Press release

Europe Dental Implants Market Set to Reach USD 3.28 Billion by 2034: Germany, Italy, and Spain Drive Regional Momentum

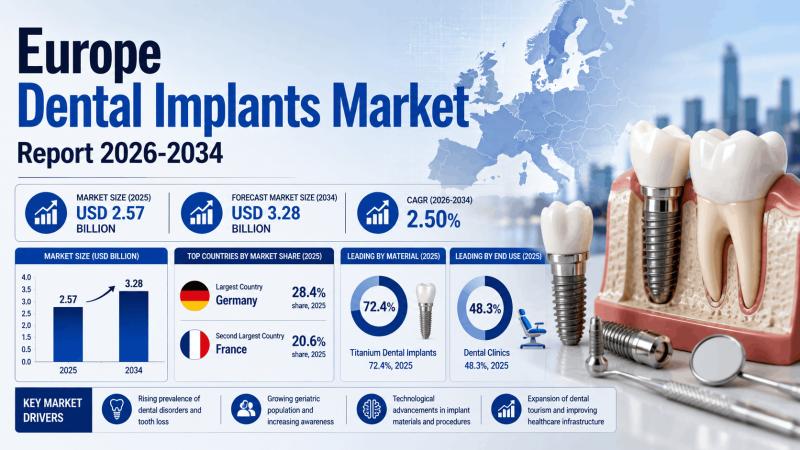

Europe Dental Implants Market Report 2026

Read the full report with the list of TOC: https://www.imarcgroup.com/europe-dental-implants-market

With more than one-fifth of Europeans (22.0%) aged 65 or older in 2025 according to Eurostat data, tooth loss is a clinical reality for an increasing share of the population, directly feeding demand for implant-based restorations. Simultaneously, the shift toward same-day procedures, AI-assisted surgical planning, and metal-free zirconia implants is expanding the addressable patient population and premium revenue opportunities for manufacturers.

Europe Dental Implants Market Size and Growth Trajectory at a Glance

The market's compound growth rate of 2.50% reflects a mature Western European base that still generates significant, high-value volume, combined with faster-growing Central and Eastern European frontiers. At a glance, the market's defining data points for 2025 are:

The market was valued at USD 2.57 Billion in 2025 and is forecast to reach USD 3.28 Billion by 2034, at a CAGR of 2.50% over 2026-2034.

Germany holds the largest national share at 28.4% as of 2025.

Titanium dental implants lead the material segment with a 72.4% share in 2025.

Dental clinics dominate end-use channels, accounting for 48.3% of total procedure volumes in 2025.

The absolute value expansion of approximately USD 710 Million over the forecast window represents a meaningful commercial opportunity across premium implant systems, digital workflow platforms, and specialty materials.

What Is Driving Growth in the Europe Dental Implants Market?

Several structural forces are working in concert to support steady market expansion through 2034:

• Demographic ageing and rising edentulism: With over 22% of Europeans aged 65 and above, the prevalence of tooth loss continues to climb. Implants represent the clinical gold standard for permanent tooth replacement, and procedure volumes are expanding with this demographic shift.

• Digital implantology adoption: The integration of cone-beam computed tomography (CBCT), intraoral digital scanners, and AI-driven surgical planning tools has significantly reduced procedure complexity. These technologies allow clinicians to plan implant placement in three dimensions, minimise complications, and offer same-day immediate loading protocols that were previously unavailable to most patients.

• Expanding private dental insurance coverage: Increasing enrolment in private dental plans across Germany, France, and the United Kingdom is lowering out-of-pocket cost barriers, particularly for patients in the 45-65 age bracket, who represent a high-expenditure cosmetic dental demographic.

• Dental tourism volume contribution: Countries including Hungary, Poland, and Croatia offer implant procedures at 40-60% below Western European pricing, which expands total pan-European procedure volumes and generates incremental demand beyond domestic patient flows.

• Zirconia premiumisation: Patient preference for metal-free restorations is driving adoption of zirconium implants, which carry higher average selling prices and above-average margins for manufacturers.

The primary restraints include high treatment costs that limit access for lower-income patient segments, and divergent national reimbursement policies that create uneven market conditions. Germany and France provide partial public reimbursement, while the UK's NHS does not routinely fund implant procedures, constraining a portion of the UK's addressable patient base.

How Are Germany, Italy, and Spain Performing in the Europe Dental Implants Market?

Germany: The Market Leader at 28.4% Share

Germany commands the largest national share in the European dental implants market at 28.4% in 2025, and its leadership position is built on systemic foundations rather than single factors. The country operates approximately 64,000 registered dental practices, benefits from one of Europe's highest implant-procedure-per-capita rates, and maintains a partial insurance reimbursement framework that meaningfully reduces patient cost exposure compared to purely private-pay markets.

Germany is also home to major implant manufacturers and a highly organised dental care ecosystem. Digital workflow adoption is among the continent's highest, with CBCT systems and guided surgery platforms widely deployed in tier-one practices. Dental Service Organisation (DSO) consolidation is accelerating across the country, creating multi-site networks that standardise implant platforms and drive preferred-supplier relationships with global manufacturers.

Italy: An Ageing Population Fuelling Implant Demand

Italy holds a 14.2% share of the European dental implants market in 2025, underpinned by one of the continent's oldest population profiles. With approximately 23.5% of Italy's population aged 65 and above, the demographic driver for implant demand is particularly acute. Italian patients demonstrate high dental awareness, and the country operates a well-established network of private dental clinics where premium restorative procedures are routine.

Italy also plays an active role in the European dental tourism corridor, functioning as both an origin and destination market for implant procedures. The country hosts notable domestic manufacturers, including Sweden & Martina S.p.A. and Biotec S.r.l., which serve the Italian market with specialised products, including bone-level micro-implants. The intersection of domestic demand, domestic manufacturing capacity, and tourism flows positions Italy as a distinct and growing contributor to European market revenues through 2034.

Spain: Dental Tourism Hub and a Growing DSO Ecosystem

Spain accounts for 10.4% of European market revenues in 2025 and represents one of the continent's most dynamic growth stories at the country level. The country functions as a leading dental tourism destination within Europe, attracting patients from Northern and Western Europe seeking high-quality implant procedures at comparatively lower costs. This tourism infrastructure is driving procedure volume growth and creating commercial opportunity for implant suppliers operating through clinic networks.

The expansion of implant-focused DSO chains across Spain is a defining structural trend. These multi-site organisations standardise implant platforms, negotiate bulk purchasing agreements, and create consistent demand for preferred global and regional manufacturers. Spain's growing small and medium enterprise dental sector is also contributing to broader adoption of digital implant workflows, particularly among younger, technology-forward practitioners.

Download a sample copy of the report: https://www.imarcgroup.com/europe-dental-implants-market/requestsample

Market Segmentation: Materials and End-Use Channels

By Material

Titanium dental implants retain a dominant 72.4% share in 2025, reflecting decades of peer-reviewed clinical validation, superior osseointegration characteristics, regulatory acceptance across all major European healthcare frameworks, and cost-effectiveness across patient demographics. Their clinical record spanning over 40 years makes titanium the default choice for the majority of implantologists and patients.

Zirconium dental implants hold a 27.6% share in 2025 but represent the market's fastest-growing segment. Patient demand for metal-free restorations, growing clinical evidence supporting Y-TZP osseointegration performance, and the commercial availability of second-generation monolithic zirconia systems are all expanding the clinical indications for this segment. Manufacturers including Straumann (PURE Ceramic) and CeraRoot have addressed earlier fracture risk concerns through gradient multi-layer zirconia architectures, opening posterior high-load applications for the first time.

By End Use

Dental clinics lead end-use channels with a 48.3% share in 2025, driven by the outpatient and elective nature of most implant procedures and the high density of specialist implant practices across Western Europe. The deployment of same-day implant protocols in outpatient settings is reinforcing this channel's dominance.

Hospitals account for 28.6% of the market, primarily serving complex implant cases requiring general anaesthesia or multi-disciplinary surgical coordination. Academic and research institutes hold a 14.4% share, reflecting Europe's strong tradition of clinical implantology research and the dual training-and-patient-care role of university dental schools.

Which Companies Are Leading the Europe Dental Implants Industry?

The competitive landscape concentrates around a small number of global manufacturers that collectively account for approximately 60-65% of total European revenues in 2025. Key players include:

• Institut Straumann AG: Market leader with a multi-brand strategy spanning Straumann (premium), Neodent (value-premium), and Medentika (value), combined with the SLActive hydrophilic surface technology platform and a full digital workflow ecosystem through Dental Wings.

• Dentsply Sirona: Operates Ankylos, Astra Tech EV, and XiVE implant lines, backed by the Primescan intraoral scanner and DS Core integrated digital platform. Strong penetration in Germany and France through hospital and clinic networks.

• Envista (Nobel Biocare): Leads in full-arch immediate loading protocols through the All-on-4 system, with particular strength across Southern European markets.

• ZimVie Inc.: Serves hospital-grade implant requirements and bone augmentation segments.

• Osstem Implant: A challenger in value-to-mid segment pricing, executing an aggressive expansion strategy across Central and Eastern Europe.

Emerging Trends Reshaping the European Dental Implants Industry

Three trends are altering the competitive and clinical landscape at a pace that will matter to manufacturers and investors through 2034.

AI-assisted treatment planning is moving from university hospital pilots into broader clinical adoption. Platforms integrating CBCT scan data automate implant positioning, identify anatomical risk zones, and simulate prosthetic outcomes before any surgical intervention. This capability is raising procedural confidence and expanding the population of patients eligible for complex multi-implant cases.

DSO consolidation is restructuring purchasing power across Germany, Spain, and the United Kingdom. As private equity-backed networks including those backed by Nordic Capital and KKR scale their clinic footprints, they are concentrating procurement into preferred-supplier agreements that favour manufacturers with multi-tier brand coverage and integrated clinical training programmes.

The zirconia material science revolution is the third vector. Second-generation monolithic zirconia systems, commercially available in Europe since 2022-2023, have largely resolved the fracture risk concerns that historically limited metal-free implants to anterior aesthetic applications. As these systems gain clinical confidence, they will progressively expand into posterior positions, creating a premium pricing opportunity that the market is only beginning to realise.

Speak to an Analyst: https://www.imarcgroup.com/request?type=report&id=2648&flag=C

What Does the Future Hold for the Europe Dental Implants Market Through 2034?

The forecast trajectory of USD 3.28 Billion by 2034 reflects a market that is evolving structurally, not just growing incrementally. Western European markets will continue delivering a stable, high-value base of procedure volumes, while Central and Eastern European markets, including Poland, Romania, and the Czech Republic, are forecast to grow at 5-7% CAGRs over the same period, well above the continental average of 2.50%.

Three forces will most decisively shape the market's character by 2034: DSO consolidation concentrating purchasing power; zirconia material advances unlocking the posterior load-bearing segment; and digital workflow platforms shifting competitive advantage from hardware components toward integrated software ecosystems and outcomes-based clinical models.

According to IMARC Group's latest research, the Europe dental implants market is well-positioned to complete its transition from a hardware-centric medical device category into a digital clinical solution ecosystem, where manufacturers compete on AI-driven planning capabilities, full-arch restorative protocols, and evidence-backed outcome analytics rather than on implant component specifications alone.

Media & Sales Contact

IMARC Group,

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No: (D) +91 120 433 0800

United States: +1-201971-6302

About IMARC Group

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Europe Dental Implants Market Set to Reach USD 3.28 Billion by 2034: Germany, Italy, and Spain Drive Regional Momentum here

News-ID: 4504910 • Views: …

More Releases from IMARC Group

Global Forage Market to Reach USD 136.1 Billion by 2034: Key Growth Drivers, Seg …

The global forage market sits at the foundation of the world's livestock economy, and its growth trajectory reflects the compounding pressures of population expansion, rising protein consumption, and a sweeping shift toward sustainable agricultural practice. The market reached USD 97.6 Billion in 2025 and is forecast to climb to USD 136.1 Billion by 2034, advancing at a CAGR of 3.77% during 2026-2034. That measured but consistent growth rate tells a…

Germany Data Center Market Size, Share, and Forecast 2034: Cloud Adoption, GDPR …

Germany has cemented its position as Europe's most important data center destination, and the numbers confirm it. The Germany data center market reached USD 10.5 Billion in 2025 and is on a clear trajectory to more than double, reaching USD 22.4 Billion by 2034 at a steady CAGR of 8.57% over the forecast period 2026-2034. This growth is not driven by a single trend but by a convergence of structural…

Brazil Electric Vehicle Market to Reach 844.1 Thousand Units by 2034: Growth Dri …

Brazil's electric vehicle industry is at an inflection point. Fuelled by aggressive government incentives, surging consumer demand, rapid charging infrastructure expansion, and a wave of Chinese manufacturers entering with competitive pricing, the Brazil electric vehicle market is scaling at a pace that few emerging economies can match. The market recorded 146.0 thousand units in 2025 and is projected to reach 844.1 thousand units by 2034, growing at a remarkable CAGR…

Copper Sulfate Pentahydrate Production Plant Cost DPR & Unit Setup 2026: Feasibi …

Setting up a copper sulfate pentahydrate production plant positions investors in one of the most fundamental and indispensable segments of the global specialty inorganic chemicals market, backed by sustained demand driven by the growing focus on sustainable farming practices, rising adoption of integrated pest management strategies, expanding water treatment infrastructure, and increasing applications in electroplating and mineral processing. As industries worldwide intensify agricultural productivity, scale water purification systems, and expand…

More Releases for Europe

2019 Strategy Consulting Market Analysis | McKinsey, The Boston Consulting Group …

Strategy Consulting Market reports also offer important insights which help the industry experts, product managers, CEOs, and business executives to draft their policies on various parameters including expansion, acquisition, and new product launch as well as analyzing and understanding the market trends

Need for strategic planning in highly competitive environment and to develop business capabilities to meet & exceed the emerging requirements are the major drivers which help in surging…

Strategy Consulting Market 2025 | Analysis By Top Key Players: Booz & Co. , Rola …

Global Strategy Consulting Market 2019-2025, has been prepared based on an in-depth market analysis with inputs from industry experts. This report covers the market landscape and its growth prospects over the coming years. The report also includes a discussion of the key vendors operating in this market.

The key players covered in this study

McKinsey , The Boston Consulting Group , Bain & Company , Booz & Co. , Roland Berger Europe…

Digital Strategy Consulting Market is Thriving Worldwide with Deloitte, McKinsey …

A Digital Strategy is a form of strategic management and a business answer or response to a digital question, often best addressed as part of an overall business strategy. A digital strategy is often characterized by the application of new technologies to existing business activity and focus on the enablement of new digital capabilities to their business.

A new report as a Digital Strategy Consulting market that includes a comprehensive analysis…

Strategy Consulting Market 2019: By McKinsey, The Boston Consulting Group, Bain …

This report studies the global Strategy Consulting market, analyzes and researches the Strategy Consulting development status and forecast in United States, EU, Japan, China, India and Southeast Asia. This report focuses on the top players in global market, like

• McKinsey

• The Boston Consulting Group

• Bain & Company

• Booz & Co.

• Roland Berger Europe

• Oliver Wyman Europe

• A.T. Kearney Europe

• Deloitte

• Accenture Europe

Get Sample Report@ https://www.reporthive.com/enquiry.php?id=1247388&req_type=smpl&utm_source=AB

Market segment by Type, the product can be split into

• Operations Consultants

• Business Strategy Consultants

• Investment Consultants

• Sales and…

Strategy Consulting Market Analysis 2018: McKinsey, The Boston Consulting Group, …

Orbis Research Present’s “Global Strategy Consulting Market” magnify the decision making potentiality and helps to create an effective counter strategies to gain competitive advantage.

The global Strategy Consulting status, future forecast, growth opportunity, key market and key players. The study objectives are to present the Strategy Consulting development in United States, Europe and China.

In 2017, the global Strategy Consulting market size was million US$ and it is expected to reach million…

Influenza Vaccination Market Global Forecast 2018-25 Estimated with Top Key Play …

UpMarketResearch published an exclusive report on “Influenza Vaccination market” delivering key insights and providing a competitive advantage to clients through a detailed report. The report contains 115 pages which highly exhibits on current market analysis scenario, upcoming as well as future opportunities, revenue growth, pricing and profitability. This report focuses on the Influenza Vaccination market, especially in North America, Europe and Asia-Pacific, South America, Middle East and Africa. This…