Press release

Commercial Vehicles Market Heads Toward USD 1.2 Trillion by 2033 as Electrification, Tariff Shifts, and Digital Fleets Redefine the Industry's Next Decade

Commercial Vehicles Market

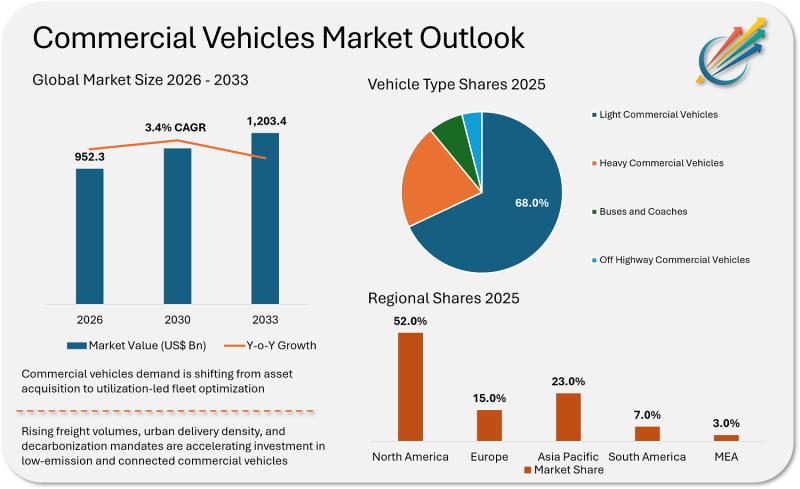

According to a new comprehensive market report published by Market Minds Advisory, the global commercial vehicles market was valued at USD 921.0 billion in 2025 and is projected to reach USD 1,203.4 billion by 2033, expanding at a steady CAGR of 3.4% over the forecast period. Beneath that headline number lies a far more dynamic and differentiated story.

Request a Sample Report to Explore Key Market Insights: https://marketmindsadvisory.com/request-sample/?report_id=29480

The Industry Is Not Transitioning - It Is Splitting

The most important thing to understand about the commercial vehicles industry right now is that there is no single market anymore. There are at least three markets running in parallel, each with its own economics, regulatory clock, and technology bet.

Light commercial vehicles - urban delivery vans, cargo vans, compact pickup trucks - have already crossed the total cost of ownership threshold for electrification in many urban zones. High utilization rates, predictable routes, and return-to-base operations make electric LCVs the most commercially rational transition underway. This segment is forecast to account for more than 68% of electric commercial vehicle sales globally, and the numbers are accelerating as Amazon, IKEA, and major last-mile logistics operators embed low-carbon asset requirements into their procurement mandates.

Heavy-duty long-haul trucks are a different matter entirely. Here, the industry is in the middle of a genuine propulsion debate - battery electric versus hydrogen fuel cell versus hydrogen internal combustion. OEMs like Cummins and PACCAR are not picking a single winner. They are developing fuel-agnostic engine platforms capable of running on diesel, natural gas, or hydrogen with minimal component changes. That is not indecision - that is a rational hedge in a market where regulatory timelines and infrastructure availability remain genuinely uncertain.

Buses and coaches are being pulled forward by municipal mandates rather than pure economics. Electric city bus penetration has already passed 50% in key markets, and intercity coaches are emerging as the next frontier for hydrogen adoption. This segment is arguably the most policy-driven of the three, and in many ways the most predictable for long-term planning.

Tariffs, Nearshoring, and the New North American Equation

The commercial vehicles market cannot be read without understanding what U.S. trade policy has done to its cost structure. In late 2025, President Trump imposed a 25% tariff on imported medium and heavy-duty trucks and components, accompanied by a 3.75% production offset credit extended through 2030 for domestically assembled vehicles. The stated goal - securing critical supply chains and boosting domestic manufacturing - is already reshaping where trucks are built, sourced, and serviced.

The USMCA trade framework is emerging as an important pressure valve. Mexico is rapidly becoming the preferred manufacturing hub for North American heavy trucking, as OEMs seek to navigate the tariff environment while maintaining cost competitiveness. For supply chain strategists, nearshoring is no longer a trend to monitor - it is a capital deployment decision with a hard timeline.

North America currently holds 52% of the global commercial vehicles market share, driven by regulatory clarity following the EPA's 2024 updated heavy-duty emissions standards and ongoing infrastructure incentives. But this dominance is being tested. California's ACT and ACF rules are creating a "border effect" where fleets actively optimize their domicile locations to navigate a patchwork of state-level mandates - a complexity that adds operational cost and procurement risk simultaneously.

Get a Custom Research Report with Region or Company-Specific Data: https://marketmindsadvisory.com/request-customization/?report_id=29480

The Ownership Model Is Changing - And That Changes Everything

One of the most underreported shifts in the commercial vehicles market is happening not in the powertrain - but in the balance sheet. Fleet purchase still dominates volume, but leasing and pay-per-use models are gaining meaningful ground, and the reason is structural rather than cyclical.

Electric and software-heavy vehicles carry 30-70% higher upfront costs compared to their diesel equivalents. For smaller operators and companies with seasonal demand patterns, that capital intensity is prohibitive. Leasing solves the problem - it offers predictable monthly costs, easier technology refresh cycles, and keeps balance sheets lighter at a time when higher interest rates are already extending fleet renewal timelines across the industry.

This shift in ownership economics is creating a significant white space opportunity: integrated solutions that bundle vehicles, charging infrastructure, fleet software, and maintenance under a single contract. The operators who can offer this - and price it compellingly - are not just selling trucks. They are selling certainty in an uncertain market. That is a fundamentally different and more defensible value proposition.

The Competitive Landscape: Consolidation at the Top, Disruption at the Edges

The heavy-duty commercial vehicles market is dominated by a concentrated group of global OEMs - Daimler Truck, Volvo Group, PACCAR, and Traton (Volkswagen Group) - whose competitive strategies have evolved in a revealing direction. Rather than competing head-to-head on R&D for every new technology, these players are partnering on shared infrastructure (Milence for charging networks) and fuel cell development (cellcentric) while differentiating on software platforms, data monetization, and service contracts.

This signals something important: the future margin battleground in commercial vehicles is not the engine. It is the software and data layer. OEMs that fail to build recurring revenue from connected fleet services risk being reduced to hardware manufacturers - a commodity position with structurally compressed margins.

Meanwhile, the retrofit and repowering segment is emerging as one of the most overlooked near-term opportunities in the market. As diesel bans approach in urban zones across Europe and North America, a substantial and growing market is forming around converting existing diesel chassis to zero-emission powertrains - bypassing the high capital expenditure of new vehicle purchases entirely. Circular battery programs and remanufacturing are gaining traction alongside this trend as residual value uncertainty on early-generation EVs rises.

Read the Complete Research Report: https://marketmindsadvisory.com/commercial-vehicles-market/

What Decision-Makers Need to Act On - Right Now

The commercial vehicle market growth trajectory is clear, but the path is bifurcated. The organizations that will win are those that make deliberate technology and partnership bets in the next 12-24 months rather than waiting for the market to stabilize - because it will not stabilize before the competitive positions are set.

For fleet operators: the pre-buy window for current-generation diesel trucks is open through 2026. After 2027, EPA Phase 3 compliance vehicles will carry higher price points and technical uncertainties. Act now, but plan the EV transition in parallel.

For OEMs and suppliers: the software monetization question is existential. Becoming a hardware foundry for tech-layer players is the worst possible outcome. Platform strategy, data ownership, and service contract economics need to be board-level priorities today.

For investors: the commercial vehicles market is not a monolithic growth story - it is a portfolio of sub-markets with very different risk and return profiles. LCVs offer the earliest electrification returns. Heavy-duty trucks offer the largest eventual prize but require patience. Retrofit, software, and charging infrastructure represent the asymmetric upside plays with the shortest time to revenue.

Contact Us

Market Minds Advisory

86 Great Portland Street, Mayfair, London,

W1W 7FG, England, United Kingdom

T: +44 020 3807 7725

Email:sales@marketmindsadvisory.com

Website:https://marketmindsadvisory.com/

LinkedIn: https://www.linkedin.com/company/market-minds-advisory/

Facebook: https://www.facebook.com/resvaultmmadvisory/

Twitter: https://x.com/MarketMindsA

Instagram: https://www.instagram.com/marketmindsadvisory

Why choose Market Minds Advisory

Market Minds Advisory delivers decision-grade intelligence trusted by executives across machinery & equipment, packaging, chemical, automotive, information & communication technology, food & beverage, consumer goods, healthcare and other industries. We provide market expansion strategies, go-to-market strategies, market share acceleration, brand positioning analysis, and account enablement and growth. Our forecasting methodology integrates primary interviews, proprietary demand models and continuous market validation to ensure accuracy in volatile and emerging industries. With over 10 years of industry experience and insights derived from primary interviews with several industry stakeholders, our research provides actionable insights and white space analysis for the emerging segments providing the opportunity gaps in the market accounting recent market developments and geopolitical risks. We believe in unlocking growth by helping businesses to see the future of their markets.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Commercial Vehicles Market Heads Toward USD 1.2 Trillion by 2033 as Electrification, Tariff Shifts, and Digital Fleets Redefine the Industry's Next Decade here

News-ID: 4485706 • Views: …

More Releases from Market Minds Advisory

Deep Sea Mining Market Surges on Critical Mineral Demand | USD 16.3 billion Grow …

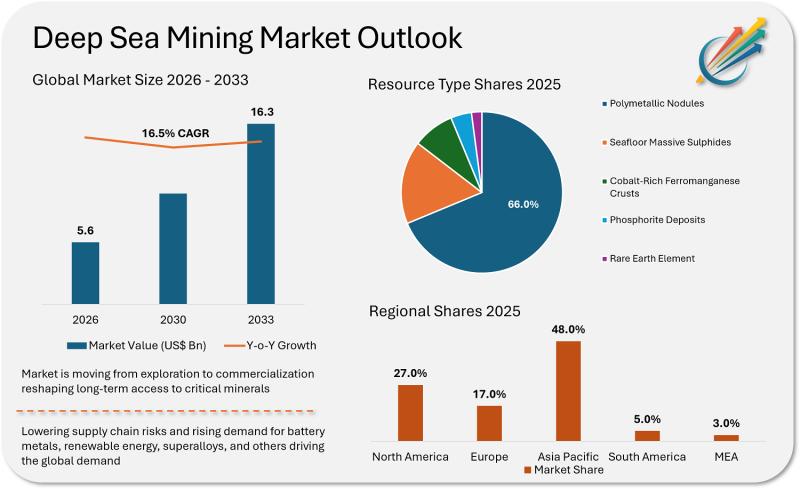

The global deep sea mining market is no longer a distant frontier concept it is rapidly becoming one of the most strategically consequential industrial sectors of the decade. According to a new comprehensive market report published by Market Minds Advisory, the global deep sea mining market is valued at USD 5.6 billion in 2026 and is projected to reach USD 16.3 billion by 2033, expanding at a robust CAGR of…

Advanced Composites Are No Longer a Specialty Play | They Are Becoming the New I …

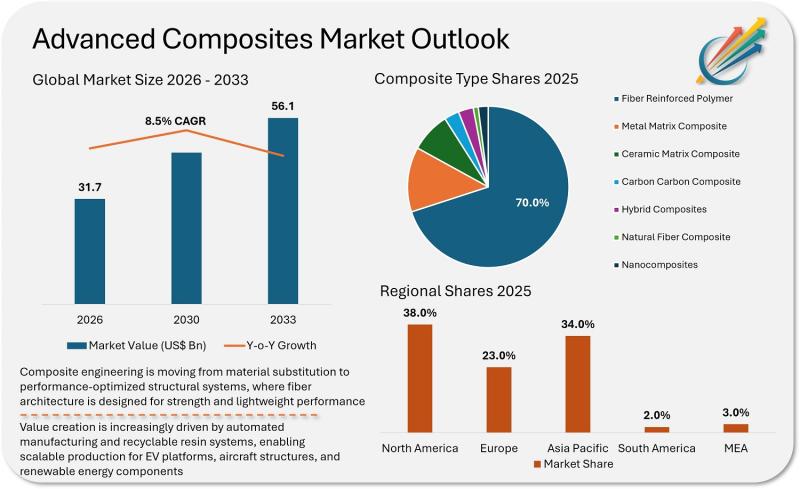

There is a pattern that repeats in every industrial transition: the companies that move early define the cost structure and supply chain relationships, while those who wait end up buying access at a premium. Advanced composites are now in that inflection window.

What is often overlooked is that this is not a materials science story anymore. It is a competitive positioning story. The aerospace OEMs that have normalized carbon fiber in…

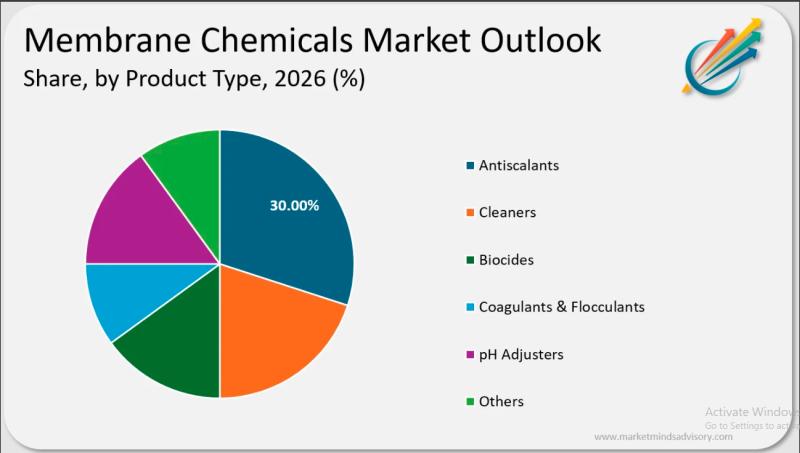

Membrane Chemicals Market to Reach USD 4.7 Billion by 2033, Driven by 7.5% CAGR

Membrane Chemicals Market Overview

The membrane chemicals market, currently valued at USD 2.8 billion in 2026, is positioned for robust expansion, with projections indicating a rise to USD 4.7 billion by 2033. This growth trajectory is underpinned by heightened demand for efficient water and wastewater treatment solutions, notably within power generation, pharmaceuticals, food & beverage, and municipal utilities. The adoption of membrane technologies such as reverse osmosis, ultrafiltration, and nanofiltration continues…

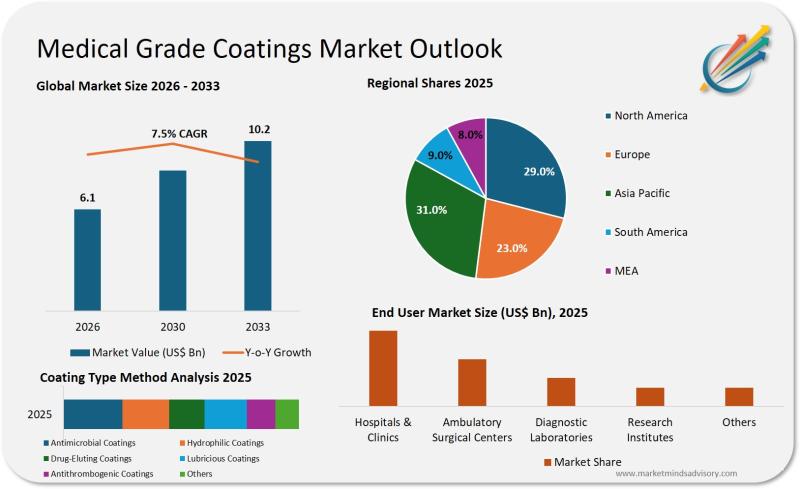

Medical Grade Coatings Market to Reach USD 10.2 Billion by 2033, Driven by 7.5% …

Medical Grade Coatings Market Overview

The medical grade coatings market is positioned at a pivotal intersection of healthcare innovation and material science. As of 2026, the sector is valued at USD 6.1 billion, reflecting robust demand from medical device manufacturers, pharmaceutical packaging, and surgical instrument producers. The market is experiencing a pronounced shift toward biocompatible, antimicrobial, and hydrophilic coatings, which are essential for enhancing device safety, longevity, and patient outcomes. Regulatory…

More Releases for OEMs

Autolink Makes European Debut in Munich, Empowering OEMs' Intelligent Vehicle Up …

On September 8, IAA Mobility 2025 officially opened in Munich, Germany. Autolink made its European debut at Booth C13, Hall A2, showcasing its full-domain solutions, including intelligent cockpit domain controllers, integrated domain controllers, and in-vehicle display systems. The company aims to support European automakers in upgrading electronic architectures and enhancing intelligent cockpit experiences.

Video: https://www.youtube.com/embed/qTkUgNxc7IQ

Video Link: https://www.youtube.com/embed/qTkUgNxc7IQ

Image: https://www.globalnewslines.com/uploads/2025/09/2264d19787cacbfcfc9bde46a98aaf6e.jpg

Europe's automotive market is undergoing a critical transformation, moving from traditional distributed electronic systems…

Automotive Original Equipment Manufacturer (OEMS) Market - Industry Trends and F …

The Automotive Original Equipment Manufacturer (OEMS) market document offers a thorough examination of the imminent challenges in terms of sales, export/import, and revenue within the market. The analysis delves into market drivers, including factors such as consumer demand and governmental policies, acting as catalysts for consumer purchases, thereby fostering market growth and advancement. This business report not only provides insights into the market and competitive landscape but also serves as…

Emerging Avenues for OEMs Drive Automotive Data Monetization Market Growth

According to a new market research report launched by Inkwood Research, the Global Automotive Data Monetization Market is estimated to progress with a CAGR of 34.48% in terms of revenue, reaching a revenue of $552460.21 million by 2030.

Browse 44 Market Data Tables and 43 Figures spread over 150 Pages, along with an in-depth analysis of the Global Automotive Data Monetization Market by Model, Deployment, Application, & Geography.

Refer to the Report…

Emerging Avenues for OEMs Drive Automotive Data Monetization Market Growth

According to a new market research report launched by Inkwood Research, the Global Automotive Data Monetization Market is estimated to progress with a CAGR of 34.48% in terms of revenue, reaching a revenue of $552460.21 million by 2030.

Browse 44 Market Data Tables and 43 Figures spread over 150 Pages, along with an in-depth analysis of the Global Automotive Data Monetization Market by Model, Deployment, Application, & Geography.

Refer to the Report…

Autonomous Heavy Truck Market Global Solution Providers, Demands, Layout of Chin …

Autonomous heavy truck market research: front runners first going public

Our Autonomous Heavy Truck Industry Report, 2020-2021 carries out research into highway scenario-oriented autonomous heavy truck industry, including OEMs and autonomous driving solution providers inside and outside China.

Several autonomous heavy truck companies try to list their shares for financing.

The surging road freight volume and a widening gap in demand for truck drivers, promote the financing boom of self-driving heavy truck industry,…

Hybrid Additive Manufacturing Machines Market: Rising Awareness among OEMs

The global hybrid additive manufacturing machines market is prophesied in a report by Transparency Market Research (TMR) to find players putting high emphasis on development of new products to boost their brand positioning. This could be evident with the launch of LUMEX Avance-25 by Matsuura Machinery Corporation in 2016. Introduction of new products could also help players to outshine their competitors in the market. Stratasys Ltd., Mazak Corporation, and DMG…