Press release

Australia Private Equity Market 2026 | Worth USD 52.27 Billion by 2034

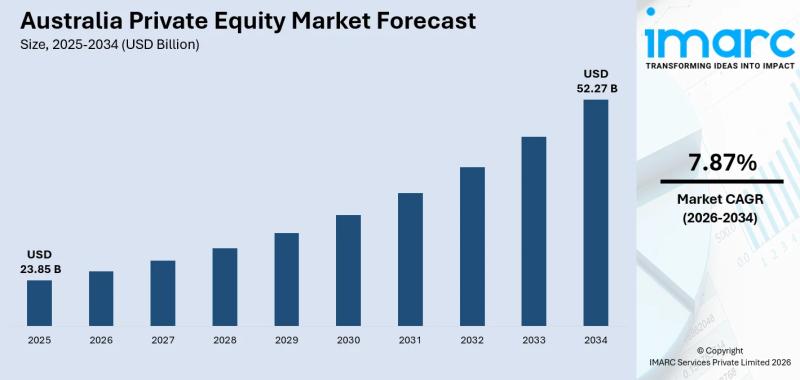

Australia's private equity market is entering a new growth phase, fueled by record deal activity in H1 2025, an estimated AUD $30 billion in dry powder ready for deployment, deepening superannuation fund engagement with alternative assets, and a maturing domestic GP ecosystem that is attracting increasing global investor interest. The Australia private equity market size reached USD 23.85 Billion in 2025. Looking forward, the market is expected to reach USD 52.27 Billion by 2034, exhibiting a growth rate (CAGR) of 7.87% during 2026-2034. The market encompasses buyout funds (44.7% share), venture capital, real estate, infrastructure, and other fund types, with capital deployed across healthcare, technology, industrials, consumer products, and renewable energy sectors. H1 2025 saw AUD $7.9 billion in completed deals (a 153% increase over the prior period), while Australia-focused private equity, venture capital, and private credit AUM reached a record $77.9 billion as of June 2025. The mandatory ACCC merger clearance regime from January 2026, increasing superannuation co-investment activity, and the evolution toward continuation vehicles and evergreen fund structures are among the key factors shaping market expansion.

Read more about Australia Private Equity Market

https://www.imarcgroup.com/australia-private-equity-market

Australia Private Equity Market Summary:

• H1 2025 delivered AUD $7.9 billion in completed private equity deals, representing a 153% increase over the prior period and signaling the strongest recovery in dealmaking since the post-pandemic rebound. Buyout activity saw both volume and value rise approximately 28% and 32% respectively over 2024, reaching USD $30.5 billion across 95 deals, with industrials capturing 45% of total deal value and technology contributing 15 completed transactions.

• Buyout funds dominate the market with a 44.7% share, reflecting the maturity of Australia's private equity ecosystem where mid-market and large-cap buyouts remain the primary capital deployment strategy. EQT's AUD $5.2 billion proposal for AUB Group represented the largest transaction, while public-to-private deals, partial acquisitions, earn-outs, and continuation vehicles are increasingly replacing traditional full buyouts as GPs exercise valuation discipline.

• Australian private capital assets under management reached $161 billion, with private equity and venture capital at $72 billion and a further $83 billion across real estate, infrastructure, and natural resources. Australia-focused PE, VC, and private credit AUM hit a record $77.9 billion as of June 2025, while participants raised $9 billion in fresh funds in the 12 months to December 2025 - up 6% on the prior year.

• An estimated AUD $30 billion in dry powder sits ready for deployment as of mid-2025, creating significant pressure on GPs to find attractive investment opportunities. As inflationary pressures subside and interest rates stabilize, PE firms are deploying this capital to capture undervalued assets, particularly in healthcare, technology, and renewable energy sectors where structural growth drivers support value creation.

• Superannuation funds with AUD $3.9+ trillion in total assets are deepening their engagement with private equity, with AustralianSuper plotting a significant private equity expansion in February 2026 and super funds increasingly seeking co-investment opportunities alongside major PE firms like BGH Capital on large ASX-listed company bids. Addressing structural impediments in super settings could unlock up to $54 billion in additional capital for startups and growth companies.

• The mandatory ACCC merger clearance regime took effect on January 1, 2026, moving Australia to a single mandatory, suspensory administrative system with the ACCC as first-instance decision-maker. This represents the most significant change to merger regulation in decades and is shifting PE dealmakers toward mid-market and bolt-on transactions less likely to attract regulatory scrutiny.

• Fundraising remains challenging, with 58% of Australian respondents reporting it is harder than a year ago (versus 48% globally). GPs are responding by expanding LP bases to include retail and offshore investors (58%), introducing continuation funds and evergreen structures (49%), and increasing transparency and reporting (52%) to meet institutional investor demands.

• ACT & New South Wales leads regional activity with 34.8% market share, reflecting Sydney's position as Australia's financial capital and the headquarters location of major PE firms including Macquarie Capital, Pacific Equity Partners, and BGH Capital, alongside the concentration of ASX-listed target companies and professional services advisors.

Request a Business Sample Report for Procurement & Investment Evaluation: https://www.imarcgroup.com/australia-private-equity-market/requestsample

Key Trends Shaping the Australia Private Equity Market:

• Buyout recovery and mid-market deal acceleration: After a subdued period following the 2022 peak, buyout activity staged a strong recovery with volume and value up 28% and 32% respectively, reaching USD $30.5 billion across 95 deals. Industrials dominated at 45% of deal value, while technology contributed 15 transactions in H1 2025 alone. The shift toward mid-market transactions, bolt-on acquisitions, and partial stakes reflects both valuation discipline and the new ACCC mandatory merger clearance regime from January 2026, which is steering PE dealmakers away from mega-deals toward less scrutinized transaction sizes.

• Superannuation capital deepening private equity engagement: Australia's $3.9+ trillion superannuation system is increasingly channeling capital into private equity, with AustralianSuper plotting a significant PE expansion in February 2026 and super funds actively seeking co-investment alongside firms like BGH Capital. The Australian Investment Council argues that reforming structural impediments - including ASIC's RG 97 fee disclosure and the Your Future Your Super performance test - could unlock up to $54 billion in additional capital for the private equity ecosystem.

• Deal structure evolution from traditional buyouts to flexible vehicles: The market is witnessing a fundamental shift in deal structures, with traditional full buyouts increasingly giving way to partial acquisitions, earn-outs, continuation vehicles, and public-to-private transactions. GPs are introducing evergreen fund structures (49% adoption) to provide permanent capital and address the fundraising challenge, while continuation funds allow managers to retain high-performing assets beyond traditional fund life cycles.

• Dry powder deployment pressure driving sector-focused investment: With an estimated AUD $30 billion in uncommitted capital and stabilizing macroeconomic conditions, PE firms face mounting pressure to deploy. Healthcare, technology, and renewable energy have emerged as the primary target sectors where structural growth drivers support the value creation required to generate acceptable returns. This sector-focused approach marks a shift from the opportunistic dealmaking that characterized earlier market cycles.

• Regulatory change reshaping deal strategy and execution: The mandatory ACCC merger clearance regime from January 2026 represents the most consequential regulatory change in Australian M&A in decades. ASIC's 2025-2026 Corporate Plan confirms increased surveillance of both retail and wholesale private funds, focusing on governance, valuation, liquidity, conflicts, fees, and distribution. These regulatory developments are driving PE firms toward greater transparency, more rigorous due diligence, and alternative deal structures that navigate the new approval landscape.

Market Growth Drivers:

Record Deal Activity, Dry Powder Deployment, and Buyout Recovery

Australia's private equity market is being driven by a powerful recovery in deal activity and significant capital available for deployment. H1 2025 delivered AUD $7.9 billion in completed deals - a 153% increase over the prior period - while full-year buyout activity saw volume and value rise 28% and 32% respectively to reach USD $30.5 billion across 95 deals. Industrials captured 45% of total deal value, with technology completing 15 transactions in H1 alone. The estimated AUD $30 billion in dry powder as of mid-2025 creates sustained pressure on GPs to find and execute attractive investments as pricing expectations reset and macroeconomic conditions stabilize. EQT's AUD $5.2 billion proposal for AUB Group demonstrated the appetite for large-scale transactions, while the broader market is shifting toward mid-market buyouts, bolt-on acquisitions, and sector-specific investment theses in healthcare, technology, and renewable energy. As interest rates stabilize and inflationary pressures ease, the conditions for value creation improve, supporting higher deal volumes and larger fund deployments. The evolution from purely opportunistic dealmaking toward sector-focused, thesis-driven investment strategies is producing more disciplined capital allocation that generates stronger returns and attracts additional institutional capital into the asset class.

Superannuation Capital Allocation and Institutional Co-Investment

Australia's $3.9+ trillion superannuation system represents the single most significant structural growth driver for the private equity market. With the system growing at approximately 12% annually and super funds increasingly seeking alternative asset exposure to meet return targets, the flow of institutional capital into private equity is accelerating. AustralianSuper's February 2026 announcement of a significant private equity expansion - managing over $49 billion and adding PE to direct investment options - signals the direction for the industry's largest allocators. Super funds are actively seeking co-investment opportunities alongside PE firms like BGH Capital on large ASX-listed company bids, reducing management fee drag while maintaining portfolio exposure. The Australian Investment Council has identified that reforming structural impediments, including ASIC's RG 97 fee disclosure rules and the Your Future Your Super performance test, could unlock up to $54 billion in additional capital for startups and growth companies. Australian private markets participants raised $9 billion in fresh funds in the year to December 2025, up 6% on the prior year, while Australia-focused PE, VC, and private credit AUM reached a record $77.9 billion. The combination of growing super fund allocations, increasing offshore investor interest, and the expansion of retail access to private markets through evergreen and continuation vehicle structures creates multiple capital formation pathways that support long-term market growth.

Fund Innovation, Regulatory Evolution, and Sector Diversification

The Australian private equity market is being reshaped by fund structure innovation and regulatory evolution that together expand the market's reach and sophistication. On the fund innovation front, 49% of GPs are introducing continuation funds and evergreen structures that provide permanent capital, address fundraising challenges, and allow managers to retain high-performing assets beyond traditional fund lifecycles. The expansion of LP bases to include retail and offshore investors (58% of GPs), combined with increased transparency and reporting (52%), is broadening the market's capital base. On the regulatory front, the mandatory ACCC merger clearance regime from January 2026 is the most consequential change to Australian M&A regulation in decades, shifting deal strategy toward mid-market transactions and bolt-on acquisitions that are less likely to trigger extended review. ASIC's 2025-2026 Corporate Plan confirms heightened surveillance of private funds across governance, valuation, liquidity, and fee dimensions, driving professionalization. Sector diversification is also expanding the market's opportunity set: beyond traditional industrials and consumer sectors, PE firms are increasingly targeting healthcare, technology (15 deals in H1 2025), renewable energy, and infrastructure - sectors where Australia's structural advantages and government policy support create compelling value creation opportunities. This combination of fund innovation, regulatory maturation, and sector expansion positions the market for sustained growth toward USD 52.27 billion by 2034.

Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Australia private equity market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on fund type and region.

By Fund Type:

• Buyout

• Venture Capital (VCs)

• Real Estate

• Infrastructure

• Others

By Region:

• Australia Capital Territory & New South Wales

• Victoria & Tasmania

• Queensland

• Northern Territory & Southern Australia

• Western Australia

Key Players:

The Australia private equity market features a competitive landscape that includes major global PE firms, established domestic managers, and emerging specialist funds. Pacific Equity Partners (PEP), founded in 1998, is widely regarded as the largest local private equity firm in Australia and New Zealand, specializing in buyouts across consumer products, healthcare, and industrial services. BGH Capital, founded in 2017 by Ben Gray, Robin Bishop, and Simon Harle, has quickly become one of Australia's most influential PE firms, specializing in control-oriented buyouts with notable investments in Navitas and Village Roadshow. Quadrant Private Equity focuses on mid-market buyouts and growth capital. Global giants Blackstone Group, KKR & Co., Bain Capital, Carlyle Group, and TPG Capital bring international capital and deal expertise. Other key players include Adamantem Capital, Archer Capital, Catalyst Investment Managers, Next Capital, Allegro Funds, Crescent Capital Partners, and Roc Partners. The market research report provides a comprehensive analysis of the competitive landscape including key player positioning, market structure, top winning strategies, competitive dashboards, and detailed company profiles.

Key Aspects Required for the Australia Private Equity Market:

• Buyout funds dominate with 44.7% share, with H1 2025 delivering AUD $7.9 billion in completed deals (153% increase). Industrials captured 45% of deal value, followed by technology (15 transactions) and healthcare. Total buyout activity reached USD $30.5 billion across 95 deals, up 28% in volume and 32% in value over 2024.

• An estimated AUD $30 billion in dry powder is available for deployment, creating GP pressure to execute as macroeconomic conditions stabilize. PE firms are targeting healthcare, technology, and renewable energy sectors where structural growth supports value creation, while mid-market and bolt-on transactions are gaining preference under the new ACCC merger regime.

• Australia-focused private equity, VC, and private credit AUM reached a record $77.9 billion as of June 2025, with total private capital AUM at $161 billion ($72 billion PE/VC, $83 billion real estate/infrastructure/natural resources). Fresh fundraising of $9 billion in the year to December 2025 was up 6% year-on-year.

• The $3.9+ trillion superannuation system is the most significant capital formation driver, with AustralianSuper expanding PE allocations and super funds seeking co-investment alongside firms like BGH Capital. Reforming structural impediments could unlock $54 billion in additional capital for startups and growth companies.

• Deal structures are evolving from traditional full buyouts toward partial acquisitions, earn-outs, continuation vehicles, public-to-private transactions, and evergreen fund structures (49% GP adoption). This flexibility reflects valuation discipline and addresses LP liquidity concerns while allowing managers to retain high-performing assets.

• The mandatory ACCC merger clearance regime from January 2026 is reshaping deal strategy, pushing PE dealmakers toward mid-market transactions less likely to attract extended regulatory review. ASIC's heightened surveillance of private funds across governance, valuation, liquidity, and fee dimensions is driving professionalization.

• Fundraising faces headwinds, with 58% of Australian GPs reporting increased difficulty (versus 48% global average). Responses include expanding LP bases to retail and offshore investors (58%), introducing continuation/evergreen structures (49%), and increasing transparency (52%).

• ACT & New South Wales leads with 34.8% regional share, reflecting Sydney's status as the financial capital with major PE firm headquarters (PEP, BGH Capital, Macquarie Capital), ASX-listed target company concentration, and the professional services ecosystem supporting transaction execution.

Recent News and Developments:

March 2026: Macquarie Capital completed an investment in Starcloud within the Aerospace and Defense industry, demonstrating continued deal activity across diverse sectors as PE firms deploy dry powder into growth opportunities.

February 2026: AustralianSuper announced plans for a significant private equity expansion, adding PE to direct investment options for its members, signaling the industry's largest super fund's deepening commitment to alternative asset allocation.

January 2026: Australia's mandatory ACCC merger clearance regime took effect, establishing a single mandatory, suspensory administrative system that represents the most significant change to merger regulation in decades and reshapes PE deal strategy toward mid-market transactions.

H1 2025: The Australian private equity market delivered AUD $7.9 billion in completed deals, representing a 153% increase over the prior period, with buyout volume and value up approximately 28% and 32% respectively to reach USD $30.5 billion across 95 deals, and industrials capturing 45% of total deal value.

2025: EQT submitted an AUD $5.2 billion proposal for AUB Group, representing one of the largest private equity transactions in the Australian market and highlighting the appetite of global PE firms for high-quality Australian assets.

2025: Australia-focused private equity, venture capital, and private credit assets under management hit a record $77.9 billion as of June 2025, while total private capital AUM reached $161 billion, reflecting the continued growth and institutional maturation of the Australian alternative assets ecosystem.

2025: ASIC's 2025-2026 Corporate Plan confirmed heightened surveillance of retail and wholesale private credit and equity funds, with focus areas including governance, valuation, liquidity, conflicts, fees, disclosure, and distribution practices.

2025: Australian private markets participants raised $9 billion in fresh funds in the 12 months to December 2025, up 6% on the prior year, as GPs expanded LP bases to include retail and offshore investors and introduced continuation funds and evergreen structures to address fundraising challenges.

Note: If you require any specific information not currently covered within the scope of the report, IMARC Group will provide it as part of customization.

Speak to an analyst:

https://www.imarcgroup.com/request?type=report&id=31707&flag=E

Contact Us

IMARC Group

134 N 4th St., Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel. No.: (D) +91 120 433 0800

United States: +1-201-971-6302

About Us

IMARC Group is a global management consulting firm that helps the world's most ambitious changemakers to create a lasting impact. The company provides a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Australia Private Equity Market 2026 | Worth USD 52.27 Billion by 2034 here

News-ID: 4495197 • Views: …

More Releases from IMARC Group

Carbon Fiber Manufacturing Plant Project Report 2026: ROI, IRR, CapEx/OpEx and P …

As global demand for lightweight, high-strength materials accelerates across aerospace, automotive, wind energy and construction, the carbon fiber manufacturing plant cost has become a critical data point for investors evaluating entry into this high-growth composites sector. IMARC Group's newly released Detailed Project Report (DPR), titled "Carbon Fiber Manufacturing Plant Project Report 2026: Industry Trends, Plant Setup, Machinery, Raw Materials, Investment Opportunities, Cost and Revenue" provides a complete roadmap for entrepreneurs…

United States Real Estate Market Size to Reach USD 2.30 Trillion by 2034 | CAGR …

IMARC Group has recently released a new research study titled "United States Real Estate Market Size, Share, Trends and Forecast by Property, Business, Mode, and Region, 2026-2034", offers a detailed analysis of the market drivers, segmentation, growth opportunities, trends and competitive landscape to understand the current and future market scenarios.

United States Real Estate Market Size and Forecast 2026-2034

The United States real estate market size was valued at USD 1.76 Trillion…

Waste Management Plant Project Report 2026: Business Plan, Setup Cost, Raw Mater …

Setting up a waste management plant positions investors in an essential, recession-resilient segment of the environmental services value chain, backed by consistent demand from municipal corporations, industrial waste generators, and environmental service providers. As urbanization accelerates and regulatory pressure around waste disposal and recycling intensifies, the global waste management industry continues to present dependable opportunities for operators and entrepreneurs seeking long-term stability in an essential-services sector.

IMARC Group's Detailed Project Report…

BESS Manufacturing Plant Project Report 2026: Business Plan, Setup Cost Analysis …

Setting up a Battery Energy Storage System (BESS) manufacturing plant positions investors at the center of one of the fastest-growing segments of the global energy transition, backed by rising demand for renewable energy integration, grid stabilization, and the rapid expansion of electric vehicles (EVs). Battery energy storage systems play a crucial role in enabling efficient storage and dispatch of energy, helping to smooth out the intermittent nature of renewable energy…

More Releases for Australia

Derila Memory foam pillow Australia: Honest Reviews About Derila Australia

Derila is one of the best memory foam pillows sold in Australia today.

Priced at around 30 dollars (USD), derila is currently the most reviewed and the cheapest memory pillow available in Australia.

What is Derila? Is Derila Pillow the best in Australia? Keep reading to discover everything worth knowing about Derila Australia.

OVERVIEW

Recently, Memory foam pillow has been trending and there is a lot of brands to choose from. Which one is…

CeraCare Australia - Where to Buy Legit CeraCare Supplement in Australia?

CeraCare Australia - Ceracare is a glucose support supplement that proposes to augment cardiovascular prosperity and to stay aware of perfect glucose assimilation in Australia. CeraCare supplement is conceptualized and executed by a threesome – Christine, Dr. Jihn and Michael. It is a natural supplement that helps one stay aware of ideal glucose levels, cardiovascular prosperity, and glucose assimilation.

Take Advantage of 80% Discount Offer in Australia >> https://boostsxproaustralia.com/ceracare-new

The indications…

Glucofort Australia - Where to Buy Legit Glucofort Supplement in Australia?

Glucofort Australia - Glucofort is an efficient, all-natural progressive glucose support supplement in Australia. This formula is made out of 12 key ingredients, 7 nutrients, and minerals, and a little of Vanadium. This supplement upholds regulated glucose levels and glucose digestion. Glucofort prides itself as the most inventive supplements available in Oceania, accentuating its solidarity, wellbeing, and quality.

Take Advantage of 75% Discount Offer in Australia >> https://boostsxproaustralia.com/glucofort-new

Rather than simply…

Australia Agriculture Market, Australia Agriculture Industry, Australia Agricult …

Australia Agriculture has been as vital within the development of Australia, because it was within the United States. Australia's ancient dominance in wheat and sheep continues into the 21st century. Recently Australian agriculture has become more and more diversified. The considerable expanses of productive land have helped Australia to become a number one world exporter of grains, meats, and wool. Each grains (predominantly wheat and barley) and wool markets round…

Australia Conveyor Maintenance Analysis by Top Companies Habasit Australia Pty l …

Global Australia Conveyor Maintenance Market and Competitive Analysis

Know your current market situation! Not only a vital element for brand new products but also for current products given the ever-changing market dynamics. The study allows marketers to remain involved with current consumer trends and segments where they'll face a rapid market share drop. Discover who you actually compete against within the marketplace, with Market Share Analysis know market position, to push…

Australia Conveyor Maintenance Market Analysis By Manufacturers Rema Tip Top Aus …

A conveyor system is a common piece of mechanical handling device that moves materials/objects from one location. A conveyor is often lifeline to a company’s ability to effectively move its products in a timely manner. While it is used constantly in a manufacturing plant, proper maintenance from trained technicians can extend the lifespan of conveyor. Furthermore, conveyor maintenance is essential as it may be subjected to different types of failures…