Press release

Data Center Chip Market Size to Reach USD 18.8 Billion by 2034 | With a 5.00% CAGR

Data Center Chip Market

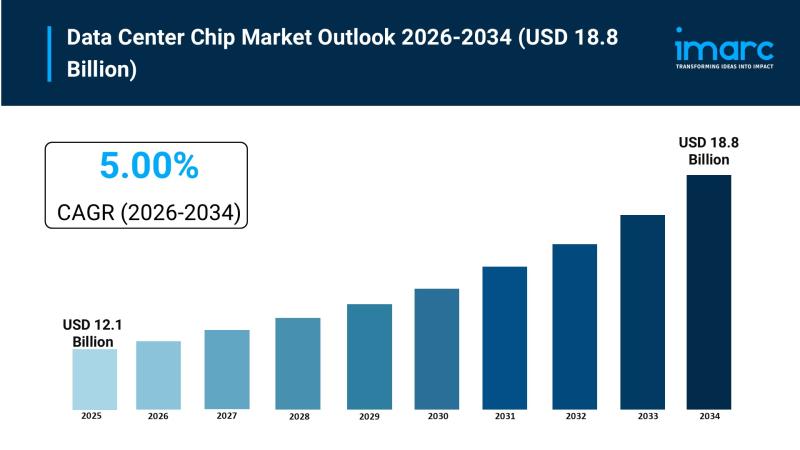

According to IMARC Group's latest research publication, "Data Center Chip Market: Global Industry Trends, Share, Size, Growth, Opportunity and Forecast 2026-2034", The global data center chip market size reached USD 12.1 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 18.8 Billion by 2034, exhibiting a growth rate (CAGR) of 5.00% during 2026-2034.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Grab a sample PDF of this report: https://www.imarcgroup.com/data-center-chip-market/requestsample

How AI is Reshaping the Future of the Data Center Chip Market

● AI training and inference workloads are fueling unprecedented GPU demand, with NVIDIA reporting USD 115.2 billion in data center revenue in fiscal year 2025, as generative AI and large language model deployments require highly parallel semiconductor architectures that conventional CPUs cannot cost-effectively deliver.

● Government programs like the U.S. CHIPS and Science Act, committing USD 52.7 billion to domestic semiconductor manufacturing, are directly incentivizing chip production capacity for AI-ready data centers, with U.S.-based semiconductor capacity projected to increase by 203% through the next decade.

● Companies like NVIDIA are co-developing full-stack AI infrastructure with hyperscalers, including a 7 MW reference architecture for the GB200 NVL72 platform that reduces implementation time by up to 50%, enabling faster deployment of AI-optimized data center chip environments.

● AI ASICs developed by Google, Amazon, and Microsoft for proprietary hyperscale workloads are reducing dependence on third-party silicon, with AI ASIC revenue expected to reach USD 84.5 billion in the near term as cloud providers pursue vertical integration and cost control across their chip procurement strategies.

● Infineon Technologies, in collaboration with NVIDIA, developed an 800V High Voltage Direct Current (HVDC) architecture that eliminates legacy 48V data center power systems, allowing facilities to run significantly denser AI workloads while reducing energy losses and ensuring reliable power delivery to next-generation GPU clusters.

Key Trends in the Data Center Chip Market

● GPU Dominance Driven by AI Workload Explosion: GPUs continue to command the largest share of the data center chip market, accounting for approximately 57% of total market revenue, with NVIDIA holding roughly 85% of AI accelerator revenue within this segment. The Blackwell architecture delivers 30 times faster AI inference than its predecessor, and the follow-on Vera Rubin platform is expected to deliver 3.3 times the performance of Blackwell Ultra, further cementing GPU supremacy across hyperscale training and inference environments.

● Rise of Custom Silicon and ASICs Among Hyperscalers: Cloud service providers are accelerating investment in application-specific integrated circuits (ASICs) and domain-specific architectures (DSAs) to reduce reliance on third-party GPUs. Google's Tensor Processing Units (TPUs), Amazon's Trainium2 and Graviton4 processors, and Microsoft's Azure Maia 100 AI Accelerator represent a structural shift toward purpose-built chip procurement, with AI ASIC revenue growing rapidly as hyperscalers pursue performance optimization at scale.

● Advanced Semiconductor Process Nodes Enabling Higher Density: The adoption of 7nm and 5nm process technologies continues to reshape data center chip performance, enabling higher transistor density, improved throughput, and materially lower power consumption per compute unit. Intel's Xeon 6 P-core series delivered approximately 1.4 times the performance of its previous generation, while chiplet-based processor architectures and heterogeneous computing integration are becoming standard design approaches for next-generation server platforms.

● 5G and IoT Expansion Amplifying Edge Chip Demand: The rapid global expansion of 5G infrastructure, with market penetration expected to grow substantially through the end of the decade, is generating enormous volumes of data from connected IoT devices that must be processed at the edge. This is driving demand for compact, low-latency data center chips deployed in edge and micro data center configurations, expanding the addressable market well beyond traditional hyperscale facilities.

● Geopolitical Realignment Reshaping Semiconductor Supply Chains: Export restrictions, tariff pressures, and national security considerations are incentivizing domestic semiconductor manufacturing investments across the United States, Europe, and Asia. The EU AI Continent Action Plan, published in April 2025, established AI Factories and Gigafactories to close Europe's compute deficit, while India's ISM 2.0 framework and a proposed INR 1 trillion semiconductor fund are accelerating the country's transition from chip consumer to chip contributor in the global data center supply chain.

Growth Factors in the Data Center Chip Market

● Surging Cloud Computing Adoption Across Enterprises: The extensive utilization of cloud computing services by businesses and consumers is among the primary factors driving demand for advanced data center chips. Amazon Web Services, Microsoft Azure, and Google Cloud collectively generated over USD 250 billion in cloud service revenue in a recent period, with chip procurement embedded throughout every tier of their infrastructure. As cloud service providers expand their offerings, the volume of chips required for virtualization, storage, networking, and AI workloads continues to scale proportionally.

● Proliferation of AI and Machine Learning Applications: The escalating demand for advanced data center chips in AI and ML algorithms to process and analyze vast datasets is a central growth driver across industries including healthcare, retail, finance, and autonomous vehicles. Hyperscalers collectively committed over USD 390 billion in AI data center capital expenditure in 2025, with the Stargate initiative alone targeting USD 500 billion in large-scale AI infrastructure, underscoring the scale of chip procurement now required to support generative AI and LLM deployments globally.

● Government Schemes and National Semiconductor Missions: Policy frameworks across major economies are directly accelerating data center chip market growth. India's Union Budget 2026-27 proposed a tax holiday until 2047 for foreign companies providing cloud services from Indian data centers, while increasing the Electronics Components Manufacturing Scheme allocation from approximately INR 22,000 crore to INR 40,000 crore. Micron's USD 2.75 billion facility in Gujarat began partial operations in 2025 under India Semiconductor Mission support, reinforcing the government's strategy to attract global chip manufacturers and diversify supply chains.

● Large Data Center Build-Out and Hyperscale Expansion: Large data centers account for approximately 72% of data center chip market revenue, driven by the economics of AI infrastructure requiring racks of hundreds or thousands of tightly networked GPUs operating with sub-microsecond interconnect latency. Over 600 new hyperscale data centers are projected to be built globally in the near term, and Microsoft alone committed USD 19 billion to Canadian AI infrastructure, signaling a sustained multi-year capital expenditure runway for chip vendors serving hyperscale operators.

● BFSI Sector Driving Chip Demand for Secure Data Processing: The BFSI industry's extensive utilization of data centers to analyze and process financial transactions, customer data, and sensitive information securely is generating consistent demand for advanced data center chips. Partnerships such as IBM Corporation's four-year agreement with BPER Banca Group to accelerate the bank's hybrid cloud strategy, combining IBM Cloud for Financial Services with IBM z16 infrastructure, illustrate how large financial institutions are embedding chip-intensive infrastructure at the core of their digital transformation programs.

Ask analyst of customized report: https://www.imarcgroup.com/request?type=report&id=5057&flag=E

Leading Companies Operating in the Global Data Center Chip Industry:

● Achronix Semiconductor Corporation

● Advanced Micro Devices Inc.

● Arm Limited

● Broadcom Inc.

● Fujitsu Limited

● Intel Corporation

● Marvell

● Micron Technology, Inc.

● NVIDIA Corporation

Data Center Chip Market Report Segmentation:

Breakup By Chip Type:

● GPU

● ASIC

● FPGA

● CPU

● Others

GPU accounts for the majority of shares on account of its unmatched parallel processing capabilities for AI training, machine learning, and scientific simulation workloads, with data centers relying on GPU clusters to handle the matrix operations and large-scale computations required by neural network architectures.

Breakup By Data Center Size:

● Small and Medium Size

● Large Size

Large size data centers hold the dominant share owing to their extensive utilization for managing massive amounts of data, high infrastructure requirements, and significant computing power demands associated with hyperscale cloud and AI deployments.

Breakup By Industry Vertical:

● BFSI

● Manufacturing

● Government

● IT and Telecom

● Retail

● Transportation

● Energy and Utilities

● Others

BFSI accounts for the largest market share on account of the extensive utilization of data centers in the sector to analyze and process financial transactions, customer data, and sensitive information securely, making advanced chip infrastructure a non-negotiable operational requirement.

Breakup By Region:

● North America (United States, Canada)

● Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

● Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

● Latin America (Brazil, Mexico, Others)

● Middle East and Africa

North America enjoys the leading position owing to the development of advanced telecommunications infrastructure, the inflating investments in cloud computing, the extensive utilization of data-intensive applications, and the concentration of leading semiconductor companies and hyperscale cloud operators driving sustained chip procurement at scale.

Recent News and Developments in the Data Center Chip Market

● March 2026: India unveiled a proposed INR 1 trillion semiconductor fund under the ISM 2.0 framework, expanding financial support for chip fabrication, design, and supply chain development, building on the India Semiconductor Mission's earlier USD 10 billion outlay to accelerate the country's transition into a global semiconductor manufacturing hub.

● February 2026: India's Union Budget 2026-27 proposed a tax holiday until 2047 for foreign companies providing cloud services using data center infrastructure based in India, while increasing the Electronics Components Manufacturing Scheme allocation to INR 40,000 crore to sustain momentum across the domestic chip and electronics ecosystem.

● November 2025: Microsoft launched its Arm-based Cobalt 200 CPU for Azure, delivering a 50% performance improvement over its predecessor and optimized for cloud workloads, improving data center efficiency and security across its hyperscale infrastructure.

● October 2025: Arm joined the Open Compute Project board and introduced a vendor-neutral chiplet standard to enable open, modular AI data centers and reduce dependency on proprietary server chip designs across the global hyperscale industry.

● May 2025: Intel Corporation announced the release of Arc Pro B60 and B50 GPUs at Computex 2025 to support AI inference, professional visualization, and compute tasks, while also expanding deployment options for Gaudi 3 AI accelerators to improve AI processing performance across enterprise and cloud data center environments

● May 2025: Infineon Technologies, in collaboration with NVIDIA, developed the 800V HVDC architecture to eliminate legacy data center power systems, enabling significantly denser AI workloads while reducing energy loss and ensuring reliable power delivery to next-generation GPU server configurations.

● April 2025: The EU AI Continent Action Plan established AI Factories, Gigafactories, and the Invest AI Facility, backed by the EU's Digital Europe Programme earmarking EUR 2.1 billion for AI infrastructure, as part of Europe's broader strategy to reduce its compute deficit and increase strategic participation in the global data center chip market.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Data Center Chip Market Size to Reach USD 18.8 Billion by 2034 | With a 5.00% CAGR here

News-ID: 4502492 • Views: …

More Releases from IMARC Group

US Medical Tourism Market Size Growth, Industry Trends & Forecast 2034

The latest report by IMARC Group, titled "United States Medical Tourism Market Size, Share, Trends and Forecast by Treatment Type, Service Provider, and Region, 2026-2034", offers a comprehensive analysis of the industry, which comprises insights on the global cheese market. The report also includes competitor and regional analysis

United States Medical Tourism Market Size, Growth, and Forecast (2026-2034)

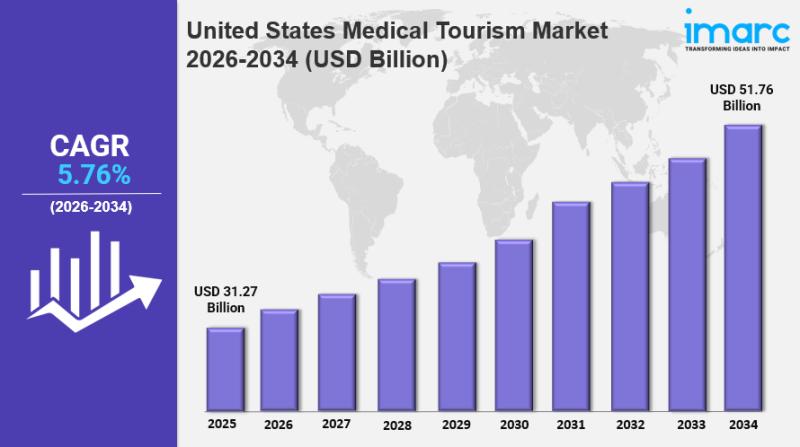

The United States medical tourism market size was valued at USD 31.27 Billion in…

Butyl Titanate Production Plant Project Report 2026: Detailed DPR, Setup Cost an …

Setting up a butyl titanate production plant positions investors in a specialty organometallic chemicals segment driven by rising growth in polymer modification and advanced composite materials, which continues to create opportunities for butyl titanate producers. According to industrial reports, Asia-Pacific is the largest regional market, accounting for over 50% of global share. IMARC Group's comprehensive DPR report provides a complete roadmap for setting up a butyl titanate production unit, covering…

Methylchloroisothiazolinone Production Plant DPR 2026: Setup Cost, CapEx, OpEx a …

Setting up a Methylchloroisothiazolinone production plant positions investors in a specialty preservative chemicals segment driven by its strong activity against bacteria, yeast, and fungi, which continues to make it valuable in formulations where microbial stability and shelf-life protection are critical. The global methylchloroisothiazolinone market size was valued at USD 127.87 Million in 2025, and IMARC Group's comprehensive DPR report provides a complete roadmap for setting up a methylchloroisothiazolinone production unit,…

Taiwan Data Center Market Size Growth, Industry Trends & Forecast to 2034

IMARC Group has recently released a new research study titled "Taiwan Data Center Market Size, Share, Trends and Forecast by Component, Type, Enterprise Size, End User, and Region, 2026-2034", offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends and competitive landscape to understand the current and Taiwan data center market scenarios.

Taiwan Data Center Market Size, Share, Trends, and Forecast 2026-2034

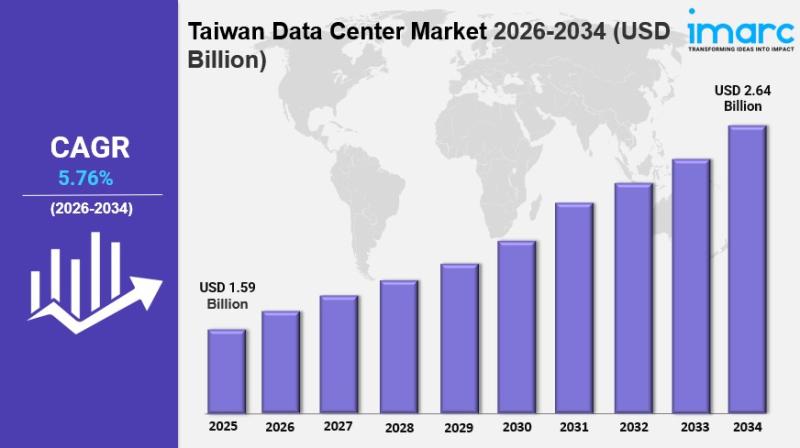

The Taiwan data center market is witnessing steady…

More Releases for Data

Data Catalog Market: Serving Data Consumers

Data Catalog Market size was valued at US$ 801.10 Mn. in 2022 and the total revenue is expected to grow at a CAGR of 23.2% from 2023 to 2029, reaching nearly US$ 3451.16 Mn.

Data Catalog Market Report Scope and Research Methodology

The Data Catalog Market is poised to reach a valuation of US$ 3451.16 million by 2029. A data catalog serves as an organized inventory of an organization's data assets, leveraging…

Big Data Security: Increasing Data Volume and Data Velocity

Big data security is a term used to describe the security of data that is too large or complex to be managed using traditional security methods. Big data security is a growing concern for organizations as the amount of data generated continues to increase. There are a number of challenges associated with securing big data, including the need to store and process data in a secure manner, the need to…

HOW TO TRANSFORM BIG DATA TO SMART DATA USING DATA ENGINEERING?

We are at the cross-roads of a universe that is composed of actors, entities and use-cases; along with the associated data relationships across zillions of business scenarios. Organizations must derive the most out of data, and modern AI platforms can help businesses in this direction. These help ideally turn Big Data into plug-and-play pieces of information that are being widely known as Smart Data.

Specialized components backed up by AI and…

Test Data Management (TDM) Market - test data profiling, test data planning, tes …

The report categorizes the global Test Data Management (TDM) market by top players/brands, region, type, end user, market status, competition landscape, market share, growth rate, future trends, market drivers, opportunities and challenges, sales channels and distributors.

This report studies the global market size of Test Data Management (TDM) in key regions like North America, Europe, Asia Pacific, Central & South America and Middle East & Africa, focuses on the consumption…

Data Prep Market Report 2018: Segmentation by Platform (Self-Service Data Prep, …

Global Data Prep market research report provides company profile for Alteryx, Inc. (U.S.), Informatica (U.S.), International Business Corporation (U.S.), TIBCO Software, Inc. (U.S.), Microsoft Corporation (U.S.), SAS Institute (U.S.), Datawatch Corporation (U.S.), Tableau Software, Inc. (U.S.) and Others.

This market study includes data about consumer perspective, comprehensive analysis, statistics, market share, company performances (Stocks), historical analysis 2012 to 2017, market forecast 2018 to 2025 in terms of volume, revenue, YOY…

Long Term Data Retention Solutions Market - The Increasing Demand For Big Data W …

Data retention is a technique to store the database of the organization for the future. An organization may retain data for several different reasons. One of the reasons is to act in accordance with state and federal regulations, i.e. information that may be considered old or irrelevant for internal use may need to be retained to comply with the laws of a particular jurisdiction or industry. Another reason is to…