Press release

High Strength Aluminum Alloys Market to Grow at 7.95% CAGR Through 2033

High Strength Aluminum Alloys Market

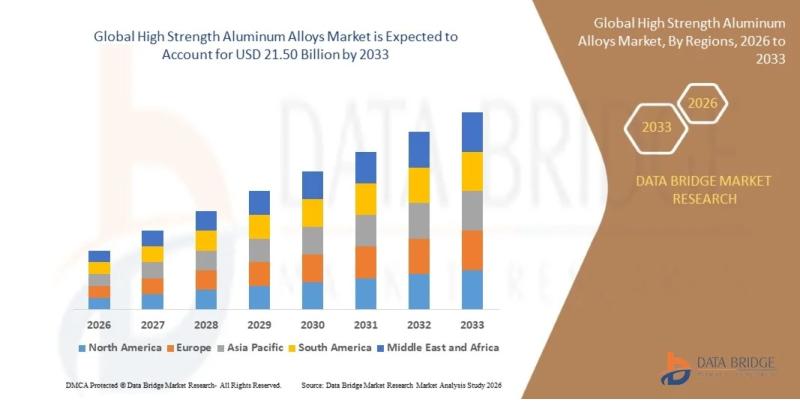

"As per Data Bridge Market Research analysis, the High Strength Aluminum Alloys Market was estimated at USD 11.66 billion in 2025. The market is expected to grow from USD 12.59 billion in 2026 to USD 21.50 billion in 2033, at a CAGR of 7.95% during the forecast period with driven by the rising demand for lightweight materials in aerospace, automotive, defense, and industrial manufacturing applications."

Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs) https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-high-strength-aluminum-alloys-market

The market is witnessing substantial growth due to increasing adoption of lightweight and high-performance materials across transportation and aerospace sectors. Automotive manufacturers are rapidly integrating high-strength aluminum alloys to improve fuel efficiency and reduce vehicle emissions. In aerospace manufacturing, rising aircraft production and modernization programs are accelerating the use of advanced 2 and 7series alloys. Technological advancements in alloy engineering, additive manufacturing, and recycling technologies are further supporting market expansion. Government regulations promoting carbon reduction and sustainable manufacturing practices are also strengthening long-term demand.

Market Size & Forecast

2025 Market Size: USD 11.66 Billion

2026 Projected Market Size: USD 12.59 Billion

2033 Projected Market Size: USD 21.50 Billion

CAGR (2026-2033): 7.95%

Largest Region: North America

Fastest Growing Region: Asia Pacific

Key Market Report Takeaways

North America held the largest market share of approximately 36% in 2025 due to strong aerospace and defense manufacturing infrastructure.

Asia Pacific is projected to witness the fastest growth during the forecast period driven by rapid industrialization and electric vehicle production growth.

The 7 series aluminum alloy segment accounted for the highest market share owing to superior tensile strength and aerospace applications.

Aerospace & defense remained the dominant application segment supported by increasing aircraft deliveries and defense modernization programs.

Transportation and automotive represented the leading end-use segment due to rising lightweight vehicle adoption.

Heat-treatable aluminum alloys maintained a dominant share because of enhanced fatigue resistance and structural strength.

Technological advancements in additive manufacturing and alloy strengthening processes are improving product performance and manufacturing efficiency.

Sustainability initiatives and recycled aluminum integration are becoming major strategic priorities among leading manufacturers.

Details about the report and current availability can be viewed : https://www.databridgemarketresearch.com/reports/global-high-strength-aluminum-alloys-market

Market Trends & Highlights

North America continues to dominate the global market due to advanced aerospace manufacturing infrastructure, high defense expenditure, and strong presence of leading aluminum alloy producers.

Asia Pacific is emerging as the fastest-growing region driven by expanding electric vehicle manufacturing, infrastructure development, and industrial growth in China, India, and Japan.

Aerospace applications remain the dominant segment as aircraft manufacturers increasingly adopt lightweight and high-strength alloys for structural optimization and fuel efficiency.

Increasing demand for lightweight vehicles, stringent emission regulations, and rising electric mobility adoption are accelerating market penetration across automotive applications.

Additive manufacturing, AI-assisted alloy development, and advanced heat-treatment technologies are reshaping production efficiency and enabling development of next-generation alloys.

Strategic investments in recycling infrastructure and low-carbon aluminum production are influencing procurement strategies across aerospace and transportation industries.

Government sustainability initiatives in Europe and North America are encouraging broader adoption of recyclable lightweight materials.

Collaborative research partnerships between alloy manufacturers and aerospace companies are accelerating innovation in high-performance aluminum systems.

Get Detailed Table of Contents (TOC) - Request Now for Complete Market Insights: https://www.databridgemarketresearch.com/toc/?dbmr=global-high-strength-aluminum-alloys-market

Market Dynamics

Market Drivers

Rising Demand for Lightweight Vehicles

Automotive manufacturers are increasingly replacing conventional steel components with high-strength aluminum alloys to reduce vehicle weight and improve fuel efficiency. The rapid expansion of electric vehicle production is significantly driving demand for lightweight materials that enhance battery performance and driving range. North America, Europe, and China are leading adoption due to strict emission regulations and sustainability targets. Aluminum alloy integration in battery enclosures, chassis systems, and structural components is accelerating long-term market growth.

Expansion of Aerospace and Defense Manufacturing

The aerospace industry remains a major consumer of high-strength aluminum alloys due to superior strength-to-weight ratio and fatigue resistance. Increasing aircraft production, fleet modernization programs, and rising defense budgets are strengthening global demand. The United States, France, and China continue to invest heavily in aerospace manufacturing capabilities. Advanced 2and 7series alloys are extensively used in fuselage structures, wings, and military systems.

Technological Advancements in Alloy Engineering

Continuous innovation in metallurgical processing, additive manufacturing, and heat-treatment technologies is improving aluminum alloy performance and manufacturing efficiency. Manufacturers are developing advanced alloys with enhanced corrosion resistance, thermal stability, and weldability. AI-assisted alloy design and precision manufacturing technologies are enabling customized high-performance solutions for aerospace and industrial applications. These developments are broadening the market scope across multiple industries.

Increasing Adoption of Additive Manufacturing

Additive manufacturing technologies are creating new growth opportunities for high-strength aluminum alloys in aerospace and precision engineering sectors. Manufacturers are increasingly investing in printable aluminum alloys with improved resistance and mechanical stability. These technologies reduce material waste, improve production flexibility, and support lightweight component manufacturing. Adoption is particularly strong in North America and Europe due to advanced industrial infrastructure.

Government Regulations Supporting Sustainable Materials

Governments across Europe and North America are implementing stringent fuel-efficiency and carbon-emission regulations that encourage lightweight material adoption. Policies promoting recyclable materials and low-carbon manufacturing are increasing aluminum alloy usage across transportation industries. Incentives supporting electric mobility and sustainable manufacturing are further strengthening long-term market demand. Regulatory alignment with environmental sustainability goals remains a major market growth catalyst.

Growth in Industrial and Infrastructure Applications

Industrial machinery, rail transportation, marine systems, and construction industries are increasingly adopting high-strength aluminum alloys due to durability and corrosion resistance benefits. Rapid infrastructure development in Asia Pacific and the Middle East is supporting alloy demand for structural applications. The shift toward energy-efficient industrial systems and lightweight infrastructure materials is creating additional growth opportunities globally.

Market Restraints

High Production and Processing Costs

High-strength aluminum alloys require advanced alloying elements, heat-treatment procedures, and precision manufacturing technologies, resulting in elevated production costs. Aerospace-grade alloys involve complex processing standards that increase operational expenditure. Smaller manufacturers often face barriers related to capital investment and advanced production requirements. Rising energy costs further impact manufacturing profitability across Europe and North America.

Volatility in Raw Material Prices

The market is highly affected by fluctuations in aluminum, copper, zinc, and magnesium prices due to geopolitical instability and supply-demand imbalances. Variations in raw material pricing directly impact manufacturing margins and long-term procurement strategies. Import-dependent regions face increased supply risks and pricing uncertainties. Commodity price volatility creates challenges for cost management and contract stability.

Corrosion and Weldability Limitations

Certain high-strength aluminum alloy grades, particularly 2 and 7 series, exhibit lower corrosion resistance and limited weldability compared to standard alloys. These limitations increase maintenance requirements and manufacturing complexity in harsh operating environments. Additional coatings and surface treatments are often necessary, increasing total lifecycle costs. Such factors may limit adoption in selected marine and industrial applications.

Supply Chain Disruptions and Resource Constraints

Global aluminum supply chains remain vulnerable to geopolitical tensions, logistics bottlenecks, and transportation disruptions. Dependence on critical alloying materials creates procurement risks for manufacturers. Supply shortages can delay production schedules across aerospace and automotive sectors. Asia Pacific and Europe are particularly exposed to international trade and logistics fluctuations.

Competition from Alternative Lightweight Materials

Carbon fiber composites, titanium alloys, and advanced steel technologies are increasingly competing with high-strength aluminum alloys across aerospace and automotive applications. Composite materials provide superior strength-to-weight performance in certain high-end applications. Manufacturers must continuously innovate to maintain competitiveness against alternative lightweight solutions. Pricing pressure from substitute materials remains a long-term market challenge.

Market Opportunities

Growth in Electric Vehicle Manufacturing

Rapid expansion of the electric vehicle industry presents substantial opportunities for high-strength aluminum alloy suppliers. Automotive manufacturers are increasingly integrating lightweight aluminum components into battery systems, structural frames, and vehicle bodies to improve efficiency. China, Europe, and North America remain key EV production hubs. Increasing investments in next-generation EV platforms are expected to generate strong long-term demand.

Expansion of Aerospace Production Programs

Commercial aviation recovery and defense modernization initiatives are generating strong demand for advanced aluminum alloys. Aircraft manufacturers are increasing procurement of lightweight structural materials to improve fuel efficiency and reduce emissions. Emerging aerospace manufacturing markets in Asia Pacific and the Middle East are strengthening future demand potential. New-generation aircraft platforms are expected to increase alloy consumption significantly.

Advancements in Additive Manufacturing Technologies

The integration of additive manufacturing into aerospace and industrial production is opening new growth avenues for printable high-strength aluminum alloys. Research advancements in -resistant and thermally stable alloys are enabling broader industrial adoption. Companies investing in 3D-print-compatible alloys are expected to gain competitive advantages in high-value applications. These developments are accelerating manufacturing innovation across industrial sectors.

Sustainable Aluminum and Recycling Initiatives

Growing emphasis on circular economy practices is creating opportunities for recycled high-strength aluminum production. Recycled aluminum significantly reduces carbon emissions and energy consumption compared to primary aluminum manufacturing. Companies investing in low-carbon aluminum technologies and recycling infrastructure are expected to benefit from increasing regulatory support and sustainability-focused procurement strategies.

Industrialization in Emerging Economies

Rapid industrial growth across India, Southeast Asia, Latin America, and the Middle East is increasing demand for lightweight industrial materials. Infrastructure development, rail transportation expansion, and industrial automation are driving adoption of advanced aluminum alloys. Government-backed manufacturing initiatives and foreign investments are supporting regional market expansion and industrial capacity growth.

Market Challenges

Complex Manufacturing and Heat-Treatment Requirements

High-strength aluminum alloys require precise heat-treatment cycles and advanced metallurgical control to achieve desired mechanical properties. Manufacturing inconsistencies can affect strength, fatigue resistance, and structural integrity. Smaller manufacturers often face technological limitations in maintaining high-quality production standards. This challenge is particularly significant in aerospace-grade applications requiring strict certification compliance.

Stringent Regulatory and Certification Standards

Aerospace and defense industries impose rigorous certification and testing requirements for aluminum alloy components. Regulatory compliance increases product development timelines and manufacturing costs. Companies operating across multiple regions must comply with varying industrial and environmental standards. These complexities can delay commercialization and limit market entry for emerging players.

Global Trade Tensions and Tariff Risks

The aluminum industry is highly influenced by tariffs, export restrictions, and geopolitical trade disputes. Trade barriers between major economies impact raw material sourcing and pricing structures. Manufacturers operating in export-oriented markets face supply uncertainties and margin pressures. Long-term geopolitical instability remains a critical challenge for global supply chains.

Technological Competition from Advanced Materials

Rapid advancements in carbon composites, magnesium alloys, and advanced steel technologies are intensifying market competition. Alternative materials offer superior performance in selected aerospace and automotive applications. Manufacturers must continuously increase R&D investments to maintain material competitiveness and technological differentiation. Competitive pressure from substitutes remains a long-term industry concern.

Energy-Intensive Production Processes

Primary aluminum production remains highly energy-intensive, exposing manufacturers to rising electricity costs and environmental scrutiny. Energy price volatility significantly affects profitability, particularly in Europe where industrial energy costs remain elevated. Sustainability expectations are pressuring producers to adopt low-carbon manufacturing technologies and renewable energy integration strategies.

Market Segmentation & Analysis

By Product Type

2Series Aluminum Alloys

The 2series alloys are widely used in aerospace applications due to high fatigue resistance and mechanical strength. These alloys maintain a strong market position in aircraft structures and military systems. Growth is supported by increasing aircraft production and defense modernization initiatives. However, lower corrosion resistance remains a limiting factor in certain industrial applications.

7Series Aluminum Alloys

The 7 series dominated the market in 2025 due to exceptional tensile strength and lightweight performance characteristics. These alloys are extensively used in aerospace structures, defense systems, and high-performance automotive applications. Rising adoption in advanced aviation platforms and electric vehicles is supporting segment growth. The segment is expected to maintain above-average CAGR during the forecast period.

6 Series Aluminum Alloys

The 6 series is gaining traction in automotive and construction industries due to balanced strength, corrosion resistance, and weldability. These alloys are commonly used in EV battery housings, transportation systems, and structural frames. Infrastructure expansion and industrial investments in Asia Pacific are supporting segment growth. Stable demand is expected throughout the forecast period.

By Application

Aerospace & Defense

Aerospace & defense represented the largest application segment in 2025, accounting for more than 40% of global market revenue. High-strength aluminum alloys are essential in aircraft wings, fuselage structures, and military systems due to superior strength-to-weight performance. Increasing aircraft deliveries and defense procurement programs continue to support segment expansion globally. North America remains the leading regional market.

Automotive & Transportation

The automotive segment is projected to witness the fastest CAGR during the forecast period due to rapid EV adoption and stringent fuel-efficiency regulations. Automotive manufacturers are increasingly replacing conventional steel with aluminum alloys in vehicle structures and battery systems. China, Germany, and the United States remain key contributors to segment growth. Lightweighting strategies continue to strengthen long-term demand.

Industrial & Marine

Industrial machinery, marine systems, and heavy equipment applications are steadily increasing adoption of corrosion-resistant aluminum alloys. Demand is supported by infrastructure modernization and industrial automation trends. The segment is witnessing rising penetration across rail transportation and energy-efficient industrial systems globally.

By End-User Industry

Transportation Industry

Transportation remained the dominant end-user segment due to extensive alloy usage across automotive, aerospace, and rail sectors. Lightweight material integration is improving operational efficiency and reducing energy consumption across transportation platforms. Global EV production growth is significantly strengthening demand. The segment is expected to maintain leadership through 2033.

Defense Industry

Defense applications continue to generate strong demand for high-strength aluminum alloys due to military aircraft modernization and armored vehicle development programs. Governments across North America, Europe, and Asia Pacific are increasing defense investments. Lightweight high-performance materials are becoming critical for advanced defense systems and aerospace technologies.

Industrial Manufacturing

Industrial manufacturing applications are expanding steadily due to growing demand for durable and lightweight materials. Aluminum alloys are increasingly used in automation equipment, industrial machinery, and infrastructure systems. Asia Pacific is emerging as a major growth center for this segment due to rapid industrialization.

Regional Analysis

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America dominated the global high-strength aluminum alloys market in 2025, accounting for approximately 36% of total revenue. The region benefits from advanced aerospace and defense manufacturing capabilities, strong R&D infrastructure, and high adoption of lightweight materials. The United States remains the key contributor due to the presence of major aerospace OEMs and alloy manufacturers. Government defense spending and technological innovation continue to support regional market leadership.

Europe

Europe represents a mature and steadily growing market supported by strong regulatory frameworks and sustainability initiatives. Germany, the U.K., and France are leading contributors due to advanced automotive and aerospace industries. Increasing investments in low-carbon aluminum production and EV manufacturing are strengthening regional demand. The region also benefits from strong research collaborations and recycling infrastructure development.

Asia Pacific

Asia Pacific is projected to register the fastest CAGR during the forecast period due to rapid industrialization and transportation manufacturing expansion. China dominates regional demand owing to large-scale EV production, infrastructure development, and aerospace investments. India and Japan are also witnessing rising adoption of lightweight materials across automotive and industrial sectors. Government manufacturing initiatives and growing local production ecosystems are supporting long-term expansion.

Latin America

Latin America is emerging as a developing market with gradual adoption of high-strength aluminum alloys across automotive and industrial sectors. Brazil and Mexico remain the primary regional contributors due to expanding manufacturing activities and automotive production. Infrastructure improvements and foreign investments are supporting market growth, although economic volatility continues to restrain expansion.

Middle East & Africa

The Middle East & Africa market is witnessing gradual growth supported by infrastructure development and industrial diversification initiatives. Governments are investing in manufacturing, aerospace, and transportation infrastructure to reduce economic dependence on oil-based industries. However, limited industrial ecosystems and infrastructure gaps continue to restrict large-scale market penetration. The UAE and Saudi Arabia are emerging as key investment hubs.

Key Insights

Largest Region: North America

Fastest Growing Region: Asia Pacific

Mature Markets: North America, Europe

High-Growth Markets: Asia Pacific

Emerging Markets: Latin America, Middle East & Africa

Regional performance differences are influenced by industrialization levels, technology adoption, aerospace manufacturing concentration, supply chain integration, and government policy support.

Competitive Landscape

Market Structure Overview

The global high-strength aluminum alloys market is moderately consolidated, with competition led by multinational aluminum producers, aerospace material suppliers, and specialized alloy manufacturers. Major companies maintain strong market positions through advanced manufacturing capabilities, extensive distribution networks, and continuous R&D investment. Competitive intensity is driven by technological innovation, sustainability initiatives, and product differentiation strategies. Competitive landscape analysis helps evaluate market positioning, operational strengths, and strategic direction among key players.

Key Industry Players

Leading companies are focusing on expanding advanced alloy portfolios, improving recycling capabilities, and strengthening aerospace and automotive partnerships. Established manufacturers maintain competitive advantages through integrated supply chains, metallurgy expertise, and strong customer relationships across aerospace and transportation industries. Companies are increasingly investing in low-carbon aluminum technologies and additive manufacturing capabilities to strengthen long-term competitiveness.

List of Key Industry Players

Alcoa

Constellium

Kaiser Aluminum

Norsk Hydro

Novelis

Arconic

UACJ Corporation

Hindalco Industries

Rio Tinto

China Hongqiao Group

Competitive Strategies

Companies are increasingly emphasizing alloy innovation, lightweight engineering, and sustainable aluminum production technologies. Strategic partnerships with aerospace OEMs and automotive manufacturers are strengthening long-term supply agreements. Mergers, acquisitions, and manufacturing capacity expansions are improving global market presence. Industry participants are also investing in recycling technologies and digital manufacturing systems to improve operational efficiency and product differentiation.

Emerging Players & Market Dynamics

Emerging manufacturers and research-focused companies are introducing specialized alloy formulations and additive manufacturing solutions. New entrants are intensifying competition by offering cost-effective and application-specific materials for industrial and transportation sectors. Increasing investments in AI-assisted alloy development and low-carbon aluminum production are reshaping market dynamics. Innovation-focused firms are challenging established manufacturers through rapid technological advancements.

Latest Developments

July 2024 - Purdue University: Researchers developed ultra-high-strength aluminum alloys optimized for additive manufacturing with improved deformability and resistance. The innovation is expected to expand aerospace and industrial applications.

February 2024 - Advanced Materials Research Team: Scientists introduced a -resistant welding solution for aerospace-grade aluminum alloys, improving structural integrity and manufacturing efficiency in aviation applications.

2024 - Oak Ridge National Laboratory: Development of advanced additive manufacturing aluminum alloys improved thermal stability and high-temperature strength for aerospace and industrial component manufacturing.

2024 - Global Aerospace Material Manufacturers: Leading companies increased investments in sustainable and recycled aluminum production capabilities to meet decarbonization goals across transportation and aerospace industries.

September 2024 - Automotive Industry Expansion: Rising electric vehicle production significantly increased demand for lightweight aluminum alloy battery enclosures and structural components globally.

2024 - Aluminum Producers in Europe and North America: Manufacturers accelerated low-carbon aluminum production initiatives and renewable energy integration strategies to reduce industrial emissions and strengthen sustainability positioning.

Check out more related studies published by Data Bridge Market Research:

https://www.databridgemarketresearch.com/reports/global-collapsible-jerry-can-market

https://www.databridgemarketresearch.com/reports/global-collapsible-sleeve-containers-market

https://www.databridgemarketresearch.com/reports/global-cosmetic-pencil-and-pen-market

https://www.databridgemarketresearch.com/reports/global-dual-flap-dispensing-closure-market

https://www.databridgemarketresearch.com/reports/global-duct-tapes-market

https://www.databridgemarketresearch.com/reports/global-ethylene-vinyl-acetate-eva-packaging-market

https://www.databridgemarketresearch.com/reports/global-growler-market

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com

Data Bridge Market Research is dedicated to deliver market intelligence with highest quality and accuracy. Through meticulous analysis and research, we strive to provide our clients with reliable and precise insights into various industries and markets. Over 500 full-time analysts at Data Bridge Market Research follow a wide array of models that allow proactive collaboration with clients, categorize new sources of incremental revenues, deliver revenue planning, and first-mover advantage about innovations and disruptions through early market research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release High Strength Aluminum Alloys Market to Grow at 7.95% CAGR Through 2033 here

News-ID: 4508252 • Views: …

More Releases from Data Bridge Market Research

Europe Epigenetics Diagnostic Market Size Projected to Hit USD 5.43 billion by 2 …

Market Summary

As per Data Bridge Market Research analysis, the Europe Epigenetics Diagnostic Market was estimated at USD 2.34 billion in 2025. The market is expected to grow from USD 2.08 billion in 2024 to USD 5.43 billion by 2032, at a CAGR of 12.70% during the forecast period driven by the rising demand for early-stage precision oncology, expanding utilization of non-invasive liquid biopsy platforms, increasing research investments in histone modification…

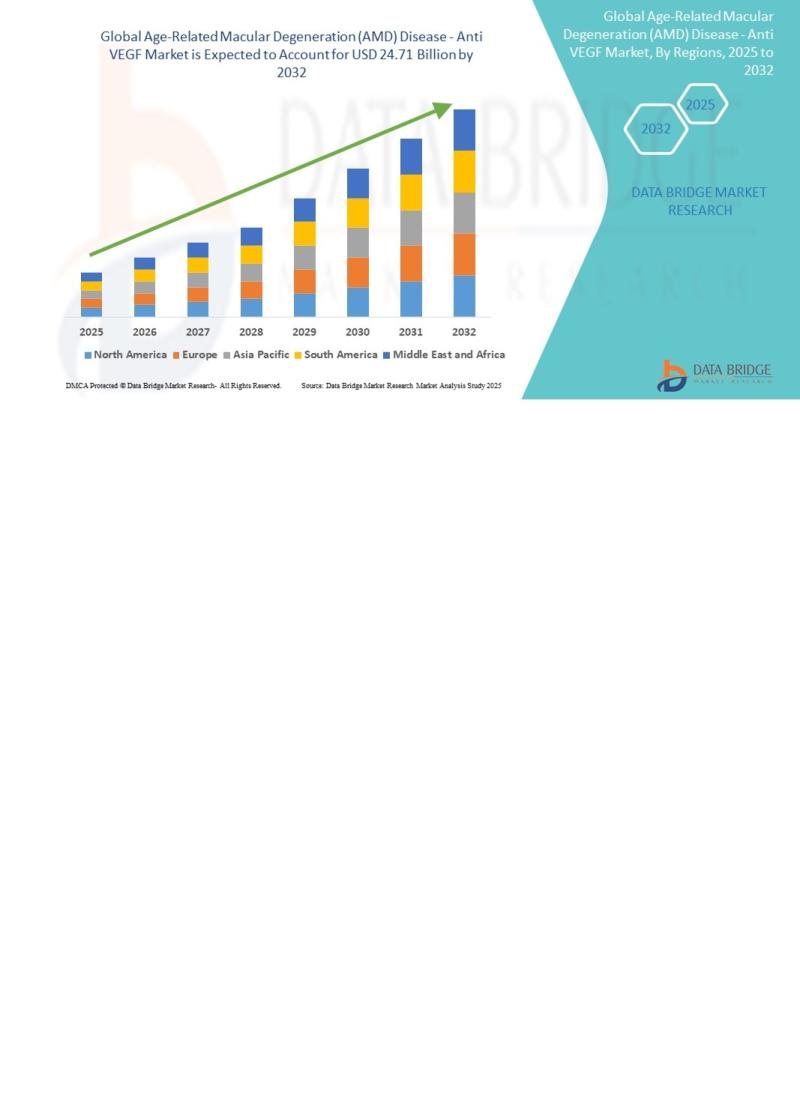

Age-Related Macular Degeneration (AMD) Anti-VEGF Therapeutics Market: Industry A …

Market Summary

As per Data Bridge Market Research analysis, the Age-Related Macular Degeneration (AMD) Disease - Anti-VEF Market was estimated at USD 15.59 billion in 2025. The market is expected to grow from USD 16.65 billion in 2026 to USD 24.71 billion in 2032, at a CAGR of 6.80% during the forecast period with driven by the rising demand for effective retinal disease therapies, increasing prevalence of age-related vision disorders, advancements…

Yogurt Powder Market Size Expected to Reach USD 1.41 Billion by 2032 at a CAGR o …

Market Summary

As per Data Bridge Market Research analysis, the Yogurt Powder Market was estimated at USD 0.28 billion in 2025. The market is expected to grow from USD 0.30 billion in 2026 to USD 1.41 billion in 2032, at a CAGR of 8.10% during the forecast period with driven by the rising demand for shelf-stable dairy ingredients, growing consumption of functional and protein-enriched foods, expansion of the food processing industry,…

Pressure Transmitter Market Size, Share & Industry Trends Analysis Report - Glob …

As per Data Bridge Market Research analysis, the Pressure Transmitter Market was estimated at USD 3.41 billion in 2025. The market is expected to grow from USD 3.54 billion in 2026 to USD 4.44 billion in 2032, at a CAGR of 3.86% during the forecast period (2026-2032), driven by the rising demand for industrial automation, increasing adoption of Industry 4.0 technologies, expansion of oil & gas and process industries, and…

More Releases for America

Stabilit America Highlights Applications of Fiberglass Roof Panels with Stabilit …

Roofing materials are very important in the realm of modern construction, as they should be long lasting, economical and attractive. Fiberglass roof panels are a few of the numerous choices among several alternatives that have received a reputation of being versatile, long life, and adaptable in various sectors. They are favored by the architects, contractors, and property developers due to their lightweight construction, resistance to weather factors, and the ease…

Deodorants Market Report by Region (North America, EMEA, Latin America, Asia)

2025 - Pristine Market Insights, a leading market research firm, announced the release of its latest and comprehensive market research report on Deodorants market. The report spans over 500 pages and delivers 10-year market forecast in US dollars (or custom currencies upon request). It provides in-depth analysis of market dynamics (drivers, opportunities, restraints), PESTLE insights, latest industry trends, and demand factors. The report includes segmented market value, share (%), compound…

Sequestrant Market Report by Region (North America, EMEA, Latin America, Asia)

2025 - Pristine Market Insights, a leading market research firm, announced the release of its latest and comprehensive market research report on Sequestrant market. The report spans over 500 pages and delivers 10-year market forecast in US dollars (or custom currencies upon request). It provides in-depth analysis of market dynamics (drivers, opportunities, restraints), PESTLE insights, latest industry trends, and demand factors. The report includes segmented market value, share (%), compound…

Buttermilk Market Study by Region (North America, Latin America, Europe, Asia, M …

2025 - Pristine Market Insights, a leading market research firm, announced the release of its latest and comprehensive market research report on Buttermilk market. The report spans over 500 pages and delivers 10-year market forecast in US dollars (or custom currencies upon request). It provides in-depth analysis of market dynamics (drivers, opportunities, restraints), PESTLE insights, latest industry trends, and demand factors. The report includes segmented market value, share (%),…

Textiles Market Analysis Report, Regional Outlook - Europe, North America, South …

Adroit Market Research has announced the addition of the “Global Textiles Market Size Status and Forecast 2025”, The report classifies the global Textiles in a precise manner to offer detailed insights about the aspects responsible for augmenting as well as restraining market growth.

This report studies the global Textiles Speaker market, analyzes and researches the Textiles Speaker development status and forecast in Europe, North America, Central America, South America, Asia Pacific…

Global Gaucher Disease Market 2018 Covering North America, South America, Europe

Gaucher Disease Market

Summary

The Global Gaucher Disease Market is defined by the presence of some of the leading competitors operating in the market, including the well-established players and new entrants, and the suppliers, vendors, and distributors. The key players are continuously focusing on expanding their geographic reach and broadening their customer base, in order to expand their product portfolio and come up with new advancements.

Gaucher Disease market size to maintain the average annual growth…