Press release

Packaging at Scale: Why Institutional Capital Is Rotating into the Global Cans Supply Chain

Between 2025 and 2032, capital allocation is increasingly directed toward high-speed production lines, lightweighting technologies, and regional capacity localization, particularly across Asia-Pacific. With an average selling price (ASP) of approximately USD 0.12 per unit and global sales volume reaching 594,441 million units, margin expansion is no longer achieved through scale alone but through operational precision. Gross margins across leading manufacturers are stabilizing around 26%, reflecting improved cost pass-through mechanisms and higher utilization rates.

This structural shift is particularly relevant for institutional investors, as the industry begins to resemble a hybrid between a commodity materials sector and an advanced manufacturing platform where return on invested capital (ROIC) is increasingly linked to technological sophistication and regional supply chain positioning.

Global Overview

The global cans market is valued at USD 65,933 million in 2025, projected to reach USD 97,535 million by 2032, reflecting a CAGR of 5.8%. This growth trajectory is supported by stable end-market demand combined with incremental pricing power in premium packaging segments.

Core demand drivers include the continued global shift toward aluminum beverage packaging due to recyclability advantages, rising consumption of ready-to-drink (RTD) beverages and processed foods in emerging markets, regulatory pressure favoring sustainable packaging formats over plastics, and expanding demand in aerosol and industrial applications requiring durable metal containment.

Regional Consumption Dynamics (APAC & SEA)

Asia-Pacific represents the fastest-growing consumption hub, driven by urbanization, income growth, and localized manufacturing expansion. Southeast Asia in particular is transitioning into a high-growth demand cluster.

Indonesia is experiencing strong growth in canned beverage consumption, supported by expanding middle-class purchasing power and domestic bottling investments. Malaysia and Thailand are leveraging their established food processing industries to increase exports of canned goods, particularly seafood and ready meals. Vietnam is emerging as a manufacturing and export hub for both beverage and food cans, benefiting from trade agreements and foreign direct investment inflows. Singapore, while smaller in volume, plays a strategic role as a regional logistics and innovation center, hosting high-value packaging R&D and distribution operations.

Large-scale capacity build-outs across APAC are increasingly supported by sovereign industrial policies aimed at strengthening domestic packaging ecosystems and reducing reliance on imports, particularly in aluminum sheet and tinplate supply.

Production and Supply Chain

Value capture within the cans industry is concentrated in upstream material processing (aluminum rolling and steel treatment) and midstream high-speed manufacturing. Downstream branding and filling operations, while critical, capture relatively lower margins compared to integrated can producers with advanced production capabilities.

Gross margins across the industry average around 26%, with leading players achieving slightly higher margins through vertical integration and proprietary manufacturing technologies. Cost of goods sold is heavily influenced by raw material inputs primarily aluminum and steel which account for approximately 60 to 70% of total production costs.

Asia-Pacific has become the backbone of global supply, with China dominating aluminum and steel substrate production, while Southeast Asia is increasingly important for final can manufacturing. Indonesia and Vietnam are attracting new investments in canning facilities due to competitive labor costs and proximity to high-growth consumer markets. Thailand and Malaysia serve as export-oriented production bases with established supply chain ecosystems.

Latest Technological Developments

Recent technological advancements are reshaping production efficiency and product performance. AI-driven telemetry systems are now deployed across production lines to optimize throughput and predictive maintenance, reducing downtime and improving yield rates. Lightweighting technologies in aluminum cans are lowering material usage per unit while maintaining structural integrity, directly improving margins.

Advanced internal coatings are being developed to enhance product compatibility and extend shelf life, particularly for acidic beverages and food products. Digital twin modeling is increasingly used to simulate production scenarios and optimize line configurations before capital deployment. High-speed canning lines now exceed 3,000 units per minute in leading facilities, significantly increasing output per line. Additionally, closed-loop recycling systems are being integrated into production ecosystems, reducing raw material dependency and aligning with ESG mandates.

Market Breakdown Categories

Material

Product Category

Structural

Capacity

Coating

Aluminum Cans

Beverage

Two Piece Can

Standard(250ml,330ml / 355ml)

Epoxy Based

Tinplate Cans

Food

Three Piece Can

Slim and Sleek (200-250ml)

BPA Free

TFS and ECCS Steel Cans

Consumer Aerosol

Large Format ( 473-500ml)

Industrual and Technical

The market is segmented across multiple technical and commercial dimensions. By material type, aluminum cans dominate due to their lightweight properties and recyclability, while tinplate cans remain essential for food preservation, and TFS/ECCS steel cans offer cost advantages in industrial applications.

Product categories are divided into beverage cans, which represent the largest share driven by carbonated drinks and beer; food cans, including preserved vegetables, seafood, and ready meals; consumer aerosol cans used in personal care and household products; and industrial and technical cans designed for chemicals and lubricants.

From a structural perspective, two-piece cans are widely used in beverage applications due to their seamless design and high-speed manufacturability, while three-piece cans are more common in food and specialty packaging due to their flexibility in size and shape.

Capacity segmentation reflects both consumption patterns and filling-line compatibility. Standard beverage cans (e.g., 250ml, 330ml, 355ml) dominate high-speed production environments due to global standardization. Slim and sleek cans (200ml250ml) are gaining share in premium beverage categories such as energy drinks and RTDs, offering higher ASP realization. Large-format cans (473ml500ml) are prevalent in North America and increasingly adopted in APAC urban markets.

Additional segmentation includes coating type (epoxy-based, BPA-free alternatives), printing technology (digital vs. offset), and end-use channel (retail, foodservice, industrial supply).

Product Pricing Variations

Pricing varies significantly depending on material composition, size, coating, and application.

In aluminum beverage cans, standard 330ml cans produced by Ball Corporation are typically priced between USD 0.10 to 0.14 per unit, reflecting high production efficiency and global scale. Premium slim cans manufactured by Crown Holdings range from USD 0.13 to 0.18 per unit, driven by branding and specialty design requirements. Specialty printed cans from Ardagh Metal Packaging can reach USD 0.18 to 0.22 per unit due to advanced decoration technologies.

For tinplate food cans, standard formats produced by Silgan Holdings are priced between USD 0.12 to 0.20 per unit, depending on size and coating requirements. High-durability cans for acidic foods manufactured by Can-Pack Group can reach USD 0.20 to 0.28 per unit due to specialized linings.

In aerosol cans, products from Mauser Packaging Solutions typically range from USD 0.15 to 0.25 per unit, while high-pressure industrial cans from Toyo Seikan Group can exceed USD 0.30 per unit due to reinforced structures and compliance requirements.

Global Top 30 Key Companies in the Cans Market

Ball Corporation (Colorado, USA)

Crown Holdings (Pennsylvania, USA)

Ardagh Metal Packaging (Luxembourg)

Can-Pack Group (Kraków, Poland)

Silgan Holdings (Connecticut, USA)

Toyo Seikan Group (Tokyo, Japan)

CPMC Holdings (Hong Kong, China)

Baosteel Packaging (Shanghai, China)

ORG Technology (Zhejiang, China)

ShengXing Group (Fujian, China)

Showa Aluminum Can Corporation (Tokyo, Japan)

Daiwa Can Company (Tokyo, Japan)

Universal Can Corporation (Tokyo, Japan)

Kian Joo Can Factory (Selangor, Malaysia)

Can-One Berhad (Kuala Lumpur, Malaysia)

Thai Beverage Can (Bangkok, Thailand)

Kingcan Holdings (China)

Great China Metal Industry (Taipei, Taiwan)

Massilly Group (Mâcon, France)

Envases Universales (Monterrey, Mexico)

Nampak (Johannesburg, South Africa)

Colep Packaging (Vale de Cambra, Portugal)

Mauser Packaging Solutions (Illinois, USA)

Hub Packaging Group (Öhringen, Germany)

Allstate Can Corporation (Ohio, USA)

Hindustan Tin Works (New Delhi, India)

EXAL Corporation (Ohio, USA)

Ceylon Can Company (Colombo, Sri Lanka)

Alucon Public Company (Bangkok, Thailand)

Grupa Kęty - Alupol Packaging (Kęty, Poland)

Chapter Outline

Chapter 1: Introduces the report scope of the report, executive summary of different market segments (by region, product type, application, etc), including the market size of each market segment, future development potential, and so on. It offers a high-level view of the current state of the market and its likely evolution in the short to mid-term, and long term.

Chapter 2: key insights, key emerging trends, etc.

Chapter 3: Manufacturers competitive analysis, detailed analysis of the product manufacturers competitive landscape, price, sales and revenue market share, latest development plan, merger, and acquisition information, etc.

Chapter 4: Provides profiles of key players, introducing the basic situation of the main companies in the market in detail, including product sales, revenue, price, gross margin, product introduction, recent development, etc.

Chapter 5 & 6: Sales, revenue of the product in regional level and country level. It provides a quantitative analysis of the market size and development potential of each region and its main countries and introduces the market development, future development prospects, market space, and market size of each country in the world.

Chapter 7: Provides the analysis of various market segments by Type, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different market segments.

Chapter 8: Provides the analysis of various market segments by Application, covering the market size and development potential of each market segment, to help readers find the blue ocean market in different downstream markets.

Chapter 9: Analysis of industrial chain, including the upstream and downstream of the industry.

Chapter 10: The main points and conclusions of the report.

Related Report Recommendation

Global Cans Market Research Report 2026

https://www.qyresearch.com/reports/6019250/cans

Global Cans Sales Market Report, Competitive Analysis and Regional Opportunities 2026-2032

https://www.qyresearch.com/reports/6482486/cans

Global Cans Market Outlook, InDepth Analysis & Forecast to 2032

https://www.qyresearch.com/reports/6482487/cans

Cans- Global Market Share and Ranking, Overall Sales and Demand Forecast 2026-2032

https://www.qyresearch.com/reports/6482488/cans

Global DWI Can Market Research Report 2026

https://www.qyresearch.com/reports/6464637/dwi-can

Global Bio Cans Market Research Report 2026

https://www.qyresearch.com/reports/6535798/bio-cans

Global Slim Can Market Research Report 2026

https://www.qyresearch.com/reports/5692990/slim-can

Global Paint Can Market Research Report 2026

https://www.qyresearch.com/reports/6550102/paint-can

Global Beer Cans Market Research Report 2026

https://www.qyresearch.com/reports/6014139/beer-cans

Global Drink Can Market Research Report 2026

https://www.qyresearch.com/reports/6517160/drink-can

About QY Research

QY Research has established close partnerships with over 71,000 global leading players. With more than 20,000 industry experts worldwide, we maintain a strong global network to efficiently gather insights and raw data.

Our 36-step verification system ensures the reliability and quality of our data. With over 2 million reports, we have become the world's largest market report vendor. Our global database spans more than 2,000 sources and covers data from most countries, including import and export details.

We have partners in over 160 countries, providing comprehensive coverage of both sales and research networks. A 90% client return rate and long-term cooperation with key partners demonstrate the high level of service and quality QY Research delivers.

More than 30 IPOs and over 5,000 global media outlets and major corporations have used our data, solidifying QY Research as a global leader in data supply. We are committed to delivering services that exceed both client and societal expectations.

Contact Information:

Tel: +1 626 2952 442 (US) ; +86-1082945717 (China)

+62 896 3769 3166 (Whatsapp)

Email: willyanto@qyresearch.com; global@qyresearch.com

Website: www.qyresearch.com

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Packaging at Scale: Why Institutional Capital Is Rotating into the Global Cans Supply Chain here

News-ID: 4484476 • Views: …

More Releases from QY Research

Top 30 Indonesian Fan Public Companies Q3 2025 Revenue & Performance

1) Overall companies performance (Q3 2025 snapshot)

PT Astra International Tbk

PT Chandra Asri Pacific Tbk

PT United Tractors Tbk

PT Barito Pacific Tbk

PT AKR Corporindo Tbk

PT Indocement Tunggal Prakarsa Tbk

PT Semen Indonesia (Persero) Tbk

PT Solusi Bangun Indonesia Tbk

PT Wijaya Karya Beton Tbk

PT Waskita Beton Precast Tbk

PT Voksel Electric Tbk

PT KMI Wire and Cable Tbk

PT Supreme Cable Manufacturing & Commerce Tbk

PT Sat Nusapersada…

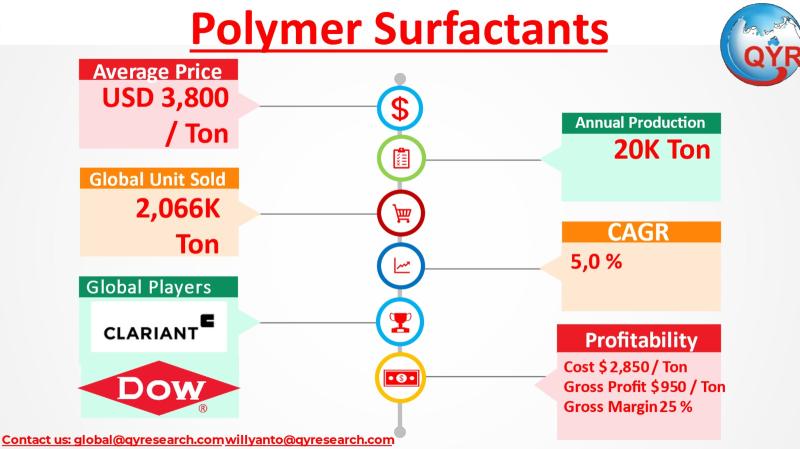

Polymer Surfactants: Margin Expansion, APAC Capacity Build-Outs, and the Next Ph …

The global polymer surfactants market is entering a non-linear value inflection phase, driven by a transition from volume-based commoditized supply toward performance-engineered, application-specific materials. Historically anchored in bulk emulsification and dispersion use cases, the sector is increasingly defined by high-value formulations in personal care, enhanced oil recovery (EOR), and advanced coatings. This shift is compressing the relevance of low-cost producers while elevating capital intensity, technical formulation capability, and downstream integration…

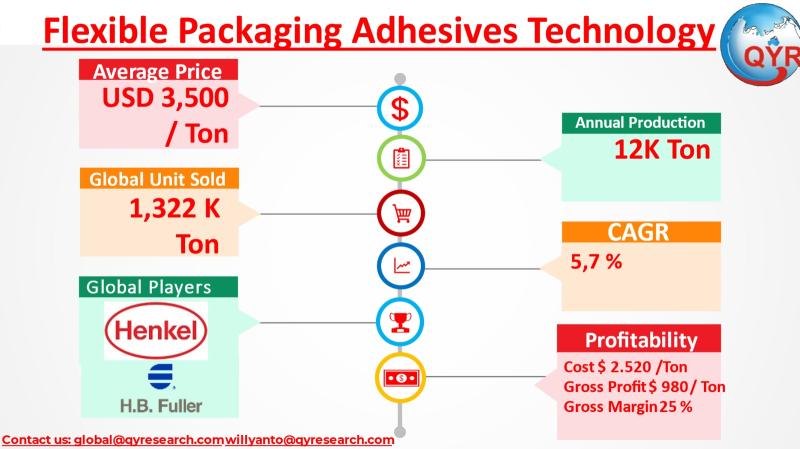

Flexible Packaging Adhesives A Quiet Re-rating Driven by Sustainability and High …

The global Flexible Packaging Adhesives Technology market is entering a non-linear value inflection phase, transitioning from a historically volume-driven business toward a capital-intensive, technology-led model. While demand growth remains steady, the underlying shift is being driven by regulatory tightening (particularly on solvent emissions), increased barrier performance requirements in food and pharmaceutical packaging, and the rising complexity of multilayer laminates. These factors are structurally increasing formulation sophistication, plant capex intensity, and…

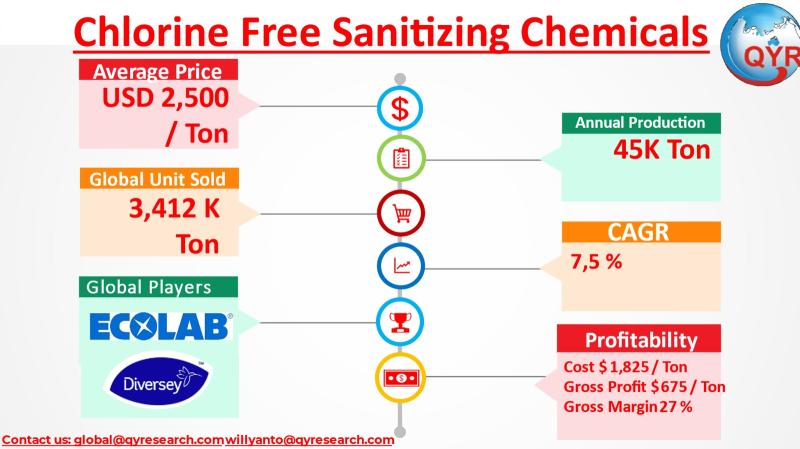

Margin Discipline and Capacity Scale: The 7.5% CAGR Story Behind Next-Gen Saniti …

The Chlorine-Free Sanitizing Chemicals market is entering a non-linear value inflection characterized by a decisive shift from commoditized volume supply to capital-intensive, formulation-driven production. Historically, the market relied on low-cost chlorine derivatives with minimal differentiation. However, tightening environmental compliance, occupational safety standards, and residue-free sanitation requirements particularly in food and healthcare are accelerating the transition toward peroxide, peracetic acid, and bio-based chemistries. This transition structurally increases capital requirements, as production…

More Releases for Packaging

Personalized Packaging Market 2019 By Key Players: Owens Illinois, Salazar Packa …

Personalized Packaging Market research report delivers a close watch on leading competitors with strategic analysis, micro and macro market trend and scenarios, pricing analysis and a holistic overview of the market situations in the forecast period.

Download PDF Sample of this Report @

http://www.supplydemandmarketresearch.com/home/contact/277379?ref=Sample-and-Brochure&toccode=SDMRCH277379&utm_source=S2

The following manufacturers are covered:

Owens Illinois

Salazar Packaging

Design Packaging

PrimeLine Packaging

International Packaging

Elegant Packaging

Pak Factory

ABOX Packaging

ACG Ecopak

CB Group

SoOPAK Company

Huhtamaki…

E-Commerce Packaging Market by Top Key Players - Pioneer Packaging, Arihant pack …

E-commerce packaging involves the use of materials for safe packaging of products sold by the e-commerce industry. E-commerce packaging plays a vital role in the consumers' perception about the e-retailer. It also indicates the perceived value of the item received. Packaging reflects the value of shipment in the e-commerce supply chain, that is, better the packaging, better the product inside it.

Get Sample Copy of this Report @ https://www.bigmarketresearch.com/request-sample/2904563

The E-Commerce…

Luxury Packaging Market 2019 SWOT Analysis By Top Key Players; MW Luxury Packagi …

Luxury Packaging Market report provides an in-depth overview of product specification, technology, product type and production analysis considering major factors such as revenue, cost, gross and gross margin. The company profiles of all the key players and brands that are dominating the Luxury Packaging Market with moves like product launches, joint ventures, merges and accusations which in turn is affecting the sales, import, export, revenue and CAGR values are mentioned…

Global Luxury Packaging Market 2019 Top Key Players: MW Luxury Packaging, Progre …

Summary

WiseGuyReports.com adds “Luxury Packaging Market 2019 Global Analysis, Growth, Trends and Opportunities Research Report Forecasting to 2024” reports to its database.

This report provides in depth study of “Luxury Packaging Market” using SWOT analysis i.e. Strength, Weakness, Opportunities and Threat to the organization. The Luxury Packaging Market report also provides an in-depth survey of key players in the market which is based on the various objectives of an organization such as…

Top Manufacturer in Luxury Packaging Market 2019: MW Luxury Packaging, Progress …

Luxury packaging is used for packaging and decorating high-end products.An increase in the luxury product consumption rate and the number of product launches in the fashion and cosmetic sectors are some major factors driving the market growth.

The global Luxury Packaging market is valued at xx million US$ in 2018 and will reach xx million US$ by the end of 2025, growing at a CAGR of xx% during 2019-2025. The objectives…

Personalized Packaging Market 2025 | Design Packaging, Inc., PrimeLine Packaging …

As per the new market report published by Research Report Insights titled ‘Personalized Packaging Market’: Global Industry Analysis and Forecast 2017-2025’, global personalized packaging market attained a value worth US$ 25,577.9 Mn in 2017 and will possibly thrive at a promising CAGR of 5.1% over the forecast period (2017-2025). The global personalized packaging market has witnessed solid growth during the past few decades, owing to the increasing trend of luxury…