10x.

A new data-intensive analysis projects the global Zero Trust Security market will surge from USD 43.0 billion in 2025 to USD 179.5 billion by 2034, driven by an unprecedented convergence of identity-based cyberattacks, cloud migration, and government mandates. Unlike…

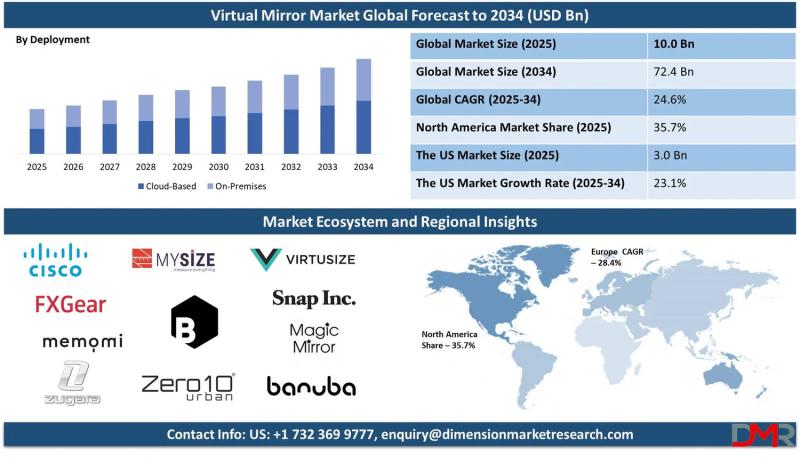

Virtual Mirror Market to Surge from $10 Billion in 2025 to $72.4 Billion by 2034 …

According to Dimension Market Research, the global virtual mirror market is accelerating at an unprecedented pace, driven by widespread adoption of augmented reality in e-commerce, rising consumer demand for contactless try-on experiences, and deep integration of AI and computer vision technologies across retail, beauty, healthcare, and automotive sectors.

A newly released comprehensive analysis reveals that the global virtual mirror market, valued at USD 10.0 billion in 2025, is projected to reach…

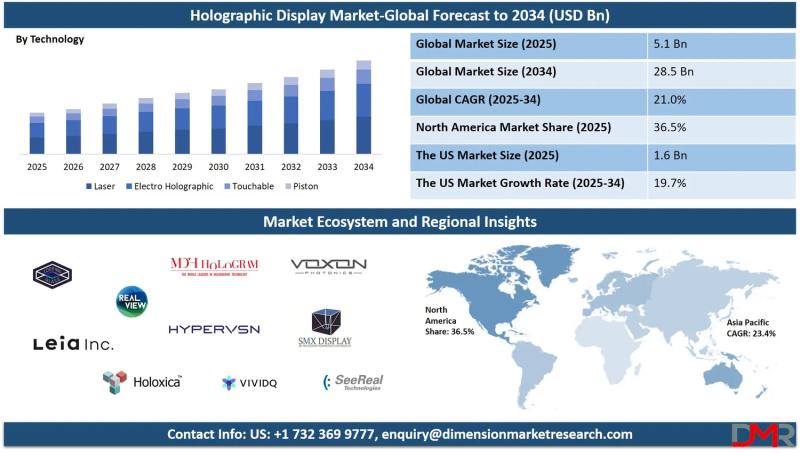

Holographic Display Market to Reach $28.5 Billion by 2034 at 21% CAGR - AI-Integ …

According to Dimension Market Research, the global holographic display market is forecast to surge from USD 5.1 billion in 2025 to USD 28.5 billion by 2034, registering a compound annual growth rate of 21.0%.

A new comprehensive analysis reveals that holographic displays are rapidly moving beyond novelty applications to become mission-critical visualization tools across healthcare, automotive, defense, and consumer electronics. Unlike traditional AR/VR solutions that require headsets or wearable devices, modern…

More Releases for Passive

Passive Rfid Tags Market Size Analysis by Application, Type, and Region: Forecas …

According to Market Research Intellect, the global Passive Rfid Tags market under the Internet, Communication and Technology category is expected to register notable growth from 2025 to 2032. Key drivers such as advancing technologies, changing consumer behavior, and evolving market dynamics are poised to shape the trajectory of this market throughout the forecast period.

The passive RFID tags market is experiencing significant growth, fueled by increasing demand for inventory management, asset…

Passive Electronic Components Market 2025-2032

Passive Electronic Components Market Overview

The three basic passive electronic components are resistors, capacitors, and inductors. Other passive components include transformers, diodes, thermistors, varactors, transducers, and many other common components.

This report provides a deep insight into the global Passive Electronic Components market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market…

Passive Optical LAN Market

The research study conducted by Report Ocean on the "Passive Optical LAN Market" spans over 100 pages and delves into various facets of this market. It analyses the business strategies adopted by emerging industry players, examines the geographical scope, dissects market segments, evaluates the product landscape, and investigates price and cost structures. This research report facilitates market segmentation based on the latest Market trends, geographical market, and technological advancements. Each…

Passive Speaker Market High-Quality Sound Reproduction with Passive Speaker Tech …

Global Passive Speaker Market Overview:

The Passive Speaker market is a broad category that includes a wide range of products and services related to various industries. This market comprises companies that operate in areas such as consumer goods, technology, healthcare, and finance, among others.

In recent years, the Passive Speaker market has experienced significant growth, driven by factors such as increasing consumer demand, technological advancements, and globalization. This growth has created both…

Passive Defence Electronics Solutions

Shoghi Communications Ltd is a leading technology oriented company in the domain of Intelligence, Surveillance and Reconnaissance. During its journey of twenty years, Shoghi has innovated and developed a large portfolio of products which are capable of monitoring various types of communication media especially in satellite, mobile and radio communication domains. Its customers include defence, intelligence and homeland security organisations in more than seventy countries covering Africa, Latin America, Middle…

Passive Optical LAN (POL) Market: Accelerating Bandwidth Requirements Driving Ne …

The market for passive optical LAN (POL) is poised for substantial growth in the coming years, registering a double-digit CAGR through the forecast period. Escalating bandwidth requirements, coupled with the energy efficient nature of passive optical components, is driving the POL market. The growth of networking technologies in the Asia Pacific and RoW markets, increasing fiber deployments, and rising investments in technological advancements and research infrastructure across both the regions…