Press release

Is the Automotive Industry Accelerating Growth in the High Performance Computing Market at 12.1% CAGR

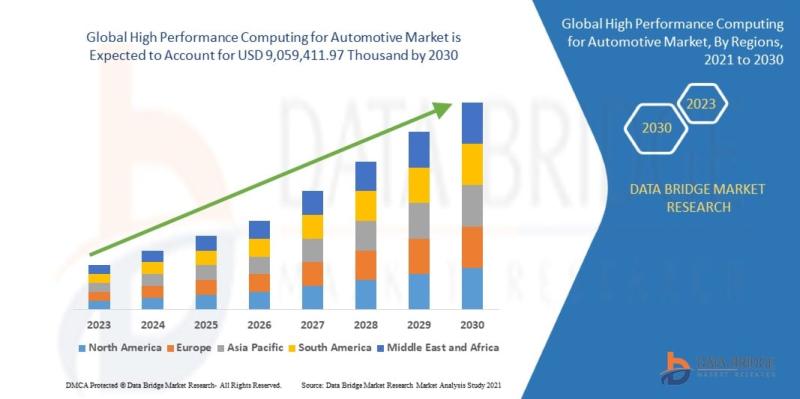

High Performance Computing for Automotive Market

Get the full PDF sample copy of the report: (Includes full table of contents, list of tables and figures, and graphs):- https://www.databridgemarketresearch.com/request-a-sample/?dbmr=global-high-performance-computing-for-automotive-market

The market is witnessing accelerated adoption of HPC platforms across automotive OEMs and Tier-1 suppliers to support autonomous driving algorithms, digital twin simulations, over-the-air software ecosystems, and advanced driver-assistance systems (ADAS). Increasing electrification of vehicles and growing computational requirements for real-time analytics are further supporting demand for scalable automotive HPC infrastructure. Regulatory emphasis on vehicle safety, emissions optimization, and cybersecurity compliance is also encouraging investments in high-performance computing environments.

Market Size & Forecast

2025 Market Size: USD 5.12 Billion

2026 Projected Market Size: USD 5.74 Billion

2030 Projected Market Size: USD 9.06 Billion

CAGR (2026-2030): 12.1%

Largest Region: North America

Fastest Growing Region: Asia-Pacific

Key Market Report Takeaways

North America accounted for the largest market share of approximately 38% due to strong autonomous vehicle R&D investments and the presence of major HPC technology providers.

Asia-Pacific is projected to register the fastest CAGR through 2030, supported by rapid EV production growth and government-backed smart mobility initiatives.

Hardware solutions, particularly GPU-accelerated computing systems, hold the highest market share owing to increasing AI workload requirements.

ADAS and autonomous driving simulation represent the dominant application segment due to extensive computational demand for sensor fusion and real-time decision-making.

Automotive OEMs remain the leading end-user segment driven by in-house software development and digital vehicle platform expansion.

Cloud-integrated HPC deployments are gaining traction as automotive companies seek scalable simulation and analytics capabilities.

AI-driven vehicle design validation and crash simulation are emerging as major computational use cases across global automotive manufacturing ecosystems.

Market Trends & Highlights

North America continues to dominate the global market due to advanced automotive software ecosystems, strong semiconductor infrastructure, and significant investments in autonomous vehicle testing.

Asia-Pacific is the fastest-growing region supported by expanding EV manufacturing capacity, smart mobility programs, and rising adoption of AI-enabled automotive platforms in China, Japan, and India.

ADAS, autonomous driving, and vehicle simulation remain the dominant application areas as automakers increase investments in sensor processing and predictive analytics.

Rising demand for connected vehicles, increasing software-defined vehicle architectures, and stricter vehicle safety regulations are key market growth drivers.

AI accelerators, GPU-based computing, edge HPC systems, and cloud-native simulation platforms are reshaping automotive computing infrastructure.

Strategic partnerships between automotive OEMs, semiconductor vendors, and cloud providers are accelerating innovation in autonomous mobility and digital engineering.

Market Dynamics

Market Drivers

Growing Adoption of Autonomous and Connected Vehicles

The increasing commercialization of autonomous driving technologies is significantly boosting demand for high-performance computing platforms. Automotive OEMs require advanced processing capabilities for real-time sensor fusion, LiDAR analytics, and AI-driven navigation systems. North America and Europe are leading autonomous vehicle testing initiatives, while China is rapidly expanding smart mobility deployments. HPC infrastructure is becoming essential for handling large-scale vehicle data processing and machine learning workloads.

Expansion of Electric Vehicle Production

The rapid global transition toward electric mobility is increasing the complexity of vehicle software and battery management systems. HPC solutions are widely used for battery simulation, thermal management analysis, and powertrain optimization. Asia-Pacific, particularly China and India, is witnessing substantial EV production expansion supported by government incentives. The integration of digital engineering tools in EV manufacturing continues to accelerate HPC adoption across automotive supply chains.

Advancements in AI and GPU Computing Technologies

Continuous innovation in GPU acceleration, AI processors, and parallel computing architectures is driving market growth. Automotive companies are deploying AI-enabled HPC systems for predictive maintenance, intelligent traffic management, and advanced simulation workloads. Technology advancements from semiconductor companies are improving computational efficiency while reducing processing latency. These innovations are enabling scalable and cost-efficient deployment of automotive HPC infrastructure.

Increasing Use of Digital Twin and Simulation Platforms

Automotive manufacturers are increasingly utilizing digital twin technologies and virtual simulation tools to reduce development timelines and improve design accuracy. HPC environments support crash simulations, aerodynamics testing, and autonomous driving scenario modeling at large scale. Europe and North America are major adopters due to high automotive R&D expenditure. Simulation-driven vehicle development is becoming a strategic requirement for reducing operational costs and accelerating innovation cycles.

Government Regulations Supporting Vehicle Safety

Stringent vehicle safety standards and emissions regulations are encouraging automotive companies to invest in computationally advanced testing environments. Regulatory frameworks related to ADAS deployment, cybersecurity, and autonomous mobility require extensive validation and software verification processes. HPC platforms enable faster compliance testing and real-time analytics capabilities. Governments across Europe, the U.S., China, and Japan are actively supporting intelligent transportation initiatives.

Market Restraints

High Infrastructure and Deployment Costs

The implementation of automotive HPC systems requires substantial investments in processors, storage infrastructure, cooling systems, and networking capabilities. Small and mid-sized automotive suppliers often face financial limitations in deploying large-scale HPC clusters. Operational expenses related to maintenance and power consumption also remain high. Cost barriers are particularly evident in emerging economies with limited digital infrastructure maturity.

Complex Integration with Legacy Automotive Systems

Many automotive manufacturers continue to operate legacy IT and engineering systems that are difficult to integrate with modern HPC environments. Compatibility issues between software platforms, simulation tools, and embedded vehicle systems increase deployment complexity. Integration challenges can delay digital transformation initiatives and increase implementation timelines. Legacy infrastructure limitations remain a key concern across traditional automotive manufacturing facilities.

Cybersecurity and Data Privacy Concerns

Automotive HPC environments process massive volumes of sensitive vehicle, consumer, and operational data. Increasing cyber threats targeting connected vehicle ecosystems are creating concerns related to data security and infrastructure vulnerability. Regulatory compliance requirements for data protection vary across regions, increasing operational complexity for multinational companies. Security investments continue to increase total ownership costs for HPC deployments.

Supply Chain Disruptions in Semiconductor Components

The market remains vulnerable to semiconductor shortages and global supply chain instability. GPU processors, advanced chips, and memory components are critical for HPC systems, making the industry dependent on limited suppliers. Geopolitical tensions and trade restrictions continue to impact semiconductor availability and pricing volatility. Supply disruptions can delay automotive production schedules and infrastructure expansion projects.

Energy Consumption and Sustainability Challenges

Large-scale HPC systems consume substantial amounts of electricity and require advanced cooling infrastructure. Rising energy prices and sustainability regulations are increasing operational pressures on automotive manufacturers and data center operators. Companies are facing growing expectations to reduce carbon emissions associated with computational workloads. Energy efficiency remains a critical challenge for scaling HPC operations globally.

Market Opportunities

Expansion of Cloud-Based Automotive HPC Platforms

Cloud-integrated HPC solutions are creating significant growth opportunities by reducing upfront infrastructure investments. Automotive companies are increasingly adopting hybrid cloud architectures for simulation, AI training, and digital engineering workloads. Cloud-based HPC platforms provide scalability, operational flexibility, and faster deployment capabilities. North America and Europe are leading adoption, while Asia-Pacific is emerging as a high-growth market.

Rising Demand for Software-Defined Vehicles

The transition toward software-defined vehicles is increasing computational requirements across vehicle architectures. Automakers are investing heavily in centralized computing platforms capable of supporting over-the-air updates and AI-driven functionalities. HPC systems play a critical role in software validation, testing, and analytics. This trend is expected to generate long-term revenue opportunities for HPC hardware and software vendors.

Strategic Partnerships Between OEMs and Technology Providers

Collaborations between automotive manufacturers, semiconductor firms, and cloud providers are accelerating innovation across autonomous mobility ecosystems. Joint ventures focused on AI computing, edge processing, and digital simulation are expanding market potential. Strategic alliances enable companies to reduce development costs and improve time-to-market efficiency. Partnerships are particularly increasing across the U.S., Germany, China, and Japan.

Growth Potential in Emerging Automotive Markets

Emerging economies in Asia-Pacific, Latin America, and the Middle East are witnessing rising investments in smart mobility infrastructure and EV manufacturing. Governments are supporting automotive digitalization through industrial modernization programs and tax incentives. Increasing urbanization and connected transportation initiatives are creating demand for scalable computing platforms. These regions offer long-term expansion opportunities for HPC solution providers.

Development of Edge AI and Real-Time Analytics

The growing use of edge computing in connected vehicles is generating new opportunities for decentralized HPC architectures. Real-time vehicle analytics, predictive maintenance, and intelligent traffic systems require low-latency processing capabilities. Automotive companies are investing in edge AI processors and distributed computing systems to enhance operational efficiency. This trend is expected to reshape future automotive computing ecosystems.

Details about the report and current availability can be viewed : https://www.databridgemarketresearch.com/reports/global-high-performance-computing-for-automotive-market

Market Challenges

Scalability Constraints in Automotive Data Processing

The exponential increase in vehicle-generated data is creating scalability challenges for automotive HPC infrastructure. Autonomous vehicles generate massive real-time data streams requiring advanced processing and storage capabilities. Many organizations struggle to efficiently scale computational resources while maintaining performance reliability. Scalability limitations may impact autonomous vehicle testing and AI training efficiency.

Shortage of Skilled HPC and AI Professionals

The market faces a growing shortage of professionals with expertise in HPC architecture, AI algorithms, and automotive software engineering. Talent gaps are particularly prominent in emerging economies and smaller automotive suppliers. Workforce limitations can slow implementation timelines and increase operational dependency on third-party vendors. The competition for specialized engineering talent continues to intensify globally.

Rapid Technological Obsolescence

Continuous advancements in processors, AI accelerators, and software frameworks create risks of rapid infrastructure obsolescence. Automotive companies must regularly upgrade systems to remain competitive and compatible with evolving technologies. Frequent technology refresh cycles increase capital expenditure requirements. Smaller organizations may face challenges in maintaining long-term infrastructure competitiveness.

Fragmented Global Regulatory Landscape

Automotive data governance, autonomous driving regulations, and cybersecurity standards vary significantly across regions. Companies operating globally must comply with multiple regulatory frameworks, increasing operational complexity and compliance costs. Regulatory uncertainty related to autonomous mobility deployment remains a challenge in several countries. Standardization gaps continue to slow cross-border technology integration.

Intense Competitive Pressure

The market is becoming increasingly competitive with the entry of semiconductor manufacturers, cloud providers, AI startups, and traditional IT vendors. Price competition and rapid innovation cycles are placing pressure on profitability margins. Established companies must continuously invest in R&D to maintain technological leadership. Market fragmentation is intensifying competitive dynamics across both hardware and software segments.

Market Segmentation & Analysis

By Component

Hardware

Hardware solutions, including GPUs, CPUs, storage systems, and networking infrastructure, account for the largest market share due to increasing computational requirements for AI and autonomous driving workloads. GPU-accelerated computing systems are widely adopted for simulation and machine learning applications. This segment is expected to maintain strong growth with a projected CAGR above 12%. North America leads hardware deployment due to strong semiconductor ecosystems.

Software

Software platforms include simulation tools, analytics platforms, workload management systems, and AI frameworks. The segment is expanding rapidly due to increasing adoption of digital twin technologies and predictive analytics. Automotive OEMs are prioritizing software-defined vehicle architectures, supporting long-term software demand. Cloud-native HPC software is emerging as a key growth area globally.

Services

Services include consulting, integration, maintenance, and managed HPC operations. Growing deployment complexity and cybersecurity requirements are increasing demand for specialized services. Managed HPC services are particularly gaining adoption among mid-sized automotive suppliers seeking cost optimization. Asia-Pacific is expected to witness strong service segment growth due to rising infrastructure modernization.

By Application

ADAS & Autonomous Driving

This is the dominant application segment due to the extensive computational power required for sensor fusion, AI training, and real-time decision-making. HPC systems are critical for processing LiDAR, radar, and camera data streams. The segment is projected to maintain the highest revenue contribution through 2030. North America and China are major deployment hubs.

Vehicle Design & Simulation

Automotive manufacturers increasingly rely on HPC systems for crash testing, aerodynamics analysis, and virtual prototyping. Simulation-driven engineering reduces development costs and accelerates product launch cycles. Europe remains a strong market due to high automotive R&D investments. The segment continues to benefit from digital engineering adoption.

Battery & Powertrain Optimization

HPC platforms are widely utilized for EV battery modeling, thermal management analysis, and powertrain efficiency optimization. Growing EV adoption is supporting strong segment expansion across Asia-Pacific and Europe. The segment is expected to witness one of the fastest growth rates during the forecast period.

By End User

Automotive OEMs

OEMs represent the leading end-user segment due to increasing investments in software-defined vehicles and autonomous mobility programs. Large automakers are establishing dedicated HPC infrastructures for simulation, AI training, and digital manufacturing. The segment benefits from strong capital investment capacity and long-term technology adoption strategies.

Tier-1 Suppliers

Tier-1 suppliers increasingly deploy HPC systems for component testing, embedded software validation, and AI algorithm development. Growing collaboration with OEMs is accelerating adoption across global automotive supply chains. Europe and Asia-Pacific are major markets for supplier-based HPC deployments.

Research Institutions & Mobility Technology Firms

Research organizations and mobility startups are utilizing HPC systems for autonomous vehicle development and transportation analytics. Public-private partnerships and government-funded mobility projects are supporting segment growth. The segment is expected to expand steadily through advanced AI research initiatives.

Get Detailed Insights Before You Buy - Request Complete Market Intelligence Now: https://www.databridgemarketresearch.com/inquire-before-buying/?dbmr=global-high-performance-computing-for-automotive-market

Regional Analysis

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America represents the largest regional market, accounting for approximately 38% of global revenue. The region benefits from advanced automotive R&D infrastructure, strong adoption of AI technologies, and the presence of major HPC solution providers. The U.S. leads regional growth due to autonomous vehicle testing programs and significant investments in connected mobility. Strong semiconductor ecosystems and cloud infrastructure further support market expansion.

Europe

Europe is a mature and steadily growing market driven by automotive engineering excellence and stringent vehicle safety regulations. Germany, the U.K., and France remain major contributors due to strong automotive manufacturing ecosystems and rising digital engineering investments. The region is witnessing increasing adoption of HPC platforms for EV development and sustainability-focused automotive innovation. Regulatory support for autonomous mobility is further supporting growth.

Asia Pacific

Asia-Pacific is the fastest-growing regional market supported by rapid industrialization, expanding EV production, and smart mobility initiatives. China dominates regional demand due to aggressive investments in autonomous driving and semiconductor manufacturing. Japan and India are also witnessing increasing HPC adoption across automotive R&D activities. Government incentives and expanding automotive manufacturing capacity are accelerating regional market growth.

Latin America

Latin America represents an emerging market characterized by gradual adoption of automotive digitalization technologies. Brazil and Mexico are key regional contributors due to growing automotive production and infrastructure modernization initiatives. Economic limitations and lower technology penetration continue to restrict rapid expansion. However, rising foreign investments are supporting long-term market potential.

Middle East & Africa

The Middle East & Africa market is experiencing steady but relatively slower growth compared to developed regions. Government investments in smart city initiatives and transportation modernization are supporting HPC adoption. Private sector participation in connected mobility projects is gradually increasing across Gulf countries. Infrastructure limitations and lower automotive manufacturing capacity remain key growth constraints.

Key Insights:

Largest Region: North America

Fastest Growing Region: Asia-Pacific

Competitive Landscape

Market Structure Overview

The global high performance computing for automotive market is moderately consolidated with the presence of major semiconductor manufacturers, cloud providers, automotive software firms, and specialized HPC infrastructure companies. Competition is strongly influenced by AI innovation, GPU acceleration technologies, cloud integration capabilities, and autonomous vehicle development expertise. Leading companies focus on advanced computing architectures and strategic partnerships to strengthen market positioning. Competitive landscape analysis highlights the strategic direction, technology leadership, and expansion capabilities of key market participants.

Key Industry Players

NVIDIA - Market leader in GPU-accelerated automotive AI computing platforms.

Intel Corporation - Strong presence in automotive processors and edge computing solutions.

Advanced Micro Devices (AMD) - Expanding GPU and AI accelerator portfolio for automotive simulation workloads.

IBM Corporation - Provides AI-integrated HPC and hybrid cloud solutions.

Hewlett Packard Enterprise (HPE) - Focused on scalable HPC infrastructure and automotive analytics.

Dell Technologies - Offers integrated HPC and edge computing platforms for automotive enterprises.

Lenovo - Expanding HPC server deployments across automotive engineering environments.

Qualcomm Technologies - Focused on connected vehicle and edge AI computing solutions.

Competitive Strategies

Companies are prioritizing AI-enabled product launches, GPU acceleration advancements, and cloud-native automotive simulation platforms to strengthen competitiveness. Strategic collaborations between automotive OEMs and semiconductor companies are accelerating autonomous mobility innovation. Mergers, acquisitions, and technology partnerships remain key strategies for expanding computational capabilities and geographic reach. Market participants are also increasing investments in edge computing, predictive analytics, and software-defined vehicle ecosystems to enhance differentiation and customer value propositions.

Emerging Players & Market Dynamics

Emerging startups and niche AI computing firms are increasing competition by offering specialized automotive simulation and edge analytics solutions. New entrants are leveraging cloud-native architectures and cost-efficient AI accelerators to disrupt traditional HPC deployment models. Venture capital investments in autonomous mobility and automotive AI continue to rise globally. The market is increasingly characterized by digital transformation initiatives, rapid innovation cycles, and expanding software-driven automotive ecosystems.

Latest Developments

January 2025 - NVIDIA: Expanded its automotive AI and simulation ecosystem with next-generation autonomous vehicle computing platforms, strengthening GPU demand in automotive HPC environments.

October 2024 - Intel Corporation: Announced advancements in AI-enabled edge computing platforms for connected vehicles, supporting real-time automotive analytics and low-latency processing capabilities.

June 2024 - Advanced Micro Devices (AMD): Expanded high-performance GPU offerings targeting automotive simulation and AI workloads, intensifying competition in automotive HPC acceleration technologies.

March 2024 - Hewlett Packard Enterprise (HPE): Strengthened hybrid cloud HPC solutions for automotive engineering and digital twin applications, supporting scalable simulation infrastructure.

November 2023 - Qualcomm Technologies: Expanded collaborations with automotive OEMs for software-defined vehicle platforms, increasing demand for edge AI and centralized computing architectures.

August 2023 - IBM Corporation: Enhanced AI-integrated cloud computing solutions for industrial and automotive simulation environments, supporting predictive analytics and autonomous mobility applications.

May 2023 - Dell Technologies: Introduced upgraded HPC infrastructure solutions optimized for AI-driven automotive engineering and advanced vehicle testing applications.

February 2023 - Lenovo: Expanded global HPC server deployment initiatives targeting automotive R&D centers in Asia-Pacific and Europe, strengthening regional computational infrastructure capabilities.

Check out more related studies published by Data Bridge Market Research:

https://www.databridgemarketresearch.com/reports/global-cybersecurity-market

https://www.databridgemarketresearch.com/reports/global-artificial-intelligence-market

https://www.databridgemarketresearch.com/reports/japan-business-process-as-a-service-bpaas-market

https://www.databridgemarketresearch.com/reports/global-smart-cities-market

https://www.databridgemarketresearch.com/reports/global-soft-skills-training-market

Contact Us:

Data Bridge Market Research

US: +1 614 591 3140

UK: +44 845 154 9652

APAC : +653 1251 975

Email:- corporatesales@databridgemarketresearch.com

About Data Bridge Market Research:

Data Bridge Market Research set forth itself as an unconventional and neoteric market research and consulting firm with an unparalleled level of resilience and integrated approaches. We are determined to unearth the best market opportunities and foster efficient information for your business to thrive in the market. Data Bridge endeavors to provide appropriate solutions to the complex business challenges and initiates an effortless decision-making process. Data Bridge is an aftermath of sheer wisdom and experience which was formulated and framed in the year 2015 in Pune.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Is the Automotive Industry Accelerating Growth in the High Performance Computing Market at 12.1% CAGR here

News-ID: 4505320 • Views: …

More Releases from Data Bridge Market Research

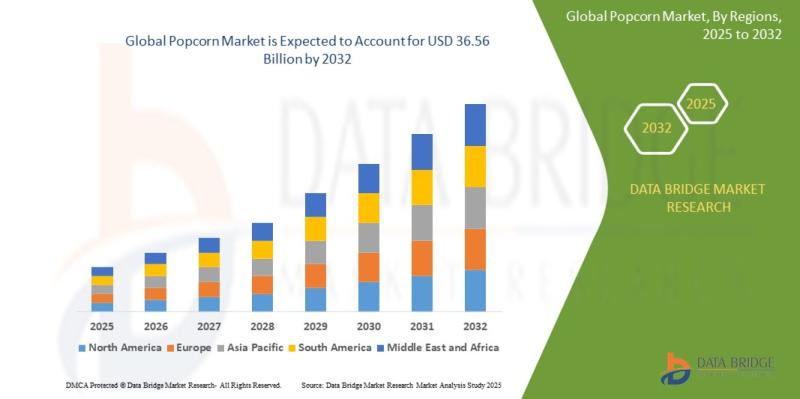

Is the Popcorn Market Evolving with Innovation in Organic and Premium Snack Prod …

As per Data Bridge Market Research analysis, the Popcorn Market was estimated at USD 23.22 billion in 2025. The market is expected to grow from USD 24.78 billion in 2026 to USD 36.56 billion in 2032, at a CAGR of 6.70% during the forecast period, driven by the rising demand for convenient ready-to-eat snacks, increasing consumer preference for healthy low-calorie food products, expansion of flavored and premium popcorn offerings, and…

Can AI and Automation Push the Background Check Market Beyond USD 39.60 Billion …

As per Data Bridge Market Research analysis, the Background Check Market was estimated at USD 17.47 billion in 2025. The market is expected to grow from USD 19.64 billion in 2026 to USD 39.60 billion in 2032, at a CAGR of 12.40% during the forecast period with driven by the rising demand for workforce verification, increasing concerns regarding fraud prevention and workplace security, rapid adoption of AI-enabled screening technologies, and…

Is the Wine Market Growing as Premium and Organic Wines Gain Popularit

As per Data Bridge Market Research analysis, the Wine Market was estimated at USD 413.67 billion in 2025. The market is expected to grow from USD 430.34 billion in 2026 to USD 545.47 billion in 2032, at a CAGR of 4.03% during the forecast period with driven by the rising demand for premium and organic wine offerings.

The global wine market is witnessing stable expansion supported by increasing consumer preference for…

Pharmaceutical Logistics Market Report 2032: Market Valued at USD 528.67 Billion …

As per Data Bridge Market Research analysis, the Pharmaceutical Logistics Market was estimated at USD 292.95 million in 2025. The market is expected to grow from USD 269.25 million in 2024 to USD 528.67 million by 2032, at a CAGR of 8.80% during the forecast period with driven by the rising demand for temperature-sensitive pharmaceutical products, expansion of biologics and vaccine distribution networks, increasing adoption of cold chain logistics technologies,…

More Releases for HPC

Surging Data Volumes Drive Growth in HPC Data Management Market: An Emerging Dri …

The HPC Data Management Market Report by The Business Research Company delivers a detailed market assessment, covering size projections from 2025 to 2034. This report explores crucial market trends, major drivers and market segmentation by [key segment categories].

What Is the Projected Growth of the HPC Data Management Market?

In recent times, the market size of HPC data management has seen a swift expansion. The market, which is set to escalate from…

Global High-performance Computing (HPC) Market Size by Application, Type, and Ge …

According to Market Research Intellect, the global High-performance Computing (HPC) market under the Internet, Communication and Technology category is expected to register notable growth from 2025 to 2032. Key drivers such as advancing technologies, changing consumer behavior, and evolving market dynamics are poised to shape the trajectory of this market throughout the forecast period.

The High-Performance Computing (HPC) market is experiencing rapid growth, driven by the increasing need for advanced computing…

High Performance Computing (HPC) Services Market Size Analysis by Application, T …

According to Market Research Intellect, the global High Performance Computing (HPC) Services market under the Internet, Communication and Technology category is expected to register notable growth from 2025 to 2032. Key drivers such as advancing technologies, changing consumer behavior, and evolving market dynamics are poised to shape the trajectory of this market throughout the forecast period.

The market for High Performance Computing (HPC) services is expanding rapidly due to the growing…

Global Artificial Intelligence HPC Cloud Market Size by Application, Type, and G …

USA, New Jersey- According to Market Research Intellect, the global Artificial Intelligence HPC Cloud market in the Internet, Communication and Technology category is projected to witness significant growth from 2025 to 2032. Market dynamics, technological advancements, and evolving consumer demand are expected to drive expansion during this period.

As more sectors embrace AI to manage intricate, data-intensive activities, the market for artificial intelligence HPC (High-Performance Computing) cloud computing is growing quickly.…

High-Performance Computing (HPC) Market: A Comprehensive Overview

The global High-Performance Computing (HPC) market was valued at approximately USD 50.02 billion in 2023 and is projected to reach around USD 109.99 billion by 2032, growing at a compound annual growth rate (CAGR) of 9.2% during the forecast period.

High-Performance Computing (HPC) Market Overview

High-Performance Computing systems are essential for processing complex computations and large datasets across various industries, including healthcare, finance, manufacturing, and scientific research. The market's…

Transforming the HPC Data Management Market in 2025: Surging Data Volumes Drive …

What Is the Expected Size and Growth Rate of the HPC Data Management Market?

The HPC data management market is expected to grow from $36.81 billion in 2024 to $43.65 billion in 2025, with a compound annual growth rate (CAGR) of 18.6%. This growth is driven by increasing demand for data storage and management, rising investments, the increasing complexity of data, the rise of artificial intelligence (AI), and the expansion of…