Press release

Photonics Electronics Convergence Technology Market to Reach USD 130.65 Billion by 2033 as AI Data Center Bandwidth Demand and Silicon Photonics Scale-Up Redefine High-Speed Computing

photonics-electronics convergence technology Market

Request Exclusive Sample: https://www.datamintelligence.com/download-sample/photonics-electronics-convergence-technology-market?kailas

Commercially, this is a market where value is migrating from standalone optics toward deeper integration between photonic and electronic functions at chip, package, rack, and system level. The practical driver is simple: AI clusters are scaling faster than electrical interconnect efficiency. Cisco's February 2026 launch of its 102.4 Tbps Silicon One G300 platform, built for large AI clusters and paired with high-density optics, and STMicroelectronics' March 2026 move into high-volume production of its PIC100 silicon photonics platform for 800G and 1.6T transceivers show that the industry is shifting from lab validation to manufacturing scale. Ayar Labs' March 2026 funding round and rack-scale partnership announcements further underline that capital is now backing deployable optical I/O architectures, not just concept technology.

DMI Analyst Opinion

The market is being shaped by a single disruption. The thermal and power boundaries of traditional chip interconnections are being pushed to their limit by the underlying AI infrastructure. The real opportunity is not necessarily faster communication alone, but a complete redesign of the compute layer around photonics that dramatically lowers heat, latency and power loss inside hyper-scale and edge use cases. The market will shift from component innovation to system redesign where photonics drives data center economics. Winners will be those companies that can address packaging and integration needs and not simply deliver individual improvements in photonic performance.

Recent Developments

1. In March 2026, STMicroelectronics announced it had entered high-volume production for its PIC100 silicon photonics platform, targeting optical interconnects for hyperscale data centers and AI clusters. The significance is that 800G and 1.6T photonic transceivers are moving into commercial manufacturing, which supports faster market adoption and lowers execution risk for system builders.

2. In February 2026, Cisco Systems launched the Silicon One G300, a 102.4 Tbps switching silicon platform for AI data center buildouts. Cisco said the associated systems support high-density optics and can improve energy efficiency by nearly 70% in certain designs, reinforcing how tightly photonics-electronics integration is now tied to AI infrastructure economics.

3. In March 2026, Ayar Labs closed a US$500 million Series E round, bringing its total funding to US$870 million and valuation to US$3.75 billion. The proceeds are being used to scale production and test capacity for co-packaged optics, a strong signal that investors see optical I/O as a near-term infrastructure category rather than a distant platform bet.

4. Also in March 2026, Ayar Labs and Wiwynn announced a strategic partnership to develop rack-scale AI systems using co-packaged optics. This matters because market momentum is shifting from component-level innovation toward system-level deployment, where manufacturability, thermal design, fiber management, and hyperscale integration determine real revenue capture.

Segment Analysis

By component, Photonics Integrated Circuits (PICs) are emerging as the commercial center of gravity. Even where share data is not publicly broken out, PICs sit at the point where bandwidth density, power efficiency, and form factor improvements are monetized. They enable the replacement of longer electrical paths with optical data movement inside or around the package, which is exactly where AI clusters and high-speed switching platforms now face their most expensive scaling constraints. The push into 800G and 1.6T interconnects, together with co-packaged optical I/O, makes PICs the segment with the strongest pricing power and the deepest strategic importance.

By material, silicon photonics remains the most commercially advantaged segment because it aligns optical performance with semiconductor manufacturing scale. ST's volume production on 300 mm lines and Intel's long-standing silicon photonics manufacturing base show why silicon remains the preferred route for data center and AI interconnect applications. Intel has already shipped over 8 million PICs and more than 32 million integrated on-chip lasers, while ST is now commercializing silicon photonics for hyperscaler-class links. In business terms, silicon photonics offers the best path to scaling yield, cost structure, and ecosystem compatibility simultaneously.

Market Segmentation

The market is segmented by component into photonics integrated circuits, electronics integrated circuits, optical interconnects, transceivers, and other enabling elements. By material, it spans silicon photonics, indium phosphide, gallium arsenide, lithium niobate, and other specialty platforms selected according to performance, wavelength, and integration requirements. By end-user, demand is distributed across IT and telecom, consumer electronics, healthcare, automotive and mobility, military and defense, industrial, and adjacent applications. Geographically, the market covers North America, South America, Europe, Asia-Pacific, and the Middle East and Africa, though near-term commercialization remains most concentrated in North America and Asia-Pacific because that is where hyperscale compute, semiconductor manufacturing, and optical network investment are deepest.

Regional Analysis

The United States is the clearest commercialization leader because the strongest near-term demand is tied to AI infrastructure, cloud networking, and semiconductor supply chain localization. As a directional policy indicator, the CHIPS and Science Act provided US$50 billion to strengthen U.S. semiconductor research, development, and manufacturing. That does not represent the photonics-electronics convergence market directly, but it is a meaningful structural tailwind because photonic interconnects are increasingly embedded in the same advanced compute and packaging ecosystem being expanded under CHIPS. On the corporate side, U.S.-based Intel, Cisco, and Ayar Labs are all actively advancing optical I/O, switching silicon, and co-packaged optics programs, which reinforces the country's role as the largest early revenue pool.

Japan is strategically important both as a technology originator and as a policy-backed scaling market. A directional indicator is Japan's FY2023 semiconductor budget of 1.85 trillion yen, which included 645.6 billion yen for Post-5G R&D, alongside explicit support for next-generation semiconductor and photonics-electronics convergence programs. METI has also highlighted optical wiring and photonics-electronics convergence in servers as necessary responses to rising power consumption in high-speed data transmission. On the corporate side, NTT's IOWN Technology Report, published in January 2026, explicitly positions Photonics-Electronics Convergence as part of next-generation data center architecture. That combination of industrial policy and domestic platform development gives Japan outsized strategic influence even when like-for-like national market sizing is not publicly disclosed.

Purchase Exclusive Copy of this Report: https://www.datamintelligence.com/buy-now-page?report=photonics-electronics-convergence-technology-market?kailas

Company Profiles

Intel Corporation

Intel Corporation remains one of the market's most consequential companies because it combines silicon photonics know-how with CPU and data center platform reach. Intel reported 2024 revenue of US$53.1 billion, and in June 2024 it demonstrated what it described as the industry's first fully integrated optical compute interconnect chiplet, co-packaged with an Intel CPU. The company matters because it can industrialize photonics-electronics convergence at the processor and packaging layer, which is where future AI cluster bottlenecks are most acute.

Cisco Systems

Cisco Systems is critical from the networking and switching side of the market. Cisco reported FY2025 revenue of US$56.7 billion, and management said AI infrastructure orders from webscale customers in fiscal 2025 were more than double its original target. Its February 2026 Silicon One G300 launch shows how optical density, switch performance, cooling, and network management are converging into a single competitive stack for AI infrastructure.

STMicroelectronics

STMicroelectronics brings manufacturing relevance that many photonics stories still lack. The company reported FY2025 net revenues of US$11.80 billion, and in March 2026 it entered high-volume production for its PIC100 silicon photonics platform aimed at hyperscaler optical interconnect applications. ST matters because it is one of the clearest examples of silicon photonics moving from development into repeatable industrial production.

Ayar Labs

Ayar Labs is smaller in revenue terms than the diversified incumbents, but strategically it punches above its weight. In March 2026 it raised US$500 million, taking total funding to US$870 million, and followed that with a rack-scale AI partnership with Wiwynn. The company matters because it is focused directly on the optical I/O and co-packaged optics problem that sits at the heart of this market's next growth wave.

Analyst View

The strongest revenue pools in this market are likely to form where optical and electronic integration solves an immediate cost-per-bit and watts-per-bit problem, especially in AI data centers, scale-up server architectures, optical interconnect modules, and high-bandwidth switching platforms. The most attractive segments are therefore PICs, silicon photonics materials, optical interconnects, and IT and telecom end-use, because these categories sit closest to urgent deployment budgets rather than exploratory R&D.

Competition is also changing shape. It is no longer just a race between component vendors. It is becoming a contest between ecosystem builders that can connect materials, chip design, advanced packaging, optical engines, thermal management, and system software into a commercially deployable stack. That raises the bar for winners. The companies best placed to capture value will be those that can prove manufacturability at 800G and 1.6T, shorten qualification cycles with hyperscalers, and deliver measurable energy savings at cluster scale. In other words, the commercial winners will not simply make better optics. They will make optics-electronics convergence easier to buy, integrate, and scale.

Contact:

Fabian

DataM Intelligence 4market Research LLP

6th Floor, M2 Tech Hub, DataM Intelligence 4market Research LLP, Lalitha Nagar, Habsiguda, Secunderabad, Hyderabad, Telangana 500039

USA: +1 877-441-4866

UK: +44 161-870-5507

Email: fabian@datamintelligence.com

About DataM Intelligence

DataM Intelligence is a renowned provider of market research, delivering deep insights through pricing analysis, market share breakdowns, and competitive intelligence. The company specializes in strategic reports that guide businesses in high-growth sectors such as nutraceuticals and AI-driven health innovations.

To find out more, visit https://www.datamintelligence.com/ or follow us on Twitter, LinkedIn and Facebook.

This release was published on openPR.

Permanent link to this press release:

Copy

Please set a link in the press area of your homepage to this press release on openPR. openPR disclaims liability for any content contained in this release.

You can edit or delete your press release Photonics Electronics Convergence Technology Market to Reach USD 130.65 Billion by 2033 as AI Data Center Bandwidth Demand and Silicon Photonics Scale-Up Redefine High-Speed Computing here

News-ID: 4484344 • Views: …

More Releases from DataM intelligence 4 Market Research LLP

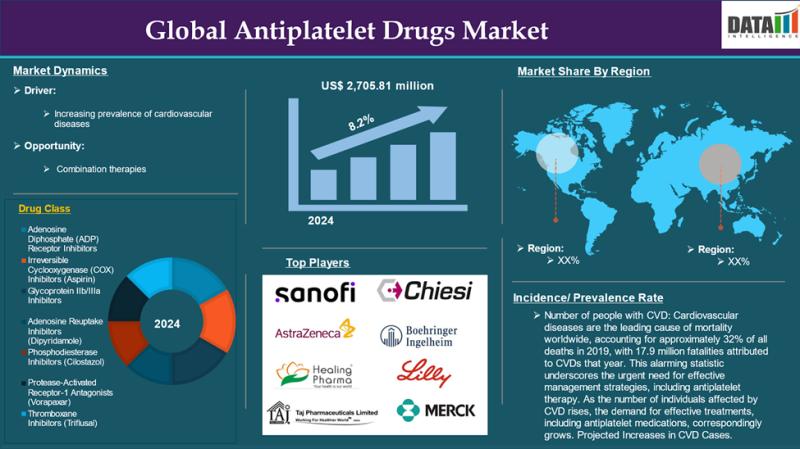

United States Antiplatelet Drugs Market 2026 | Growth Drivers, Trends & Market F …

Market Size and Growth 2026

The Global Antiplatelet Drugs Market reached US$ 2,705.81 million in 2024 and is expected to reach US$ 5.056.03 million by 2032, growing at a CAGR of 8.2% during the forecast period 2025-2032.

DataM Intelligence has released a new research report titled Antiplatelet Drugs Market Size 2026 The report delivers in-depth insights into key market dynamics, including regional growth trends, market segmentation, CAGR projections, and the revenue performance…

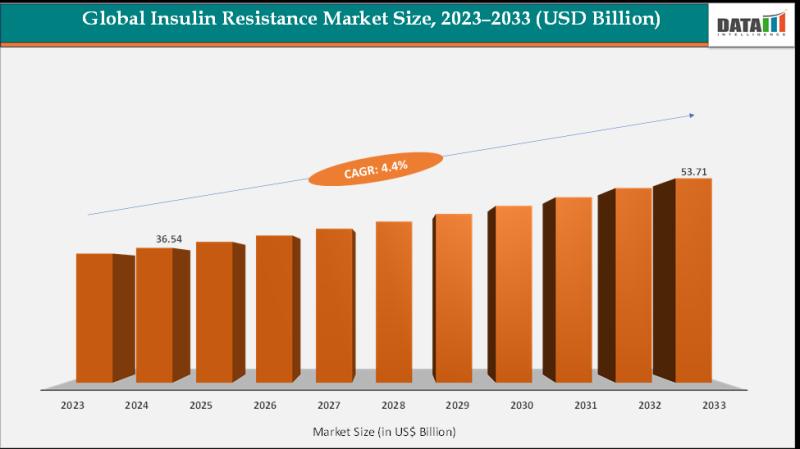

United States Insulin Resistance Market 2026 | Growth Drivers, Trends & Market F …

Market Size and Growth 2026

The Global Insulin Resistance Market Size Reached US$ 36.54 Billion in 2024 from US$ 35.12 Billion in 2023 and is expected to reach US$ 53.71 Billion by 2033, growing at a CAGR of 4.4% during the forecast period 2025-2033.

DataM Intelligence has released a new research report titled Insulin Resistance Market Size 2026 The report delivers in-depth insights into key market dynamics, including regional growth trends,…

Global Chromium Market Outlook 2026: Supply Chain Restructuring, Ferrochrome Dem …

Market Size and Growth 2026

Global Chromium Market reached US$ 23.36 billion in 2024 and is expected to reach US$ 36.61 billion by 2032, growing with a CAGR of 5.78% during the forecast period 202-2033.

DataM Intelligence has released a new research report titled Chromium Market Size 2026 The report delivers in-depth insights into key market dynamics, including regional growth trends, market segmentation, CAGR projections, and the revenue performance of leading…

Spinal Muscular Atrophy Market to Reach $20.06 Billion by 2033 | Gene Therapy Br …

Market Size and Growth 2026

Spinal Muscular Atrophy Market size reached US$ 4.40 Billion in 2024 and is expected to reach US$ 20.06 Billion by 2033, growing at a CAGR of 16.5% during the forecast period 2026-2033.

DataM Intelligence has released a new research report titled Spinal Muscular Atrophy Market Size 2026 The report delivers in-depth insights into key market dynamics, including regional growth trends, market segmentation, CAGR projections, and the revenue…

More Releases for Intel

Vision Processing Unit Market Is Booming Rapidly with Strong Demand By 2033 | In …

Coherent Market Insights has added a new research study on the Global "Vision Processing Unit Market" 2026 by Size, Growth, Trends, and Dynamics, Forecast to 2033 which is a result of an extensive examination of the market patterns. This report covers a comprehensive investigation of the information that influences the market regarding fabricates, business providers, market players, and clients. The report provides data about the aspects which drive the expansion…

Global Slim Laptop Market By Type (Intel I3, Intel I5 Low Power Version, Sharp D …

The Global Slim Laptop Market 2020 report implement in-depth research of the industry with a focus on the current market trends future prospects. The Global Slim Laptop Market report aims to provide an overview of Slim Laptop Market players with detailed market segmentation by product, application and geographical region. It also provides market share and size, revenue forecast, growth opportunity. The most recent trending report Worldwide Slim Laptop Market Economy…

Wearable Computer Market Global Forecast 2018| Studied By LG, ,Honeywell, Epson, …

UpMarketResearch published an exclusive report on “Wearable Computer market” delivering key insights and providing a competitive advantage to clients through a detailed report. The report contains 115 pages which highly exhibits on current market analysis scenario, upcoming as well as future opportunities, revenue growth, pricing and profitability. This report focuses on the Wearable Computer market, especially in North America, Europe and Asia-Pacific, South America, Middle East and Africa.…

Smart Grid Security Market - Competitive Analysis | Cisco Systems, Inc., Intel C …

The global market for smart grid security is highly influenced by the rise in the population and the rapid pace of urbanization in emerging economies. The main factor behind this is increasing shift of energy resources companies to smart meters and smart appliances by leveraging Internet of Things (IoT) and cloud, owing to the augmenting pressure on them to meet the ever-increasing energy requirements of the urban population. With this,…

Intel Labs launches the Intel Collaborative Research Institute for Computational …

22 May, 2012

—While computer performance exceeds human performance in many respects, there are still many tasks that humans perform easily and computers have a hard time with. Intel, in collaboration with the Technion–Israel Institute of Technology and the Hebrew University of Jerusalem, hopes to change this situation by exploring technologies that mimic the human brain's mode of action—

Intel today announced it is establishing the Intel Collaborative Research institute for…

Intel Distributes ESET Security Software With Intel® Desktop Boards

ESET Validates Market Strength as Industry-Leading AV Solution

Dubai, United Arab Emirates, September 23, 2009 – ESET, the leader in proactive threat protection, announced today that Intel will distribute ESET security software products with Intel-branded desktop motherboards starting in Q1 2010. As a result of the distribution agreement, Intel Desktop Boards will include either a 45-day or one-year product license for ESET Smart Security.

ESET will ship exclusively with new Intel®…